Sample Category Title

USDJPY Bullish Above 113.68 Level

The U.S dollar has moved sharply higher against the U.S dollar during the European trading session, hitting 113.88, amidst strong technical buying in the USDJPY pair. Intraday sellers failed to defend the 113.68 level, which triggered an acceleration of buying interest in the USDJPY. The U.S dollar index remains mixed on the day, with traders now awaiting the key October Consumer Price inflation data from the United States economy.

The USDJPY pair remains strongly intraday bullish while trading above the 113.68 technical level. Further upside towards 114.10 and 114.50 seems increasingly likely.

Should price-action decline below the 113.68 level on the USDJPY pair, sellers will likely target the 113.24 and 112.94 technical levels.

Precious Metals And Commodities

Life has been dull on precious metals to start the week as financial markets and currencies, in particular, await the buildup to a heavy data end of the week. The passage (or not) of the U.S. tax bill is being awaited with eager anticipation. Precious metals have been range bound with gold lacking conviction but silver and platinum attempting quiet recoveries. Palladium seems set for a slight downward correction of its mega-bull trend.

Copper has an interesting triangle formation that suggests some temporary downward pressure may be to come.

Natural gas traded much higher in anticipation of colder weather in the U.S. but gave back its gains with a whimper. That said, it does appear to be gathering its strength as winter is coming!

Brent and WTI’s severely overbought RSI on both have eased somewhat, but the charts suggest the danger still lies to a correction lower within their overall bullish uptrends. The Crude Inventory data should be the first test of this theory.

Over on the soft commodities, sugar has rallied as the Brazilians cut 2018’s harvest forecasts.

Brazil is at it again in Corn and Soybeans but for different reasons this time. Rain in Brazil has produced optimum growing conditions pushing down North American prices.

Wheat feels the heat of Russia’s Black Sea region harvest and a weaker Rouble making their exports more appealing than strong U.S. dollar North American ones.

Gold 0:0:00, Silver 00:02:40, Platinum 00:04:35, Palladium 00:06:10, Copper 00:08:30, Natural Gas 00:10:15, Brent Oil 00:12:15, WTI Oil 00:16:10, Sugar 00:18:15, Corn 00:20:25, Soybeans 00:21:50, Wheat 00:23:50

Are Markets Looking Overextended?

- Equity Market Rally Appears to Have Stalled Despite Strong Earnings Season;

- GBP Slips Further After Softer Than Expected Inflation Data;

- Fed, ECB, BoE and BoJ Heads Create No Shocks in Panel Discussion;

- API Data May Support Oil Rally in Near-Term.

It's been a mixed start to trading again on Tuesday and US futures are pointing to similar moves ahead of the open, a sign that markets are starting to look a little overextended.

The rally in equity markets has been very gradual and relatively uninterrupted over the last couple of months, leading many to question whether a correction of some kind is both warranted and healthy. Despite another strong earnings season, the rally has stalled which suggest we may now be a levels again that investors can't justify going far above, which may leave them susceptible to a pull back, even one that isn't particularly large.

After getting off to another tough start on Tuesday, driven primarily by increased political risk and Brexit concerns, the pound suffered further losses as CPI data fell short of market expectations and those of the Bank of England. The central bank earlier this month raised interest rates after inflation – which it claimed would peak above 3% in October – rose above the level that policy makers would tolerate, even in these exceptional circumstances.

However, with inflation having not risen as much as anticipated, the question of whether the BoE acted prematurely will likely be raised given the uncertain economic backdrop and significant headwinds facing the economy. The pound slid further after the data showed inflation rising only 3% last month – 2.7% on a core basis – although interestingly, it still remains range-bound against the dollar, euro and yen, despite the political risk, dovish rate hike and the data.

Another event today that had the potential to rattle the pound, as well as the greenback, euro and yen, was the panel discussion that took place in Frankfurt involving Janet Yellen, Mario Draghi, Mark Carney and Haruhiko Kuroda, the heads of the Federal Reserve, European Central Bank, Bank of England and Bank of Japan, respectively.

