Sample Category Title

Dollar Supported by Fed Officials Comments, But Cautious on Senate Tax Plan

Trading remains rather quiet in the forex markets this week so far. Dollar was supported by upbeat comments from Fed officials regarding a new term rate hike. Jerome Powell also indicated that he preferred continuity when taking over the Fed chair job. But Dollar traders stay cautiously watching how the Republican's tax plan will work out in the Senate this week. Meanwhile, Euro also lost some upside moment ahead of the grand coalition talk between CDU/CSU and SPD. Yen also lacks conviction in this week's rally attempt.

Trading remains rather quiet in the forex markets this week so far. Dollar was supported by upbeat comments from Fed officials regarding a new term rate hike. Jerome Powell also indicated that he preferred continuity when taking over the Fed chair job. But Dollar traders stay cautiously watching how the Republican's tax plan will work out in the Senate this week. Meanwhile, Euro also lost some upside moment ahead of the grand coalition talk between CDU/CSU and SPD. Yen also lacks conviction in this week's rally attempt.

Powell expects interest rates to rise and balance sheet to shrink

Fed chair nominee Jerome Powell released a statement to the Senate Banking Committee before his confirmation hearing today. Powell said in the statement that Fed policy makers "expect interest rates to rise somewhat further and the size of our balance sheet to gradually shrink." Adding to that, he emphasized "while we endeavour to make the path of policy as predictable as possible, the future cannot be known with certainty." So far, Powell sounded like he would like maintain continuity from the Yellen era. But we may read deeper into his mind in the Q&A session today.

Dallas Fed Kaplan: Appropriate to hike in the near future

Dallas Fed President Robert Kaplan said that " it will likely be appropriate, in the near future, to take the next step in the process of removing monetary accommodation." And, "this should be done in the context of an overall strategy of removing accommodation in a gradual and patient manner." Kaplan warned that "if we wait too long to see actual evidence of inflation, we may get behind the curve and have to subsequently raise rates more rapidly." He added that "this type of rapid rate rise has the potential to increase the risk of recession."

NY Fed Dudley: Not concerned with inflation a little below target

New York Fed President William Dudley expressed that he's "not particularly concerned that inflation is a little bit below target." He pointed out that unemployment has fallen to 4.1% percent and reached "full employment. And with that unemployment rate, inflation would be prompted up. And there, "we have been gradually raising interest rates."

Merkel ready to compromise in grand coalition talk

In Germany, Chancellor Angela Merkel talked about the coalition with SPD in her CDU headquarters yesterday. She emphasized that "people expect their problems to be solved, and we believe that the best way to achieve that is by forming a stable government." And, "that's why we are ready to begin talks with the SPD. We of course know that such talks require compromise." SPD leader Martin Schulz continued to sound open as he said in a press briefing that "we are entering into talks, and we don't know where they'll lead," but "no option is off the table." Merkel will meet with SPD leader Martin Schulz, CSU leader Seehofer and President Frank-Walter Steinmeier on Thursday, on reformation of the grand coalition.

On the data front

Germany will release import price index and Gfk consumer sentiment in European session. Eurozone will release M3. Canada will release IPPI and RMPI later in the data. US will release wholesale inventories, trade balance, and house price indices. But Conference Board consumer confidence is the more important one to watch.

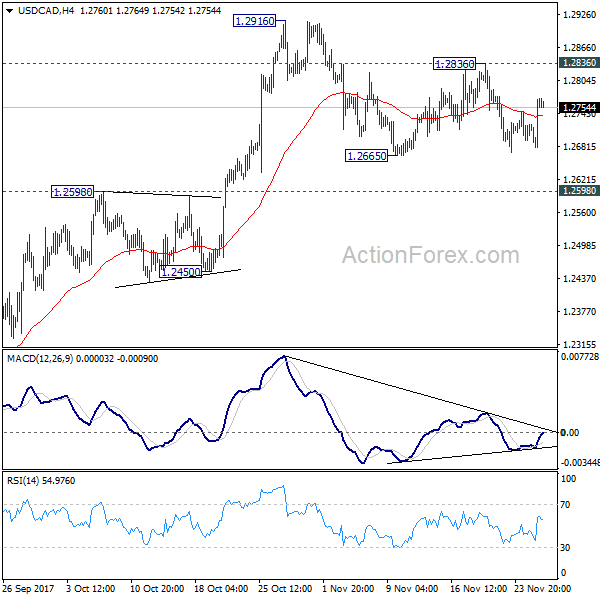

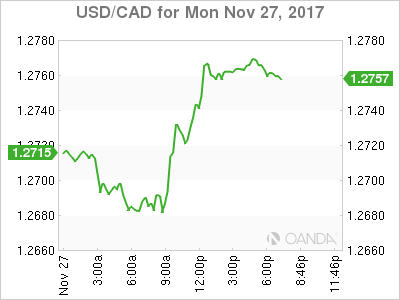

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2708; (P) 1.2739; (R1) 1.2799; More....

