Sample Category Title

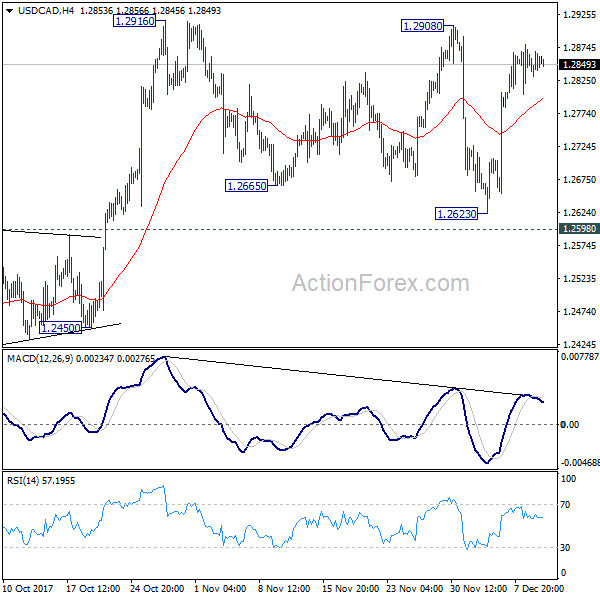

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2834; (P) 1.2851; (R1) 1.2872; More....

Intraday bias in USD/CAD remains neutral for the moment as consolidation from 1.2916 might extend. On the upside, firm break of 1.2916 will resume whole rally from 1.2061 and target 1.3065 medium term fibonacci level next. In case of another fall, we'd expect strong support from 1.2598 to contain downside and bring rebound. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2888). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7503; (P) 0.7524; (R1) 0.7546; More...

Intraday bias in AUD/USD remains neutral for consolidation above 0.7500 temporary low. Upside of recovery should be limited below 0.7652 resistance to bring fall resumption. Break of 0.7500 will extend the fall from 0.8124 and target 0.7322/8 cluster support next.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8029). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7732 near term resistance holds.

Aussie Steady Despite Weakening Business Conditions, Dollar Stays Soft

Trading activities in the forex markets are rather subdued today. Dollar weakens mildly as traders are staying cautious ahead of FOMC rate decision later on Wednesday. Sterling is also soft as markets eye today's inflation data. On the other hand, New Zealand Dollar remains the strongest one this week and commodity currencies are generally firm. But there is no confirmed signs of a trend there yet. In other markets, US indices gained some ground overnight but DOW and S&P 500 are kept below the historical highs made last week. Treasury yields were mixed with 10 year yield gained a little by 0.002 to 2.385. Asian markets are also mixed with Nikkei trading nearly flat at the time of writing.

Australia business conditions dropped sharply

Australia NAB business conditions dropped sharply by -9 to 12 in November, down from 21. Business confidence dropped -2 to 6, down from 8. NAB chief economist Alan Oster noted that "we expected to see last month's spike in business conditions unwound fairly quickly as it both came as a bit of a surprise, and was also out of sorts with what we were seeing in some of the other leading indicators from the survey, such as forward orders." Also, "we are paying close attention to what now appears to be a downward trend in business confidence as that could naturally have some implications for decisions around hiring and investment."

For Australia, sluggish wage growth is a key concern for keeping inflation low. But Oster noted that "we saw some tentative signs of higher wages in the survey, although that does appear to be weighing on the confidence of some firms as well." However, "prices are rising the most in mining, while retail and personal services prices are the softest - a reflection of the cautious spending behavior by consumers."

Also from Australia house price index dropped -0.2% qoq in Q3, below expectation of 1.5% qoq.

