Sample Category Title

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7610; (P) 0.7630; (R1) 0.7651; More...

AUD/USD's fall from 0.8124 is still in progress and reaches as low as 0.7575 so far. Intraday bias remains on the downside for next key cluster level at 0.7322/8. On the upside, above 0.7649 minor resistance will turn intraday bias neutral. But outlook will stay bearish as long as 0.7729 resistance holds.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

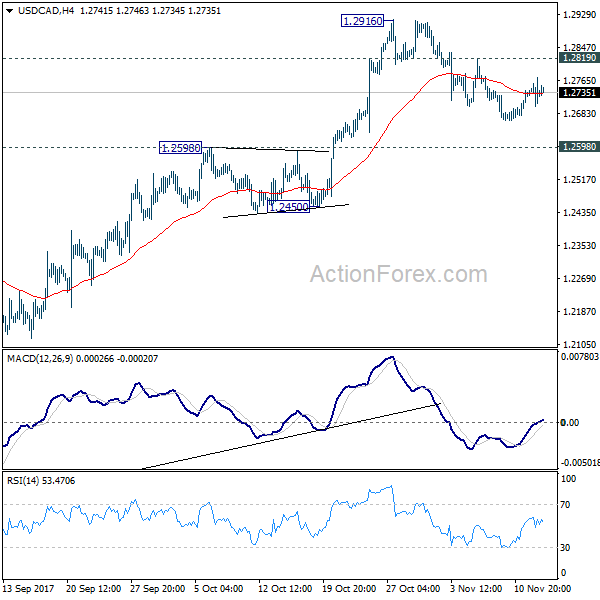

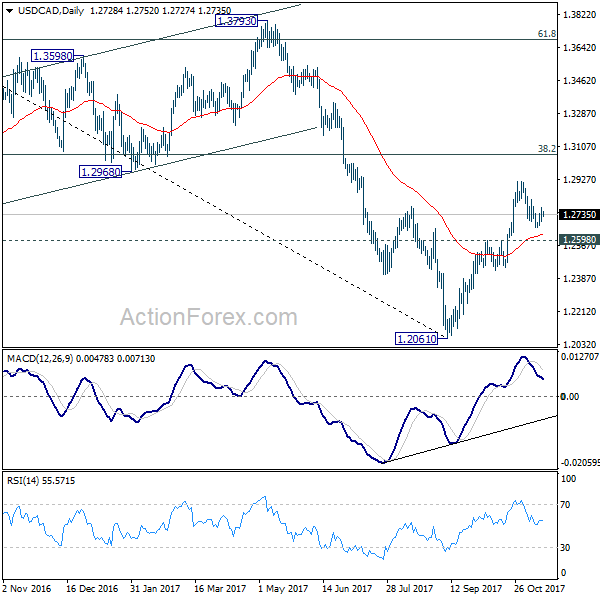

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2696; (P) 1.2734; (R1) 1.2768; More....

At this point, USD/CAD's correction from 1.2916 could still extend lower. But still, near term outlook remains bullish as long as 1.2598 resistance turned support holds. On the upside, above 1.2819 minor resistance will turn bias back to the upside for 1.2916 high first. Break there will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2916). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

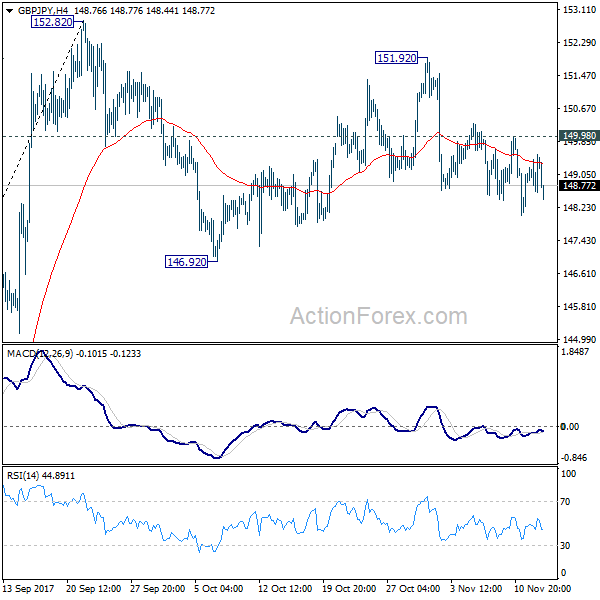

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.79; (P) 149.17; (R1) 149.73; More...