While the participants did discuss aspects of monetary policy, they avoided saying anything that caused any shock moves in the currency markets, which was possibly aided by the fact that they all recently made policy announcements and any near-term changes – i.e. Fed rate hike in December – are almost entirely priced in. While more clarity is always sought on medium to long-term policy changes, there was clearly no need or desire to say anything on this, with the heads instead reflecting on the challenges and lessons from monetary policy having ventured repeatedly into uncharted territory since the financial crisis.

While there's plenty of data coming from the US this week, Tuesday – as was the case on Monday – will be very quiet on this front. PPI data for October is the only notable release today and this typically doesn't have a great impact on the markets. The most notable release today may be the crude inventory data from API which acts as a precursor to tomorrow's EIA release and comes as oil prices trade around a more-than two year high. Further drawdowns may well continue to support the rally although having already risen significantly since the summer, I do wonder how much higher prices can go before output starts to rise again, particularly from US shale companies.

WTI Oil Futures Consolidate Around Key 57 Level After Rally Loses Steam

WTI oil futures have paused after a strong rally from 49.07 to 57.89. The market reached overbought levels on the 4-hour chart, as indicated by RSI rising above 70, and consequently, prices corrected lower and fell below the key 57.00 level.

A falling RSI is tilting immediate risk to the downside. A dip in the market would target the 23.6% Fibonacci retracement level (55.81) of the rise from 49.07 to 57.89.

If prices can remain above yesterday's low of 56.28 during the next few sessions then the risk of a deeper pullback will diminish. Staying above dynamic support provided by the 50-period moving average would help stabilize the market.

The market needs to rise above key resistance at 57.00 to push momentum back to the upside to see a re-test of 57.89 and clearing this would confirm the uptrend. A move back below the 50% Fibonacci (53.47) would end the broader uptrend.

The neutral bias is expected to hold in the near-term and prices are likely to consolidate around the key 57.00 level. Overall, the three moving averages (50, 100 and 200-period) are positively aligned and rising, which is keeping the bigger picture bullish.

Dollar Not Weak, EUR Is Strong

Overnight, European equities have shrugged off the broad-based declines in Asian stocks as better-than-expected German growth data this morning is boosting market confidence (preliminary Q3 GDP +0.8% vs. +0.6%).

In Fixed income, sovereign bond prices are under pressure as the world's most powerful central bankers gather in Frankfurt.

While in currencies, the EUR (€1.1717) remains better bid, while the pound (£1.3098) trades somewhat steady.

Currently, the markets focus of attention is on the European Central Banks (ECB) conference featuring appearances from ECB's Draghi, the Fed's Yellen, the BoE's Carney and BoJ's Kuroda.

Elsewhere, U.S inflation and retail sales numbers tomorrow are expected to influence the Fed's interest-rate hike odds, while U.S tax overhaul discussions remain ongoing.

1. Global equities struggle

Asian regional equities completed a third consecutive day of declines after China's industrial production (see below) came in lower than market expectations.

In Japan, the Nikkei share average ended little changed overnight in choppy trade, while the broader Topix slipped -0.25%.

Down-under, Australia's S&P/ASX 200 index dropped -0.9% and the Kospi index in Seoul slid -0.2%.

In Hong Kong, shares finished down after data showed the mainland economy cooled further last month.

Note: China's economy lost steam in October, with industrial output (+6.2% vs. +6.5%), fixed asset investment (+7.3% vs. +7.5%) and retail sales (+10% vs. +10.5%) missing expectations as the government extended a crackdown on debt risks and factory pollution.

The Hang Seng index fell -0.1%, while the China Enterprises Index lost -0.7%.

In China, the blue-chip index posted its worst day since mid-August on the weaker data. The CSI300 index was down -0.7%, while, the Shanghai index was down -0.52%.

