Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1584; (P) 1.1631 (R1) 1.1708; More...

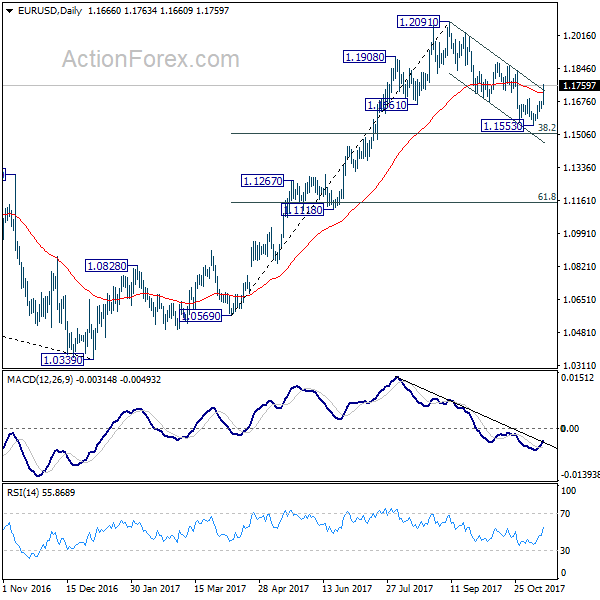

EUR/USD surges to as high as 1.1759 so far today. The strong break of 1.1689 minor resistance and near term falling channel indicates the correction from 1.2091 has completed at 1.1553 already. Intraday bias is now back on the upside for 1.1836 resistance first. Break there will pave the way to retest 1.2091 high. On the downside, below 1.1689 resistance turned support will turn bias back to the downside for 1.1553 low instead.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1346) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Solid GDP Data Boosts Euro, EUR/USD Reversing Near Term Trend

Euro surges broadly today as supported by solid economic data that supports ECB's tapering plan next year. Growth in Germany was particularly impressive. Technically, EUR/USD's strong break of 1.1689 resistance now indicates near term reversal. And more upside would likely be seen back to 1.18 level. Euro's strength also helps lift its cousin Swiss Franc, which follows as the second strongest one. On the other hand, Sterling remains one of the weakest as CPI was unchanged at a five year high but didn't accelerate. Both Dollar and Yen are also struggling.

Eurozone GDP Solid, Germany and Italy accelerated

Eurozone GDP grew 0.6% qoq in Q3, in line with consensus and maintained same pace as prior quarter. German GDP grew more than expected by an impressive 0.8% qoq, up from 0.6% in Q2, beat consensus at 0.6% qoq. The steam engine of Eurozone is now on track for the best year since 2011. Italy GDP grew 0.5% qoq, up from Q2's 0.3%, in line with consensus. Eurozone industrial production dropped -0.6% mom in September. German CPI was finalized at 1.6% yoy in October. Also from Europe, Swiss PPI rose 0.5% mom, 1.2% yoy in October.

ZEW: Prospects remain encouragingly positive

German ZEW economic sentiment rose to 18.7 in November, up from 17.6 but missed expectation of 19.5. Current situation gauge rose to 88.8, up from 87.0 and beat expectation of 88.0. Eurozone ZEW economic sentiment rose to 30.9, up from 26.7 and beat expectation of 30.9. ZEW President Achim Wambach noted in the release that "the prospects for the German economy remain encouragingly positive. Overall high levels of growth across Europe in the third quarter are supporting further growth in Germany and boosting expectations for the coming six months. This favorable economic climate should be used to create a stronger and more robust basis for future growth."

Draghi, Yellen, Carney, Kuroda speak at ECB conference

Speaking in a ECB conference in Frankfurt, ECB President Mario Draghi declared that "forward guidance" is a success and has now "become a full-fledged monetary policy instrumental". Still-Fed chair Janet Yellen also said that forward guidance is useful but "all guidance should be conditional and related to the outlook for the economy. Yellen also said that Fed could be confusing the public with the voices of so many officials and "this is really one of the challenges of our system". BoJ Governor Haruhiko Kuroda urged policy makers to communicate and explain in a straightforward manner to the public. BoE Governor Mark Carney urged a reasonable transition period post Brexit.

