Sample Category Title

GBP/JPY Daily Outlook

Daily Pivots: (S1) 151.01; (P) 151.66; (R1) 152.11; More...

Intraday bias in GBP/JPY remains neutral for consolidation below 153.39 temporary top. Further rally is expected as long as 149.74 support holds. Break of 153.39 will resume the medium term up trend and target 61.8% projection of 139.29 to 152.82 from 146.96 at 155.32. However, break of 149.74 will dampen our bullish view and turn bias back to the downside for 146.96 key support instead.

In the bigger picture, current development suggests that medium term rise from 122.36 is resuming. Sustained trading above 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 146.96 support will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

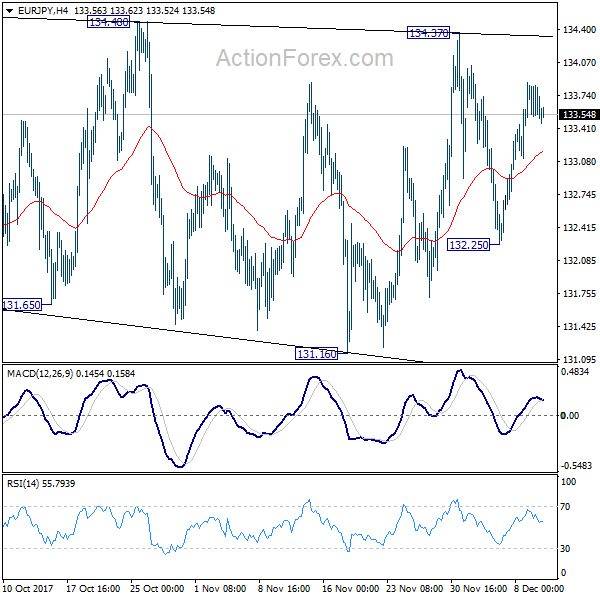

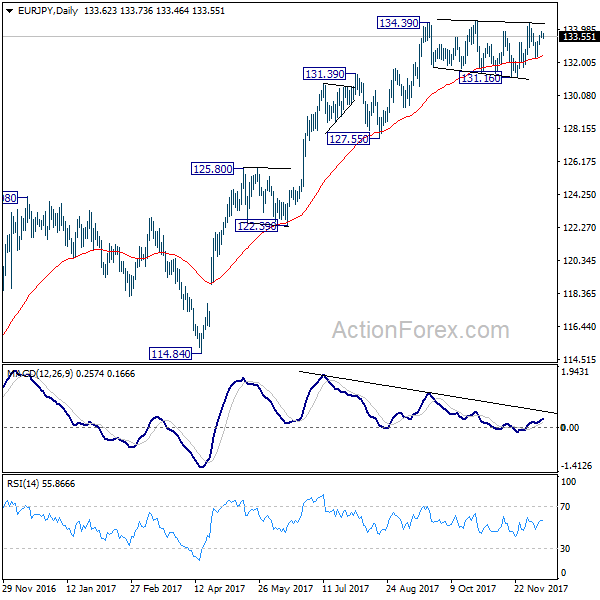

EUR/JPY Daily Outlook

Daily Pivots: (S1) 133.47; (P) 133.68; (R1) 133.83; More....

Intraday bias in EUR/JPY remains neutral as range trading could continue inside 131.16/134.48. But further rise will be expected as long as 131.16 support holds. Decisive break of 134.48 will resume medium term rise from 114.84 and target 141.04 resistance next. However, sustained break of 131.16 support will now indicate near term trend reversal and turn outlook bearish for 127.55 key support.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). Sustained break of 61.8% retracement of 149.76 to 109.03 at 134.20 will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will suggest medium term topping and will turn outlook bearish for deeper fall back to 114.84/124.08 support zone at least.

Forex: Lackluster Markets Await Central Banks

Markets were somewhat lackluster on Monday, and that trend appears set to continue Tuesday as traders await a host of Central Bank meetings starting on Wednesday, with the Federal Reserve expected to hike rates at their last FOMC meeting of 2017. With the markets “pricing-in” a hike of 0.25%, we are likely to see a degree of USD volatility as positions are squared and new positions opened. The focus will be on the outlook for next year and beyond, with the markets debating the impact of coming policy normalization on global asset markets.

