Sample Category Title

EURUSD Further Intraday Bullish Above 1.1655

The euro continues to advance against the U.S dollar, hitting 1.1675, as investors move away from commodity related currencies, and into euros. The EURUSD pair currently trades close to the November 3rd Non-farm payrolls high, as buyers continue to support any dip lower in the single-currency. During the European trading session, ECB President and FED Chair Jent Yellen will be speaking, we also see the releases of key inflation data from Germany and the United States economies, which promises to set the tone for the trading day.

The EURUSD pair remains further intraday bullish while trading above the 1.1655 technical level. Further upside towards the 1.1684 and 1.1710 level seems increasingly likely.

Should the EURUSD pair decline below the 1.1655 level, sellers will likely push-price-action towards the 1.1632 and 1.1610 support levels.

Data-Driven Tuesday To Sway Investor Sentiment

After a slow start to the week, economic data are back in focus, with reports from both sides of the Atlantic scheduled to make headlines.

The action picks up at 07:00 GMT with a report on German consumer prices. Germany’s CPI index is forecast to rise 1.6% annually in October. The so-called Harmonized Index of Consumer Prices is expected to come in at 1.5%.

The German government will also release a preliminary report on third quarter GDP. Europe’s largest economy is projected to rise 0.6% in the third quarter, which translates into a year-over-year gain of 2.3%.

The Spanish government is also expected to produce the latest inflation figures on Tuesday. Later in the day, the Swiss will unveil their latest report on factory-gate prices. Italy and Portugal are also expected to release their latest GDP figures.

The United Kingdom will see a heavy release schedule on Tuesday, including reports on consumer inflation, retail prices and the producer price index (PPI).

Eurozone data will also make headlines at 10:00 GMT with reports on gross domestic product, industrial production and institutional investor sentiment.

In North America, the US Labor Department will issue its latest report on producer inflation. The producer price index (PPI) is expected to climb 2.4% annually in October, following a gain of 2.6% the previous month.

On the monetary policy front, Bank of England Governor Mark Carney is scheduled to deliver a speech at 10:00 GMT. In the United States, St. Louis Federal Reserve President James Bullard will deliver remarks at 13:15 GMT. Fifteen minutes later, European Central Bank (ECB) official Benoit Coeure is also scheduled to deliver a speech.

Earlier in the day, the Chinese government reported slower than expected growth across retail sales, industrial production and urban investment. Retail sales rose 10% annually in October; industrial production climbed 6.2% and urban investment added 7.3%.

EUR/USD

The euro advanced sharply at the start of the week, with the EUR/USD approaching 1.1700 for the first time since late October. The pair faces immediate resistance at 1.1690, a region of prime selling interest. On the opposite side of the ledger, immediate support is located at 1.1620.

GBP/USD

Cable recovered some lost ground on Monday after briefly falling below 1.3100. The GBP/USD exchange rate was last seen trading at 1.3117. Immediate support for cable is located at 1.3061, which represents Monday’s bottom price. On the flipside, resistance is located at 1.3140.

USD/CAD

The US dollar gained ground against its northern rival on Monday, with the USD/CAD racing back toward 1.2740. This pair is expected to see much more volatility later in the week as market participants weigh the latest batches of US economic data.

Can Euro Retain Gains Vs British Pound?

Key Highlights

- The Euro made a nice upside move from the 0.8810-0.8800 area against the British Pound.

- There was a break above a major bearish trend line with resistance at 0.8855 on the 4-hours chart of EUR/GBP.

- The Germany's wholesale price Index in Oct 2017 posted no change, whereas the forecast was +0.4% (MoM).

- Today in the UK, the CPI for Oct 2017 will be released which is forecasted to increase by 3.1% (YoY).

EURGBP Technical Analysis

The Euro after declining towards 0.8800 against the British Pound found support. The EUR/GBP pair traded higher recently and broke an important resistance near 0.8865.

During the upside move, there was a break above a major bearish trend line with resistance at 0.8855 on the 4-hours chart. The pair also settled above 0.8850, the 200 simple moving average (green, 4-hour) and the 100 SMA (red, 4-hour).

The current price action is positive with a close above the 50% Fib retracement level of the last decline from the 0.8937 high to 0.8791 low. On the upside, the next major hurdle for buyers is near 0.8950, followed by another bearish trend line at 0.8970. On the downside, supports are at 0.8865 and 0.8850.

Germany's Wholesale Price Index

Recently in the Euro Zone, the Germany's wholesale price Index for Oct 2017 was released by the Statistisches Bundesamt Deutschland. The forecast was slated for an increase of 0.4% in the WPI in Oct 2017 compared with the previous month.