USD/CAD's correction from 1.2916 is still in progress and intraday bias stays neutral. Deeper decline could still be seen. . But we'd expect downside to be contained by 1.2598 resistance turned support and bring rebound. Above 1.2836 minor resistance will turn bias back to the upside for 1.2916 first. Further break of 1.2916 will resume whole rally from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2895). Near term outlook will be turned bearish in this case.

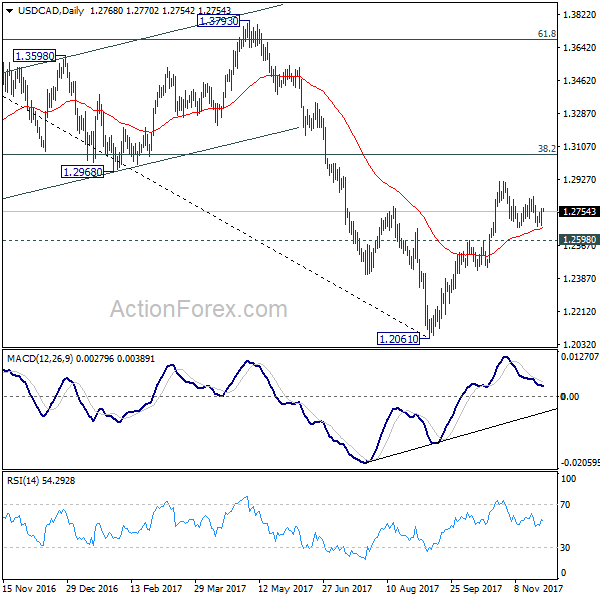

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | EUR | German Import Price Index M/M Oct | 0.40% | 0.90% | ||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Oct | 5.10% | 5.10% | ||

| 12:00 | EUR | German GfK Consumer Confidence Dec | 10.7 | 10.7 | ||

| 13:30 | USD | Advance Goods Trade Balance Oct | -65.0B | -64.1B | ||

| 13:30 | USD | Wholesale Inventories M/M Oct P | 0.40% | 0.30% | ||

| 13:30 | CAD | Industrial Product Price M/M Oct | -0.30% | |||

| 13:30 | CAD | Raw Materials Price Index M/M Oct | -0.10% | |||

| 14:00 | USD | House Price Index M/M Sep | 0.50% | 0.70% | ||

| 14:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Sep | 6.00% | 5.92% | ||

| 15:00 | USD | Consumer Confidence Index Nov | 124 | 125.9 |

Market Morning Briefing: Euro Is Testing Resistance Near 1.19

STOCKS

Dow (23580.78, +0.10%) looks positive to test 23750-23800 levels. Movement is narrow and almost stable so the rise may take a few sessions to materialize before again coming off towards 23500 or lower. Near term looks stable to bullish.

Dax (13000.20, -0.46%) is stuck in the 13200-12900 region as expected and the range is likely to hold in the near term. A re-test of 12900 is possible over the next couple of sessions before again rising back towards 13100.

Nikkei (22527.97, +0.14%) is also stuck in the narrow 22750-22250 region and a sharp fall towards 22190-22000 and lower would be needed to confirm an upcoming downtrend. While 22000 holds, there could be chances of moving up again in the longer run.

Shanghai (3312.71, -0.29%) is probably giving first signs of a sharp fall coming in the near term. While the index sustains below 3325, a fall towards 3280-3250 is on its way in the coming sessions.

Nifty (10399.55, +0.09%) could re-test 10500 over today and tomorrow but we are doubtful if a sharp fall would follow in the coming sessions. A 2-3 sessions corrective dip to 10200 is possible but the index could remain stable in the near term. a rise above 10500, if seen could open up higher levels keeping the index bullish for some more time.

COMMODITIES

Gold (1294.15) is trying to rise towards 1300 and there is enough room on the upside for the coming sessions towards 1320 and higher. Also note that the price could possibly see another down leg from 1300 before making a final rise towards 1315-1320 and higher.

Silver (17.02) is almost stable and could trade within 17.00-17.25 region for a while. Contraction in the near term is likely to be seen.

Brent (63.68) is trading above support near 63. While the price looks bullish towards 65-66 levels, WTI (57.76) is respecting the resistance near 59 and looks bearish for the near term. If the prices follow the mentioned view the Brent-WTI (5.91) spread could widen in the coming sessions.

Copper (3.1140) is testing support near 3.10 and while that holds, a rise back to levels near 3.20-3.25 is possible. Also note that 3.20/25 is a medium term resistance and may not allow a rise above 3.25 just now. A rejection from 3.25 back to 3.00 looks probable in the medium term.

FOREX

Dollar Index (92.908) saw a low of 92.49 yesterday, but has stayed above support near 92.70 and is currently trading around 92.90, indicating possibility of some sideways movement between 92.80 to 93.00 in the next couple of sessions, before it moves up towards the end of the week.

Euro (1.1900) is testing resistance near 1.19 on the weekly line charts. It has fallen slightly compared to yesterday’s levels around 1.192 but it is yet to be seen if this resistance will hold. With a weakening of German 10 yr Yields and bullishness in crude prices expected to boost dollar strength, the resistance should hold; however if it doesn’t, hen Euro could rise beyond 1.22 quickly.