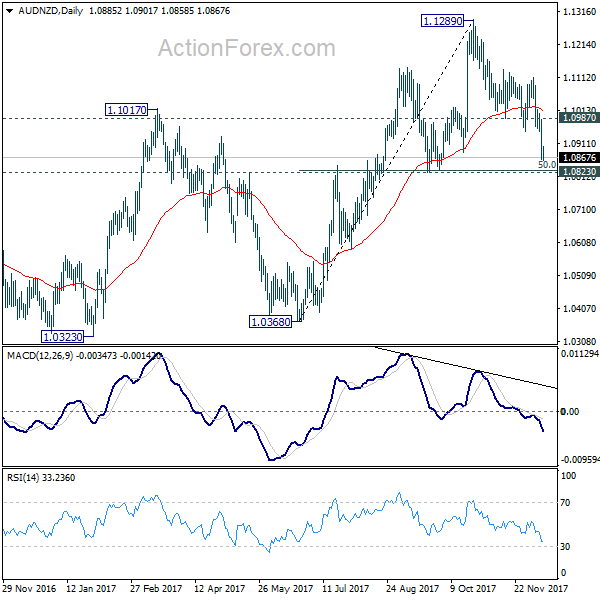

AUD/NZD in steep pull back this week

AUD/NZD dives sharply this week. Kiwi was boosted by positive reactions to appointment of Superannuation Fund chief Adrian Orr as the next RBNZ Governor. That's is seen as guaranteeing a practical approach in RBNZ reform. AUD/NZD's recent fall from 1.1289 is so far seen as a corrective move. While more downside could be seen, we'd expect strong support at 1.0823 (50% retracement of 1.0368 to 1.1289 at 1.0829) to contain downside and bring rebound. Above 1.0987 resistance will turn bias to the upside for retesting 1.1289.

Merkel to react in concrete way to Macron's EU proposals

German Chancellor Angela Merkel said she wanted to complete the coalition talks with the Social Democrats quickly. And to her, a "stable" government is the basis Germany can work best with France and Europe. In her view, it's a "historical necessity" to reform Europe. And Germany would be able to "react in a concrete way" to French President Emmanuel Macron's proposals. She emphasized that "Europe does not only need a stronger economic and monetary union but we must also have a Europe of security and the rule of law, internally and externally."

Looking ahead

UK inflation data will take center stage in European session. CPI is expected to be unchanged at 3.0% yoy in November. RPI is expected to unchanged at 4.0% yoy. PPI will also be released too. German will also release ZEW economic sentiment. Later in the day, US will release PPI, but traders will likely look beyond that to tomorrow's CPI and FOMC rate decision.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7503; (P) 0.7524; (R1) 0.7546; More...

Intraday bias in AUD/USD remains neutral for consolidation above 0.7500 temporary low. Upside of recovery should be limited below 0.7652 resistance to bring fall resumption. Break of 0.7500 will extend the fall from 0.8124 and target 0.7322/8 cluster support next.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8029). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7732 near term resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI M/M Nov | 0.40% | 0.20% | 0.30% | |

| 23:50 | JPY | Domestic CGPI Y/Y Nov | 3.50% | 3.30% | 3.40% | |

| 00:30 | AUD | NAB Business Conditions Nov | 12 | 21 | ||

| 00:30 | AUD | NAB Business Confidence Nov | 6 | 8 | ||

| 00:30 | AUD | House Price Index Q/Q Q3 | -0.20% | 0.50% | 1.90% | |

| 04:30 | JPY | Tertiary Industry Index M/M Oct | 0.20% | -0.20% | ||

| 09:30 | GBP | CPI M/M Nov | 0.20% | 0.10% | ||

| 09:30 | GBP | CPI Y/Y Nov | 3.00% | 3.00% | ||

| 09:30 | GBP | Core CPI Y/Y Nov | 2.70% | 2.70% | ||

| 09:30 | GBP | RPI M/M Nov | 0.30% | 0.10% | ||

| 09:30 | GBP | RPI Y/Y Nov | 4.00% | 4.00% | ||

| 09:30 | GBP | PPI Input M/M Nov | 1.50% | 1.00% | ||

| 09:30 | GBP | PPI Input Y/Y Nov | 6.70% | 4.60% | ||

| 09:30 | GBP | PPI Output M/M Nov | 0.30% | 0.20% | ||

| 09:30 | GBP | PPI Output Y/Y Nov | 3.00% | 2.80% | ||

| 09:30 | GBP | PPI Output Core M/M Nov | 0.20% | 0.10% | ||

| 09:30 | GBP | PPI Output Core Y/Y Nov | 2.20% | 2.10% | ||

| 09:30 | GBP | House Price Index Y/Y Oct | 5.20% | 5.40% | ||

| 10:00 | EUR | German ZEW Economic Sentiment Dec | 17.9 | 18.7 | ||

| 10:00 | EUR | German ZEW Current Situation Dec | 88.7 | 88.8 | ||

| 10:00 | EUR | German ZEW Expectations Dec | 18 | 18.7 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | 30.2 | 30.9 | ||