UK CPI didn't accelerate in October

UK headline CPI was unchanged at five year high of 3.0% yoy in October, below expectation of 3.1%. Core CPI was also unchanged at 2.7% yoy, below expectation of 2.8% yoy. RPI accelerated to 4.0% yoy, below expectation at 4.1% yoy. PPI input slowed to 4.6% yoy versus expectation of 4.7% yoy. PPI output slowed to 2.8% yoy versus expectation at 3.3% yoy. PPI output core slowed to 2.1% yoy, below expectation of 2.2% yoy. House price index rose 5.4% yoy in September, above expectation of 5.2% yoy.

Chicago Fed Evans advocates price-level targeting

Chicago Fed President Charles Evans called for a new approach in setting interest rates. One option that becomes handy during time that interest rates alone are not enough to responds to market shock is "price-level targeting". This echoes comments from San Francisco Fed President John Williams, who also embraced price-level targeting. The key idea is that inflation would be allowed to run high for a period of time in situation when inflation is too low. Evan's main message is that "we should be planning for these inevitable future situations today."

Dallas Fed President Robert Kaplan said he is "actively considering" to vote for another rate hike in December. He said in an interview that "history has shown that normally when we have a substantial overshoot the Fed ultimately needs to take actions to play catch-up". For now, unemployment rate at 17 year low in October required additional vigilance.

Released from US, PPI accelerated to 2.8% yoy in October, above expectation of 2.3%. PPI core accelerated to 2.4% yoy, above expectation of 2.2% yoy.

Australia NAB: Better than expected performance for the economy ahead

In Australia, NAB business conditions jumped 7 points to 21 in October, hitting the highest level the series began back in 1997. It's also nearly four times the historical average. Business confidence, on the other hand, was unchanged at 8. NAB chief economist Alan Oster noted that "this is an extremely strong result and of itself would suggest a better than expected performance for the economy." However, he also warned that "it is unclear just how long conditions can remain at these record levels given that the result was driven by a surprise jump in manufacturing, while some of the leading indicators such as forward orders - which have been giving a more accurate read on the strength of the economy - have actually softened a little in recent months."

Bond yields jump in China

Notwithstanding disappointing headlines, China's economic activities and credit conditions in October were a result of the government's regulatory tightening and the "neutral and prudent" monetary policy with a tighter bias. China's 10 year yields jumped to a 3-year high, approaching 4%, while 5-year yields breached 4% the first time in over 3 years, on Tuesday.

The surge in yields can be attributed to a confluence of factors, including a selloff of sovereign bonds after softer-than-expected macroeconomic data and a reflection of tightened liquidity in the financial system. However, we believe the most critical factor is the rallies in US yields, on expectations of a December rate hike, and UK yields, amidst BOE's rate hike earlier this month.

Released today, retail sales rose 10.0% yoy in October, below expectation of 10.5% and slowed from prior 10.3% yoy. Fixed asset investment rose 7.3% yoy, inline with expectation but slowed from prior 7.5% yoy. Industrial production rose 6.2% yoy, meeting consensus but also slowed from prior 6.6 yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1584; (P) 1.1631 (R1) 1.1708; More...

EUR/USD surges to as high as 1.1759 so far today. The strong break of 1.1689 minor resistance and near term falling channel indicates the correction from 1.2091 has completed at 1.1553 already. Intraday bias is now back on the upside for 1.1836 resistance first. Break there will pave the way to retest 1.2091 high. On the downside, below 1.1689 resistance turned support will turn bias back to the downside for 1.1553 low instead.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1346) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Oct | 8 | 7 | 8 | |

| 02:00 | CNY | Retail Sales Y/Y Oct | 10.00% | 10.50% | 10.30% | |

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Oct | 7.30% | 7.30% | 7.50% | |