Dollar-Yen (111.23) has moved down further with a strengthening of Japanese 10 yr yields (see Interest Rates below) and could be expected to test levels near 110 by next week. However, there are signs of dollar strength resurfacing, which could thereby lead to a quick reversal in trend from levels near 110.50.

Pound (1.3322) continues to trade just below resistance levels at 1.335 and looks like a slight corrective dip is in process of occurring, starting off another phase of range wise movement between 1.33 and 1.335.

Dollar Rupee (64.51) is likely to test 64.40 while below 64.60. Downside chances have increased just now as support near 64.60 has broken.

INTEREST RATES

Slight bounce in the 30-5Yr US yield Spread, from 0.69% yesterday to 0.72%, in line with expectation. A rise above 0.75% will reduce the market's fear of further curve-flattening and the conjoined fear of recession.

We see Supports near current levels on the 5Yr (2.06%), 10yr (2.33%) and 30yr (2.77%). US yields have been softening as the market's expectations of future inflation is muted, with 2018 inflation projected at 2.05% as compared to a projection of 2.10% for 2017. We could be wrong, but perhaps the market is not factoring in enough of a possible rise in Brent towards 67-68 in the coming weeks.

It will be interesting to see if the US Q3 GDP will come in near/ higher/ lower than the market expectation of 3.30% tomorrow.

The German 2Yr (-0.696%) has come down a bit from its Resistance near -0.69% mentioned yesterday. However, the Japanese 10Yr (0.039%) has moved up a bit more from 0.036% yesterday. Resultantly, the Germany-Japan 10yr Spread (0.31%) seems to be breaking the uptrend from -0.06% (Sep 2016). A break below 0.30% (if seen) will confirm.

The 10yr GOI yield (7.0563%) has moved up further. Market consensus seems to be veering towards higher rates now. It will be interesting to see if the SBI Treasurer's contrarion view is borne out or not. Some consolidation between 7.10% and 6.90% is certainly possible.

USD/CAD Bouncing Off Key Zone

It's a lovely Tuesday morning in Sydney today and I hope you're back fully immersed in the markets for the week with me. There are some absolutely fantastic opportunities popping up all over my MT4 watch list and we want to be around to take advantage of them! I mean yesterday's AUD/USD short was about as clean of a setup that you're going to see, and today's USD/CAD bounce has similar potential.

Sticking with USD/CAD, let's cast our mind back to when I was talking about how to handle momentum moves and to really pay attention to how price reacts around major support/resistance levels to manage your risk.

Click the link to the blog that outlines my thoughts on the topic in the paragraph above, then take a look at today's daily chart below:

USD/CAD Daily:

As you can see, this zone has been key for both bulls and bears. Today's call just happens to be using it to manage your risk as support.

So much for that Bank of Canada inspired drop, right?

A Spoonful Of Morning Jitters

A Spoonful of Morning Jitters

A spoonful of morning jitters sent New York investors scurrying to the local bond desks as the skittish demand for US treasuries guided the USD lower initially only to stage a tentative recovery in some FX pockets after US home sales surged to a ten year high.

Indeed, wobbly China equity markets are not helping global sentiment, but at the core of the matter, investors continue hanging by a thread over US tax reform as the market remains embroiled in the US Senates competing priorities. This morning, media sources report that without changes to the Senate tax bill, Republican Senator Ron Johnson is a no in Tuesday's Senate Budget Committee. And of course, the great unknown remains Senator Bob Corker who remains on the fence

Also, it's worth noting that we are encroaching on year-end type liquidity. The markets have been driven to the back of position-momentum swings lately, and with USD the most prominent short, Traders get nervous about the crowded trade mentality in less than ideal liquidity condition and will head for the exits quickly. Needless to say with the numerous risk- off triggers hitting the market regularly, it gets a bit spooky trading in sub-par conditions and certainly dampens speculator appetite.

Asian equity markets continue to trigger ' risk off.' moves and this will remain the immediate focus as the overall global risk environment remains queasy.

The Japanese Yen

One of those ' FX pockets ' where the dollar continues to struggle is USDJPY. The pair remains exceptionally susceptible to both Risk and Yield with both key drivers hammering the pair mercilessly yesterday. Beefy flow in US bonds started the slide as investors were growing ever so nervous about the recent China market machinations. But a vague rumour that North Korea may test another ICBM also weighed on sentiment.

The Euro

The EURUSD continues to hold around the 1.1900 levels. But the advancing strength in the European economic data stream will continue to reverse out any expectations for ECB dovishness. This positivity alone will keep the EURO firmly bid on dips as traders await a clean, decisive break in Germany political deadlock before taking the Euro higher.

The Australian Dollar

The Aussie dollar trade is becoming more of a chess match than anything else as two competing ideas are driving current sentiment.

