Sample Category Title

EURUSD Turning Bullish Above 1.1790 Level

The euro continues to press higher against the U.S dollar, with the pair hitting 1.1803 during the European trading session. The EURUSD is benefiting from U.S dollar index weakness on Monday, as investors remain concerned about persistently weak inflation within the U.S economy. With a lack of macroeconomic data on Monday, traders will be increasingly focused on the key technical areas. The 1.1790 remains key for the euros next directional move, likewise the 93.60 support level is important for the U.S dollar index.

The EURUSD pair is turning intraday bullish above the 1.1790 level, further upside towards the 1.1815 and 1.1860 levels appears possible. The 1.1900 level offers extended weekly resistance.

If the EURUSD pair fails to hold above the 1.1790 level, the 1.1750 technical level remains the most relevant support area for traders.

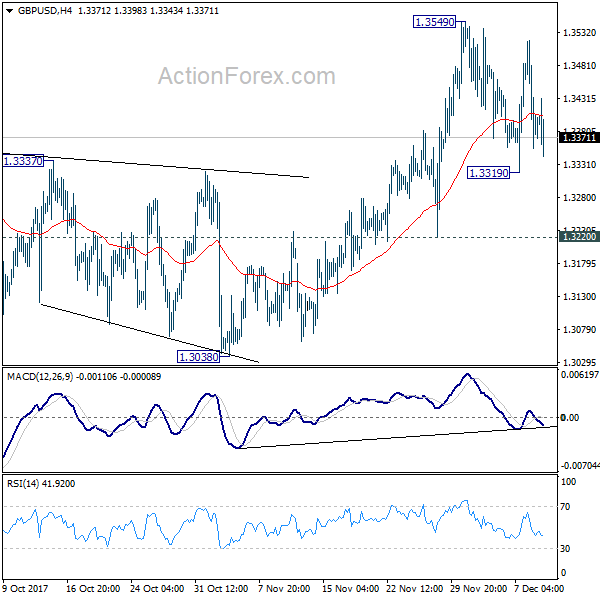

GBPUSD Intraday Bearish Below 1.3400 Level

The British pound remains under downside pressure against the U.S dollar after EU officials expressed concerns that the UK will be unable to finish Brexit trade negotiations, before finally exiting EU on March 2019. The GBPUSD pair currently trades around the 1.3390 level, after dipping towards the 1.3340 support level earlier this morning. The pair is likely to become increasingly volatile as the trading week progresses, with both the FED and BOE deciding on interest rates, amidst ongoing Brexit trade negotiations in Brussels.

The GBPUSD pair remains bearish while trading below the 1.3400 level, further downside towards the 1.3340 and 1.3320 levels seems likely.

Should GBPUSD buyers move price-action above the 1.3400 technical level, further buying towards the 1.3470 and 1.3550 levels remains possible.

GBPUSD: Bearish, Looks To Weaken Further

GBPUSD: The pair closed lower the past leaving risk of more weakness on the cards in the new week. Support lies at the 1.3350 level where a break will turn attention to the 1.3300 level. Further down, support lies at the 1.3250 level. Below here will set the stage for more weakness towards the 1.3200 level. Conversely, resistance stands at the 1.3450 levels with a turn above here allowing more strength to build up towards the 1.3500 level. Further out, resistance resides at the 1.3550 level followed by the 1.3600 level. On the whole, GBPUSD looks to pullback further.

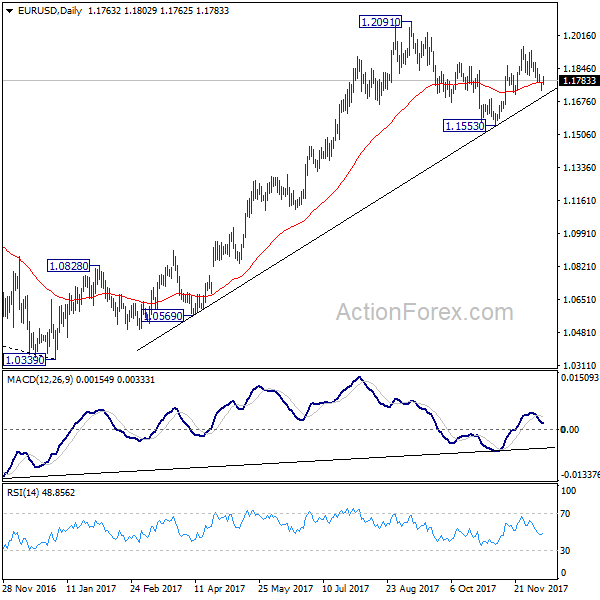

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1739; (P) 1.1758 (R1) 1.1786; More....

