Sample Category Title

USD/JPY Analysis: Heads To North In Ascending Channel

In result of the previous trading session previously dominant descending channel ceased to exist, as the currency rate broke through its upper boundary that was additionally protected by the 100-hour SMA. As a result, now movement of the pair is guided by the four-day long ascending channel. However, that pattern might not sustain for long, as the exchange rate is approaching towards another combined resistance formed by the 200-hour SMA and the weekly PP at 113.80. Unless the buck receives a proper impulse, for instance, from the Fed Chair Yellen speech at the Central Bank Communications Conference, it is expected to fail to advance any further. On the other hand, the rapid fall might not happen as well, as the southern side is additionally backed up by a combination of the 55- and 100-hour SMAs.

XAU/USD Analysis: Forms Minor Triangle Pattern

Early hours of this trading session showed that yesterday’s attempt to return the price of gold back to the pre-fall 1,283.90 level failed. In particular, the exchange rate did not manage to bypass the monthly PP at 1,279.41 that was additionally backed up by the slipping 55- and 100-hour SMAs. In the meantime, the fact that it also failed to fall below the slope whose fourth confirmation point lies near the 1,275.80 level indicate on existence of a small ascending triangle formation. If this assumption is true, then the pair is expected to climb to the 1,279.00 mark. However, then a breakout most probably is going to occur in the opposite direction due to pressure from the above moving averages. But if traders give more weight to the larger rising wedge pattern, the pair is likely to break to the top.

EUR/USD: US Monthly Budget Statement

The EUR/USD exchange rate sustained an upward trend after the monthly report of the US budget balance was published. The Euro was little changed against the Greenback at the 1.1665 mark to remain under bullish sentiment, targeting the 1.1680 area on Tuesday morning.

The Treasury Department stated that the US Federal Government had a deficit of $63B over the course of October, where higher spending was attributed to disaster relief after a hurricane season. Steven Mnuchin, the US Treasury Secretary, projected that the tax-cut plan is likely to accelerate the US economic growth, which would raise revenue and narrow a fiscal gap. However, higher-than-anticipated deficit highlighted concerns that excess of spending over receipts could increase further.

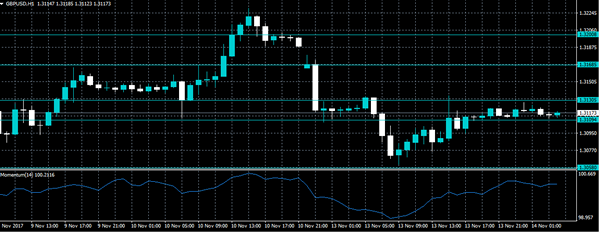

GBPUSD Is Neutral In The Short-Term With Key Support At 1.3000

GBPUSD is neutral in the short-term and trading in a range between 1.3026 and 1.3337 following a decline from 1.3656. The RSI and MACD are neutral as momentum has weakened, suggesting the consolidation phase is expected to continue in the near term.

Risk it tilted to the downside as gains have stalled in the past few days below the 50% Fibonacci retracement level (1.3215) of the latest rally from 1.2773 to 1.3656. The market is also trading below the 50-day moving average. Prices need to rise above the 38.2% Fibonacci at 1.3318 to weaken downside pressure and shift the market’s focus to the upside for a re-test of the 1.3656 high. From here the market would see a resumption of the longer-term uptrend.

Key support is at the psychological level of 1.3000. A move lower would target the 1.2773 low to retrace all of the August to September rise. Any further extension lower would shift the short-term bias from neutral to bearish.

In the bigger picture GBPUSD is slowly tracking higher and the bullish crossover of the 50 and 200-day moving averages back in May supports the trend higher. But the market needs to remain above the key 1.3000 level to keep upside momentum going.

Pound Slides As UK Parliament Votes On Brexit Bill, Aussie Bounces On Business Confidence

Ahead of a busy day in terms of economic data out of the UK, the US and the Eurozone, the pound moved lower as doubts over May’s leadership continued weighing on the currency, while markets were also cautious whether British lawmakers would approve the government’s Brexit bill. The aussie was the biggest winner of the session, gaining on business confidence despite disappointing figures out of China pressuring the currency.

With the UK Prime Minister Theresa May facing increasing political challenges following a report published by the Sunday Times newspaper and stating that forty Conservative MPs would sign a no-confidence letter on her leadership, the pound could not gain ground during the session, retreating 0.16% on the day to $1.3095. Inflation data out of the UK, though, could bring some volatility to the market later in the day, with headline inflation forecasted to break above 3.0%.