| 11:00 | USD | NFIB Small Business Optimism Nov | 104 | 103.8 | ||

| 13:30 | USD | PPI M/M Nov | 0.40% | 0.40% | ||

| 13:30 | USD | PPI Y/Y Nov | 3.00% | 2.80% | ||

| 13:30 | USD | PPI Core M/M Nov | 0.20% | 0.40% | ||

| 13:30 | USD | PPI Core Y/Y Nov | 2.40% | 2.40% | ||

| 19:00 | USD | Monthly Budget Statement Nov | -135.2B | -63.2B |

Market Morning Briefing: Pound Has Broken Support At 1.335

STOCKS

Dow (24386.03, +0.23%) may be slowly and steadily heading towards 24600 in the coming sessions. Movements could be small and narrow but looks positive for the near term.

Dax (13123.65, -0.23%) came off slightly and remained below 13200. Looking at the 3-day and the weekly candle charts, there is support below current levels which could eventually push the index to higher levels above 13200 in the medium term. View remains bullish for the long term while above 13000.

Nikkei (22944.21, +0.02%) has tried to test 23000 and may possibly attempt to break above 23000. Not that 23000-23200 could be a decent near term support which could push the index back towards 22800 and lower. A break above 23200, if seen and sustained would initiate further bullishness with an upside target of 23400-23800 in the longer run. Important to watch 23000-23200 levels.

Shanghai (3307.68, -0.44%) tested 3325 as expected but came off from there instead of moving up further towards 3340. A re-test of 3300 or lower is possible before the index again bounces back towards 3340-3350 levels.

Nifty (10322.25, +0.55%) and Sensex (33455.79, +0.62%) were up by more than 0.50% yesterday. Nifty may test 10350 and come off from there to see a short dip while Sensex could test resistance at 33750. While the resistances hold, Dollar Rupee could bounce back from levels near 64.30.

COMMODITIES

Gold (1244.54) looks weak and the bears seems to be dominant just now. A break below 1240, if seen would be crucial and take it down towards 1220 in the coming sessions. But while above 1240, we keep some chances of a bounce back towards 1260-1280 soon. Crucial to watch 1240 on Gold and 94 on Dollar Index.

Silver (15.76) is almost stable after the recent fall from levels near 17.25. Maximum downside of 15.50 is possible before the price starts to move up towards 16.25 and higher.

Brent (65.22) and WTI (58.26) have moved up sharply. Brent could target 68 in the coming sessions while WTI has resistance at 59.0-60.0 which needs to break to ensure further bullishness on the price. For now Brent has a possibility of moving up faster compared to that of WTI.

Copper (3.0040) has moved up in line with our expectation and could rise further towards 3.05-3.07 in the coming sessions.

FOREX

Dollar-Index (93.945) is now testing resistance around 94.00 on the 3 day candles and daily line charts. This is an important resistance, whose hold could indicate to a possible downtrend towards 93 by end of this month. However a breach of resistance would possibly lead to a test of 94.40-94.50 on the daily candles, from where a definitive dip could follow.

Euro (1.1768) is trading just above immediate support (around 1.173-1.175) on the 3 day candles, which is likely to hold and take it towards 1.19 by the end of the month. A break of immediate support could however lead to testing of lower support around 1.17 (as seen on daily candles, 3 day candles & daily line charts), which could then prove to be a strong support.

Dollar-Yen (113.48), like the Dollar Index, seems to be seeing a dip from resistance level (around 113.5-113.6) on the daily line chart. A further test of higher resistance at 114 could still be possible with an eventual dip back towards 112-112.5 by next month.

Pound (1.3340) has broken support at 1.335 and is now expected to move towards 1.32-1.3225, which is seen as a strong support level on daily, 3 day and weekly charts.

Dollar Rupee (64.3650) may test 64.30/25 today and then bounce back towards 64.50 by the end of the week. Possibility of corresponding movement in the Nifty towards resistance (10350) and a dip from there coincides with predicted Dollar Rupee movement.

INTEREST RATES

The US yields are almost stable. The 10YR (2.38%) is down by 1bps while the 5Yr (2.15%) and the 30Yr (2.77%) are stable. The 30YR is testing immediate resistance at 2.80% while the 10Yr could move up to 2.45% in the near term. The 5Yr also has some room on the upside and could test 2.20% in the near term.

The UK-US 10YR (-1.18%) has fallen sharply breaking below important support near -1.12%. While the spread moves lower, Pound could also be bearish towards 1.32-1.31 in the coming sessions.