Intraday bias in EUR/USD is neutral for the moment with focus on 1.1712 cluster support (61.8% retracement of 1.1553 to 1.1960 at 1.1708). Decisive break there will indicate that rebound from 1.1553 has completed at 1.1960. In that case, deeper fall would be seen to 1.1553 and possibly below to extend the decline from 1.2091. Meanwhile, with 1.1712 support intact, break of 1.1814 minor resistance will retain near term bullishness. And in that case, intraday bias will be turned back to the upside for 1.1960. Break will target 1.2091 high.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1423) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

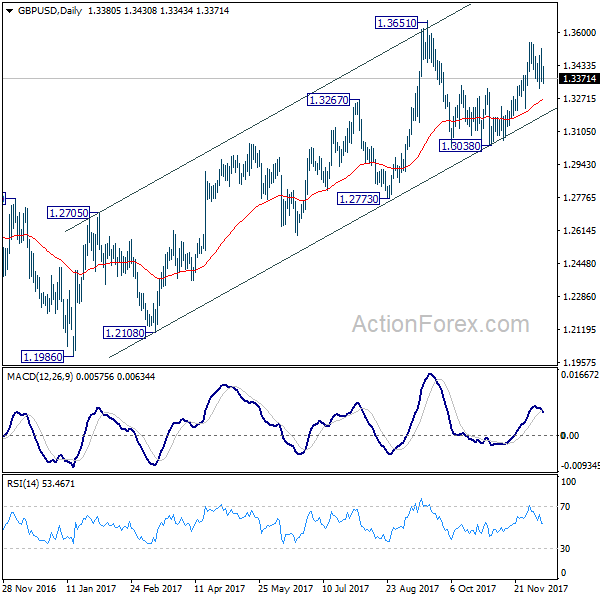

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3314; (P) 1.3417; (R1) 1.3480; More....

Intraday bias in GBP/USD remains neutral for the moment. We'll slightly favor another rise as long as 1.3220 support holds. Break of 1.3549 will target 1.3651 high next. However, firm break of 1.3220 will turn near term outlook bearish for 1.3038 key support level.

In the bigger picture, while the medium term rebound from 1.1946 low was strong, it's limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

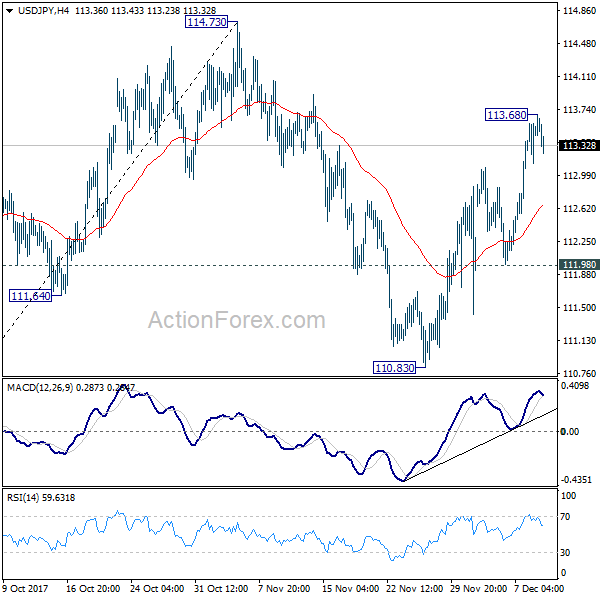

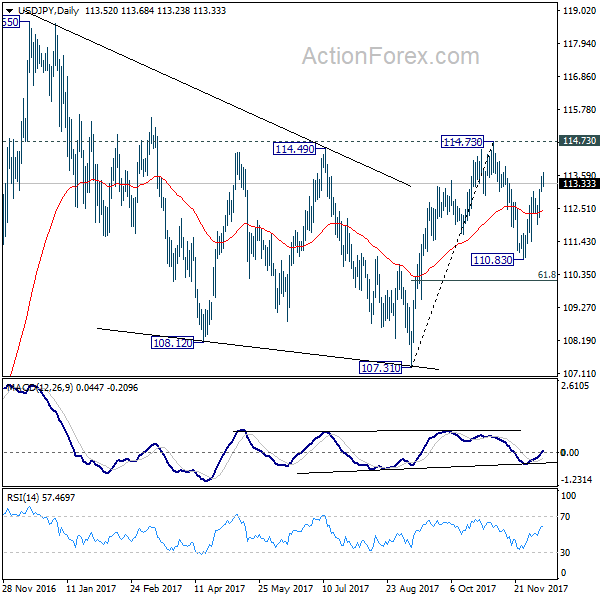

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.16; (P) 113.37; (R1) 113.67; More...