In the meantime, the UK parliament is ready to kick-off a two-day debate on the Brexit bill later on Tuesday, which will define Britain’s plan to leave the EU. However, the legislation is said to go through several stages in the upper and lower house of parliament before it turns into law. It might take lawmakers a total of eight days to make changes to the plan.

The dollar index was mostly flat around 94.50 during the session, finding support on higher US Treasury yields and on expectations of a third-rate hike in December, despite uncertainties regarding the US tax overhaul pressuring the currency. Figures on US producer prices will gather some attention later in the day.

Dollar/yen climbed by 0.22% to 113.85.

The dollar-denominated gold fell by 0.46% to $1,271.70 per ounce.

The euro approached a three-week high, touching a session-high at $1.1695 (+0.21%) after German preliminary figures on GDP growth for the third quarter beat expectations. According to the numbers, the German economy expanded by 0.8% q/q, while forecasts were for growth to stand at 0.6%. Year-on-year, GDP growth rose by 2.3% as expected, above the 1.0% (upwardly revised from 0.8%) seen in the previous quarter.

In the wake of Chinese data, the aussie made a fresh four-month low at $0.7608 after China’s industrial output slowed down to 6.2% y/y in October, compared to 6.3% expected and the 6.6% tracked in September. Chinese retail sales and spending on capital investments also missed expectations. However, an upbeat survey on Australia’s business conditions conducted by the National Australia Bank helped the aussie to recoup earlier losses and jump to $0.7621. The survey showed that the index of business conditions surged by seven points to +21 in October, reaching a record high. The index on business confidence climbed by one point to +8.

The kiwi, which is also sensitive to Chinese economic conditions, tumbled by 0.75% to $0.6851.

Dollar/loonie was on track to post its third day of gains, climbing slowly to a three-month high of 1.2749. The fifth round of NAFTA negotiations will start in Mexico City between November 17-21.

An ECB-organised policy panel in Frankfurt will gather some attention as well today as major chief central bankers, including the ECB’s Mario Draghi, the BOJ’s Haruhiko Kuroda, the Fed’s Janet Yellen and the BOE’s Mark Carney, might deliver important remarks on monetary policy.

Overblown UK Inflation Data Demand Answers | Chinese Economic Numbers Disappoints

Carney to defend overblown inflation data

Chinese economic growth stout during the last nine months

US tax reforms still have no considerable progress

Central Bankers and their view matters

Investors are cautious but steady while they await more clues on the monetary policies and digest the economic news. We had a slew of economic data out of China which was mostly on the sub-standard side. The fixed asset investment for the country during the period of January and October was dreary. It printed the reading of 7.3%, below the forecast of 7.4%. The retail sales number also missed the forecast of 10.4%, There has not been any good news in the industrial production number either as it was also below (6.2%) the forecast of 6.3%.

Overall, the Chinese economic growth has been stout during the last nine months and this has given investors assurance to continue to believe in the Chinese economic growth story. However, the activity in the property and growth sector has raised some eyebrows but the slowdown is mainly due to the government led policies which are trying to cool the property market.

Over on Wall Street, investors are still anxious about the US tax reforms because of no considerable progress, while the president continues to beat down the drums that an extraordinary progress has been made to push the new US tax laws over the line. President Trump has called for additional amendments in the tax plans which included his old slogan of repealing the Affordable Care Act, So far president Trump has accomplished nothing but bitter results whenever he talked about repealing the Affordable Care Act.

Moving away from president Trump's tweet and his Disneyland, investors are going to pay close attention to the message coming out from the head of major central bankers who would be speaking later today in Frankfurt. Janet Yellen, who will be leaving her current position as a Fed Chair would possibly be the least relevant one as her own views would have minimal weight amid investors on the dollar index. An Intriguing aspect would be if she delivers the overall view of the committee with respect to how many interest rate hikes could be on the table for the next year while the Fed continues to reduce the size of their balance sheet. Mario Draghi the president of the European Central Bank and Haruhiko Kuroda the governor of the Bank of Japan, would also be participating in the central bankers conference and their comments would be the most relevant for traders.

Back in the UK, the inflation number would require the governor of the Bank of England to defend the number to the chancellor of the Exchequer, Philip Hammond. The forecast number of 3.1% is nearly one percent above the bank's target so the governor would have to use all the justifications such as the devaluation of the currency, Brexit and other to use as an explanation of this number. However, the good news for the governor would be that inflation seems to be peaking at its current level, therefore the bank may not be required to increase the interest rate again next year.

Nonetheless, a large number of inflation components would be behind the changes in the headline annual CPI rate. We expect the food prices ranching up on the 12-month rate due to the sterling depreciation and electricity prices should also add their weight by putting upward pressure due to the increase in tariffs.

