Sample Category Title

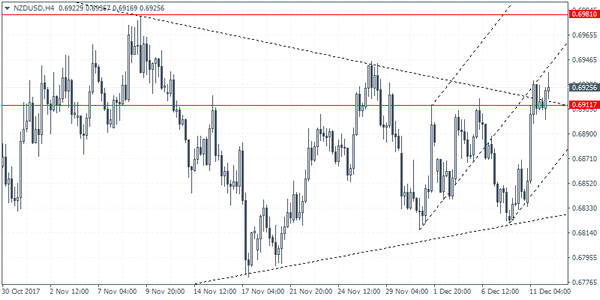

NZDUSD Intraday Analysis

NZDUSD (0.6925): The NZDUSD currency pair closed bullish yesterday as price action is looking to maintain the bullish momentum. Following the consolidation off the triangle pattern formed near the bottom, NZDUSD is seen attempting to breakout to the upside. Short term resistance at 0.6911 remains key and a bullish close above this level could signal further gains. On the 4-hour chart, price action is biased to the upside. Short term consolidation near 0.6911 could remain in play. The next resistance level is identified near the 0.6981 level which could be breached if the kiwi dollar maintains the bullish momentum.

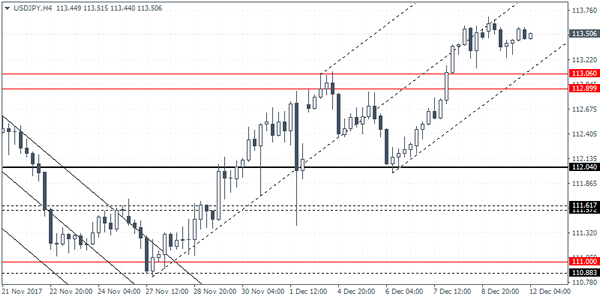

USDJPY Intraday Analysis

USDJPY (113.50): The USDJPY attempted to post further gains but with price action closing with a doji candlestick pattern on the daily chart, we expect the rally to stall in the short term. The downside bias is increasing as a retest of the support level area near 113.06 - 112.90. This remains as the most likely price level that could be tested for support. Further gains can be expected after USDJPY will establish support at this level. In the event that the support level fails, we could expect to see further declines that could push USDJPY lower towards 112.04 support.

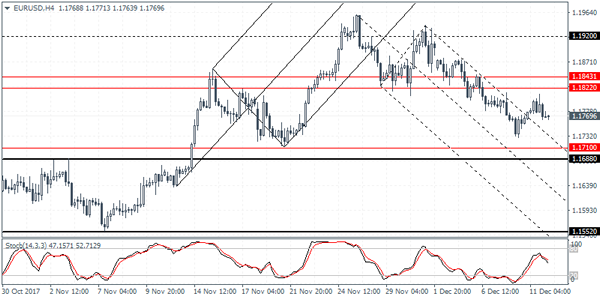

EURUSD Intraday Analysis

EURUSD (1.1769): The EURUSD was trading flat although intraday volatility picked up. Price action spiked to a two-day high, but the gains were short lived. We expect that the sideways price action will continue in the short term. As long as EURUSD remains supported above the 1.1704 support level, the bias remains to the upside. On the 4-hour chart, EURUSD will need to post a higher low in order for price to test the resistance level area near 1.1843 - 1.1822 region. Establishing resistance at this level will signal a short term retracement. However, we expect to see price action resume its decline on a reversal near the resistance level.

GBP Looks To Inflation Data For November

The U.S. dollar was seen consolidating on Monday ahead of the two-day FOMC meeting that starts today. The lack of economic data kept the greenback in check as investors await tomorrow’s FOMC rate hike decision. The Kiwi dollar was seen posting strong gains on Monday after the appointment of the new RBNZ Governor, Adrian Orr.

Looking ahead, the economic data today will include the UK's inflation report for November. According to the median forecasts, inflation in the UK is expected to have risen at a steady pace of 3.0% in November. Core inflation rate is also expected to be steady at 2.7%. This comes after the BoE's rate hike in early November.