GBP has retreated from recent highs, as optimism has faded following the “deal” made between the UK and the EU last week. The Rand Corporation, an influential US “think-tank”, recently released a study stating that nearly all the possible trading relationships between Britain and the European Union following Brexit would be less favorable than staying in the European Union. The study said the worst option would be a “no deal”, which would leave the UK economy 4.9% poorer by 2029. The study also said that even a “soft Brexit”, which would involve staying in the free market, would not be as positive economically as staying in the EU. According to Rand, there is only 1 option that would leave the UK better off outside the European Union: a comprehensive 3-way free trade deal between Britain, the US and the EU. However, the report admits that is an extremely unlikely scenario, given that the present trade negotiations between the US and the EU (the Trans-Atlantic Trade and Investment Partnership) are not supported by President Donald Trump and are “in a hiatus”. Charles Ries, VP of Rand and the study’s lead author commented “The analysis clearly shows that the UK will be economically worse-off outside of the EU under most trade scenarios – the key question for the UK is how much worse-off”.

The Kiwi (NZD) strengthened as the markets reacted positively to the appointment of Adrian Orr as the Next Reserve Bank of New Zealand Governor starting on March 27th, 2018. Mr. Orr is currently the Superannuation Fund chief and was a former RBNZ Deputy Governor and Chief Economist. NZDUSD is 0.25% higher in early Tuesday trading at around 0.6925.

EURUSD is little changed overnight, currently trading around 1.1770.

USDJPY is unchanged in early session trading at around 113.50.

GBPUSD is near to Tuesday lows, currently trading around 1.3338.

Gold is 0.17% higher in early Tuesday trading at around $1,244.25.

WTI is 0.45% higher overnight to trade around $58.33. With a major Brent pipeline “off-line” for major repairs, Brent’s rise has caused WTI to also move higher.

Major data releases for today:

At 09:30 GMT: The UK Office of National Statistics (ONS) will release a plethora of data sets. The major focus will be on the annualized Consumer Price Index (CPI) for November. The previous annualized CPI reading of 3% is well above the Bank of England’s target rate of 2% and the forecast for November is expected to come in slightly higher at 3.1%. Annualized Core CPI is forecast to come in at 2.8%, slightly higher than the previous release of 2.7%. Month-on-Month CPI is forecast to come in at 0.2% from the previous 0.1%. Whilst CPI remains above the BoE target level, there is no expectation that there will be any further hikes in interest rates until Q2 of 2018 at the earliest. The ONS will also be releasing Core PPI & PPI Input and Output (MoM & YoY) for November. Any significant deviation from expectations will see GBP volatility.

At 19:00 GMT: The US Financial Management Service will release its Monthly Budget Statement for November. The report summarizes the financial activities of federal entities, disbursing officers, and Federal Reserve banks.

GBPUSD Consolidates Recent Gains, Risk Of More Weakness

GBPUSD has been neutral since last week following a rise from near the 1.3000 level to a high of 1.3549 hit on December 1. The market is consolidating these recent gains and price action remains above the previous two months’ range. The 50 and 200- day moving averages are positively aligned. However, near-term risk is tilted to the downside, as RSI has been falling.

There is immediate support at the 38.2% Fibonacci retracement level (1.3320) of the upleg from 1.2773 to 1.3656. A daily closing below this would increase near-term pressure to the downside for a move towards the 50% Fibonacci (1.3216) and 61.8% Fibonacci (1.3112). From here the key psychological 1.3000 level comes into view but it is considered to be a strong support area. GBPUSD has been trading above this level since early September.

Overall the market has been searching for direction since reaching the 1.3656 peak on September 20. This was the highest level since June 2016. Resistance at 1.3445 needs to be cleared to see a re-test of 1.3656 and then a resumption of the prior uptrend.

As long as the market can stay above 1.3000 and above the 200-day moving average, the big picture remains positive and the longer-term uptrend that has been taking place since early this year is still in progress.