| 02:00 | CNY | Industrial Production Y/Y Oct | 6.20% | 6.20% | 6.60% | |

| 07:00 | EUR | German GDP Q/Q Q3 P | 0.80% | 0.60% | 0.60% | |

| 07:00 | EUR | German CPI M/M Oct F | 0.00% | 0.00% | 0.00% | |

| 07:00 | EUR | German CPI Y/Y Oct F | 1.60% | 1.60% | 1.60% | |

| 08:15 | CHF | Producer & Import Prices M/M Oct | 0.50% | 0.20% | 0.50% | |

| 08:15 | CHF | Producer & Import Prices Y/Y Oct | 1.20% | 0.80% | ||

| 09:00 | EUR | Italian GDP Q/Q Q3 P | 0.50% | 0.50% | 0.40% | 0.30% |

| 09:30 | GBP | CPI M/M Oct | 0.10% | 0.20% | 0.30% | |

| 09:30 | GBP | CPI Y/Y Oct | 3.00% | 3.10% | 3.00% | |

| 09:30 | GBP | Core CPI Y/Y Oct | 2.70% | 2.80% | 2.70% | |

| 09:30 | GBP | RPI M/M Oct | 0.10% | 0.20% | 0.10% | |

| 09:30 | GBP | RPI Y/Y Oct | 4.00% | 4.10% | 3.90% | |

| 09:30 | GBP | PPI Input M/M Oct | 1.00% | 0.80% | 0.40% | 0.20% |

| 09:30 | GBP | PPI Input Y/Y Oct | 4.60% | 4.70% | 8.40% | 8.10% |

| 09:30 | GBP | PPI Output M/M Oct | 0.20% | 0.30% | 0.20% | |

| 09:30 | GBP | PPI Output Y/Y Oct | 2.80% | 2.90% | 3.30% | |

| 09:30 | GBP | PPI Output Core M/M Oct | 0.10% | 0.20% | 0.00% | -0.10% |

| 09:30 | GBP | PPI Output Core Y/Y Oct | 2.10% | 2.20% | 2.50% | |

| 09:30 | GBP | House Price Index Y/Y Sep | 5.40% | 5.20% | 5.00% | |

| 10:00 | EUR | Eurozone Industrial Production M/M Sep | -0.60% | -0.60% | 1.40% | |

| 10:00 | EUR | German ZEW Economic Sentiment Nov | 18.7 | 19.5 | 17.6 | |

| 10:00 | EUR | German ZEW Current Situation Nov | 88.8 | 88 | 87 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | 30.9 | 29.3 | 26.7 | |

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | 0.60% | 0.60% | 0.60% | |

| 13:30 | USD | PPI M/M Oct | 0.40% | 0.10% | 0.40% | |

| 13:30 | USD | PPI Y/Y Oct | 2.80% | 2.30% | 2.60% | |

| 13:30 | USD | PPI Core M/M Oct | 0.40% | 0.20% | 0.40% | |

| 13:30 | USD | PPI Core Y/Y Oct | 2.40% | 2.20% | 2.20% |

Will USD Index Continue Lower, or Will it Reverse Higher?

Good day traders. Hope everybody is having a splendid day.

Today we will look at USD Index and its mid-term view.

USD Index can still be trading within a higher degree bearish impulse, with current rise labeled as a potential wave 4). If that is the case, then rally since start of September can see limited upside near the upper trendline and unfold a drop in five waves for the upcoming wave 5). But if price continues higher, and decisevely breaches above the trendline, then this would suggest a completed bearish impulse and a change in trend from bearish to bullish.

USD Index, Daily

Canadian Dollar Steady, US Inflation Data Next

The Canadian dollar has edged higher in the Tuesday session. In the North American session, USD/CAD is trading at 1.2713, down 0.16% on the day. On the release front, there are no Canadian indicators on the schedule. Central bankers will attend an ECB event in Frankfurt, with Fed Chair Janet Yellen participating in a panel discussion. The US will release PPI reports, which are expected to show very small gains. Wednesday promises to be busy, with the US releasing CPI and retail sales reports.

US President Trump is wrapping up his tour of Asian Pacific countries, and he reiterated his message of "America first". This protectionist stance could signal trouble for Canada and Mexico, as Trump has vowed to renegotiate the NAFTA free trade agreement. On his Asian trip, Trump reiterated that he favors bilateral trade agreements rather than multilateral arrangements. Negotiators from the three countries are meeting for another round of talks on Wednesday, and by all accounts, the talks are progressing slowly. NAFTA covers more than $1 trillion a year in trade, and if the agreement is not renegotiated, the Canadian economy will be adversely affected, and the Canadian dollar would likely lose ground against the greenback.