The German-US 10YR (-2.09%) has moved lower as expected but may not stop at -2.10%. The spread looks weak in the near term.

The Indian 10YR GOI (7.1717%) has risen sharply yesterday and could move up to test 7.20-7.25% in the near term.

Analog Versus Digital Gold

Before we start, Litecoin has just hit a new record at $220, up more than 4000% this year. Gold has a virtually unblemished track record as a store of value over 6000 years but that didn't matter in 2017 as Bitcoin dug into its market. Will it be the same in 2018? The New Zealand dollar was the top performer Monday while the pound lagged for the second day. Australian house price data is up next. There are 10 open trades ahead of this week's busy set of central bank meetings & key US data.

The week started off with all eyes on Bitcoin as CBOE had a successful launch. Volume was at 7000 contracts, which is only $119m notional but it certainly can't be called a failure. More importantly, Bitcoin prices climbed above $17000 and were relatively stable (at least by BTC standards). Ultimately, those are all good signs for the near term.

Bad signs, meanwhile, continue to mount in gold. We have no doubt that many gold investors or would-be investors have turned to crypto. At the margins, that means less excitement and buying in precious metals. Anything could change in crypto at a moment's notice but for now, the outflows from gold are considerable and speculative net longs are at 4-month lows.

Technically, the trend is increasingly weak. Last week, gold broke below the October low of $1260 and slid another $12 to $1240 on Monday. The July low of $1200 is a major support level that needs to hold if gold is going to rebound in the months ahead. If not, it could get ugly for the old-fashioned analog store of value.

Looking to the short-term, housing investments have been better than gold for the past five years of the QE era. That's expected to continue in 2018, even as regulators find creative ways to curb speculation. One spot to always watch is Australia where Q3 house prices are due at 0030 GMT. Through Q2, prices were up 10.2% y/y and 1.9% q/q. That's expected to cool to 8.8% y/y and +0.5% q/q. Look for a small reaction in AUD.

A Lull in Currency Markets

New York traders started their day off with terror incident at the Port Authority train station, but as we've seen so often in the past, the market is desensitised to lone wolf attacks, and held unshakable through this deplorable attack.

With a deluge of Centeral Banks on tap this week and year-end position sweep on the near horizon, Forex traders spent the last 24 hours doing little more than rehashing old narratives. Outside of some idiosyncratic chronicles on the NZD and MXN, it was one of the quietest 24 hours trading session in some time

But the Greenback has some reasonably fat risk events to manoeuvre through this week like US CPI tonight, elections in the heart of Dixie, Tax Reform monkey business and the FOMC forward guidance. So don't confuse the lull in price action overnight as anything more than a brief respite before the market goes lights, camera, action.

US equity markets have remained on the ups feeding of tax reform positivity, a likely extension of the " Goldilocks " economy and a sprinkling of US infrastructure fairy dust for good measure. While in China market have remained stable to positive as investors reacted favourably to the weekend's softer-than-expected CPI report.

OIL

Oil prices ripped higher with Brent topping a 2015 chart plot after reports came to view that a 450,000 barrel-a-day North Sea pipeline has had to be shut down due to a worsening crack. Brents chart-topping move looks quite bullish despite it comes on the back of the North Sea news. But none the less, it suggests market players remain bulled up Oil near term.

Bitcoin

Bitcoin futures on the CBOE survived its first of many ramps, but as expected participation levels were relatively low. While the naysayer vs soothsayer debate rages, there doesn't appear to be any real rush to judgement as the market is patiently waiting for more players with deeper pockets to enter the Bitcoin fray. At the moment, some of the major US bank futures clearers are not taking orders, but we expect that to change after year-end code freeze ends and risk managers have had some time to digest the volatility. But granted, with few if any reasonable YTD correlations to play Bitcoins off, it remains a daunting task for both compliance and risk to navigate.

Greater participation from institutional level type "whales" could ultimately smooth out the market volatility and reduce "FUD "( 'fear, uncertainty and doubt'). And hopefully, there will be fewer causes to trigger circuit breakers designed to calm the market.

But we're long ways off from the big Financial institutions accepting Bitcoin as an investment grade product to sell to clients as trying to predict Bitcoin price movements remains no less confident then predicting the path of a raging Tornado.

