Sample Category Title

Technical Outlook: COPPER – Daily Cloud Top To Ideally Contain Correction

Copper price moved lower on Monday, pulling back from nearly one-month high at $3.1750, posted on uninterrupted six-day rally.

Dip was so far contained by strong support at $3.1198 (Fibo 38.2% of $3.0305/$3.1750 upleg), which guards another significant support at $3.1087, provided by top of ascending daily cloud.

Deeper correction cannot be ruled out as daily RSI is heading lower while slow stochastic has turned south and is about to emerge from overbought territory.

Overall structure is bullish and positive sentiment maintained by strong demand for the metal from China, its biggest consumer, despite signs of resilience in country’s industrial sector.

Extended corrective action should be ideally contained by daily cloud top ($3.1087) with deeper dips not to exceed daily Tenkan-sen ($3.1027) to keep bulls intact.

Res: 3.1395, 3.1477, 3.1541, 3.1750

Sup: 3.1198, 3.1087, 3.1027, 3.0857

Technical Outlook: US Crude Oil Price Eases From 2 ½ Year High, O/B Studies Warn Of Correction

WTI is holding in red at the beginning of the week, after hitting fresh high at $59.02 (the highest since late June 2015) last Friday.

Oil price maintained strong bullish sentiment in past couple of weeks on strong signals of oil market rebalancing and hopes that OPEC-led output cut agreement will extend.

Traders booked some profits from last week’s strong rally, as overbought daily studies suggest corrective easing before oil price resumes towards psychological $60 barrier which also marks initial target.

Meeting of oil ministers of OPEC and other big oil producers on 30 Nov in Vienna is in focus this week, as markets expect major oil producers to extend their current production cut program beyond its expiration in march 2018.

Meanwhile, oil price may extend corrective easing towards initial support at $57.90 (former top of 08 Nov), with extended dips to be contained by rising 10SMA (currently at $56.97).

Res: 59.02,59.82,60.00,60.27

Sup: 58.34,57.90,56.79,56.53

Market Update – European Session: Optimism That Germany Can Resolved Its Political Impasse Without Elections

Notes/Observations

Political clouds dispersing across Europe; optimism abound as Germany's Social Democrat party agreed to discuss forming a "grand coalition" with Chancellor Merkel and her Christian Democratic party.

Tightening financial conditions in China weighs upon Far east markets; Shanghai Composite having its worst 3-day decline since Jun 2016

OPEC and Non-Opec members said to be leaning towards an extension of the current production cut agreement at this Thursday’s meeting

Asia:

Japan Govt said to compile FY17/18 extra budget of €2.7-2.9T; with construction bond issuance of ~¥1T

BOJ’s Suzuki reiterates view that must maintain powerful monetary easing; yield Control changes is possible when CPI is near 2% level

China Oct Industrial Profits Y/Y: 25.1% v 27.7% prior

Europe:

German Chancellor Merkel: Europe needed a strong Germany, so it needed a new govt in place as soon as possible. Caretaker govt will be able to carry out the day to day business of the govt

CDU’s Guenther: Firm intention of having an effective Govt. Firmly believed this was not a minority Govt and that it was an alliance with a parliamentary majority, a grand coalition

CSU’s Seehofer: Alliance of Conservatives and SPD is the best choice for Germany – better than coalition of FDP and Greens, new election or minority Govt

EU's Tusk: sufficient progress in Brexit talks at Dec council is possible, but a huge challenge remained. Set Dec 4th deadline for UK effort before the summit; PM May agreed on the timeline

UK PM has agreed to pay more than £40B when UK leaves the EU but the final bill will be kept secret from the public even after final deal is done in 2019

Ireland PM Varadkar: we need to resolve political matters by Tues, Nov 28th; if we don't, we will be into an election

Americas:

(US) According to ShopperTrak, shopper visits to brick-and-mortar retail stores on Thanksgiving Day and Black Friday -1.6% y/y (combined)

(MX) Mexico Fin Min Meade said to step down soon

Economic Data:

(FI) Finland Nov Consumer Confidence: 23.0 v 23.1 prior; Business Confidence: 14 v 12 prior

(HK) Hong Kong Oct Trade Balance (HKD): -44.0B v -41.9Be; Exports Y/Y: 6.7% v 10.1%e; Imports Y/Y: 7.9% v 9.5%e

(SE) Sweden Oct Household Lending Y/Y: 7.1% v 7.0%e

(IT) Italy Nov Consumer Confidence: 114,3 v 116.5e; Manufacturing Confidence: 110.8 v 111.8e, Economic Sentiment: 108.8 v 109.1 prior

Fixed Income Issuance:

(NO) Norway sold NOK3.0B vs. NOK3.0B indicated in 6-month Bills; Avg Yield: 0.32% v 0.37% prior; Bid-to-cover: 2.55x v 3.45x prior