Investors are keeping close eye on developments with President Trump's tax proposal. There are some differences in the House and Senate bills, with some Republicans opposed to eliminating federal deductions of state and local taxes. The Republicans hope to present Trump with a new tax code by the end of the year, but with Democrats putting up fierce resistance, it's unclear whether the bill will have enough votes to get through Congress. If the proposal is successful, the resulting economic growth could lead to higher interest rates, which would likely boost the US dollar against other currencies.

WTI OIL – Break Below Rising 10SMA is Needed to Generate Stronger Reversal Signal

WTI oil remains in red on Tuesday with reversal signal developing on daily chart but downside attempts are still limited and holding above rising 10SMA which marks the first pivot at $56.27.

Near-term price action shows no clear direction on mixed fundamentals as prospects for further increase of US production offsets expectations for further tightening in oil market on OPEC-led output cut which is likely to extend.

Overextended daily studies are negative indication with bearish signal developing on attempts of daily RSI to return from overbought territory.

Initial requirement for stronger bearish acceleration is close below 10SMA which would open support at $55.82 (Fibo 23.6% of $49.09/$57.90) and more significant support at $54.53 in extension (Fibo 38.2% / rising 20SMA).

Falling hourly cloud (spanned between $56.82 and $57.02) is expected to cap and maintain bearish near-term bias.

Res: 56.82; 57.02; 57.51; 57.90

Sup: 56.29; 55.82; 54.53; 53.88

EURUSD Strengthens, Targets The 1.1750/99 Zone

EURUSD: With the pair strengthening further on Tuesday, more gain is expected in the days ahead. Resistance comes in at 1.1750 level with a cut through here opening the door for more upside towards the 1.1800 level. Further up, resistance lies at the 1.1850 level where a break will expose the 1.1900 level. Its daily RSI is bullish and pointing higher suggesting further strength. Conversely, support lies at the 1.1700 level where a violation will aim at the 1.1650 level. A break of here will aim at the 1.1600 level. Below here will open the door for more weakness towards the 1.1550. All in all, EURUSD faces further corrective recovery threats.

US Inflation Expected to Ease as Fed Preps to Raise Rates Again

A run of strong economic indicators in the United States in recent weeks has left investors in no doubt that the Federal Reserve is on track to raise interest rates for a third time this year at its December policy meeting. Inflation data due on Wednesday is unlikely to shift those expectations much even if the figures were to cast some further doubt that price pressures are still nowhere to be found in the US economy.

As the American economy enjoys its ninth year of expansion and with a labour market considered to be at full employment, there is yet little sign of inflation or wage growth running wild. Despite the benign outlook for inflation, the Fed has increased borrowing costs four times since the end of the financial crisis and is widely expected to raise rates again in December to a target range of 1.25%-1.50%.

With growth gaining further traction this year, Fed policymakers have been keen to gradually remove monetary accommodation. However, a prolonged delay in inflation moving towards the Fed's 2% objective may prompt a rethink of the current stance. The headline CPI rate, which is not targeted by the Fed, has already risen above 2%, but is forecast to moderate from 2.2% to 2.0% in October, while the core rate is expected to remain unchanged at 1.7% for the fifth straight month in October. The Fed's preferred measure of inflation - the core PCE price index - is running much lower at 1.3%.

A bigger-than-expected increase in the CPI rate would reinforce expectations that the Fed will continue to raise rates at the current pace next year and be supportive of further gains for the US dollar. However, a soft reading would question the sustainability of the current rate path and may deter the doves within the Fed from voting in favour of further rate hikes, putting the focus on December's FOMC projections for 2018.

Released alongside the inflation numbers will be the latest retail sales figures. Month-on-month growth in retail sales is expected to be flat in October, though given the 1.6% surge in September, the figure is unlikely to cause any alarm.

Unless there is a large surprise, Wednesday's data is not expected to cause much of a reaction in forex markets, especially as the immediate focus right now is on the US tax plan and its passage through Congress. A big miss is in the data would possibly see the dollar finding support around the 113-yen level, which has acted as the bottom of the range for the pair since late October. Upside surprises meanwhile could see dollar/yen attempting to beat November's 8-month top of 114.72, but first it would have to overcome resistance areas around 113.70 and 114.20.