Aussie remains well entrenched above significant support levels ( .7500) The recent run of reasonably constructive price action as the Aussie yield premium all but evaporated has some elements in the market dipping into the tactical pond buying Aud feeding of the regional EM soaring GDP prints. While others prefer flat-out selling the Aussies diminishing carry advantage, the result is a is a currency stuck in neutral awaiting fresh news to take another leg in either direction.

Overall we remain in no man's land until either .75 gives way to .7675 is taken out so choose your sides carefully.

But given that risk off sentiment looks likely to extend further this week tactically short AUDJPY would be the go-to trade from that perspective

Energy Prices

WTI oil prices traded with a negative bias due to the firm US dollar, and the likely early onset of profit-taking ahead of Thursday's Opec meeting. There were rumours that Russia may not be eager to extend production cuts. This rumour play's not the view that anything short of a complete buy-in by Russia to roll over the production cut sends oil prices sliding given the markets bullish positioning.

Asia FX

USD Asia liquidity has not recovered yet from Thanksgiving which has traders not so keen to speculate. And of course, the wobbly China equity markets has created some regional risk wobbles.

None the less, I am confident China regulators will not let this get too out of hand and provide liquidity to settle any of the nervous nellie jitters their Financial Reforms movement is causing. Overall I view this short-term pain as the long-term extremely positive gain for the region. Unfortunately, we are trading in year-end markets when a long-term view is considered holding a position longer than 3 minutes which is not helping risk sentiment.

The Chinese Yuan

The Yuan has remained exceptionally stable given the wobbly mainland equity markets. The RMB complex continues to provide an excellent proxy of USD sentiment as it shadows broader USD dollar trends.

Entering month end, we should expect the usual USD corporate demand to provide a near-term base for USDCNH.

Sentiment remains guardedly optimistic for the Yuan, but traders need to see an extended rally on mainland equities before diving into the waters again.

The Malaysian Ringgit

The USDMYR market has become less one-sided with shorts pared ahead of significant 2-way USD risk this week. But with rebound in EUR and dovish November FOMC minutes still fresh in the market mind this should continue to favour regional EM demand. Also, the cleaner positioning suggests the MYR could extend its decisive run as the currency remains in favour on both macro and monetary policy fronts.

On a slight negative WTI oil prices opened with a negative bias, dropping from $58.52 to $57.57, due to the firm US dollar, and the likely early onset of profit-taking ahead of Thursday's Opec meeting. But given that the MYR has been less sensitive to falling oil prices of late, this should not be a substantial adverse bias as OIL prices remain above the Malaysian Government budgeted oil price targets

Five Potential Inflation Surprises for 2018

Inflation came strongly out of the gate in 2017. After nearly half a decade below the Fed's target, the PCE deflator reached 2 percent in January amid a rebound in energy prices and pickup in core inflation. It looked as if both parts of the FOMC's dual mandate were finally giving a clear greenlight to raise interest rates.

That all came crashing down in March, however. Core inflation fell 0.2 percent, which was bigger than the cumulative decline registered over the entire Great Recession. Driving the drop was a 7.0 percent decline in wireless phone services as falling plan costs coincided with new ways in which the BLS adjusted for changes in plan quality. Although only a sliver of the CPI with a weight of 1.5 percent, the drop in March was enough to subtract 0.2 percentage points off the year-over-year rate of headline inflation and kick off a run of disinflation that lasted through the summer. Could we be in for another such surprise in 2018?

Our baseline forecast is for inflation to slowly strengthen over the course of the coming year. Further tightening in the labor market and the unwinding of what we believe to be largely one-off effects should push inflation higher. A 5 percent decline in the dollar since January and stronger global inflation should also lend some support to core goods prices as import prices rise.

Offsetting the upward thrust of these dynamics, however, is likely to be further declines in the prices of autos as replacement demand from recent natural disasters will not be enough to right-size dealer inventories and absorb the swath of vehicles coming off lease. At the same time, competitive pressures generated by new technology and the slow sales environment, as well as low inflation expectations, will continue to weigh on firms' ability and willingness to raise prices.

That said, there is no shortage of sources that could knock inflation off our projected course for 2018. A stronger labor market is no guarantee of wage growth as we have seen in recent years, and even higher labor costs do not necessarily mean higher prices if margins are reduced. On the flip side, since the reasons behind inflation's more modest response to labor conditions are not well understood, there is the risk that the link reasserts itself more quickly than anticipated.1 Throw in the potential for unusual weather, a collapse in trade agreements, other geopolitical crises and the typical noise in inflation data that can emerge from small sampling, and the inflation story could change dramatically in 2018. In this report, we focus on five specific inflation categories that have the potential to drive an inflation surprise next year.

1. Inflator: Natural Gas - From One Weather Extreme to Another

Heading into the draw down season, natural gas in storage is currently at the lowest level for this time of year since 2014 (Figure 1). This alone would not be enough to generate higher heating costs in the coming months, but when combined with unusually cold temperatures this winter, prices could jump. The National Oceanic and Atmospheric Administration is predicting a 65-75 percent chance of La Niña weather patterns this year, which would bring colder-than-average temperatures to the Northwest, Midwest and heavily populated Northeast.