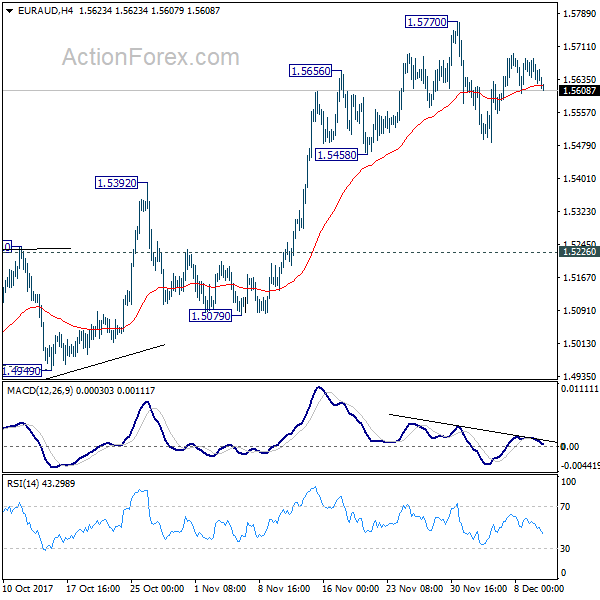

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5613; (P) 1.5647; (R1) 1.5670; More....

Intraday bias in EUR/AUD remains neutral for consolidation below 1.5770 short term top. Deeper decline could be seen and break of 1.5458 support cannot be ruled out. But downside should be contained above 1.5226 key support to bring rally resumption. On the upside, break of 1.5770 will resume the medium term rise and target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low).

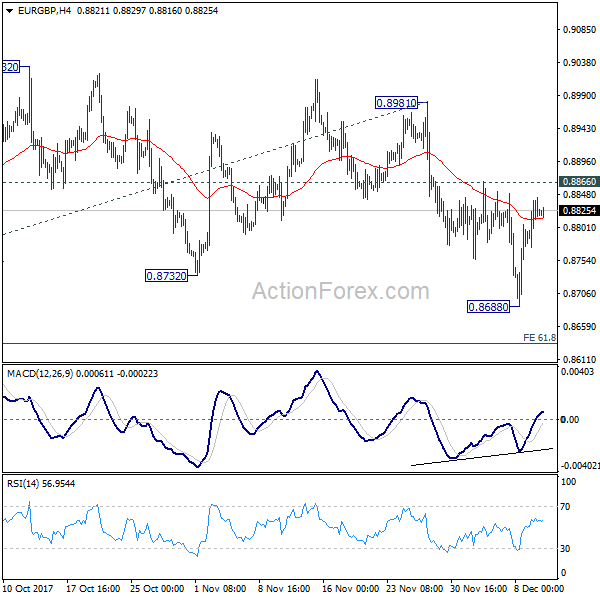

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8781; (P) 0.8812; (R1) 0.8853; More...

Intraday bias in EUR/GBP remains neutral for consolidation above 0.8688 temporary low. Deeper fall is expected as long as 0.8866 resistance holds. Below 0.8688 will target 61.8% projection of 0.9305 to 0.8745 from 0.8981 at 0.8468 first and then 100% projection at 0.8151 next. However, break of 0.8866 resistance will indicate near term reversal and turn bias back to the upside for 0.8981 resistance instead.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

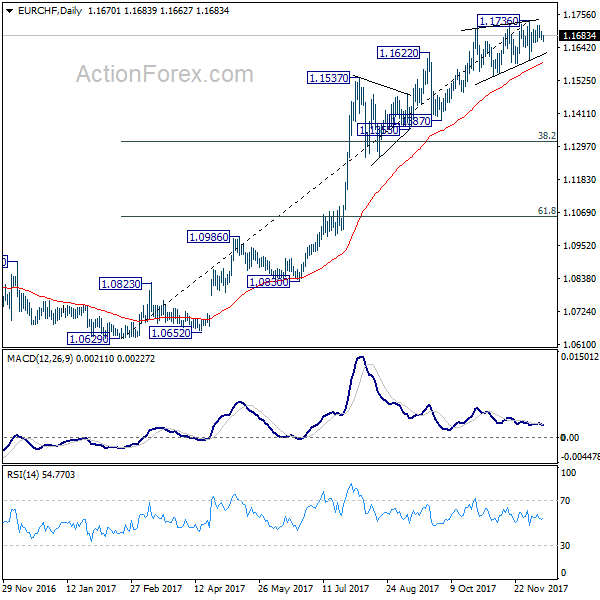

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1663; (P) 1.1680; (R1) 1.1689; More...