Intraday bias in GBP/JPY remains mildly on the downside for 146.92 support and below. Fall from 151.92 is seen as the third leg of the corrective pattern from 152.82. We'd expect strong support from 61.8% retracement of 139.29 to 152.82 at 144.45 to contain downside and bring rebound. On the upside, break of 149.98 resistance will turn bias back to the upside for 151.92/152.82 resistance zone instead.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

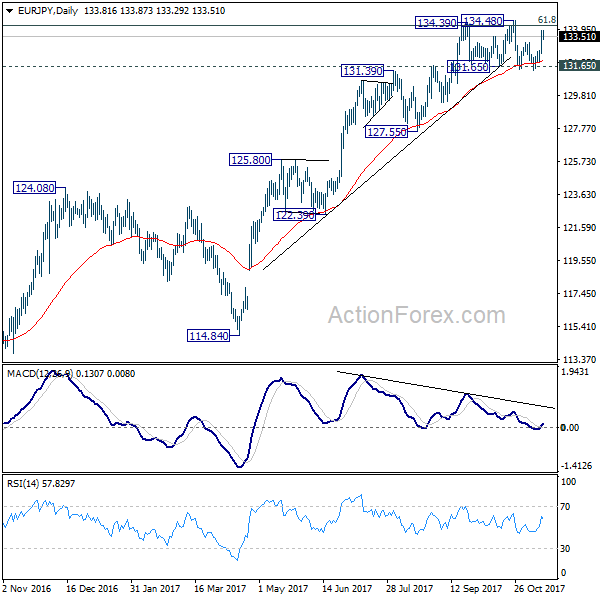

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.93; (P) 133.38; (R1) 134.29; More....

EUR/JPY rebounds further but stays in range of 131.65/134.48 and intraday bias remains neutral at this point. On the upside, decisive break of 134.39/48 resistance zone will confirm medium term up trend resumption. In that case, 141.04 resistance will be the next time. On the downside, though, decisive break of 131.65 will confirm rejection from 134.20 fibonacci level and confirm near term reversal. And, in such case, intraday bias will be turned to the downside for 127.55 key support level.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will argue that the medium term trend has reversed and will turn outlook bearish for deeper fall back to 114.84/124.08 support zone at least.

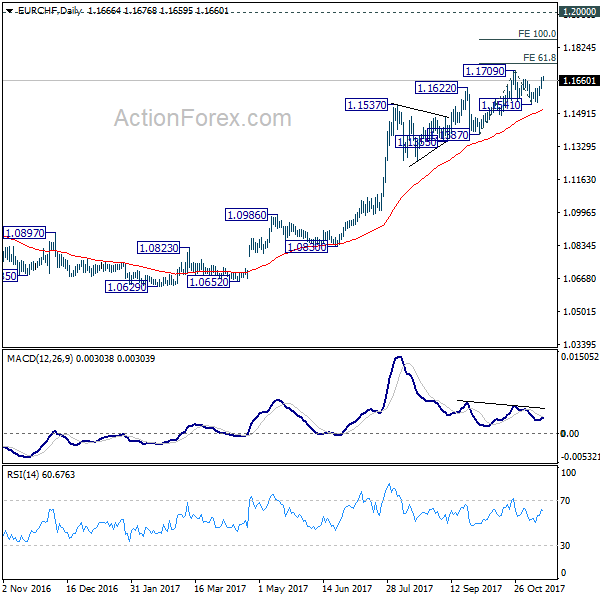

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1635; (P) 1.1655; (R1) 1.1691; More...

EUR/CHF's break of 1.1663 minor resistance suggests that pull back from 1.1709 has completed with three waves down to 1.1541 already. Intraday bias is back on the upside for 1.1709 resistance first. Break there will resume medium term rally and target 61.8% projection of 1.1387 to 1.1709 from 1.1541 at 1.1740 first, and then 100% projection at 1.1863. For now, this will be the favored case as long as 1.1541 support holds.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1105) and possibly below.

