Sample Category Title

Bitcoin Opens For Future Business

Monday December 11: Five things the markets are talking about

Central Banks will again dominate proceedings this week while economic data is on the thin side.

Within in the G10, four central banks meet this coming week including the Fed, the Bank of England (BoE), Swiss National Bank (SNB) and Norway's Norges bank.

Only the Fed is expected to change its interest rate on Wednesday (2 pm EDT) after last Friday's non-farm payroll (NFP) report showed robust job growth, supporting U.S economic conditions and a solid labor market that policy makers hope will eventually “fan inflation.” Fixed income traders have priced in a +25 bps hike in the fed funds to +1.5%.

On Thursday, the market is anticipating the ECB (07:45 am EDT) to divulge details of how it will begin to taper its monthly asset purchases (QE) beginning in the New Year. While the BoE (07:00 am EDT) is widely expected to keep its key rate on hold after last months increase.

Also this week, among the top U.S economic reports are consumer inflation on Wednesday and retail sales on Thursday. While in Europe, lawmakers continue to debate Brexit and weigh moves on the next step, while NAFTA negotiators meet again.

Elsewhere, in Japan, the Q4 Tankan survey will be monitored closely especially after the healthy revised Q3 GDP estimate, while in the U.K, November labor market report dominates Wednesday.

1. Stocks grind higher

Ahead of the U.S open, Euro equities are following their Asian counterparts higher, after another record close in the U.S on Friday.

In Japan, stocks hit a fresh 25-year high overnight in choppy trade as gains in financial shares and large cap stocks offset falls in real estate and construction companies. The Nikkei share average ended +0.6% higher, while the broader Topix gained +0.5%.

Down-under, Australia's S&P/ASX 200 rallied less than +0.1% despite gains in commodity stocks as most bank majors pulled back. In South Korea, the Kospi closed out little changed.

In Hong Kong, stocks rose the most in nearly three-weeks overnight, as index heavyweight Tencent (telecommunication conglomerate) rebounded for the third consecutive session. At close of trade, the Hang Seng index was up +1.14%, while the Hang Seng China Enterprises index rose +1.26%.

In China, stocks rebound as Beijing considers impact of new asset management rules. The Shanghai Composite index was up +0.98%, while the blue-chip CSI300 index was up +1.65%.

Note: Chinese equities plummeted in November after Beijing issued draft guidelines to tighten rules on the asset management industry, in its latest step to fend off 'systemic risks' from the country's growing shadow banking sector.

In Europe, regional indices are off their highs and trading mixed, with the exception of notable strength in the FTSE100 trading higher by over +0.5%.

U.S stocks are set to open in the black (+0.1%).

Indices: Stoxx600 flat at 389.3, FTSE +0.6% at 7438, DAX +0.1% at 13162, CAC-40 flat at 5400, IBEX-35 -0.2% at 10306, FTSE MIB -0.2% at 22736, SMI flat at 9322, S&P 500 Futures +0.1%

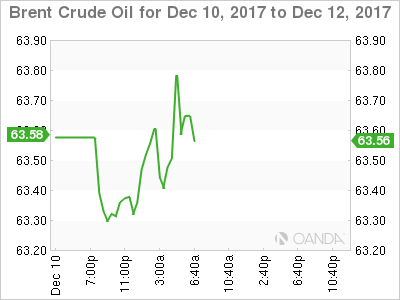

2. Oil prices slip, under pressure from U.S. drilling, gold higher

Oil prices have edged a tad lower as ongoing output cuts led by OPEC are being countered by rising U.S drilling activity that points to a further increase in U.S production.

Brent crude futures are -15c lower at +$63.25 a barrel, while U.S West Texas Intermediate (WTI) crude futures are at +$57.03 a barrel, down -33c from Friday's close.

Note: Both Brent and WTI crude oil settled more than +1% higher on Friday, and oil prices have gained well over a third in value from their 2017 lows.

The gains are largely due to production cuts by the OPEC and non-OPEC producers, including Russia, which have been in place since the start of 2017.

However, the effect of these cuts are being undermined by rising output from the U.S, which is not participating in the deal to voluntarily withhold production.

Data on Friday from Baker Hughes noted that the number of rigs drilling for new oil output in the U.S rose by +2 in the week to Dec. 8, to +751, the highest level since September.

Note: Kuwait's oil minister said yesterday that OPEC and other oil producers would study before June the possibility of an exit strategy from the oil supply-cut agreement.