G-10

The New Zealand Dollar

Continues to benefit from the market-friendly association for incoming RBNZ governor Adrian Orr who is currently the CEO of the New Zealand Superannuation. A great selection from the market perspective as it eliminates the fear of a wild card appointment steering the ship.

The Japanese Yen

Outside of blip in risk aversion which saw a low print of 113.25 after the US terror attack, the market is back to a happy place around 113.50 awaiting the next wave of market drivers.

The Euro

Remains a sideshow ahead of the ECB where the tail risk is for a more hawkish narrative and so it's unlikely the EURO bills will lose the plot ahead of the central bank meeting.

The Australian Dollar

The more supportive narrative in China along with firming commodity markets has kept the bears at bay so far this week. And given little ambit for the Feds or ECB to surprise this week I suspect profit taking into the central bank meetings will support the Aussie near-term

Asia FX

Malaysian Ringgit

The Ringgit is showing a bit stronger in pre-open trade driven by higher oil prices and stability in regional equity markets. And given there is little scope for a surprise from the Fed this week and with tepid wage growth it also suggests inflation via the CPI or PCE will be muted as was.

So as long as the Feds interest path to normalisation remains more heavily weighted to inflation rather than the growth in this weeks FOMC guidance, the Riggit will trade constructively.

Canadian Dollar Flat Ahead of Central Bank Week

The Canadian dollar traded in a narrow range on Monday. The loonie ended last week lower versus the USD as tax reform hopes and a strong U.S. non farm payrolls (NFP) was released on Friday. The loonie remains close to the levels it ended at then and with little Canadian data releases this week it will be mostly driven by US indicators. Inflation data in the US will be published by the Bureau of Labor Statistics on Wednesday, December 13 at 8:30 am. Core CPI is expected to gain 0.2 percent but prices taking into consideration food and energy are forecasted to increase by 0.4 percent.

The U.S. Federal Reserve will release its quarterly economic projections and Federal Open Market Committee (FOMC) statement on Wednesday, December 13 at 2:00 pm EST. The highly anticipated December meeting of the Fed is expected to bring a 25 basis points rate hike. The market has already priced in that move as it was heavily telegraphed by policy makers. Economists are forecasting 3 rate hikes in 2018 and the dot-plots could align with those estimates. Fed Chair Janet Yellen will make her final appliance as Chair when she hosts the FOMC press conference at 2:30 pm EST.

Bank of Canada (BoC) Governor Stephen Poloz will deliver a speech in Toronto titled: "Three Things Keeping Me Awake at Night". The central bank has gone from a hawkish cheerleader of the economy in the summer to a dovish bystander as so many unknowns complicate the path of interest rates in Canada. Rising household debt is a concern as inflation could rise forcing the BoC into higher rates. The gap with the Fed will continue to grow unless the economy can shake off the Q3 slowdown but there is little evidence of that despite strong job numbers last month.

The USD/CAD gained 0.8 percent on Monday. The currency pair is trading at 1.2857 near flat from the close of the market on Friday. The loonie has depreciated more than 1.34 percent in December as the Bank of Canada (BoC) was dovish and kept rates unchanged in the last statement while the market has fully priced in a rate hike by the U.S. Federal Reserve this week. The meeting will be Fed Chair Janet Yellen's last hurrah as she steps down in February to make way for her successor Jerome Powell. Polls point to 3 rate hikes in 2018 and with Powell having a chance to reshape the Fed by filling so many open positions it will be interesting to see how quickly can he put his stamp on monetary policy.

The Trump administration is near its biggest accomplishment to date if they can reconcile the two tax bills despite mounting pressure from various citizen groups. The NAFTA negotiations will restart next week but with no clear goal in sight the talks are sure to carry over to next year despite both Mexico and the United States having elections which could distract from the original objectives.

Oil prices rose in the last 24 hours. The price of West Texas Intermediate is trading at 57.87 after a disruption of North Sea supply and the after effects of a terrorist attack in New Y York. The Forties pipeline was shut down for repairs and could take weeks to get back online. The pipeline carries 450,000 daily barrels into Scotland, 40 percent of the UK's oil and gas production. A hairline crack was discovered on Wednesday and the line was running at reduced pressure since then.

Supply disruptions have been the third major factor driving oil prices of late. The Organization of the Petroleum Exporting Countries (OPEC) oil cut agreement with other producers and the rise of US shale production have offset each other. Natural and geopolitical issues have caused disruptions which in turn have driven the price of crude higher.