A temporary top is in place at 113.68 in USD/JPY and intraday bias is turned neutral for consolidation. Further rally is expected as long as 111.98 support holds. Above 113.68 will target 114.73 resistance first. Decisive break there will resume whole rise form 107.31. More importantly, that will confirm completion of medium term correction from 118.65 at 107.31. In that case, retest of 118.65 should be seen next. However, break of 111.98 support will extend the correction from 114.73 with another fall, possibly to 61.8% retracement of 107.31 to 114.73 at 110.14 before completion.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed a 107.31. And medium term rise from 98.97 (2016 low) is resuming. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

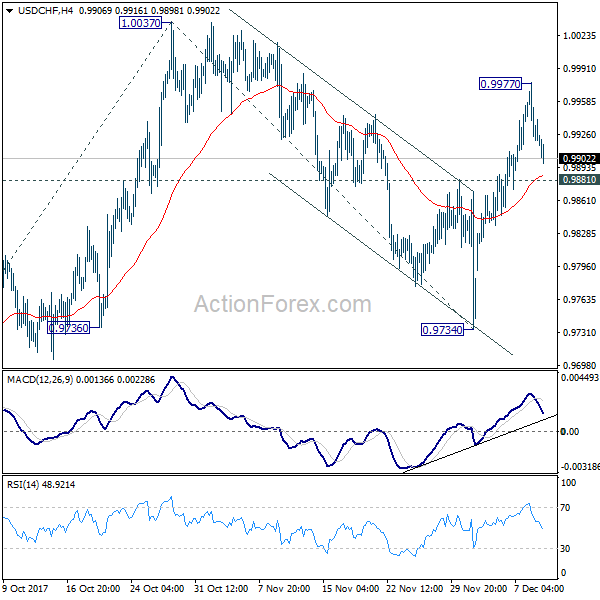

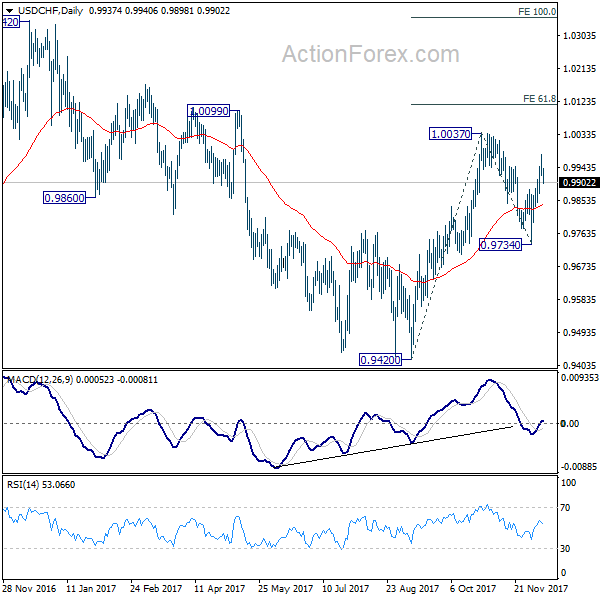

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9901; (P) 0.9939; (R1) 0.9958; More....

USD/CHF's retreat from 0.9977 temporary top extends lower. But intraday bias remains neutral. We'd holding on to the view that correction from 1.0037 has completed at 0.9734 already. Also, rise from 0.9420 might be resuming. On the upside, above 0.9977 will target 1.0037 high first. Break will extend the rise from 0.9420 to 61.8% projection of 0.9420 to 0.9734 from 1.0047 at 1.0115 next. Nevertheless, firm break of 0.9881 support will dampen this immediate bullish case and turn bias to the downside for 0.9734 instead.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

New Zealand Dollar Surged on RBNZ Governor Appointment, Dollar Turns Cautious

New Zealand dollar is the star performer today as markets respond very positively to the appointment of the new RBNZ governor. Strength in the Kiwi also took Aussie generally higher. Meanwhile, Dollar is paring recent gains against all but Sterling and Loonie. Dollar traders are cautiously adjusting their positions ahead of the FOMC rate hike and new forecasts on Wednesday. But it's Sterling who's the weakest and impact from Brexit breakthrough faded. More volatility is anticipated ahead with Fed, ECB, BoE and SNB meeting this week, in addition to heavy weight data like US and UK CPI.