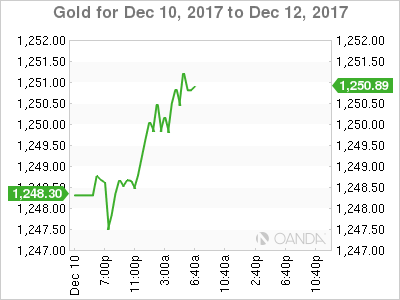

Gold prices have ticked up a tad amid a softer dollar ahead of the U.S open, but the 'yellow' metal lacks impetus to push higher weighed by expectations of a Fed interest rate hike Wednesday stateside. Spot gold is up +0.2% at +$1,249.90 an ounce.

Note: Gold printed its lowest price since July 26 at +$1,243.71 last week.

3. Sovereign yields diverge

The gap between the benchmark German Bund and the U.S 10-year Treasury yield are close to it's widest in seven-months ahead of the U.S open as the fiscal and policy paths diverge. The U.S/ German 10-year yield gap reached +208 bps earlier this morning, just shy of the +209 bps eight-month high hit earlier in December.

The paths are expected to deviate even further as President Trump pushes a tax overhaul that could put the U.S economy at risk of overheating and reason why fixed income traders are starting to price in multiple rate hikes from the Fed in 2018, after an almost-certain hike this week.

Note: Despite pressure from the divergence being most pronounced in the short end of the yield curve, the U.S Treasury curve is close to its flattest in a decade. However, the long-end is being impacted particularly after the risk of a U.S government shutdown last weekend was averted.

The yield on U.S 10's is unchanged at +2.38%, the highest in more than a week. While in Germany, 10-year Bund yield has fallen -1 bps to +0.30%, while in the U.K the 10-year Gilt yield decreased -2 bps to +1.257%.

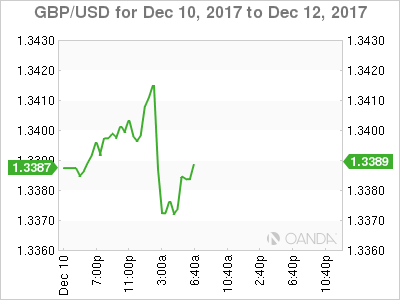

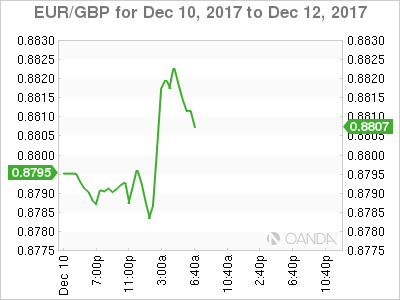

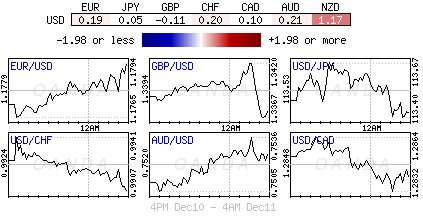

4. Sterling back to pre-Brexit breakthrough levels

FX markets are expected to remain range bound ahead of a plethora of rate decisions on Thursday. Aside from the Fed (Wednesday), within the G10, there is the BoE, Norges and SNB on Thursday. While in emerging markets there will be Indonesia, Philippines, Turkey, Colombia, Mexico and Chile deciding on rates.

Amongst the majors, sterling (£1.3375) is back to trading around the levels it was before the E.U said sufficient progress has been made to move on to trade negotiations with the U.K on Friday.

The pound reached a peak on Friday of £1.3521 outright, and €0.8690 per Euro. To many, it remains unclear exactly what progress has been made, especially regarding the Irish border. Weekend press includes a report that a number of non-EU countries have voiced their displeasure at the prospect of the U.K getting a special deal.

Elsewhere, the EUR trades atop of the €1.1800 handle, while USD/JPY is little changed at ¥113.38.

5. Bitcoin open for 'future' business

Trading in Bitcoin futures began in Tokyo last night, as Cboe Global Markets became the first major exchange to offer the contracts pegged to the cryptocurrency.

Similar contracts will start trading in a week on the CME Group – it's a test whether institutional money will go after Bitcoin, which so far has mainly attracted individual investors.

Note: The virtual currency has divided opinions among financial executives and central bankers worldwide about its legitimacy as an asset.