(IT) Italy Debt Agency (Tesoro) sold €2.0B vs. €1.5-2.0B indicated range in Oct 2019 CTZ; Avg Yield: -0.337% v -0.167% prior; Bid-to-cover: 2.19x v 2.02x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.2% at 387.3, FTSE +0.3% at 7428, DAX +0.1% at 13075, CAC-40 +0.2% at 5402, IBEX-35 +0.7% at 10121, FTSE MIB +0.2% at 22464, SMI flat at 9326, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes:

European Indices trade higher across the board reversing early weakness with the Spanish IBEX outperforming as the index leads the gainers on dip buying. Indices traded lower initial following the weaker lead from Asia overnight, with a downgrade of Tech giant Samsung Electronics leading the tech sector lower.

In Europe shares of Infineon and Dialog Semi trade lower in sympathy. Elsewhere Euler Hermes trades sharply higher after a takeover offer from Allianz, while Julius Baer drags on the SMI after the immediate departure of their CEO.

On the Earnings front, Stablius trades lower after prelim FY17 results and 2025 tragets which Arzyta trades over 4% higher after Q1 update.

Equities

Consumer discretionary [Patisserie [CAK.UK] +6.2% (Earnings), Euler Hermes [ELE.FR] +21% (Allianz offer €122/shr), Aryzta[ARYN.CH] +4% (Earnings)]

Industrials: [ Stabilus [STM.DE] -1.8% (prelim earnings)]

Financials: [Icade [ICAD.FR] +2.4% (Capital markets day)]

Technology: [Infineon [IFX.DE] -1.4%, Dialog Semi [DLG.DE] -0.8% (down in sympathy with tech sector sell off in Asia)]

Speakers

ECB said to maintin its NPL proposal despite opposition from Italian officials

Poland Central Bank's Lon: Interest rates might be stable in the long term

Turkey PM Yildirim: 2017 GDP growth seen between 6.0-7.0% area

South Africa Presidency said to be looking at revenue enhancing plans. To find ways to increase revenues by ZAR15B and cut spending by ZAR25B

Russia Energy Mon Novak: Almost all OPEC/Non-OPEC members in favor of extending current round of production cuts

China PBoC renewed a CNY400B currency swaps agreement for another 3 years with Hong Kong Monetary Authority (HKMA)

Currencies

EUR/USD at 2-month highs aided by recent German business confidence and reduced anxiety about political instability in Europe's biggest economy. Political clouds seemed to be dispersing across Europe as optimism was abound as Germany's Social Democrat party agreed to discuss forming a "grand coalition" with Chancellor Merkel and her Christian Democratic party.

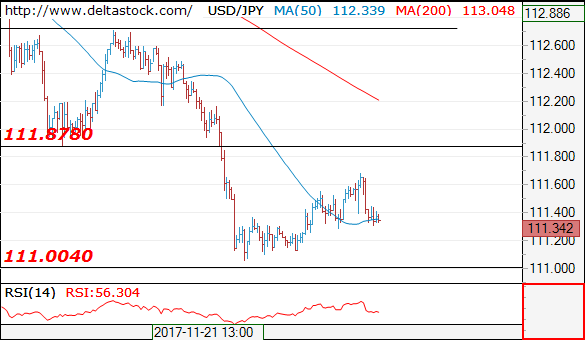

USD/JPY was probing the lower end of the 11 handle on some safe-haven flows. Dealers were taking notice of tightening financial conditions in China which weighed upon Far East equity markets as the Shanghai Composite endured its worst 3-day decline since Jun 2016

Fixed Income

Bund futures trade 162.90 up3 ticks, following strong German business confidence and reduced anxiety about political instability in Europe's biggest economy. Continued upside sees 163.40 then 163.63. A reversal targets 162.50 then 162.38.

Gilt futures trade at 125.24 down 10 ticks as markets await Brexit news. Continued upside eyeing 125.675 then 126.47. Downside targets include 124.90 then 124.24.

Monday's liquidity report showed Friday's excess liquidity rose €10B to €1.850T. Use of the marginal lending facility rose to €420M from €343M prior.