Intraday bias in EUR/CHF remains neutral and outlook is unchanged. We maintained the view that EUR/CHF is close to topping, if not formed. This is supported by persistent bearish divergence condition in 4 hour MACD, and rising wedge like structure. On the downside, break of 1.1597 support will will be a strong sign of trend reversal and should turn outlook bearish for 38.2% retracement of 1.0629 to 1.1736 at 1.1313.

In the bigger picture, while a medium term top could be around the corner, there is no change in the larger outlook. That is, long term rise from SNB spike low back in 2015 is still in progress and would extend. As long as 1.1198 resistance turned support holds, we'll hold on to this bullish view and expect another to prior SNB imposed floor at 1.2000. Though, we'll reassess the outlook if 1.1198 is firmly taken out.

Daily Wave Analysis: EUR/USD Bullish Breakout Faces Resistance From Wave-X Fibs

Currency pair EUR/USD

The EUR/USD bounce at the 50% Fibonacci level of wave 2 vs 1 could indicate the end of wave 2 (pink) but the retracement is rather short (see horizontal Fibonacci time levels 2 vs 1). An expansion of the wave 2 via a WXY (purple) is therefore possible and could indicate a potential bearish bounce at resistance (red).

The EUR/USD could build a bullish ABC (blue) zigzag within wave X (purple). Price seems to be bouncing at the 61.8% Fib of wave B (blue) and could move towards the 61.8% Fib of wave X (purple).

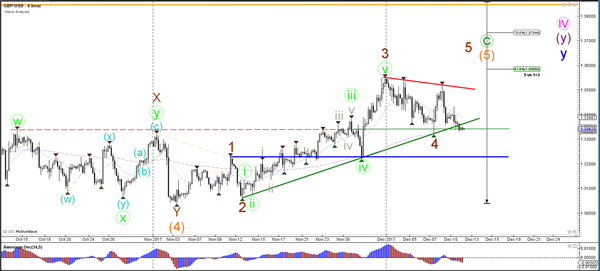

Currency pair GBP/USD

A GBP/USD break below the support (green) could still belong to a wave 4 (brown) as long as price does not break below the top of wave 1 (blue line). A bullish bounce could see price retest the resistance (red) but a breakout is needed before price is better positioned to complete the waves 5.

The GBP/USD would invalidate wave 2 (blue) if price breaks below the 100% Fib level of wave 2 vs 1. For the moment, price seems to be building a falling wedge chart pattern (orange/blue), which is a potential reversal signal.

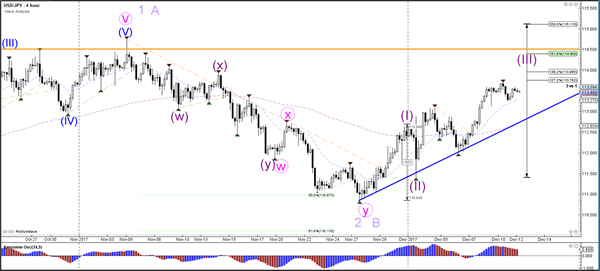

Currency pair USD/JPY

The USD/JPY could be a in wave 3 (purple) if price stays above the support trend line (blue). The alternative scenario is that price is building a wave C rather than a wave 3.

The USD/JPY is showing a triangle chart pattern which fits within the current wave 4 (blue) correction.

Market Update – Asian Session: Light Trading Ahead Of Central Bank Meetings Later In The Week

Headlines/Economic Data

General Trend: Equities trade mostly lower and there continues to be subdued price action ahead of Wed’s US FOMC statement /forecasts

Energy shares outperform

Brent Crude trades above $65/bbl (for the first time since June 2015) amid shutdown related to the North Sea Forties pipeline system

Japan

Nikkei 225 opened flat; closed -0.3%

TOPIX Information/Communications Index -0.5%; KDDI -1%

Financials trade higher: TOPIX Securities index +1.3%; Sumitomo Mitsui Financial +1.9%, Mitsubishi UFJ +1.5%, Mizuho Financial +1.2%

Toshiba +1.2%: Confirms settlement talks with Western Digital, but said has not yet reached an agreement

JAPAN NOV PPI (CGPI) M/M: 0.4% V 0.2%E; Y/Y: 3.5% V 3.3%E

(JP) Japan Oct Tertiary Industry Index m/m: 0.3% v 0.2%e

Bank of Japan (BOJ): Benchmark ratio for macro add-on balance kept unchanged; The Benchmark Ratio during the December 2017, January, and February 2018 reserve maintenance periods is 21.5%; The Policy-Rate Balance in financial institutions' current account balances at the Bank, to which a negative interest rate is applied, will be about 10 trillion yen on average during the above three reserve maintenance periods.