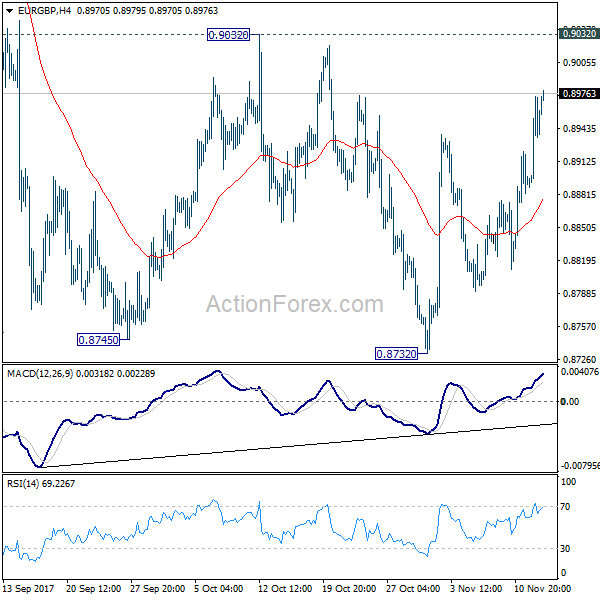

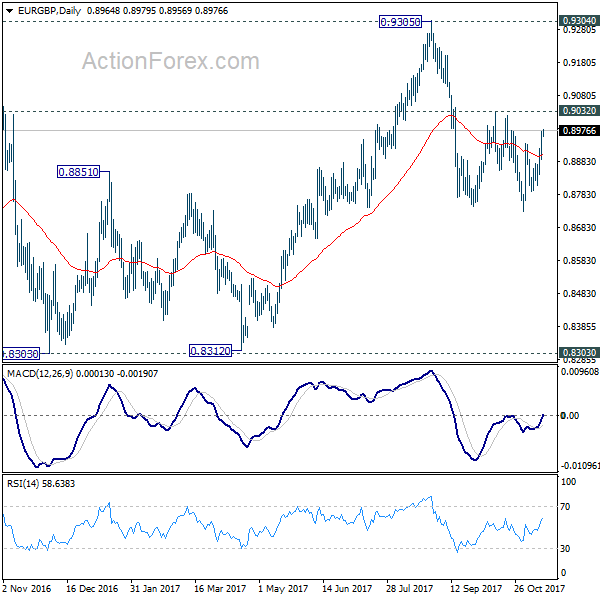

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8792; (P) 0.8840; (R1) 0.8889; More...

EUR/GBP's rebound from 0.8732 extends higher today but still, it's staying in range of 0.8732/9032. Intraday bias remains neutral first. With 0.9032 resistance intact, deeper decline is mildly in favor in the cross. Break of 0.8732 will resume the decline from 0.9305 and target 0.8303 key support level. However, on the upside, decisive break of 0.9032 will confirm completion of the decline from 0.9305. In such case, intraday bias will be turned back to the upside for retesting 0.9305 key resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