In the U.S. the producer price index data is expected to show a 0.4% increase, rising at the same pace as the month before. Core PPI is expected to slow, rising just 0.2% down from 0.4% increase previously. The ECB president Mario Draghi is expected to speak later this evening.

EUR/GBP Rebounds In The Established Trading Range Despite Brexit Deal

Asian equities lost momentum on Tuesday despite U.S. stocks ending at record highs on Monday. Traders shrugged off a Manhattan Subway explosion, in what was called a terrorist attack, but trading volumes were low ahead of the final round of central bank meetings for 2017. Energy stocks are outperforming other sectors, as Brent crude climbed to its highest level since June 2015, on the shutdown of the Forties North Sea pipeline. Brent traded above $65.70 and widened the spread with WTI to $7.21, a level last seen in August 2015. Such a reaction indicates that supply disruptions can no longer be ignored in tight markets.

In currency markets, traders are on stand-by. The dollar is moving in very narrow ranges ahead of the Fed's monetary policy decision on Wednesday. A 25-basis points rate hike is completely priced in the dollar, so traders should take their signals from different catalysts. Chair Janet Yellen's tone, economic projections, and the dot plot, are what's going to drive the dollar for the remainder of 2017. Given that we're getting closer to a deal on tax reforms, the Fed might become slightly more hawkish and ignore the stubbornly low wage growth. Whether this will lift the central bank's growth projections and the dot plot, remain to be seen, but chances are high.

Having successfully moved into phase 2 of Brexit talks, the focus will shift back to economic data in the U.K. Today's November CPI will likely be a market moving indicator for Sterling. A rise above 3% in inflation requires Mark Carney to write a letter to the chancellor explaining why inflation is above its 2% target. I think chances of U.K. CPI exceeding expectations are high, given the surge in oil prices. This will likely provide short-term support for the GBPUSD as traders will begin projecting another interest rate hike early 2018.

After surging to a new all-time high on Monday, Bitcoin fell below $16,000 today, before recovering some of its losses. The CBOE's bitcoin futures launched on Monday, proved to be more volatile than the original asset itself, although futures contracts are meant to tame volatility. The fear of short sellers attacking the bitcoin didn't arise yesterday, indicating that the cryptocurrency isn't seen yet as the big short. However, what scares me now is that people are taking out mortgages in order to buy bitcoins according to U.S. securities regulator, and this is not a good sign.

Currencies: USD On Consolidation Modus Ahead Of Tomorrow’s Fed Meeting

Sunrise Market Commentary

- Rates: Inconclusive, low-volume trading as higher oil prices are ignored

A surge in oil prices has limited impact on other markets so far. Ahead of tomorrow's Fed meeting and Thursday's ECB meeting, we expect more inconclusive, low-volume trading. Today's US PPI could spark some intraday volatility, but probably without technical consequences. The German 10-yr yield is still testing 0.3% support. - Currencies: USD on consolidation modus ahead of tomorrow's Fed meeting

The dollar found a bottom yesterday as selling after Friday's soft US wage data petered out. Today's eco calendar is modestly interesting. However, the data will probably only be of intraday significance for USD trading as investors look forward to tomorrow's Fed decision. Sterling traders keep an eye at the UK CPI and the voting on the Brexit bill.

The Sunrise Headlines

- US stock markets closed 0.25% to 0.5% higher yesterday with energy shares taking the lead on surging oil prices. Overnight, Asian risk sentiment deteriorates as we head to the closing bell (-0.5%).

- International Trade Secretary Fox said the UK would like a trading relationship with the EU after it leaves the bloc that's “virtually identical” to the one it has now.

- The effects of a hairline crack in one of the world's most important oil conduits is rippling through markets. The Forties Pipeline is being shut after the fault was discovered, pushing Brent over $65/b for the 1st time since June 2015.