Japan MoF sells ¥2.2T v ¥2.2T indicated in 0.1% 5-yr JGBs; avg yield -0.104%; bid to cover 4.38x

Looking Ahead: Japan Oct Core Machinery Orders due for release on Wed

Korea

Kospi opened flat

Cosmetics and tourism firms trade lower amid concerns related to tourism: Amorepacific -3.5%, Lotte Tour -4%

Hynix Semi -1.3%

South Korea Nov Export Price Index M/M: -1.8% v +0.5% prior; Y/Y: 2.3% v 8.0% prior

South Korea has asked US to delay joint military drills on Olympics; **Note: The 2018 Winter Olympics are due to be held in South Korea. The start is expected on Feb 9th.

(KR) South Korea FSC Choi: South Korea will not allow cryptocurrency futures trading; considering measures to curb speculation

003550.KR Guides FY18 new investment spending KRW19T, to hire 10K new workers

China/Hong Kong

Markets opened mixed: Hang Seng flat, Shanghai -0.1%

Indices later trade lower

Hang Seng Information Technology Index -1.4%

There has been some weakness in China’s insurance sector: New China Life Insurance -2.3%, Ping An -2%

(CN) China insurance regulator, CIRC, plans to revise certain guarantee fund rules for insurance industry – Chinese Press

(CN) China monetary policy to be neutral with a tight bias; may raise open market rates next year - China Securities Journal; May cut RRR for some banks;**Note: The PBoC currently has a ‘prudent and neutral’ policy stance

(CN) China reportedly working on a plan to react to US tax reforms and rate hikes; considering higher interest rates and tighter capital controls - press

(CN) Yuan may fluctuate at 6.4-6.8 in 2018; has potential appreciation in long term - China Daily

(CN) China to hold Central Economic Conference Dec 18-20th

(CN) PBOC Open Market Operations (OMO): injects CNY150B v CNY80B prior in 7 and 28-day reverse repos v skips prior; Net injections CNY40B v CNY20B prior

USD/CNY (CN) PBoC sets yuan reference rate at 6.6162 v 6.6152 prior

(CN) Reportedly US, EU and Japan plan to step up trade pressure on China to address "severe excess capacity" in sectors like steel – FT

(CN) CHINA NOV NEW YUAN LOANS (CNY): 1.12T V 800BE

(CN) CHINA NOV AGGREGATE FINANCING (CNY) 1.600T V 1.225TE

(CN) CHINA NOV M2 MONEY SUPPLY Y/Y: 9.1% V 8.9%E; M1 MONEY SUPPLY Y/Y: 12.7% V 12.9%E

Australia/New Zealand

ASX 200 opened flat; closed +0.2%

ASX 200 Energy Index +1%; Utilities -0.8%

Tabcorp and Tatts Group each trade higher by over 2% ahead of merger vote

(AU) Australia Nov NAB Business Conditions: 12 v 21 prior; Confidence: 6 v 8 prior

(AU) AUSTRALIA Q3 HOUSE PRICE INDEX Q/Q: -0.2% V 0.5%E; Y/Y: 8.3% V 8.8%E

(AU) Australia sells A$150M v A$150M indicated in Aug 2040 indexed bond, avg yield 0.9236%, bid to cover 2.45x

AHY.AU Guides FY17 (A$) underlying Net 59-60M (prior low single digit growth); EBITDA 124-125M (prior low single digit growth); -7%

Looking Ahead: Comments expected on Wed from RBA Gov Lowe and Assist Gov Kent, along with the Westpac Dec Consumer Sentiment

Other Asia

(IN) India 10-year bond yield at 7.23%, +6bps amid rise in oil prices

(MY) Malaysia Oct Industrial Production y/y: 3.4% v 4.1%e (smallest rise since Sept 2016); Manufacturing Sales Value y/y: 11.0% v 10.6% prior