Looking Ahead

(CH) Swiss Parliament holds Winter Session in Bern

(DE) German President confirms that will meet with CDU, CSU and SPD representatives ( Chancellor Merkel, CDU's Seehofer and SPD's Schultz)

05:25 (BR) Brazil Central Bank Weekly Economists Survey

06:00 (RO) Romania to sell 2.3% 2020 Bonds

06:00 (IL) Israel to sell 2021, 2022, 2026 and 2027 bonds

06:45 (US) Daily Libor Fixing

07:00 (BR) Brazil Oct Total Federal Debt (BRL): No est v 3.431T prior

08:05 (UK) Baltic Dry Bulk Index

08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

08:55 (FR) France Debt Agency (AFT) to sell combined €4.8-6.0B in 3-month, 6-month and 12-month BTF Bills

09:00 (IL) Israel Central Bank (BOI) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.10%

09:00 (MX) Mexico Oct Trade Balance: No est v -$1.9B

09:30 (EU) ECB announces Covered-Bond Purchases

09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

10:00 (US) Oct New Home Sales: 624Ke v 667K prior

10:30 (US) Nov Dallas Fed Manufacturing Activity: 24.0e v 27.6 prior

13:00 (US) Treasuries to sell 2-year and 5-year notes

13:30 (UK) BOE’s Ramsden in London

16:00 (US) Weekly Crop Progress Report

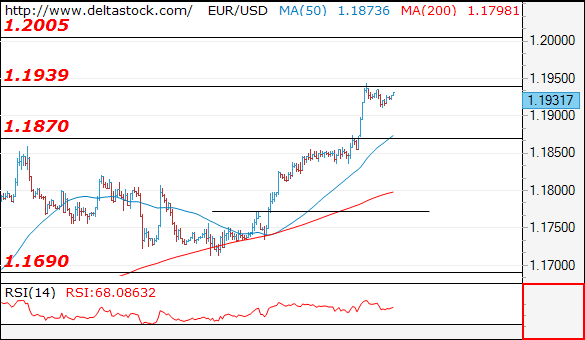

EUR/USD – Lack Of Events Leaves Euro Unchanged

The euro has started the week with little movement. Currently, EUR/USD is trading at 1.1934, up 0.01% on the day. On the release front, there are no eurozone events. In the US, the sole indicator is New Home Sales, which is expected to slow to 627 thousand. On Tuesday, the US releases CB Consumer Confidence, with an estimate of 123.9 points. We’ll also hear from Fed Chair Designate Jerome Powell and Treasury Secretary Steven Mnuchin.

German indicators continue to point upwards, and the week ended on a positive note, as German Ifo Business Climate in November set another record high. The indicator climbed to 117.5, above the estimate of 116.6 points. On Thursday, Final GDP in the third quarter accelerated to 0.8%, its strongest quarter since 2014. Manufacturing PMI surged to 62.5, pointing to strong expansion in the manufacturing sector. On the political front, there are renewed hopes that another election can be avoided, as the SPD (socialist democrats) have reluctantly agreed to hold coalition talks with Merkel’s conservative bloc. The SPD was the junior partner in the previous government, and is expected to come with a shopping list if it agrees to a “grand” coalition. This could mean more government spending and no cap on asylum seekers. The euro has not lost a stride since the political crisis, and on Friday, the currency pushed above 1.19 for the first time since late September.

Federal Reserve policymakers remain upbeat about the U.S economy, according to the minutes of the most recent policy meeting. The minutes indicated that policymakers expected the U.S economy to continue showing strong growth, and predicted that interest rates will be raised in the “near term”. The members discussed the vexing question of why inflation has been persistently low (no quick-fix solution was provided), with most agreeing that a tight labor market should lead to higher inflation levels. Although policymakers did not provide further hints about the timetable of a rate hike, the markets remain convinced that additional rates are imminent. The odds of a rate hike in December are 93%, and the odds of a January raise are at 91%.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1931

The uptrend is still intact, currently testing 1.1940 resistance area. Next resistance lies at 1.2000 and initial support is projected at 1.1870.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1940 | 1.1940 | 1.1870 | 1.1690 |

| 1.2000 | 1.2090 | 1.1835 | 1.1550 |

USD/JPY

Current level - 111.34

The rebound above 111.00 was capped at 111.70 and the intraday bias is bearish, for another test of the mentioned support. An eventual break will expose 109.50 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.90 | 112.70 | 111.00 | 109.50 |

| 112.70 | 114.70 | 109.50 | 107.30 |

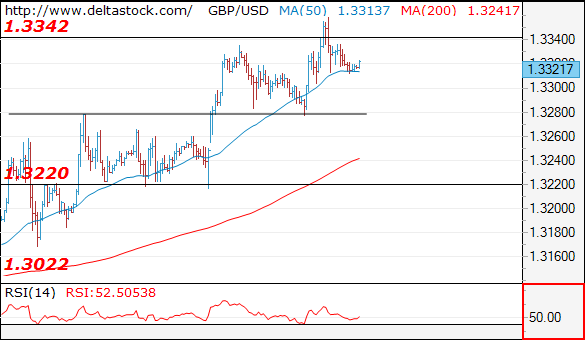

GBP/USD

Current level - 1.3321

The uptrend is still underway and a clear break through 1.3340 area will challenge 1.3460 zone. Crucial on the downside is 1.3280 low.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3340 | 1.3340 | 1.3280 | 1.3220 |

| 1.3460 | 1.3460 | 1.3220 | 1.3020 |

Elliott Wave Analysis: EURUSD And AUDUSD Update

Markets did not move much since Sunday open, so trends since Friday are still intact.