- The EU, Japan and the US are set to announce a new alliance to take on China more aggressively over trade issues such as overcapacity in steel and forced technology transfers..

- The rapid growth the Trump administration is banking on in its budget will deliver around $1.8tn of extra tax revenue, the US Treasury said, as it aims to validate previous claims that tax cuts can pay for themselves.

- China will continue its neutral monetary policy with a bias toward tightening next year, according to a front-page commentary in Securities Times.

- Today's eco calendar contain UK inflation data, US NFIB Small Business Optimism and US PPI data. Germany holds a 2-yr Schatz auction and the US Treasury sells 30-yr bonds

Currencies: USD On Consolidation Modus Ahead Of Tomorrow's Fed Meeting

USD on consolidation modus ahead of Fed

There was little news to guide USD trading yesterday. The dollar stayed slightly in the defensive after Friday's soft US wage data. EUR/USD tried to regain the 1.18 barrier, but the attempt failed. The dollar found a bottom later in the session, supported by a slight intraday rise in US yields and ongoing positive equity sentiment. USD/JPY closed the session at 113.56 (from 113.48). EUR/USD finished the day at 1.1769, little changed from Friday.

Asian equities opened mixed, but lost gradually ground as the trading session proceeded. There is no obvious driver for trading this morning. Oil extends its recent rebound, with Brent trading at the highest level in 2 ½ years. For now there are little spill-off effects on other markets. The trade-weighted dollar holds near the highest level in two weeks. USD/JPY stabilizes in the mid 113 area, despite softer equities. EUR/USD holds in the 1.1775 area. Business confidence and house price data in Australia were soft, but caused no further sustained losses of the Aussie dollar. AUD/USD holds near recent lows in the 0.7500/50 area. The kiwi dollar tries to extend yesterday's rebound after the nomination of a new RBNZ governor (NZD/USD currently 0.6930).

The eco calendar is moderately interest today with German ZEW investor confidence, US NFIB small business confidence and US PPI data. ZEW investor confidence is expected to ease slightly, but to stay at very lofty levels, especially for the current conditions component. NFIB US small business confidence is expected to improve slightly from 103.8 to 104, a historically high level. US headline PPI is expected to rise 0.3% M/M and 2.9% Y/Y (from 2.8%). A positive PPI surprise might cause some nervousness ahead of tomorrow's US CPI data and Fed policy decision/statement. It might also be marginally positive for the dollar. However, we don't expect traders/investor to adapt positions in a profound way on the PPI release, just one day before the Fed. We expect more technically driven sideways USD trading. Yesterday's USD price action might be an indication that the downside is rather well protected. Further progress on a US tax bill further support this. Evidently, tomorrow's Fed policy decision/guidance holds the clue for the next directional move of the dollar. We assume that the Fed will stick to a scenario of 3 additional rate hikes next year, which should be good for USD

From a technical point of view: EUR/USD set a post-ECB low mid-November, but the dollar's momentum wasn't strong enough. EUR/USD settled in a directionless sideways consolidation pattern in the 1.17/19 area. A return below 1.1713 would signal an improvement in the ST USD momentum. The payrolls were unable to force this break. EUR/USD still gives no clear directional signal. Next support comes in at 1.1554 (November low). USD/JPY's momentum deteriorated early November, dropping below the 111.65 neckline. No aggressive follow-through selling occurred though. Over the previous two weeks, the pair succeeded a nice rebound, calling off the downside alert and returning to the 110.84/114.73 consolidation range. We amended our ST bias from negative to neutral. We maintain the view that a sustained break north of 115 won't be easy.

EUR/USD in consolidation modus ahead of tomorrow's Fed meeting

EUR/GBP

Will UK CPI exceed 3.0%?