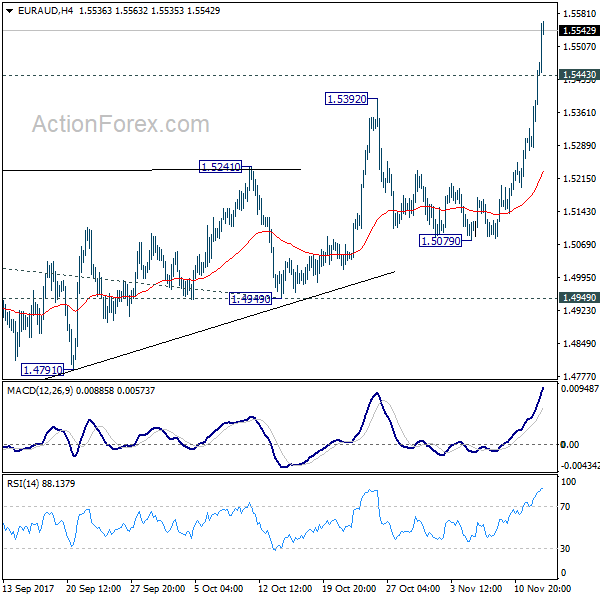

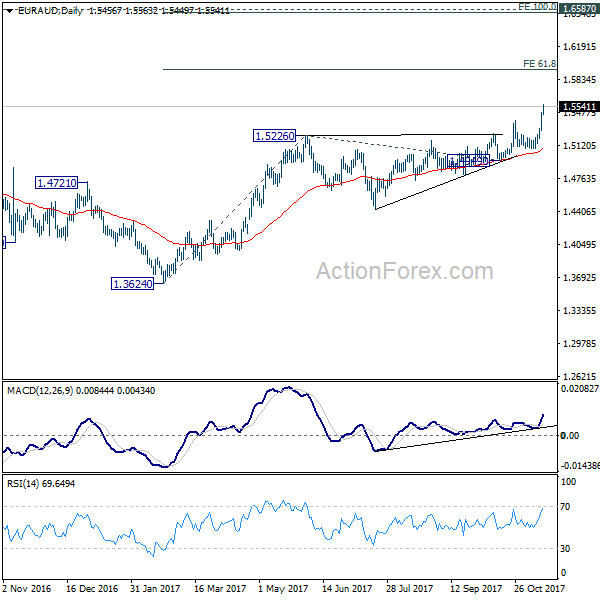

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5332; (P) 1.5402; (R1) 1.5525; More....

EUR/AUD's strong break of 1.5392 resistance confirms resumption of medium term rally from 1.3624. Intraday bias stays on the upside for 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. Break will target 100% projection at 1.6551, which is close to 1.6587 key resistance. On the downside, below 1.5443 minor support will turn intraday bias neutral and bring consolidations before staging another rally.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low).

Wage Growth Miss Hammers Australian Dollar, Yen Surges as GDP Disappoints

Australian dollar tumbles broadly today as wage growth data disappoints. That also add to case for RBA to divergence from global tightening and stand pat ahead. Yen surges broadly as GDP miss pressures Nikkei. But Yen is outperformed by Euro, which surges this week on strong German GDP data. Euro is firm in Asian session and is on course for further rally. More important economic data will be released today. Sterling will look into employment data for some support. Meanwhile, Dollar will look into CPI and retail sales to solidify the case for a December Fed hike.

Australian wage growth missed expectations

Australia wage price index rose 0.5% qoq in Q3, unchanged from quarter's figure and missed expectation of 0.7% qoq. Annually, wage grew 2.0% yoy, also missed expectation of 2.2% yoy. Growth in wage was driven by end of financial year salary reviews as well as the annual minimum wage review. The 3.3% rise in minimum wage already boosted quarterly wage growth by 0.2%. Hence, considering all factors, wage growth was like non-existent in the September quarter. And that clearly support RBA's neutral stance to divergence from global monetary tightening and stands pat ahead. Also from Australia, Westpac consume confidence dropped -1.7% in November.

Yen surges on Japan GDP miss

Japan GDP grew 0.3% qoq in Q3, below expectation of 0.4% qoq. That's also just half of prior quarter's 0.6% qoq. Nonetheless, that's still the second straight quarter of growth, held by exports as global economy recovers. GDP deflator rose 0.1% yoy, in line with consensus. Japanese markets respond quite negatively to the data as Nikkei stays weak after the release and is losing -200 pts, or -0.9% at the time of writing. Yen trades inversely proportional to Nikkei and surges higher.