There has been no shortage of extreme weather lately. With the past two winters cracking the top 10 warmest on record, if this winter went from one extreme to the other, natural gas prices could soar like in early 2014. That winter was only the 29th coldest on record, but saw consumer prices for utility/piped gas services jump 16 percent between December 2013 and March 20142 (Figure 2). When combined with prices for electricity (for which natural gas is now the number one source), utility services had lifted the year-over-year rate of headline CPI by 0.3 percentage point by March.

2. Inflator: Food Away From Home - Not to Be Minimized

The cost of dining out has grown more slowly over the past two years. The 12-month change in the CPI for food away from home, which carries a 5.8 percent weight in the index, has fallen by half a percentage point since mid-2016 (Figure 3). That slowdown is ripe for a reversal, however. Prices for food away from home are especially sensitive to changes in minimum wages given the high share of low-wage workers in the hospitality industry. In 2018, 20 states are scheduled to raise the minimum wage (Figure 4). That is slightly fewer than in 2017 (22), but recent research from the Boston Fed finds that inflation is raised by minimum wage hikes not only in the first year in which they go into effect, but also the following year.

While a growing number of states and cities have been raising the minimum wage in recent years, restaurants and other food prep establishments have gotten a respite from declining food costs. That breathing room could change in the coming year as food costs are beginning to rise again. The Commodity Research Bureau food index is up 6.8 percent over the past year, the largest increase since 2014 when more states began to raise the minimum wage.

3. Inflator: Medical Care - "Healthy" Inflation Again

Medical care price growth has moderated somewhat in recent years amid efforts by insurers and the government to rein in costs (Figure 5). However, upward pressure from drug prices and labor costs could boost the CPI for medical goods and services in 2018. Prescription and over-the-counter drugs make up about 1.8 percent of the CPI consumption basket while medical services contribute 6.6 percent, giving them considerable weight in the overall CPI. As recently as September 2016, an upswing in medical goods and services contributed more than 43 basis points to year-over-year CPI inflation.

Fewer generic drugs are set to enter the market in 2018, which will likely push up prescription drug inflation. According to the PWC Health Research Institute, the sales value of drugs coming off patent protection declined by 32 percent in 2016 and 41 percent in 2017 from a year earlier.4 Cost savings from generics usually show up 1-2 years after patent expiration, so the impact of fewer patent expirations in the past two years should be felt in 2018. Since generic alternatives cost 80-85 percent less than branded drugs, their presence (or absence in this case) in the market can make a substantial difference to medical goods costs.

Higher labor costs as the labor market continues to tighten are also likely to put upward pressure on medical care prices. More than half of the industry's input costs is employee compensation, and wage costs have been picking up over the past year. With the rate of job openings also trending higher, we expect to see higher labor costs to put more upward pressure on the services component of medical inflation.

4. Deflator: Rent of Primary Residence - The Affordability Wall

Slower rent growth may be in the offing next year as the torrent of multifamily housing supply since the recession and eroding affordability collide. Shelter costs represent some of the largest slices of the CPI basket (altogether 30 percent), with rent of primary residences making up about 8 percent. Industry measures of apartment rent growth, which tend to lead the rent-of-primary-residence component of CPI, have slowed over the past year (Figure 7).

We see a risk that developers overestimated the future strength of demand for multifamily properties and have overbuilt. Multifamily housing starts reached a level in February not seen since 1989, and higher vacancy rates point to the surge in supply outpacing demand. Homeownership rates have stabilized this year, helped by easier credit and low interest rates. At the same time, rent continues to grow faster than household income. The CPI for rent of primary residence rose 25 percent since the start of the expansion in 2009, but median household incomes have expanded 18 percent. Unlike the purchase market where financing terms can keep monthly payments in check, landlords may be unable to continue raising rents at the same pace until incomes catch up.

5. Deflator: Lodging Away from Home - Hotel Headaches

Growth rates in the CPI for lodging away from home have already moderated this year. However, there is scope for a more dramatic fall if a mismatch between hotel supply and demand pulls down occupancy further, and hotel managers respond with substantially lower rates. Hotel occupancy rates have declined slightly in 2017 after peaking in Q4-2016 (Figure 9). Vacancies put pressure on room rates as hotels compete for customers with discounting and special offers; real room rates fell year-over-year in Q3 for the first time since Q2-2010 on a seasonally adjusted basis. While the weight of lodging away from home in the CPI is small - just 0.9 percent - changes in this component have moved the headline by as much as 8 basis points in recent years, and when combined with other factors can make a palpable difference to inflation.

An uptick in the number of hotel rooms in planning or construction phases this year suggests that hotel occupancy may continue to be a challenge in 2018, as new supply outpaces demand. Rooms in the pipeline as a share of existing supply were up 1.4 percentage points in October compared to January 2016 (Figure 10). Given an average construction lead time of eight months for private nonresidential projects, these hotel rooms will likely feed into supply early next year. Services such as Airbnb are also providing lodging alternatives to traditional hotels and increasing competition for attracting customers.