However, the actual result was disappointing, as there no change in the index. The yearly change in the WPI was +3%, which was less than the last +3.4%. For the complete list and details, please visit this link.

Overall, the EUR/GBP pair is showing a lot of positive signs, but it might struggle to break the 0.8950 and 0.8970 levels in the near term.

Economic Releases to Watch Today

German Consumer Price Index for Oct 2017 (YoY) – Forecast +1.6%, versus +1.6% previous.

German Consumer Price Index for Oct 2017 (MoM) – Forecast 0%, versus 0% previous.

German ZEW Business Economic Sentiment Index for Nov 2017 – Forecast 20, versus 17.6 previous.

UK Retail Price Index Oct 2017 (YoY) – Forecast +4.1%, versus +3.9% previous.

UK Producer Price Index Oct 2017 (YoY) – Forecast +2.9%, versus +3.3% previous.

UK Producer Price Index Oct 2017 (MoM) – Forecast +0.3%, versus +0.2% previous.

UK Consumer Price Index Oct 2017 (YoY) – Forecast +3.1%, versus +3.0% previous.

UK Core Consumer Price Index Oct 2017 (YoY) – Forecast +2.8%, versus +2.7% previous.

Euro Zone Gross Domestic Product Q3 2017 (QoQ, Prelim) – Forecast 0.6%, versus 0.6% previous.

Euro Zone Gross Domestic Product Q3 2017 (YoY, Prelim) – Forecast 2.5%, versus 2.5% previous.

US Producer Price Index Oct 2017 (MoM) – Forecast +0.1%, versus +0.4% previous.

US Producer Price Index Oct 2017 (YoY) – Forecast +2.4%, versus +2.6% previous.

Forex: Chinese Data Disappoints

China's economy has been robust throughout 2017 as a continued recovery in manufacturing and industrial sectors, a healthy property market and surprisingly strong exports have helped push growth in the first three quarters close to 6.9%. However, data on Tuesday from the Chinese National Bureau of Statistics showing fixed-asset investment growth declined to 7.3%, through January to October, below forecasts of a 7.4% growth. Further disappointing data showed year-on-year industrial output coming in at 6.2% in October and significantly lower than September's strong release of 6.6%. Many believe this contraction in growth is likely to continue in the coming months, albeit at a very moderate pace, as China looks to limit the risk of debt, which slows demand, and its push to improve pollution that has negatively impacted factory output. Consumer data is also showing signs of waning as Retail Sales (YoY) for October came in at 10%, missing forecasts of 10.4% and below the previous months reading of 10.3%. With President Xi Jinping stating that 'China will focus on quality over speed as it pursues economic growth' and restating the need to improve pollution and reduce riskier lending, it is likely that China will struggle to move towards a more domestic demand driven economy.

The markets are now focused on today's gathering of several central bankers in Frankfurt, Germany, who are taking part in an ECB organized event. The central bankers, including the Fed's Janet Yellen, the BoE's Mark Carney, the ECB's Mario Draghi and the BoJ's Haruhiko Kuroda, will participate in a panel titled: 'At the heart of policy: challenges and opportunities of central bank communication'. Needless to say, the markets will be keenly listening to any hints on future monetary policy that could cause market volatility.

EURUSD is slightly higher in early Tuesday trading at around 1.1672.

USDJPY is little changed, trading at around 113.65.

GBPUSD is unchanged overnight, currently trading around 1.3115.

Gold is 0.15% lower in the early trading session at around $1,276.50.

WTI is 0.15% lower in early Tuesday trading at around $56.82.

Major data releases for today:

At 07:00 GMT, the Statistical Office of the European Union, Destatis, will release the Harmonized Index of Consumer Prices (YoY) for October. The statistical methodology results in an index of Consumer Prices correlated across all EU member states to define and assess price stability. Consensus is calling for an unchanged reading of 1.5% – any significant deviation from the forecast could see EUR volatility.

At 08:05 GMT, the CEO of the Federal Reserve Bank of Chicago and current FOMC member Charles Evans is scheduled to speak at the European Central Bank Conference in Frankfurt, Germany on the topic of 'Communications Challenges for Policy Effectiveness, Accountability and Reputation'.

At 9:00 GMT, Sabine Lautenschläger, a member of the European Central Bank's Executive Board, is scheduled to speak at the opening discussion at the Banking Supervision, Resolution and Risk Management Conference during 20th Euro Finance Week in Frankfurt, Germany.

At 9:30 GMT, UK National Statistics will release Consumer Price Index (YoY) for October. Consensus is calling for a slightly higher release of 3.1% from the previous 3.0%. The Bank of England had suggested that inflation in the UK will peak in 2018 at near to 3.5% before retracing lower. If this release of CPI is significantly higher than expected, we may see a change in monetary policy from the BoE that will result in higher interest rates. Be aware that any deviation from forecast is likely to result in GBP volatility.