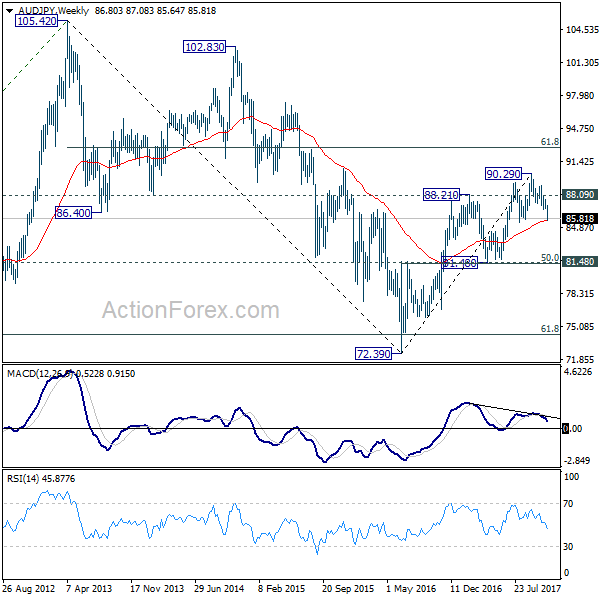

AUD/JPY heading back to 81.34/48 key medium term support

The sharp decline in AUD/JPY this week affirms the case that medium term rebound form 72.39 has completed at 90.29 already, on bearish divergence condition in weekly MACD. Near term outlook will now stay bearish as long as 88.09 resistance holds. Sustained break of 55 week EMA (now at 85.59) will pave the way to key cluster support at 81.48 (50% retracement of 72.39 to 90.29 at 81.34.

St Louis Fed Bullard concerned with Fed hike

St Louis Fed President James Bullard said yesterday that "inflation data during 2017 have surprised to the downside and call into question the idea that U.S. inflation is reliably returning toward target." And he warned that "the main concern I would have is that we raise rates in December and inflation expectations fall... which would in my view be a vote of no confidence from markets."

Currently, fed fund futures are pricing in 96.7% chance another rate hike by Fed in December to 1.25-1.50%. The CPI data to be released today will be a key to solidify this case for the Fed.

News regarding tax plan will also be crucial for the Dollar. It's reported that Senate Republicans would include a repeal of the Obamacare individual mandate with their version of the tax bill. Such an act could complicate the efforts to rush to pass the reconciled bill in both chambers. But it's also seen as a move that can help to pay for the proposed tax cuts by slashing more than USD 300b in government spending over 10 years. Senate Majority Leader Mitch McConnell expressed his confidence that "we're optimistic that inserting the individual mandate repeal would be helpful."

Looking ahead

The economic calendar is full of key data today. UK job data will be a major focus in European session. Sterling is trading as the weakest European and will need to draw support from very solid data. Eurozone will also release trade balance.

Later in the day, US CPI and retail sales will be the main feature. Empire state manufacturing index and business inventories will also be featured.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5332; (P) 1.5402; (R1) 1.5525; More....

EUR/AUD's strong break of 1.5392 resistance confirms resumption of medium term rally from 1.3624. Intraday bias stays on the upside for 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. Break will target 100% projection at 1.6551, which is close to 1.6587 key resistance. On the downside, below 1.5443 minor support will turn intraday bias neutral and bring consolidations before staging another rally.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Nov | -1.70% | 3.60% | ||

| 23:50 | JPY | GDP Q/Q Q3 P | 0.30% | 0.40% | 0.60% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 P | 0.10% | 0.10% | -0.40% | |

| 00:30 | AUD | Wage Price Index Q/Q Q3 | 0.50% | 0.70% | 0.50% | |

| 04:30 | JPY | Industrial Production M/M Sep F | -1.10% | -1.10% | ||

| 09:30 | GBP | Jobless Claims Change Oct | 2.4K | 1.7K | ||

| 09:30 | GBP | Claimant Count Rate Oct | 2.30% | |||

| 09:30 | GBP | Average Weekly Earnings 3M/Y Sep | 2.10% | 2.20% | ||

| 09:30 | GBP | ILO Unemployment Rate 3M Sep | 4.30% | 4.30% | ||

| 09:30 | GBP | Employment Change 3M/3M Sep | 50k | 94k | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Sep | 21.4B | 21.6B | ||