In Europe, regional indices trade little changed in a relatively flat session, coming off the earlier highs as the Euro strengthens on better German GDP and ZEW (18.7 vs. 17.6) numbers.

In the U.S, stocks are set to open up in the red (-0.1%).

Indices: Stoxx600 -0.2% at 385.5, FTSE +0.1% at 7425, DAX +0.1% at 13085, CAC-40 +0.1% at 5347, IBEX-35 +0.2% at 10066, FTSE MIB +0.2% at 22487, SMI flat at 9158, S&P 500 Futures -0.1%.

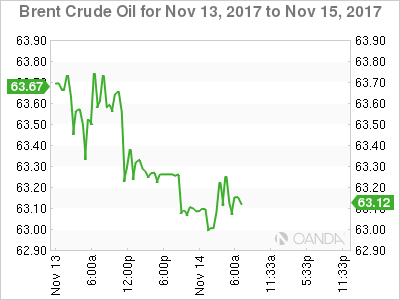

2. Oil is steady, tempered by caution over rising U.S output, gold lower

Oil prices are little changed as the prospect of further rises in U.S output is offsetting some of the optimism that OPEC led production cuts would tighten the balance between crude supply and demand.

Brent crude futures are at +$63.11 per barrel, down -5c, while U.S West Texas Intermediate (WTI) crude is down -13c at +$56.63.

Note: Both benchmarks managed to print two-year highs last week.

Recent EIA data continues to show the extent of rising U.S. oil output – it has grown by more than +14% since mid-2016 to a record +9.62m bpd. Yesterday, the U.S government said that U.S shale production in December would rise for a 12th consecutive month, increasing by +80k bpd.

Note: A cooling Chinese economy has also stoked some concerns about demand, although so far the country's refiners are processing crude oil near record levels of +11.89m bpd.

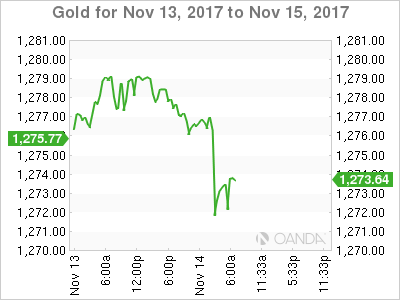

Ahead of the U.S open, gold prices have inched down, hurt by higher U.S Treasury yields amid uncertainty over the outlook for tax reforms stateside. Spot gold is down -0.1% at +$1,276.26 per ounce.

3. German yields rally on data

Eurozone bond yields have rallied across the board as strong growth in Germany has pushed the ‘single' unit higher and increased the case for tighter monetary policy.

The yield on Germany's 10-year government bond has backed up to +0.43% on this morning's German GDP print.

Note: The target for central banks is ‘inflation' – GDP growth is important, but central bank's mandate is inflation.

Elsewhere, the yield on 10-year U.S Treasuries have gained less than +1 bps to +2.41%, hitting the highest in almost three weeks with its fifth straight advance. In the U.K, the 10-year Gilt yield has climbed +1 bps to +1.339%.

4. Dollar not weak, EUR is strong

Strong German economic growth data this morning has pushed the EUR (€1.1720) to a three-week high – the economy is growing at annualized rate of more than +3%. Coupled with higher Euro bond yields would suggest the market is pricing in an end to ECB stimulus.

Elsewhere, the pound (£1.3090) remains under pressure after slightly softer than forecast inflation (see below). The currency is also pressured on concerns that PM Theresa May might be losing her grip on power.

Note: May's blueprint for the U.K's departure from the E.U faces a test starting today, when lawmakers try to win concessions on legislation to sever ties.

The dollar is up +0.2% at ¥113.88 after bouncing from ¥113.25 support levels overnight.

5. U.K inflation flat in October

Data this morning showed that annual inflation in the U.K. held steady at +3% in October, suggesting a surge in prices fueled by a steep fall in the pound (£1.3088) after last year's referendum on E.U membership may be coming to an end.