At 10:00 GMT, ECB President Mario Draghi, Fed Chair Janet Yellen, Bank of England Governor Mark Carney and Bank of Japan Governor Haruhiko Kuroda are scheduled to participate in a policy panel: 'At the heart of policy: challenges and opportunities of central bank communication' at the conference 'Communication challenges for policy effectiveness, accountability and reputation' organized by the ECB in Frankfurt, Germany.

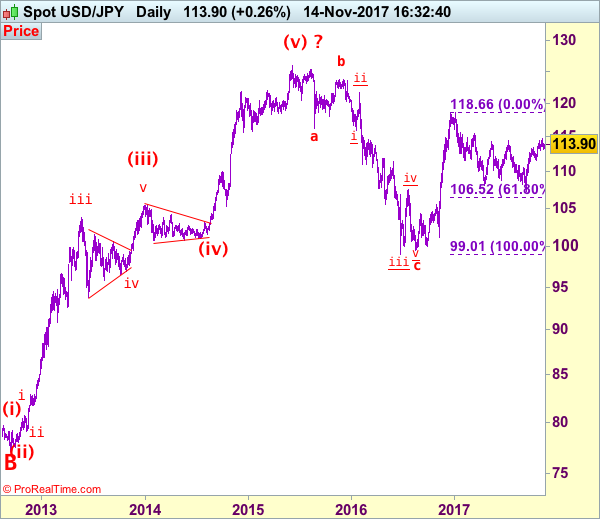

USD/JPY Elliott Wave Analysis

USD/JPY - 113.86

USD/JPY – Wave V of larger degree circle V has possibly ended at 75.31 and major correction has commenced and already met indicated target at 125.00.

As the greenback has retreated after rising briefly to 114.74 early last week, suggesting consolidation below this level would be seen and pullback to 113.00-10 cannot be ruled out, however, reckon downside would be limited to 112.50-60 and bring another rise later, above said resistance at 114.74 would extend recent upmove to 115.00, break there would signal the correction from 118.66 top has ended earlier at 107.32 and the rise from there may bring further gain to previous resistance at 115.51. Looking ahead, a sustained breach above this level at 115.51 would retain bullishness, then subsequent gain to 116.00-10 and possibly 116.50-60 would follow.

Our preferred count is that, triangle wave IV (with circle) ended at 101.45 and the circle wave V brought dollar down to the record low of 75.31 in 2011 and the subsequent rebound signal major correction has commenced with A leg ended at 84.19, followed by wave B at 77.14 and impulsive wave C is now unfolding (indicated upside target at 125.00 had been met) for gain towards 127.00 level. In the event dollar drops below support at 99.01, this would confirm medium term decline from 125.86 top (2015 high) has resumed for subsequent weakness to 98.00 and possibly 97.00.

Under this count, this wave C is unfolding as impulsive waves with (1) (2), 1 2 ended at 80.67, 79.07, 82.84 and 81.69 respectively, hence the extended wave 3 has ended at 103.74 and wave 4 correction of recent upmove should bring weakness to 92.57, then towards 90.88 but psychological support at 90.00 should limit downside and bring another rally later in wave 5, indicated target at 125.00 had been met and gain to 127.00 cannot be ruled out but reckon price would falter below 130.00.

On the downside, whilst initial pullback to 113.00-10 cannot be ruled out, reckon downside would be limited to 112.50-60 and 112.00 would contain downside, renewed buying interest should emerge above support at 111.65 and bring another rise later. Only a drop below said support at 111.65 would suggest a temporary top is formed instead, bring weakness to 111.00 but downside should be limited to 110.40-50 and support at 109.55 should remain intact. A breach of strong support at 109.55 would abort and suggest the rebound from 107.32 has ended instead, risk weakness to 109.00 and possibly 108.50-60 but price should stay well above said support at 107.32 and bring another rebound later.

Recommendation: Buy at 112.50 for 114.50 with stop below 111.50.