Immediate introduction saw prices for the volatile cryptocurrency jump back above +$15,000 and within four hours had eclipsed +$16,000. Just 24 hours earlier, Bitcoin had been at +$13,000. It was recently trading at around +$16,400.

Euro Edges Higher As Markets Digest Mixed US Jobs Data

The euro has ticked higher to start the week. In the Monday session, EUR/USD is trading at 1.1794, up 0.20% on the day. On the release front, there are no major eurozone events. The US will release JOLTS Job Openings, which is expected to drop to 6.03 million. On Tuesday, we’ll get a look at ZEW Economic Sentiment reports out of Germany and the eurozone, and ECB President Mario Draghi will speak at an event in Frankfurt. The US will release PPI, an important inflation indicator.

There was positive news for Prime Minister Theresa May on Friday, as EU Commissioner Jean-Claude Juncker announced that sufficient progress had been made on non-trade issues in the Brexit talks. The announcement came as May was able to get both the Irish government and the DUP party on board, after she promised both that Northern Ireland would not have any hard borders after Brexit. This breakthrough means that Britain and Europe can now move to Phase II and discuss trade relations. With Britain scheduled to leave the EU in March 2019, time is of the essence. What will a new trade relationship look like? On Sunday, Brexit minister David Davis said he envisions a comprehensive trade deal with Europe, which would be signed just after Britain leaves the bloc. The EU recently signed a free-trade treaty with Canada, and Davis said that he wants an agreement “Canada plus plus plus”, meaning that the deep trading ties between the sides and access to European markets would remain intact.

The markets continue to digest Friday’s US employment numbers, which were a mix. Nonfarm Employment Change softened in November, but the reading of 228 thousand easily beat the estimate of 198 thousand. However, Average Hourly Earnings, which measures wage growth, came in at 0.2%, shy of the estimate of 0.3%. Analysts remain stumped as to why wages remain stubbornly low, given a red-hot labor market which is running at full capacity. On an annual basis, wages rose 2.5%, short of the forecast of 2.7%. The Fed is also concerned with the lack of wage growth, and this could have a significant effect on monetary policy – if wage growth and inflation shows improvement in 2018, the Fed could raise rates up to three times in 2018.

USD Reverses Gains Ahead Of Central Banks’ Week

Busy week for central bankers

The US dollar ended last week on a solid footing with the dollar index testing the 94.16 resistance area (high from November 21) on Friday. However, the greenback seems to have lost momentum on Monday morning. The Federal Reserve, which will hold its last meeting of the year this week, is expected to lift borrowing costs by 25bps. market participants have already priced in the decision. The 3m LIBOR has risen to 1.44% since mid-November, an increase of 20bps. According to the Fed funds futures, there is a 98% probability of a 25bps increase.

Therefore, investors will focus on the updated forecast for economic growth and interest rates. According to the last forecast, which was released in September, Fed members are expecting three rate hikes next year. A downward revision would send a very dovish message to investors, which would translate into a USD sell-off. Over the last few months, Fed members have systematically avoided to take strong positions regarding the monetary policy outlook. We anticipate that this behaviour will persist.

The ECB is also holding its last meeting of the year. We do not expect much from this meeting as it will likely be a non-event. The focus will be on Draghi’s press conference, which will follow the rate decision, and the updated inflation projections. We anticipate that Draghi will maintain his traditional neutral and cautious tone to avoid strengthening the euro.

EUR/USD fell more than 1% last week as the USD extended gains across the board. The single currency started the week on a firmer footing with EUR/USD climbing back to 1.18. We maintain our medium and long-term bullish view on the pair with the 1.25 target as first objective.

Futures push Bitcoin price higher

It was a widely awaited event that took place yesterday. It is now possible to trade futures on the first digital currency on the CBOE and CME platform. Bitcoin is becoming more and more mainstream and smart money have now all the tools to get into it. Contrary to many people’s expectations, the Bitcoin price has not collapsed amid the introduction of futures trading and has actually surged.

However, the weekend was tough for Bitcoin with a very strong volatility. Fears are that the institutional are going to enter short Bitcoin position and that futures will artificially increase the Bitcoin supply as what is happening for Gold. It is also important to note that the settlement will be cash and not in Bitcoin. We firmly believe that futures may weigh in a longer run on the Bitcoin price. Yet, the Bitcoin price has not reached its top yet and we may see insane prices within the next couple of years.