We have seen an interesting strong run up on EURUSD right into Sep 24 gap where pair slowed down last week, but not for long as we see market making a corrective wave four which is expected to find a base at 1.1910/1.1880 area.

EURUSD, 1H

Finally after a very long-time commodity currencies area moving in-line with current euro gains. We see Aussie turning up with five-waves within wave A, first part of a three-wave bullish reversal and now even breaching higher towards wave C. Wave C must also unfold five minor waves, which means more upside may follow on AUDUSD, idally towards 0.7667 level.

AUDUSD, 1H

USD On The Back Foot Again

It's been a relatively slow start to what is otherwise likely to be a busy week for the markets, with appearances from prominent central bankers being accompanied by numerous data releases.

As is so often the case, Monday is looking a little quiet compared to what is to come although we will hear from two notable central bankers – FOMC voter Neel Kashkari and Bank of England Chief Economist Andy Haldane. Kashkari is arguably the most dovish of the current crop of voters on the FOMC and has been open about his objection to further rate hikes which would suggest he's preparing to dissent at the meeting in December, when the central bank is expected to raise interest rates. I would expect him to remain of this opinion when he speaks today.

Haldane on the other hand was one of those on the Monetary Policy Committee that backed a rate hike having not done so previously and it will be interesting to see whether he supports the current outlook of two of the next few years, or whether he feels further action is warranted in the more immediate future. I imagine Haldane will take a more conservative approach once again, with the recent hike having come at a very uncertain and difficult time for the UK economy.

US equity markets are poised to open a little higher again on Monday after having recovered in the latter part of last week to trade back at record highs. A strong showing for online retailers on Black Friday may have boosted sentiment, with Cyber Monday having the potential to be even better in a sign that the consumer is healthier than other numbers this year have indicated. New home sales from the US will also be in focus today.

The US dollar is starting the week on the back foot again after coming under significant pressure in the latter part of last week. While progress is being made on tax reforms, traders may well be doubting how quickly they will be enacted and how significant the final draft will be for the economy and therefore interest rates.

Technical Outlook: SPOT GOLD – Daily Cloud Base Continues To Cap Near-Term Action

Spot Gold maintains bullish bias on weaker dollar and concerns about Fed's next steps regarding interest rates, but upside attempts were repeatedly limited.

Recovery faces very strong resistance, provided by the base of widening daily cloud which repeatedly resisted several attacks last week.

Firmly bullish daily techs suggest further upside and test of $1297 (Fibo 38.2% of $1357/$1260 descend) and psychological $1300 barrier, which requires firm break above cloud base (1294). Stronger bullish acceleration would expose another key barrier at $1309 (daily cloud top/50% retracement) break of which is needed to confirm bullish continuation. Conversely, repeated close below daily cloud would signal further extension of near-term congestion and also keep the downside at risk.

Res: 1297, 1300, 1306, 1309

Sup: 1286, 1283, 1281, 1274

Technical Outlook: AUDUSD – Limited Recovery But Key 20SMA / Trendline Barriers Remain Under Pressure

The pair remains congested between 10 SMA (0.7596) and 20SMA (0.7632) which caps upside attempts for the third straight day, along with bear-trendline from 0.8102 (20 Sep high).

Corrective action from 0.7530 (21 Nov low) is likely to be capped here as overall trend remains bearish and overbought slow stochastic is generating negative signal on daily chart.

However, bullishly aligned near-term studies are supportive for further upside on firm break above trendline / 20SMA.

Extended upticks would look for 55SMA barrier (0.7677) and expected to be capped by 200SMA (0.7694), before bears resume for retest of key 0.7530 support.

Res: 0.7632, 0.7665, 0.7667, 0.7694

Sup: 0.7596, 0.7584, 0.7555, 0.7530

NZD/JPY 1H Chart: Kiwi Moves Sideways

The NZD/JPY currency pair has been guided by three channels. The most senior one was formed mid-June. The Kiwi tested a 2016/2017 high at 84.00 a month later and then edged lower. Meanwhile, the pair bounced off the bottom boundary of the senior channel and the monthly S1 at 76.3025 last week. It started to move in a slight movement up, but has nevertheless failed to accelerate. Currently, the pressure of the monthly S1 and the 200-hour SMAs from both sides are squeezing the Kiwi in a continually narrowing trading range. In case the latter is breached, a subsequent surge is expected to occur towards the monthly PP at 78.86. Conversely, a breakout of the strong support cluster formed by the monthly and weekly S1s at 76.2960 are likely to guide the Kiwi down to the monthly S2 at 74.80.