Meanwhile, macroeconomic factors are not supportive of sizable increases in hotel demand in the near future. Corporate profit growth is expected to be in only the low-single digits next year, limiting growth in business travel. Meanwhile, modest growth in disposable income is also holding back growth in leisure travel. U.S. air travel shrank this year, with passenger enplanements down 2.9 percent year-to-date compared to 2016. Given our forecast for modest corporate profit and disposable income growth into next year, we expect continued softness in travel activity and associated hotel demand.

Conclusion

Inflation is notorious for being knocked around by a few categories. While inflation watchers are accustomed to the volatility caused by food and gasoline prices, this year was a reminder that other categories that are typically more stable and/or smaller can have meaningful effects on aggregate price movements. We are watching a number of categories that could similarly upset our baseline forecast of moderately stronger inflation next year. These items, however, offer the potential of both upside and downside pressure. As a result, we see the risks these categories present to our forecast as roughly balanced.

Powell Expects Further Hikes

The Fed's Powell hinted at a continuation of Yellen-era gradual rate hikes in the text of his confirmation statement. Trump lifted the USD via a tweet, expressing his optimism on a tax deal in Congress. The yen and kiwi were the top performers while the Canadian dollar lagged. More Fedspeak is due in the hours ahead. A new USD trade was issued for Premium subscribers. DOW short was stopped out, leaving one index trade in progress and in the green.

Powell faces questions on Wednesday from Senators on his economic and regulator leanings as part of his confirmation process. His opening statement was released late Tuesday and said he expects interest rates to rise 'somewhat further.' He also hinted at lightening the regulatory burden facing banks while maintaining the core reforms. For the most part, the published comments were the usual platitudes about independence and the dual mandate.

The big question is how the Fed will proceed in the months ahead if inflation moves up only slowly. A hike in December is seen as a slam dunk but March and beyond will depend on progress in the economy and inflation. What remains a mystery is the where the Fed's minimal inflation threshold lies and if there is eventually a point where they will hit the pause button until prices near 2% growth.

Dallas Fed President Kaplan hinted at growing confidence and hawkishness. He said he was beginning to worry about an overheating jobs market and signaled that gradual hikes are likely necessary. He isn't a voter next year but is generally a good barometer for the core of the FOMC.

One issue the Fed may have to confront in the years ahead is housing. New home sales in October were at a 685K annual pace compared to 625K expected. It was the second month in a row of strong numbers.

In terms of market moves, the US dollar bounced to start the week but only recovered a small portion of last week's drop. The yen remained red hot and was boosted in part on a report that North Korea is preparing another missile launch.

The Asia-Pacific calendar is light in the day ahead but Chinese stock markets are increasingly in focus. The Shanghai Composite fell 0.9% to start the week and is at the lowest since August on signs the government will tighten liquidity.

CFTC Commitments of Traders

Speculative net futures trader positions as of the close on Tuesday. Net short denoted by - long by +.

- EUR +95K vs +84K prior

- GBP -1vs -4K prior

- JPY -123K vs -147K prior

- CHF -30K vs -28K prior

- CAD +45K vs +47K prior

- AUD +40K vs +44K prior

- NZD -14K vs -12K prior

The extreme yen short was trimmed but still remains in a highly vulnerable spot given the steady declines in USD/JPY and yen crosses. A washout could come any time.

Canadian Dollar Lower as Oil Price Falters

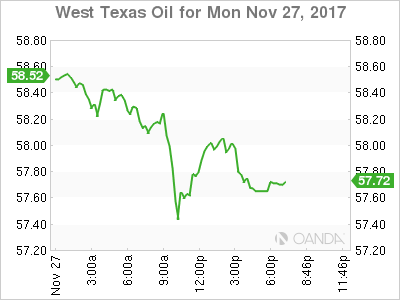

The Canadian dollar depreciated on Monday after oil prices fell more than 1 percent at the start of the week. Higher supply in North America and concerns about Russia's commitment to the OPEC production cut agreement have lowered energy prices after touching two year highs. The fall in energy prices affected the loonie as the correlation between the two is resurfacing.

The Bank of Canada will release its Financial System Review on Tuesday, November 28 at 10:30 am EST. US Federal Reserve members will also feature heavily this week, with Chair nominee Jerome Powell due to testify before the US Senate at 10:00 am EST on Tuesday.

BMO released a report on the impact of NAFTA ending with the impact to Canada about 1 percent of GDP. Inflation would rise given the potential weak loonie and pricier imports which could put pressure on the BoC to raise rates. After the fifth round of talks ended in Mexico City there was a sense that little progress has been made. The end of the year is fast approaching and with the new year will come Presidential elections in Mexico and the US primaries adding more uncertainty to an already dicey negotiation. The next round of talks will happen in Washington on December 11.