In the short-term the greed will still prevail and this is pushing the Bitcoin price higher. For the time being, many investors are still rushing into it. The Bitcoin price is ready to challenge the 17k level anytime soon.

Market Update – European Session: Quiet Start To A Jammed Central Bank Rate Decision Week

Notes/Observations

Plethora of central bank decisions later this week.

Asia:

China Nov CPI M/M: 0.0% v 0.1% prior; Y/Y: 1.7%vV 1.8%e

China said to be considering delaying asset-management product rules to end of 2020 (**Note: On Dec 7th reports circulated that 10 Chinese banks pushed back on new asset management rules in closed meeting. Banks noted that rules on breaking implicit guarantee could trigger liquidity risk, increase market volatility. Requested to extend transition period to 3 years

Japan Govt expected to upgrade its FY18/19 GDP forecast of 1.4% to ~2% with an expanding global economy seen boosting exports and capital investment expected to remain firm

Europe:

Michael Gove (Environment Min) and Boris Johnson (Foreign Min) to insist that PM May presses for a hard Brexit when Britain begins trade negotiations. Stance would be payback for their support for her deal last week

UK British Chamber of Commerce (BCC) Quarterly Economic Outlook: Trimmed growth forecast for 2017 thru 2019 citing continued uncertainty over Brexit

La Vanguardia poll on Catalan Regional elections: Pro-independence parties seen gaining 66-67 seats compared to 72 seats in prior regional ballot (held in 2015)

Energy:

UAE Energy Min Al Mazrouei: Next year will be better for oil market; OPEC/nOPEC plan to announce exit strategy from supply cuts in June does not mean we will exit in June

Kuwait Oil Min Almarzooq: production cuts may end before 2019 if the market re-balances by June next year

Economic Data:

(NO) Norway Nov CPI M/M: 0.1%0.2%e; Y/Y: 1.1% v 1.2%e

(NO) Norway Nov CPI Underlying (ATE) M/M: -0.3% v 0.0%e; Y/Y: 1.0% v 1.2%e

(TR) Turkey Q3 GDP Q/Q: 1.1% v 1.8%e; Y/Y: 11.1% v 8.5%e

(TR) Turkey Oct Current Account: -$3.8B v -$4.1Be

(DK) Denmark Nov CPI M/M: -0.3% v -0.1%e; Y/Y: 1.3% v 1.5%e

(DK) Denmark Nov CPI EU Harmonized M/M: -0.3% v -0.1%e; Y/Y: 1.3% v 1.5%e

(FR) Bank of France Nov Business Sentiment: 106 v 107e

(CZ) Czech Nov CPI M/M: 0.1% v 0.1%e; Y/Y: 2.6% v 2.7%e (12th straight reading at or above the central bank's target)

(IT) Italy Oct Retail Sales M/M: -1.0% V 0.0%e; Y/Y: -2.1% v 3.1% prior

(CN) China Nov Aggregate Financing (CNY) 1.600T v 1.225Te

(CN) China Nov M2 Money Supply Y/Y: 9.1% v 8.9%e

(CN) China Nov New Yuan Loans (CNY): 1.12T v 800Be

(BR) Brazil Dec IGP-M Inflation (1st Preview): 0.7% v 0.7%e

Fixed Income Issuance:

(SE) Sweden sold SEK2.33B in 0.25% I/L 2022 bond; Avg Yield: -2.0678%

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 flat at 389.3, FTSE +0.6% at 7438, DAX +0.1% at 13162, CAC-40 flat at 5400, IBEX-35 -0.2% at 10306, FTSE MIB -0.2% at 22736, SMI flat at 9322 , S&P 500 Futures +0.1%]

Market Focal Points/Key Themes: European Indices trade mixed this morning with notable strength in the FTSE100 trading higher by over 0.5%. European Indices are off the highs after initial strength following on from a positive session in Asia. Shares of Steinhoff has seen a rebound after heavy losses in the past few sessions after Chairman is in talks with lenders to seek a standstill on a €1.5B margin loan, as well as appointing an international advisory team. In the Healthcare space Argenx, PharmaMar and Mereo Biopharma trade higher after positive trial results, while Hollywood Bowl trades sharply higher after strong Full year results. In the M&A Space Apollo partner and Archer Daniels reportedly look to bid for Unilever's spread business, whilst Apple is said to be nearing a deal to acquire music app developer Shazam.