The OPEC successfully pulled off an extension of its deal with other major producers until the end of 2018. Demand continues to stagnate which could undo all the hard work of negotiators to stabilize prices at current levels if oil producers that are not part of the agreement like Brazil, Canada and the United States start ramping up their production significantly to take advantage of higher prices.

Market events to watch this week:

Tuesday, December 12

- 4:30 am GBP CPI y/y

- 8:30 am USD PPI m/m

Wednesday, December 13

- 4:30 am GBP Average Earnings Index 3m/y

- 8:30 am USD CPI m/m

- 8:30 am USD Core CPI m/m

- 10:30 am USD Crude Oil Inventories

- 2:00 pm USD FOMC Economic Projections

- 2:00 pm USD FOMC Statement

- 2:00 pm USD Federal Funds Rate

- 2:30 pm USD FOMC Press Conference

- 7:30 pm AUD Employment Change

- 7:30 pm AUD Unemployment Rate

- 9:00 pm CNY Industrial Production y/y

Thursday, December 14

- 3:30 am CHF Libor Rate

- 3:30 am CHF SNB Monetary Policy Assessment

- 4:00 am CHF SNB Press Conference

- 4:30 am GBP Retail Sales m/m

- 7:00 am GBP MPC Official Bank Rate Votes

- 7:00 am GBP Monetary Policy Summary

- 7:00 am GBP Official Bank Rate

- 7:45 am EUR Minimum Bid Rate

- 8:30 am EUR ECB Press Conference

- 8:30 am USD Core Retail Sales m/m

- 8:30 am USD Retail Sales m/m

- 8:30 am USD Unemployment Claims

*All times EDT

Pound Edges Lower on Weak Housing Inflation Report, CPI Next

The British pound has posted slight losses in the Monday session. In North American trade, GBP/USD is trading at 1.3353, down 0.26% on the day. On the release front, British Rightmove HPI declined 2.6%, marking the fourth decline in five months. In the US, JOLTS Openings softened to 6.00 million, shy of the estimate of 6.03 million. On Tuesday, inflation indicators will be in focus. The UK releases CPI, which is expected to remain unchanged at 3.0%. The US will release the Producer Price Index.

There was positive news for Prime Minister May, who appears to have received a green light from Brussels to move forward in the thorny Brexit negotiations. There was a major breakthrough on Friday, as EU Commissioner Jean-Claude Juncker announced that sufficient progress had been made on non-trade issues in the Brexit talks. The announcement came after May managed to appease both the Irish government and the DUP party, after she promised both that Northern Ireland would not have any hard borders after Brexit. The role of the European Court of Justice was also a prickly issue, but the EU has apparently agreed that European citizens living in the UK will be subject to British courts only. This means that Britain and Europe can now move to Phase II and discuss trade relations. With Britain scheduled to leave the EU in March 2019, time is of the essence. What will a new trade relationship look like? On Sunday, Brexit minister David Davis said he envisions a comprehensive trade deal with Europe, which would be signed just after Britain leaves the bloc. The EU recently signed a free-trade treaty with Canada, and Davis said that he wants an agreement "Canada plus plus plus", meaning that the deep trading ties between the sides and access to European markets would remain intact.

The markets continue to digest Friday's US employment numbers, which were a mix. Nonfarm Employment Change softened in November, but the reading of 228 thousand easily beat the estimate of 198 thousand. However, Average Hourly Earnings, which measures wage growth, came in at 0.2%, shy of the estimate of 0.3%. Analysts remain stumped as to why wages remain stubbornly low, given a red-hot labor market which is running at full capacity. On an annual basis, wages rose 2.5%, short of the forecast of 2.7%. The Fed is also concerned with the lack of wage growth, and this could have a significant effect on monetary policy – if wage growth and inflation shows improvement in 2018, the Fed could raise rates up to three times in 2018.

Yen Ticks Higher, Japanese Manufacturing Report Misses Expectations

The Japanese yen has posted slight gains in the Monday session. In North American trade, USD/JPY is trading at 113.30, down 0.16% on the day. On the release front, Japanese BSI Manufacturing Index improved to 9.7 points, but this fell short of the estimate of 10.1 points. In the US, JOLTS Openings softened to 6.00 million, shy of the estimate of 6.03 million. On Tuesday, the US releases PPI, an important inflation indicator.