Market consensus had been expecting a pickup, to +3.1%. Data from the Office for National Statistics also show that wholesale prices grew at the slowest rate for a year.

Bank of England (BoE) had said they expected consumer price-growth to peak in October as the effect of the devaluation fades.

Nevertheless, data continues to show that U.K prices are still rising faster than wages, suggesting consumer spending will remain subdued unless wage growth picks up.

Note: Earlier this month, BoE policymakers increased borrowing costs for the first time in a decade, reversing the emergency -25 bps cut enacted shortly after Brexit.

Technical Outlook: EURGBP – Fresh Bulls Penetrate Into Daily Cloud, 0.9000+ Advance Likely N/T Scenario

The cross advances through key barrier at 0.8938 (02 Nov post-BoE rally peak) to fully retrace 0.8938/0.8791 downleg and signal extension of recovery leg from 0.8791 trough. Today's bullish acceleration penetrated into thick daily cloud (spanned between 0.8927 and 0.9026) and cracked 100SMA (0.8945), as pound was hit by weaker than expected UK data while the Euro was inflated by upbeat Italian data. Fresh bullish momentum is building on daily chart with daily MA's turning into full bullish setup which could boost the pair for advance through psychological 0.9000 barrier and test of key short-term barriers at 0.9022/32 (peaks of 20/12 Oct/daily cloud top). Close above broken cloud base is needed to confirm bullish signals while alternative scenario requires return below 30SMA (0.8890) to turn near-term focus lower.

Res: 0.8975, 0.9000, 0.9022, 0.9032

Sup: 0.8927, 0.8890, 0.8872, 0.8856

Technical Outlook: GBPJPY Eases But Still Away From Key Daily Cloud Top Support

The cross dipped on weaker than expected UK data, turning near-term focus lower after upside attempts were repeatedly capped by 10SMA.

Additional pressure comes from formation of 10/20SMA bear-cross which could result in fresh attack at daily cloud top (148.19).

The support was attacked several times but without clear break lower with last downside rejection seen yesterday, when the price spiked to 148.05 (the lowest since 20 Oct) but subsequent quick bounce signaled another downside failure.

Daily indicators are in mixed mode and so far do not give clear direction signal.

Penetration into daily cloud and violation of next pivot at 147.67 (Fibo 38.2% of 139.30/152.85 ascend) will be negative signal while sustained break above 10/20SMA's would shift near-term bias higher.

Res: 149.18, 149.50, 149.67, 150.00

Sup: 148.77, 148.14, 148.05, 147.67

CRUDE OIL Continued Consolidation

Crude oil is consolidating after the commodity set up resistance at 57.92 (08/11/2017 high). The commodity is trading at 1-year high. Expected to show further shot-term bearish consolidation. Indeed the technical structure has a history of decent consolidation phase.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Edging Lower

Silver is heading lower. Hourly support can be found at 16.60 (27/10/2017 low). Hourly resistance is given at 17.46 (13/10/2017 high). Additional support can be found at 16.13 (06/10/2017 low).

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009)

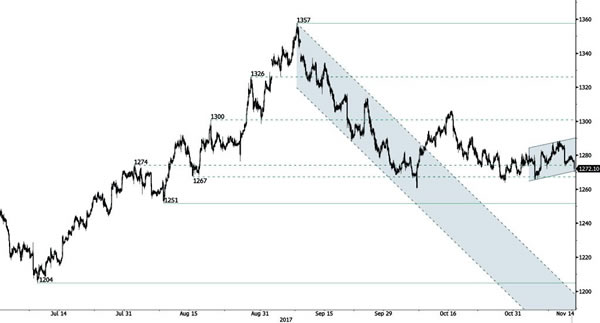

GOLD Riding Short-Term Uptrend Channel

Gold is pushing higher. The technical structure confirms the end of the consolidation phase. Support lies at a distance at 1251 (08/08/2017 high). Resistance is now located at 1288 (20/10/2017).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).