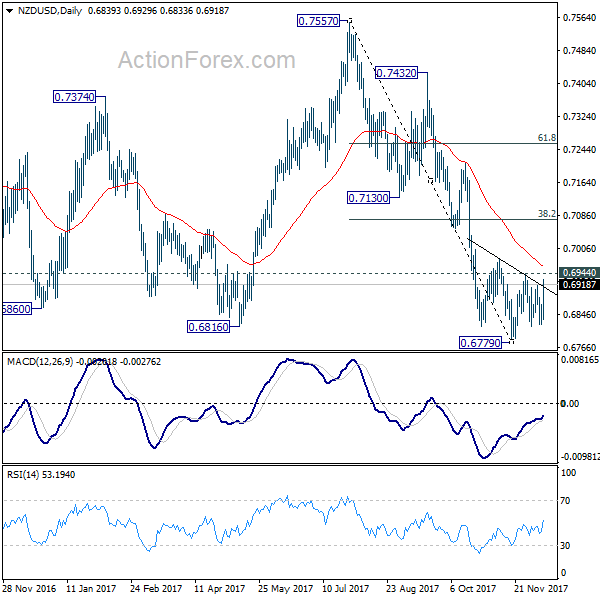

Kiwi surges on RBNZ Governor appointment

New Zealand Dollar responds very positively today after Finance Minister Grant Robertson named Superannuation Fund chief Adrian Orr as the next RBNZ Governor, beginning March 27. Orr was also a former RBNZ Deputy Governor and chief economist. Economist are skeptical on the Labour led government's idea of reforming RBNZ and transit it to Fed-style dual mandate. That is, price stability and full employment would both be the central bank's targets. And some worried that it would make it much harder for RBNZ to raise interest rates. However, Orr's employment, with his background, provides some certainty that the reform and transitions will be practical and realistic, rather pure political ideology driven.

NZD/USD breached 0.6816 key support to 0.6779 back in November but quickly recovered. Current development argues that it could be completing a head and shoulder bottom pattern. With today's rebound, focus is back on 0.6944 resistance. Break there should at least bring rebound to 38.2% retracement of 0.7557 to 0.6779 at 0.7076.

ECB Nouy: Banks M&A to accelerate

ECB Supervisory head Daniele Nouy said in a newspaper interview that merger and acquisitions in the Eurozone banking sector will acceleration ahead. She said that "with growth returning and with the huge amount of work that is being done in relation to non-performing loans, we are going to see a number of mergers taking place within countries and across borders." Meanwhile, ECB's plan on bad loans may be delayed after hearing the negative feedback from the industry. But she emphasized that "it doesn't change much whether it happens on say 1 January, 1 April or 1 June,"

David Davis stirring things up after last week's Brexit deal

Just two days UK Prime Minister Theresa eased her nerve with the Brexit deal with EU, Brexit Secretary David Davis seemed to be stirring up the issues again. Davis told BBC that UK won't be paying the divorce bill if there is no trade deal. He said "it is conditional on an outcome. It is conditional on getting an implementation period, it is conditional on a trade outcome." This is the exact opposite of what Chancellor Philip Hammond told a parliamentary committee last week. Hammond did say that "nothing is agreed until everything is agreed in this negotiation." But he also said "I find it inconceivable that we as a nation would be walking away from an obligation that we recognized as an obligation." Hammond also emphasized that "that is not a credible scenario. That is not the kind of country we are. Frankly, it would not make us a credible partner for future international agreements."

Japan business conditions improved

In Japan, the Ministry of Finance's business survey index (BSI) showed generally improved business conditions. For large corporations, with capital of JPY 1b or above), all industry business conditions improved to 6.2, up from 5.1. Large manufacturing conditions rose to 9.7, up from 9.4. Large non-manufacturing business conditions rose to 4.5, up from 2.9.

China CPI slowed, ease pressure for tightening

In China, CPI slowed to 1.7% yoy in November, down from 1.9% yoy and missed expectation of 1.8% yoy. PPI also dropped to 5.8% yoy, down from 6.9% yoy and met expectations. Slowing inflation is seen as welcomed by both the authority and the markets. The data suggests that China is in no rush to raise interest rate or tighten up monetary policies.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9901; (P) 0.9939; (R1) 0.9958; More....