However, the overall effect from the upward pressure by food and electricity would be diluted due to the lower fuel prices. This is simply due the reason that the cost of filling the car tank at the fuelling station dropped nearly 0.4% in October of this year. The core side of inflation is likely to add more weight on the 12 month rate of inflation. If you also look at the hotel and holiday packages, they clearly seem to have ticked higher which have meaningful impact on annual inflation.

Technical Outlook: USDJPY – Bulls Pressure Pivotal 114.00 Resistance Zone

The pair extends recovery from 113.22 higher base on Tuesday and probes through 10SMA barrier at 113.80.

Bounce from 113.09 correction low so far retraced 50% of 114.73/113.09 pullback and needs sustained break above 113.90/114.10 barriers (daily Tenkan-sen / Fibo 61.8% of 114.73/113.09 downleg) to confirm reversal and expose key barrier at 114.73 (06 Nov peak).

Daily techs are bullish and favor further advance however, risk of recovery stall would remain in play if bulls fail to clear 113.90/114.10 pivots.

Rising 20SMA underpins the advance (currently at 113.63), followed by rising 30SMA (113.23) loss of which will be bearish.

Res: 113.90, 114.10, 114.45, 114.73

Sup: 113.63, 113.23, 113.09, 112.84

Technical Outlook: GBPUSD Holds Negative Tone Under Daily Cloud, UK Data In Focus

Cable is in directionless mode in early Tuesday's trading but maintaining negative bias following Monday's bearish close and awaiting UK data for fresh signals.

Rising 100SMA and Fibo 61.8% of 1.2773/1.3655 (1.3112/10) are marking immediate supports which kept the downside protected in past few sessions despite multiple spikes lower.

Overall structure is bearishly aligned with negative tone persisting while daily cloud caps (cloud base lies at 1.3214).

Plethora of MA barriers that lies in between also weighs on near-term action for clear break of 100SMA and test of key supports at 1.3038/26 (02 Nov / 06 Oct low) which mark the base of five-week congestion between 1.3026 and 1.3337.

Better than expected data today would lift pound however, sustained break above daily cloud (1.3214/1.3262) is needed to confirm bullish action.

Conversely, disappointing numbers would risk final break through 1.3038/26 pivots for continuation of broader downtrend from 1.3655 (20 Sep peak.

Res: 1.3139, 1.3165, 1.3176, 1.3214

Sup: 1.3090, 1.3061, 1.3038, 1.3026

Technical Outlook: EURUSD Advances After Strong German Q3 GDP, Data From EU In Focus

The Euro holds firm tone on Tuesday and rose to three-week high on bullish acceleration after upbeat German GDP data (Q3 GDP 0.8% vs 0.6% f/c/prev). Bullish signals were generated on advance through 20SMA (1.1674) and broken neckline (1.1685) for probes above 1.1700 handle towards 30SMA (1.1715) and 100SMA (1.1731).

Tuesday's calendar is full, with ECB President Draghi talking at 10:00GMT and a batch data from the Eurozone due at the same time.

German ZEW economic sentiment is forecasted to rise in November (20 f/c vs 17.6 in Oct), EU Q3 GDP is expected to stay unchanged at 2.5%, EU industrial production is forecasted to fall in September (-0.6% f/c vs 1.4% in Aug) while EU ZEW economic sentiment is forecasted at 29.3 in November vs 26.7 previous month.

Forecasted numbers look supportive overall and releases at/above consensus could send the single currency higher.

Lift above 100SMA target (1.1731) would open way towards 55SMA (1.1795) and daily cloud base (1.1815).

Rising hourly cloud (cloud is spanned between 1.1653 and 1.1636) and 10SMA (1.1636) continue to underpin the advance and violation of these supports would turn near-term structure negative.

Res: 1.1715, 1.1731, 1.1770, 1.1795

Sup: 1.1685, 1.1674, 1.1661, 1.1636

GBPUSD Still Bearish Below 1.3130 Level

The British pound continues to trade in a narrow range against the U.S dollar, ahead of the release of key October inflation data from the United Kingdom economy. The GBPUSD pair currently trades around the 1.3115 technical level, as traders remain cautious about the volatile CPI data. This morning's UK inflation release takes on extra importance, as the Bank of England watches inflation closely, and may decide to hike interest rates again, if inflation in the United Kingdom remains elevated.

The GBPUSD pair remains bearish while trading below the 1.3130 technical level. Worse than expected UK CPI data may see the pair fall towards the 1.3109 and 1.3058 levels. Extended support is found at 1.3038 and 1.2980.

Should UK CPI data come in better than expected later today, the GBPUSD pair will likely advance towards the 1.3168 and 1.3200 levels. Extended resistance is found at 1.3268 and 1.3320.