Sterling continued the slide that started after Friday's press conference of EC Juncker and UK PM May on a ‘separation deal'. The agreement clearly was far away from a detailed, legally binding text. A commission spokesman called it a gentlemen's agreement. Several hot topics were avoided last week in order to be able to move to the next stage of negotiations. The feeling that little progress has been made erased last week's tentative sterling optimism. Sterling ceded further ground against the euro and the dollar yesterday. EUR/GBP closed the session at 0.8823 (from 0.8792). Cable finished the day at 1.3341 (from 1.3390).

Policy makers from both sides and financial analysts continue to float ideas on what the next steps in EU-UK negotiations should be and on how the future relationship may look like. In this respect, UK trade Secretary Liam Fox indicated that the UK wants a deal that is virtually identical to current trade relationship. He also suggested that paying the separation bill might be linked to reaching such trade deal. This analysis obviously isn't shared by EU chief negotiator Barnier. We also keep an eye on the handling of the Brexit bill in the UK Parliament. UK November CPI will be published today. UK Headline CPI is expected unchanged at 3.0% Y/Y. BoE Carney will have to explain the overshoot in a letter to the chancellor for the Exchequer in case of a rise north of 3.0%, potentially causing some debate whether the BoE should move sooner with a next rate hike. However, we doubt that it will change the BoE's assessment as the central bank anticipates that inflation could peak slightly above 3.0%.

Recent developments pushed EUR/GBP lower in the 0.8690/0.9033 consolidation pattern. EUR/GBP tested 0.8693 support (62% retracement) on Friday,, but the test was rejected. Next support comes in at 0.8653. We assume that the 0.8653/90 area won't be easy to break short-term. We hold a neutral bias on EUR/GBP short-term. We consider a return to the bottom of this range as an opportunity to reduce sterling long exposure against the euro.

EUR/GBP rebounds in the established trading range despite Brexit deal

GBPUSD Further Bearish Below 1.3340 Level

The British pound continues to fall against the U.S dollar after buyers again failed to gain traction above the 1.3400 level on Monday. The GBPUSD pair is now slipping below the key 1.3340 support level, ahead of the release of key inflation data from the United Kingdom economy. UK CPI figures out during the European trading session are expected to show that inflation rose 0.2 percent during the month of November, and 3 percent year-on-year. Sterling remains focused on Brexit negotiation headlines coming from Brussels, and the outgoing FED Chair Janet Yellen’s last scheduled monetary policy statement on Wednesday.

The GBPUSD pair remains intraday bearish while trading below the 1.33400 level, further downside towards the 1.3300 and 1.3220 levels seems likely.

If GBPUSD buyers can hold price-action above the 1.3340 technical level, further buying towards the 1.3400 and 1.3470 resistance levels remains possible.

EURO Weaker Intraday Below 1.1790 Level

The euro currency has failed to build on upside momentum above the 1.1790 level against the U.S dollar, and has started to slip back towards the 1.1770 support region. The U.S dollar index has now retraced most of Monday’s losses, as investors start to position for the expected rate hike from the Federal Reserve on Wednesday. The EURUSD pair will likely be driven by the release of the German ZEW economic survey during the European trading session. Moving into the U.S session, the market mover for the pair will be the release of U.S PPI inflation figures, and scheduled speech from ECB President Mario Draghi.

The EURUSD pair remains weaker intraday while price-action trades below the 1.1790 level, further selling towards the 1.1750 and 1.1730 technical levels may occur.

Should the EURUSD pair move above the 1.1790 technical level, intraday buyers may start to target towards the 1.1811 and 1.1850 resistance levels.

Federal Reserve Policy Meeting Kicks Off In Washington Tuesday

Monetary policy is back in focus on Tuesday as the Federal Reserve coalesces in Washington for its final meeting of the year. Although the rate announcement will come on Wednesday, investors will be keeping tabs on all the latest developments involving the Fed.

Action begins at 09:30 GMT with a series of UK inflation indicators. The Office for National Statistics will report on the retail price index, producer price index and consumer price index. These measures are closely watched by the financial markets, and will have a direct impact on the British pound.