USD/CHF's retreat from 0.9977 temporary top extends lower. But intraday bias remains neutral. We'd holding on to the view that correction from 1.0037 has completed at 0.9734 already. Also, rise from 0.9420 might be resuming. On the upside, above 0.9977 will target 1.0037 high first. Break will extend the rise from 0.9420 to 61.8% projection of 0.9420 to 0.9734 from 1.0047 at 1.0115 next. Nevertheless, firm break of 0.9881 support will dampen this immediate bullish case and turn bias to the downside for 0.9734 instead.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BSI Large All Industry Q/Q Q4 | 6.2 | 5.8 | 5.1 | |

| 23:50 | JPY | BSI Large Manufacturing Q/Q Q4 | 9.7 | 10 | 9.4 | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Nov | 4.00% | 4.10% | 4.10% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Nov P | 46.90% | 49.80% |

SPOT GOLD – Correction Seen as Positioning for FOMC Event

Spot Gold entered corrective mode on Monday after last week's steep fall showed signs of stall, as Friday's trading ended in Doji candle after hitting 4 1/2 month low at $1244.

Doji reversal pattern is forming on daily chart, with deeply oversold slow stochastic on daily chart suggesting further corrective action.

However, limited upside is seen as overall structure remains firmly bearish, with converging 10/200SMA on track to form death-cross and increase downside pressure.

Key event this week, FOMC policy meeting is in focus, with wide expectations of rate hike at Fed's last meeting this year, as Friday's solid jobs data reinforced expectations.

Initial resistance lies at $1252 (Friday's high), ahead of $1256 (Fibo 23.6% of $1299/$1243 downleg), with key barriers at $1265/67 (Fibo 38.2%/200SMA) expected to cap before larger bears resume. Continuation of downtrend from $1357 (2017 high posted on 08 Sep) would focus immediate target at $1240 (50% retracement of larger $1122/$1357 ascend (Dec 2016/Sep 2017) and could extend towards $1212 (Fibo 61.8%) and $1204 (10 July trough).

Res: 1252; 1256; 1260; 1265

Sup: 1246; 1244; 1240; 1235

Dollar Weaker ahead of JOLT’s Job Openings; Stocks Gold Strong

Here are the latest developments in global markets:

FOREX: The pound was steady around $1.3385 despite May saying there is a new "sense of optimism" in the Brexit talks on Monday after she satisfied the European Commission's demand last week on the three key divorce elements. However, the outline agreed must be voted by all European members at Thursday's summit for negotiations to move officially to trade discussions. The dollar was weaker against a basket of major currencies as investors were worried that disappointing wage growth readings released on Friday could negatively affect the Fed's plans to restrict monetary stimulus next year. The kiwi paused its rally around two-week highs of 0.6910 (+1.00%) reached earlier today after the appointment of the new RBNZ governor, Adrian Orr, reduced the chances of a radical change in the country's monetary policy.

STOCKS: The pan-European STOXX 600 index was flat around one-month highs at 1040GMT as gains arising from basic materials and banking shares were offset by losses in the tech sector. The German DAX 30 was 0.22% up on the day, while the British FTSE 100 surged by 0.65%, trading near a two-week high. The Spanish IBEX 35 retreated by 0.20% with most industry sectors in the red.

COMMODITIES: Oil prices were mixed. WTI crude dropped by 0.21% to $57.24 per barrel as concerns over rising US output weighed on the markets, whereas Brent rose by 0.16% to $63.50. In other news, the Saudi Arabian energy minister announced that the state's giant oil producer Aramco will maintain its exports steady at 2017 lows in January. Gold posted soft gains, rising to $1,250.70 per ounce.

Day ahead: JOLTs Job Openings awaited; Fed & US tax deliberation in focus

With the economic calendar lacking major releases, JOLTs Job Openings out of the US will gather some attention at 1300GMT. The survey conducted by the Bureau of Labor Statistics will likely show that the number of positions opened in November will not deviate far away from record highs, inching down by 3,000 to 6,090 million.

However, any potential updates on the progress of the tax legislation as well as any news on monetary policy will likely bring bigger volatility to the markets. Recall that the Fed will kick its last two-day meeting of 2017 on Tuesday with the decision on interest rates being only available on late Wednesday. Although investors are widely expecting policymakers to raise rates by 0.25 percentage points to 1.25%, the monetary statement following the decision will be under the spotlight for any clues on the path of future rate hikes as the central bank recently hinted further tightening next year.

The European Central bank, the Bank of England and the Swiss National Bank will also decide on interest rates on Thursday but no changes on monetary policy are expected to be announced.

In the fiscal front, the US President, Donald Trump will deliver a closing argument on tax cuts on Wednesday as Senate and House Republicans are currently debating to create a common outline that will be signed by Trump as soon as the year-end.