CAC Slide Continues Despite Solid Eurozone Data

The CAC remains under pressure, and has posted slight losses on Tuesday. Currently, the CAC is at 5,331.50, down 0.19% on the day. On the release front, Eurozone Flash GDP remained unchanged at 0.6%, matching the forecast. ZEW Economic Sentiment jumped to 30.9, above the estimate of 29.3 points. Central bankers will attend an ECB event in Frankfurt, and the markets will be listening closely to Mario Draghi and Janet Yellen. On Wednesday, the eurozone releases Trade Balance.

The eurozone economy received a respectable grade on Tuesday, as Flash GDP for the third quarter came in at 0.6%. The eurozone expanded in Q3 at an annualized rate of 2.5 percent. Germany's robust economy has led the way, with annualized growth of 2.5%, but traditional laggards France and Italy have also rebounded in 2017. At the same time, steady growth has failed to boost inflation, which remains well behind the ECB's target of around 2.0%. German Final CPI underscored the lack of inflation, with a reading of 0.0% in October. As long as inflation remains at low levels, the ECB is likely to continue its asset purchases program.

Heads of central banks are meeting on Tuesday in Frankfurt, and will be discussing how to communicate with the markets. With central banks signalling major policy shifts, communicating clearly is a critical skill. Janet Yellen and Mario Draghi will both be participating in the discussions. The ECB is set to taper its asset-purchase program in January, while the Fed has started trimming its massive balance sheet. Both Yellen and Draghi are all-too-familiar with unwanted movement in the currency markets when investors were kept in the dark or misinterpreted the Fed or the ECB. Investors will be listening carefully, looking for clues regarding future monetary policy.

Japanese Economy Expected To Have Grown For Seventh Straight Quarter In Q3 But At Slower Pace

Japanese third quarter GDP figures are due on Tuesday, November 14 at 2350 GMT. Quarter-on-quarter, the economy is expected to have grown by 0.3%, while on an annualized basis, economic activity is projected to have expanded by 1.3%.

Should the figures come out as anticipated, then they would reflect a slowdown relative to the second quarter’s 0.6% q/q and 2.5% annualized expansion. However, they would also mark the seventh consecutive quarter of positive economic growth, the longest such stretch since the period between Q2 1999 and Q1 2001 during which the Japanese economy grew for eight straight quarters.

An upside surprise in the figures is expected to strengthen the Japanese currency. In that case, a declining dollar/yen pair could find support around the 113 mark, this being an area of congestion recently as well as 113 being a potential psychological level.

If on the other hand the numbers come out worse-than-expected, then market participants would likely push dollar/yen higher. The range around 114.50 could act as a barrier to a rising dollar/yen pair. The area around 114.50 encapsulates a number of peaks from the recent past, with the latest one being the eight-month high of 114.72 recorded on November 6. Before reaching this area though, the pair would need to clear the 114 mark, this being another potential psychological level. Should the figures differ from expectations, then the sharper the divergence the stronger the market reaction is expected to be.

Despite the world’s third largest economy being on track to expand for yet another quarter, highly accommodative fiscal and monetary policies are expected to remain in place with inflation being well below the Bank of Japan’s target of 2% on an annual basis. With the US’s Federal Reserve remaining on what looks a firm path of policy tightening, in stark contrast to the BoJ, then barring other external factors, dollar/yen is expected to move higher in the medium- to longer-term.

In the broader picture, a Chinese slowdown and a conflict with North Korea would rank high in terms of risks the Japanese economy could potentially face (with the latter one looking not that likely at the moment). On the upside, external demand due to an ever-strengthening global economic recovery would likely considerably benefit Japanese economic activity moving forward.

GBPUSD Bearish Below 1.3109 Level

The British pound has moved lower against the U.S dollar, following weaker than expected October inflation data from the United Kingdom. The GBPUSD pair currently trades around the 1.3080 mark, after falling to 1.3075, following a weaker than expected 0.1 percent monthly rise in October CPI in the UK economy. Sterling traders now look to United States inflation data for the next directional move, as the U.S economy releases key CPI and PPI data for October.

The GBPUSD pair remains intraday bearish while trading below the 1.3109 technical level, further declines towards the 1.3061 and 1.3030 support levels seems likely.

Should price-action move above the 1.3109 level, buyers likely force price-action towards the 1.3130 and 1.3168 technical regions.