The USD/CAD gained 0.52 percent on Monday. The currency pair is trading at 1.2769 as the US dollar managed to get a leg up after a short holiday week had the greenback on the backfoot. The negative impact on the US tax reforms issues remains when talking about the JPY but against all the other majors the USD appreciated. Friday, December 1 will be a busy week for CAD traders. Statistics Canada will release the monthly GDP figures as well as the employment report both at 8:30 am EST. GDP is expected to have shrunk by 0.1 percent and there is some anxiety on the job front as the first ADP job report for Canada showed a loss of 5,700 in October.

Oil prices fell at the beginning of the week. The price of West Texas Intermediate is trading at $57.65 after the Keystone pipeline will restart operations on Tuesday and doubts about Russia's willingness to extend the OPEC production cut agreement, put pressure on crude prices.

Oil ministers will meet in Vienna on Thursday a year after a deal was reached to reduced crude production to stabilize prices by the Organization of the Petroleum Exporting Countries (OPEC). Russia and other major producers joined the agreement in December, and have already extended the deal until March of 2018, but the likely outcome from the meeting in Vienna is a second extension. The main topic of debate is for how long as different timelines have been discussed. Russia has taken the leadership position in a time when Saudi Arabia is opening too many fronts in the diplomatic arena.

The mercurial nature of OPEC members has already resulted in failed summits in the past, but it appears that Russia is seen as a conciliatory third party that could push through an extension. The main issue now is by how much will the new head of the energy class want to extend the production cut agreement. Russia was slow to comply with the cuts, and might not be as willing to go for a full 9 month extension this time around.

Market events to watch this week:

Tuesday, November 28

- 2:00am GBP Bank Stress Test Results

- 10:00am USD CB Consumer Confidence

- 11:15am CAD BOC Gov Poloz Speaks

- 3:00pm NZD RBNZ Financial Stability Report

Wednesday, November 29

- All Day All OPEC Meetings

- 8:30am USD Prelim GDP q/q

- 10:30am USD Crude Oil Inventories

- 7:00pm NZD ANZ Business Confidence

- 7:30pm AUD Private Capital Expenditure q/q

Thursday, November 30

- 8:30am USD Unemployment Claims

Friday, December 1

- 4:30am GBP Manufacturing PMI

- 8:30am CAD Employment Change

- 8:30am CAD GDP m/m

- 10:00am USD ISM Manufacturing PMI

*All times EDT

British Pound Looking for Footing

The British pound moved higher on Monday, but has given up these gains. In North American trade, GBP/USD is trading at 1.3332, up 0.02% on the day. On the release front, there are no UK events on the schedule. In the US, New Home Sales surged to 687 thousand, well above the estimate of 627 thousand. On Tuesday, the focus will be on the Bank of England which publishes the results of its bank stress tests, as well as the semi-annual Financial Stability report. The US releases CB Consumer Confidence, with an estimate of 123.9 points. As well, Federal Reserve Chair Designate Jerome Powell will testify before a Congressional committee.

There may be signs that the British economy is slowing down, but CBI retail sales and manufacturing reports looked sharp last week. Retail sales jumped in November, as CBI Realized Sales rebounded with a strong reading of 26 points. The release was all the more impressive, as the indicator came in at -36 points in October. CBI Industrial Order Expectations, an important barometer of activity in the manufacturing sector, also impressed. The indicator surged to 17 points in October, rebounding from the September release of -2 points. Manufacturing indicators continue to point upwards, boosted by strong global demand and a weak British pound. Export order books are at their highest levels since 1995, and the markets are predicting that the export and manufacturing sectors will continue to shine in the fourth quarter.

All eyes will be on Jerome Powell, who testifies before the Senate Banking Committee on Tuesday for his confirmation hearing. Will Powell be a clone of outgoing chair Janet Yellen? Powell inherits an economy that is in excellent shape, but persistently low inflation remains a nagging problem. Fed policymakers have differing views on what to do about inflation, with some members proposing that the Fed drop its 2 percent target, in favor of a "gradually rising path" for prices. The Fed remains confounded by low inflation and wage growth, despite a labor market that is at full capacity. Still, the Fed will likely pull the rate trigger next month, and could raise rates up to 3 more times in 2018 if the economy continues to expand at its current pace.

Gold Pushes Higher as Dollar Sags

Gold has jumped on the bandwagon, as the US dollar is broadly lower in the Monday session. In North American trading, the spot price for an ounce of gold is $1295.12, up 0.52% on the day. Gold pushed above the $1299 line earlier in the day, its highest level since October 16. On the release front, New Home Sales surged to 687 thousand, well above the estimate of 627 thousand. On Tuesday, the US releases CB Consumer Confidence, with an estimate of 123.9 points. As well, Federal Reserve Chair Designate Jerome Powell will testify before a Congressional committee.

Federal Reserve policymakers remain upbeat about the U.S economy, according to the minutes of the most recent policy meeting. The minutes indicated that policymakers expected the U.S economy to continue showing strong growth, and predicted that interest rates will be raised in the "near term". The members discussed the vexing question of why inflation has been persistently low (no quick-fix solution was provided), with most agreeing that a tight labor market should lead to higher inflation levels. Although policymakers did not provide further hints about the timetable of a rate hike, the markets remain convinced that additional rates are imminent. The odds of a rate hike in December are 93%, and the odds of a January raise are at 91%.