The Centre for European Economic and Social Research (ZEW) will report on German investor sentiment at 10:00 GMT. The main economic sentiment gauge is expected to fall to 17.4 from 18.7 the previous month.

ZEW will also present its euro-wide sentiment indicator at 10:00 GMT.

Shifting gears to North America, the US Department of Labor will report on the producer price index (PPI) for November at 13:30 GMT. The monthly indicator is expected to read 0.3%, which translates into a year-over-year gain of 2.9%.

The Federal Open Market Committee (FOMC) is widely expected to raise interest rates at the conclusion of its December meeting on Wednesday. That would mark the Fed’s third upward adjustment of the year, which is in line with previous forecasts.

Policymakers will also unveil their latest summary of economic projections covering GDP, unemployment and inflation. US GDP is growing faster than expected, a sign that the Trump reflation trade is benefiting the broader economy. Meanwhile, the employment picture has also brightened, with the Labor Department recently reporting the creation of 228,000 nonfarm jobs in November.

In other policy news, European Central Bank (ECB) Governor Mario Draghi will deliver a speech at 19:00 GMT, just days before his Governing Council votes on interest rates.

EUR/USD

The euro bounced back on Monday after a sharp selloff at the end of last week. However, it continues to trade well below 1.1800 US, which presents an imminent resistance area. The EUR/USD exchange rate was last seen trading at 1.1769, where it was little changed compared with the previous close. Monetary policy will loom large for this pair in the coming days.

GBP/USD

Pound sterling has lost its luster in recent days even as Theresa May struck a breakthrough deal with the European Union over Brexit. Cable (GBP/USD) was last seen trading at 1.3339, having declined more than 150 pips from Friday’s peak. British economic data could have considerable sway on Tuesday.

USD/JPY

The Japanese yen continued to backtrack against the dollar on Tuesday, with the USD/JPY hovering around 113.50. Money is pouring back into the greenback as expectations for an imminent rate hike continue to grow.

The UK, November Inflation Data Is Due To Be Released Today

Market movers today

In the UK, November inflation data is due to be released today. Headline inflation surged to 3.0% in October, but with the GBP depreciation pace abating there is a good chance that the November print will mark the start of a deceleration in inflationary pressures and we estimate core inflation remained stable at 2.7%.

German ZEW expectations for December are also due out this morning. Consensus is for a small decline from the current level of 18.7, due possibly to the recent heightened political uncertainty about the German government formation process.

In Sweden, focus is on the November inflation print , which we estimate will have been boosted by soaring energy prices (see next page).

Selected market news

Brent oil has risen 1.28% and is currently trading at 65.52 dollar per barrel, the highest since 2015, as the Ineos's North Sea Forties oil pipeline has been closed due to a crack. According to reports, it should take around two weeks to fix the pipeline. The higher oil price is likely to push up headline inflation globally near term but we still believe underlying inflation pressure will stay fairly muted, as we do not believe wage growth will pick up significantly next year.

In China, WSJ writes that officials are worried about investors pulling money out of China due to a combination of US tax reform and US rate hikes. According to the story, contingency plans are in place, with the PBOC ready to raise interbank rates, the possibility of tighter capital control and FX interventions.

With respect to Brexit, UK trade secretary Liam Fox has said that the UK wants a ‘virt ually identical' trade deal with the EU to the one it has now and dismissed the EU's chief negotiator Michel Barnier's comments that something like the EU's free trade arrangement with Canada (CETA) was the best the UK could hope for, as the UK wants to leave both the single market and the customs union. The comments underline that it is still difficult to say what the UK really wants to get out of the upcoming discussions on the future relationship and thus it is too early for markets to price out the Brexit risk premium in GBP.

In the US, Republicans still hope to hold a final vote on tax reform in both the House and the Senate next week so that President Trump can sign it on 20 December or even sooner. However, according to POLITICO, House and Senate Republicans are not getting closer to finding a compromise. While most of the negotiations are behind closed doors, a public hearing in the conference committee (consisting of both House and Senate members) is scheduled for Wednesday.