The markets continue to digest Friday's US employment numbers, which were a mix. Nonfarm Employment Change softened in November, but the reading of 228 thousand easily beat the estimate of 198 thousand. However, Average Hourly Earnings, which measures wage growth, came in at 0.2%, shy of the estimate of 0.3%. Analysts remain stumped as to why wages remain stubbornly low, given a red-hot labor market which is running at full capacity. On an annual basis, wages rose 2.5%, short of the forecast of 2.7%. The Fed is also concerned with the lack of wage growth, and this could have a significant effect on monetary policy – if wage growth and inflation shows improvement in 2018, the Fed could raise rates up to three times in 2018.

Will the real Kuroda please stand up? Bank of Japan Governor Haruhiko Kuroda has been sending mixed signals over the BoJ's monetary policy. Kuroda has insisted that there will be no reduction of stimulus until the Bank's inflation target of 2% is met. Still, there has been pressure on him to reconsider, given the marked improvement in Japanese economy this year. However, the governor has recently dropped subtle hints about easing monetary policy. Last week, Kuroda said that a change in economic conditions could lead the BoJ to raise its yield target, which would be a significant change to current policy. Kuroda noted that an exit from quantitative and qualitative easing would be "quite an important topic" to communicate to the markets. Although the BoJ is unlikely to tighten policy before next year at the earliest, these deliberate hints indicated that the Bank is preparing for a time when conditions will warrant tightening monetary policy, after years of an ultra-accommodative stance.

UK Inflation Expected to Remain at Multi-Year High; Implications for BoE and Sterling

The UK will see the release of November inflation figures at 0930 GMT on Tuesday. Annual inflation is expected to grow by 3.0%, the same more-than-five-year-high pace that was recorded in October and September. The pace of inflation has implications for the rate hike path that is to be implemented by the Bank of England.

Month-on-month, CPI is anticipated to have grown by 0.2% in November, exceeding the 0.1% pace that was recorded in October, while the 3.0% y/y rate projected by analysts compares to the BoE's target rate for inflation of 2.0%. Core inflation, the measure that excludes volatile food and energy items, is expected to grow by 2.7% on an annual basis in November, the same as in the preceding three months which is also the highest since late 2011.

An upside deviation from inflation forecasts is expected to push sterling higher as market participants will likely push their expectations for an additional rate hike by the BoE - after the one delivered in early November - closer rather than later in time. In such an event, resistance to up movements in price could come at around the 11-week high of 1.3549 that was recorded on December 1. Notice that late September's 17-½-month high of 1.3656 lies not far above this level - the area around this peak could act as a barrier to stronger bullish movements further ahead by the pair. For the record, markets currently expect the BoE to hike rates by 25 bps - for the bank's target rate to reach 0.75% - by late 2018.

Should inflation forecasts fall short of expectations, then sterling will likely weaken as more questions about how fast the central bank will deliver additional interest rate increases would emerge. A declining pound/dollar could meet support around the current level of the 50-day moving average at 1.3243.

One should not forget though that in the case of the UK, things are not as "binary" as might be in the US or the eurozone for example where inflation is running below the respective central banks targets and where a higher reading would definitely be welcome. In the UK, higher-than-anticipated inflation might raise hopes for interest rate hikes to be delivered sooner, but is also eating out of consumers' purchasing power (as inflation is outpacing wage growth), affecting their spending habits and thus the outlook for growth which either way is not looking that bright at the moment; a weakening growth outlook is also acting to the detriment of the outlook for monetary policy normalization. Besides this, it should be taken into account that other releases out on Tuesday also have the capacity to move sterling. Producer prices and retail price inflation (a measure used to calculate payments on instruments such as index-linked government bonds and other contracts such as indexed-pensions) for November will me made public at the same time as the aforementioned CPI figures.

Other forces driving sterling throughout the week are of course developments on the Brexit front. Following last week's breakthrough, it is expected that by the end of the EU summit taking place on Dec. 14-15, the EU heads of state will formally decide that negotiations should move to the second stage, that of determining the future relationship - including trade talks - between Britain and the EU. In terms of data, Wednesday will see the release of November's claimant count, as well as October's unemployment rate and average earnings. Linking the latter to what was previously mentioned, it would be interesting to see to what extent the divergence between price pressures and wage growth, which acts to the detriment of households' purchasing power, continues. Thursday will see the release of November's retail sales while the completion of the BoE's two-day meeting on monetary policy will complement the day. The bank is widely expected to hold its benchmark rate steady at 0.5%.