All eyes will be on Jerome Powell, who testifies before the Senate Banking Committee on Tuesday for his confirmation hearing. Will Powell be a clone of outgoing chair Janet Yellen? Powell inherits an economy that is in excellent shape, but persistently low inflation remains a nagging problem. Fed policymakers have differing views on what to do about inflation, with some members proposing that the Fed drop its 2 percent target, in favor of a "gradually rising path" for prices. The Fed remains confounded by low inflation and wage growth, despite a labor market that is at full capacity. Still, the Fed will likely pull the rate trigger next month, and could raise rates up to 3 more times in 2018 if the economy continues to expand at its current pace.

Dollar Broadly Weaker; Sterling Rises Despite Brexit Uncertainty; Oil Retreats

With US new home sales being the day's major release during today's session, upcoming developments, such as US tax reform deliberations and Brexit negotiations, were in forex market participants' minds during today's European session. Meanwhile, the yen was advancing on some softness in Asian and European equity markets.

At 1523 GMT, the dollar index, which measures the greenback against the currencies of six major US trading partners, was 0.1% down at 92.74. The gauge finished lower in the three preceding weeks, while today it touched a three-month low of 92.50. The US currency was deeper in losses earlier in the day but managed to reverse some of its losses later in the session.

Jerome Powell, President Trump's nominee to lead the Fed once Janet Yellen's term expires in February, will be having his confirmation hearing in Washington on Tuesday (1500 GMT) with senators having the opportunity to question him on key issues. Any comments on monetary policy, deregulation and the economy overall have the capacity to act as market movers.

The US Senate will be resuming deliberations on tax reform this week following last week's Thanksgiving break. Donald Trump is scheduled to meet Senate Republicans on Tuesday to discuss continuing efforts to pass the tax plan legislation. Developments on this front are also likely to act as catalysts for dollar positioning.

In today's main release, October new home sales rose by 6.2% m/m to reach 685k units, contrasting expectations for a decline by 6.0% after September's surge by 14.2% (downwardly revised from 18.9%). Sales in October constitute a decade high as well as the third straight monthly increase and reflect strong demand across the US. The dollar managed to erase some of its losses relative to major rivals following the release at 1500 GMT.

Dollar/yen was last 0.3% lower, trading above the 111 mark, a level violated on the downside earlier in the day as the pair hit a two-month low of 110.87. Euro/dollar was flat after advancing in the three preceding days. At its highest, it recorded a two-month peak of 1.1960. Upbeat data in recent days and political uncertainty withering out in Germany on the back of rising prospects for a coalition between Social Democrats and Merkel's Christian Democrats, have been supportive of a stronger euro.

Eurozone's common currency was losing ground relative to the yen during today's trading though. Euro/yen was 0.4% down at 132.63. Still, the pair held most of the gains from Friday's advance, a day on which it rose by 1.1%. The yen's capacity as a funding currency appears to have supported it today as there was a pullback of some sorts in non-US equity markets. Pound/yen was also lower (by 0.2%) at 148.42.

Sterling was last stronger versus both the dollar and the euro despite the Irish border issue – a key consideration in Brexit negotiations – getting more complicated ahead of political uncertainty in Ireland, with elections potentially being put on the table for December; this will become clearer by tomorrow. Pound/dollar was 0.1% up after tracking a two-month high of 1.3382 earlier in the day. Euro/pound was 0.1% lower at 0.8935 after previously rising to an 11-day high of 0.8966.

UK PM Theresa May was given a deadline up to December 4 by EU counterparts to improve its position on key pending Brexit issues in order for leaders from the bloc to approve the commencement of talks on trade relations during the summit scheduled for December 14-15.

Dollar/loonie was 0.1% higher at 1.2726, reversing earlier losses. Meanwhile, the aussie was flat relative to the greenback at $0.7611 and the kiwi was up by 0.5% versus its US counterpart at $0.6913. At their highest, they both touched two-week peaks versus the greenback.

In notable movements within the emerging markets spectrum, the South Africa rand was making up on some of its losses from previous days relative to the dollar after credit rating agency Moody's decided to place South Africa on review for a downgrade rather than proceed with an outright credit cut as was the case with Standard & Poor's which now rates the nation's credit ability within the "junk" category. There is some relief in the markets, as should Moody's had gone ahead with a downgrade, then South African bonds would had been removed from numerous key global bond indexes. Dollar/rand was last 0.9% down at 13.7435.

In commodities, gold was 0.5% up at $1,294.40 per ounce. Its highest on the day, which also constituted a more than one-month peak, was $1,299.13. The precious metal is on a positive footing on the back of dollar weakness, but it also benefitted on cautiousness in stock markets during today's trading. WTI and Brent crude traded lower by 2.15% and 1.1%, at $57.68 and $63.26 a barrel respectively. Despite the sell-off, both benchmarks remained relatively close to recently-hit more than two-year high levels.