| 13:30 | USD | CPI M/M Oct | 0.10% | 0.50% | ||

| 13:30 | USD | CPI Y/Y Oct | 2.00% | 2.20% | ||

| 13:30 | USD | CPI Core M/M Oct | 0.20% | 0.10% | ||

| 13:30 | USD | CPI Core Y/Y Oct | 1.70% | 1.70% | ||

| 13:30 | USD | Empire State Manufacturing Nov | 25 | 30.2 | ||

| 13:30 | USD | Advance Retail Sales M/M Oct | 0.00% | 1.60% | ||

| 13:30 | USD | Retail Sales Ex Auto M/M Oct | 0.20% | 1.00% | ||

| 15:00 | USD | Business Inventories Sep | 0.00% | 0.70% | ||

| 15:30 | USD | Crude Oil Inventories | 2.2M | |||

| 21:00 | USD | Net Long-term TIC Flows Sep | 34.6B | 67.2B |

EUR/USD Benefiting From USD Weakness, Ripping Higher

Amid a lack of European positive data, EUR/USD has pushed back above major horizontal range resistance.

EUR/USD Hourly:

A 130 pip, straight line rally like this on an intraday chart without the accompaniment of a news release isn’t something you see everyday and speaks volumes about the markets that we’re seeing lately.

Strong selling pressure can be seen across the majors and with Euro breaking above and reactivating that highly significant support/resistance level, the pair has been a major benefactor.

EUR/USD Weekly:

Euro Reigns Supreme

Euro reigns supreme

The Euro regained its debatably rightful throne as King of the Hill overnight stampeding higher across the board as currency traders applauded German GDP after Q3 YoY printed an impressive 2.8 %, the highest rate since 2011.

And while the GDP print provided the initial catalyst, the velocity of the move suggests that investors are finally discounting the ECB dovish guidance in the face of stronger economic data and have now entirely back -peddled the sell-off in EUR following the Draghi press conference on October 26.

Besides the robust economic data, there was no shortage of ECB dissenter Hawks flying into the picture last week that probably added to the momentum. As we test the 1.1800 level in early APAC trade, the ECB’s dovish taper is all but a distant memory.

But it was a challenging day for the dollar across the board as investors were unabashedly offloading $ risk ahead of tonight’s critical US CPI print. And, with year-end quickly approaching, investors are more predisposed to reduce rather than hold risk, so USD appetite was low anyway.

It wasn’t just the dollar that was getting hammered but EM investors were dialling into the year-end mode as well and reducing risk.Predictably the natural risk-correlated assets were moving in tandem as Gold suddenly spiked up to over 1280.00, USDJPY came off the interday highs, and WTI prices spilt lower.

While not quite the perfect storm for dollar bulls, indeed a sobering reminder about the greenbacks numerous shortcomings. And what started off as little more than an exercise in consolidation could quickly snowball into an all-out blizzard, even more so with the judge Roy Moore scandal presenting blustery headwinds to tax cuts and the Republican Senate majority

Petro FX

In oil markets, it was more or less a belief that eventually, something had to give after this months 10 % tireless rally.And while the overnight sell-off started with a global risk wobble, profit-taking likely triggered the more significant move amidst extended money manager position in the petroleum complex. But given the correlation between oil and FX has been sidelined most of the year, any proportional currency knock-on effect should be limited. The market remains ramped up bullish crude, so currency traders expect any correction to be finite.

The Japanese Yen

Another chop fest, but if anything, overnight price action should remind us just how entrenched current ranges are as positions are quick to mean revert from the maximal edges. But traders are becoming frustrated and capricious and getting no joy from long USDJPY. With that in mind, a definitive broader-based selling theme is developing from uncertainty on both risk and US inflation narratives. So I suspect only a considerable upside surprise on CPI will get the markets anywhere near 114.50 levels suggesting the downside may open up on a CPI fail

The Australian Dollar

Just when the Aussie looked positioned to move below.7600 The frothy NAB business conditions in October said NO. Unquestionably a solid print, but the AUDUSD couldn’t muster up enough steam to clear .7650 even when the big dollar wobbled overnight. If it’s not a perceived dovish shift in the dormant RBA, its fickle economic data out of China and yesterday’s dialled back China production numbers have weighed on commodity prices overnight, and the Aussie is once again mouldering at the lower end of recent ranges.

Indeed the bearish signals are aligning, but I’m not sure just how much energy the market has left heading into year-end to make any significant downside assault. Stretched positions are suggesting any move lower will most likely be driven by US side of the equation which at this stage is as big a question mark as what the RBA policy will be in 2018.