Equities

Consumer discretionary [ Steinhoff [SNH.ZA] +20% (Appoints international advisory team), Hollywood Bowl [BOWL.UK] +9.5% (Earnings)]

Financials: [ Investec [INVP.UK] +3% (comments on exposure to Steinhoff)]

Healthcare: [ Argenx [ARGX.BE] +16% (Reports positive topline results from Phase 2 proof-of-concept trial of ARGX-113 (efgartigimod) in generalized myasthenia gravis), Pharmar [PHM.MAC] +18% (Positive results from Admyre Phae III pivotal trial), Mereo Biopharma [MPH.UK] +4% (Positive trial data)]

Speakers

ECB's Nowotny (Austria): ECB must be careful in unwinding low interest rates

ECB's Nouy (SSM chief): NPL rules may be final a month or two later, large majority of euro countries support NPL plans

UK Brexit Minister Davis: Could avoid hard border with Ireland whatever the outcome of Brexit trade talks. Brexit transition might last 21 months

Poland Central Bank's Sura: No reason to change rate stance based upon data. Saw 2017 GDP growth above 4.5%

China Foreign Min Wang: China, India and Russia to deepen economic and strategic relations -

Currencies

FX markets were quiet ahead of a plethora of rate decisions on Thursday. Within the G10 there are BOE. Norges and SNB on Thursday. In Emerging markets there will be Indonesia, Philippines, Turkey, Colombia, Mexico and Chile deciding on rates

Fixed Income

Bund futures trade 163.50 up 4 ticks, holding up comfortably and near the December highs. Continued downward pressure sees 162.10 followed by 161.50. A reversal targets 163.75 then 164.33.

Gilt futures trade at 125.55 up 46 ticks, sliding amid PM May's Brexit truce is under pressure. Continued upside eyeing 125.75 then 126.35. Downside targets include 124.25 then 123.75.

Monday's liquidity report showed Friday's use of the marginal lending facility fell to €135M from €146M prior.

Looking Ahead

(RU) Russia Q3 Preliminary GDP (2nd reading) Y/Y: 1.8%e v 1.8% advance reading

(IL) Israel Central Bank (BOI) Nov Minutes

(MX) Mexico Nov ANTAD Same-Store Sales Y/Y: No est v 2.1% prior

05:25 (BR) Brazil Central Bank Weekly Economists Survey

05:30 (NL) Netherlands Debt Agency (DSTA) to sell Bills

06:00 (IL) Israel Nov Consumer Confidence: No est v 128 prior

06:00 (PT) Portugal Oct Trade Balance: No est v -€1.2B prior

06:30 (TR) Turkey TCMB Survey of Expectations

06:45 (US) Daily Libor Fixing

08:00 (PL) Poland Nov Final CPI M/M: No est v 0.5% prelim; Y/Y: No est v 2.5% prelim

08:05 (UK) Baltic Dry Bulk Index

08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming actions in week

08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

08:30 (CH) Swiss Government Question Time in Parliament

08:55 (FR) France Debt Agency (AFT) to sell combined €5.2-6.4B in 3-month, 6-month and 12-month BTF Bills

09:30 (EU) ECB announces Covered-Bond Purchases

09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

10:00 (US) Oct Oct JOLTS Job Openings: No est v 6.093M prior

11:30 (US) Treasuries to sell to 3-month and 6-month bills

13:00 (US) Treasuries to sell 3-Year Notes

13:00 (US) Treasuries to sell 10-Year Notes Reopening

16:00 (US) Weekly Crop Progress Report

Central Banks In Focus This Week

It's been another quiet start to trading in what is otherwise going to be a very busy week in financial markets, with a number of central banks scheduled to make interest rate announcements.

The Federal Reserve, ECB and Bank of England will be among those meeting this week, which should make Wednesday and Thursday particularly lively. Of these, only the Fed is expected to announce a change, with another 25 basis point rate hike all but priced in. That will take the number of hikes this year to three, as per its forecast towards the back end of last year, which markets were initially behind the curve on.

That currently remains the case for 2018, with the Fed projecting three more and markets only anticipating one or two. The most interesting thing on Wednesday is likely to be what the central bank says on this and whether the dot plot continues to forecast three hikes. With so many unknowns – vacant positions on FOMC and tax reform to name a couple – expectations are likely to change over the next six months, impacting how many rate hikes we actually get.