(SG) SINGAPORE OCT RETAIL SALES M/M: 1.5% V 2.0%E; Y/Y: -0.1% V 1.0%E; EX-AUTO Y/Y: 0.8% V 2.2%E

North America

US equities closed mostly higher: Dow Jones +0.2%, S&P500 +0.3%, Nasdaq +0.5%, Russell 2000 -0.1%

S&P 500 Technology Sector +0.9%, Energy +0.8%

SEMI: Forecasts 2017 global new semiconductor manufacturing equipment sales to $55.9B, +35.6% y/y (record high), 2018 sales seen at $60.1B, +7.5% y/y

(US) TREASURY'S $20B 10-YEAR NOTE REOPENING DRAWS 2.384%; BID-TO-COVER RATIO: 2.37 V 2.54 PRIOR AND 2.49 OVER THE LAST 8

(US) TREASURY'S $24B 3-YEAR NOTE AUCTION DRAWS: 1.932%; BID-TO-COVER RATIO: 3.15 V 2.76 PRIOR AND 2.82 OVER THE LAST 12 AUCTIONS

Tax Reform: (US) Joint Committee on Taxation study of House GOP tax plan with dynamic scoring: bill would add $1.0T to US debt over 10 years

(US) Treasury Dept: GOP tax plan would pay for itself due to increase in long-run growth rate – press; Treasury says GOP plan would boost long-run growth rate to 2.9% from 2.2% (assumptions that are in contrast to official congressional estimates)

M&A: 21st Century Fox: Comcast confirms "no longer engaged" in review

Looking Ahead: US Weekly API Crude Inventories due on Tuesday.

Europe

(UK) Germany Chancellor Merkel reportedly informs party members that a Brexit mandate is not likely until Feb – press

M&A: Gemalto [GTO.NL]: Atos proposes to acquire Gemalto at €46/shr in €4.3B all-cash deal

Akzo Nobel [AKZA.NL]: Lanxess reportedly partnering with Apollo on bid for Akzo chemicals division; talks said to be in early stages - press

Vallourec [VK.FR]: Considering divesting its Drilling Products business to National Oilwell Varco after getting binding offer of $63M

Energy: North Sea Forties pipeline system could be shut for weeks – FT; **NOTE: earlier report said that the Forties pipeline was being shut for immediate repairs after a crack worsened. The crack had been causing the pipeline to run at reduced capacity.

Looking Ahead: UK Nov CPI and German Dec ZEW survey due for release on Tuesday

Levels as of 01:00ET

Nikkei225 -0.3%, Hang Seng -0.4%; Shanghai Composite -0.8%; ASX200 +0.3%, Kospi -0.5%

Equity Futures: S&P500 +0.0%; Nasdaq100 +0.1%, Dax -0.0%; FTSE100 +0.1%

EUR 1.1779-1.1765; JPY 113.58-113.44; AUD 0.7537-0.7519;NZD 0.6937-0.6902

Feb Gold -0.0% at $1,246/oz; Jan Crude Oil +0.8% at $58.44/brl; Mar Copper -0.3% at $3.01/lb

Australia’s Business Confidence Index Slid In November

For the 24 hours to 23:00 GMT, the AUD rose 0.16% against the USD and closed at 0.7529.

LME Copper prices rose 0.1% or $9.0/MT to $6547.5/MT. Aluminium prices declined 0.03% or $0.5/MT to $1991.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7531, with the AUD trading a tad higher against the USD from yesterday's close.

Overnight data showed that Australia's NAB business confidence index eased to a level of 6.0 in November, from a revised reading of 9.0 registered in the prior month. Additionally, the nation's NAB business conditions index fell to a level of 12.0 in November. In the previous month, the index had registered a level of 21.0.

The pair is expected to find support at 0.7517, and a fall through could take it to the next support level of 0.7503. The pair is expected to find its first resistance at 0.7545, and a rise through could take it to the next resistance level of 0.7559.

Going ahead, traders would keep a close watch on a speech by the Reserve Bank of Australia's Governor, Philip Lowe along with Australia's Westpac consumer confidence index for December, both due overnight.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.