The BoE and ECB meetings are likely to be a more uninteresting affair, with both central banks having only recently tightened monetary policy and in no rush to do so again. That said, the ECB press conference can often be a volatile period for markets and traders will be keen to know what the next steps are beyond quantitative easing.

Friday's agreement between Theresa May and Jean-Claude Juncker on phase one of Brexit negotiations was an important milestone but this is likely to remain heavily in the news this week, with the European Council due to vote on it on Friday. While this is expected to be a formality, should anything get in the way of the vote being passed, it would be a major setback for the negotiations and prevent them moving onto phase two, in which the future trade relationship will be discussed.

Bitcoin won't be far from the headlines this week, despite attention potentially being diverted elsewhere at times, with volatility in the cryptocurrency remaining at extraordinary levels over the weekend as CBOE prepared to launch its first futures contract. Still, Bitcoin is back trading near record highs this morning, allaying fears for now that the ability to short would trigger a sell-off.

Technical Outlook: WTI Oil – Limited Downside Risk While Rising Daily Kijun-Sen Holds Dips

WTI Oil price edged lower on Monday after strong rally on Thu/Fri which peaked at $57.77, retracing over 61.8% of $58.86/$55.81 bear-leg.

Today's action was so far shaped in Doji candle and holding between daily Kijun-sen ($56.91) and Tenkan-sen ($57.34), which suggests no immediate downside threats while Kijun-sen line holds.

Negative near-term sentiment rose on renewed concerns about rising US oil output, after data on Friday showed that the number of US oil drilling rigs rose to the highest since September.

Overall picture is still bullish and favors further recovery off $55.81 (07 Dec trough). Initial bullish signal is seen on break above daily Tenkan-sen, with close above $57.69 (Fibo 61.8% of $56.86/$55.81) needed to confirm scenario.

Conversely, loss of Kijun-sen support would risk deeper pullback and would expose key near-term support at $55.81.

Res: 57.34, 57.77, 58.14, 58.66

Sup: 56.91, 56.53, 56.06, 55.81

CRUDE OIL Short-Term Decrease

Crude oil continues its consolidation phase and should not challenge the 60-dollar level anytime soon. Expected to show continued bearish move. Support is given at a distance at 54.81 (14/11/2017 low).

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

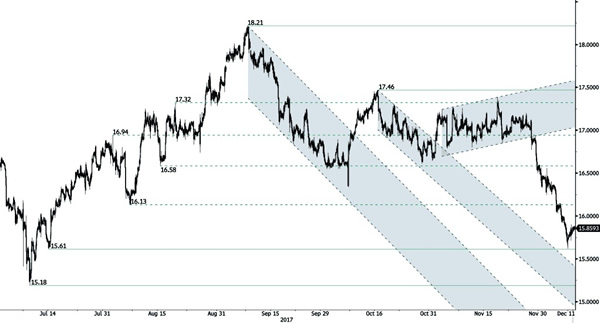

SILVER Bouncing On Support

Silver has been bouncing on hourly support at 15.61 (14/07/2017 low). Hourly resistance is given at 17.46 (13/10/2017 high). Expected to keep pushing lower.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

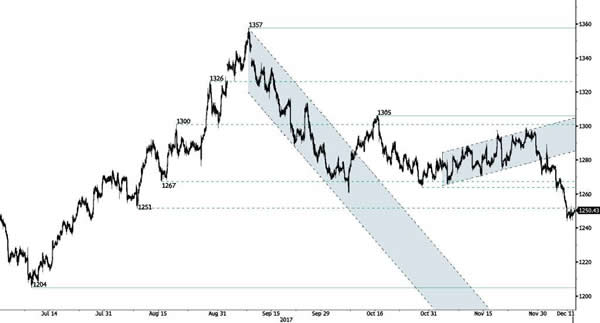

GOLD Consolidating Below 1250

Gold is now consolidating after strong collapse. The technical structure confirms a further consolidation phase. Support given at 1251 (08/08/2017 high) has been broken. Resistance is located at 1288 (20/10/2017).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Ready For Another Upside Move

Bitcoin's bullish momentum is far fom over. The technical structure has shown a tremendous positive short-term momentum. Hourly support is located below 14k (08/12/2017 low). Strong support stands very far at 2975 (22/08/2017 low). In the short-term, the digital currency should continue rising at levels unseen so far.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $40'000 in 2018.