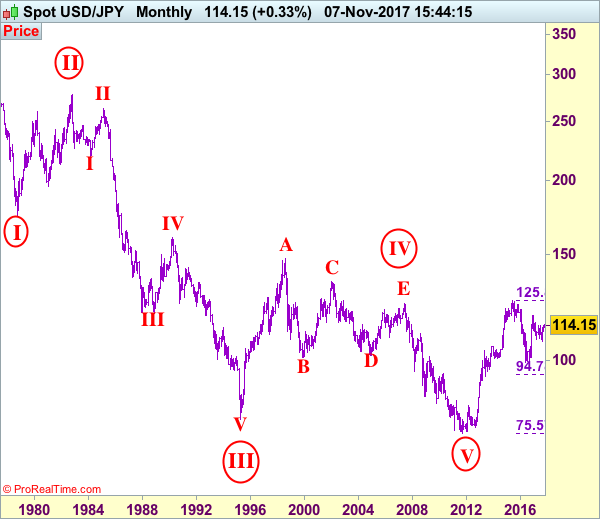

On the monthly chart, we have changed our preferred count that an impulsive wave is unfolding with major wave III with circle ended at 79.75, then followed by wave IV with circle and is labeled as a triangle with A: 147.64 (11 August, 1998), B: 101.25, C: 135.20, D: 101.67 and E leg ended at 124.14 to end the wave IV with circle. Hence, wave V with circle commenced from there and hit a record low of 75.31, however, the subsequent strong rebound signals this circle wave V has possibly ended there, hence gain to (indicated upside target at 122.00 and 125.00 had been met), the retreat from 125.86 suggests wave A of major correction has ended there and wave B correction back to 99.00, then 95.00 would be seen, however, reckon downside would be limited to 90.00, bring another rebound in wave C next year.

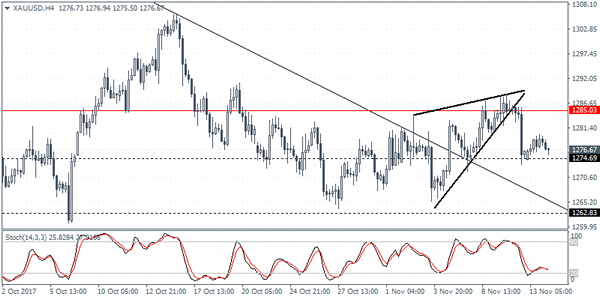

XAUUSD Intraday Analysis

XAUUSD (1276.67): Gold prices posted a modest bounce off the initial test of support near 1274.70. However, the bounce was short lived as price action was seen falling back to this level. We expect that further downside is possible on a breakdown below the 1274.70 support. This will push gold prices lower towards the 1270.00 handle. Alternately, in the event that the support level holds out, gold prices could remain trading sideways. Further direction could be established on a breakout above 1285.00 to the upside and below 1274.70 support.

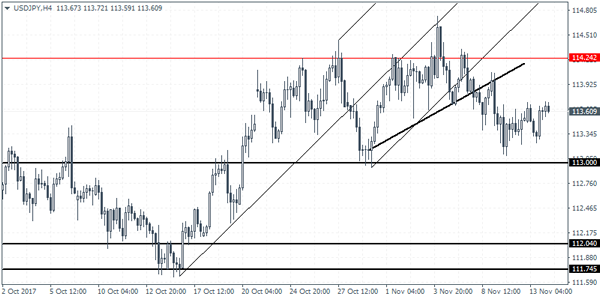

USDJPY Intraday Analysis

USDJPY (113.60): The USDJPY continues to remain trading flat with price action seen hovering near the breakout level from the rising wedge pattern formed on the daily chart. With price failing to break out from the resistance level near 114.31 - 114.07 we expect the consolidation to continue near this level. Support is seen at 113.00 which could be tested in the near term. The BoJ Governor Kuroda is expected to speak today followed by the quarterly GDP numbers coming out from Japan. These events could potentially bring some volatility to the currency pair and help establish a short-term direction in the currency pair.

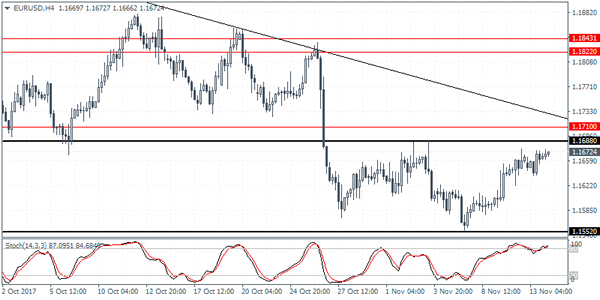

EURUSD Intraday Analysis

EURUSD (1.1672): The EURUSD has been inching higher gradually over the past four sessions. Price action remains steady near the main resistance level of 1.1672 region. The rally back to this level invalidates the bearish flag pattern. The bounce off the support level near 1.1552 suggests that EURUSD could remain caught in the range. However, a breakout above 1.1688 could suggest a retracement in price with further gains expected above this level. To the downside, the risks are limited unless EURUSD manages to breach past the previous support level that has been established.

UK Inflation Expected To Accelerate

The markets were seen trading a bit subdued in yesterday's session. The US dollar managed to hold its ground amid a quiet trading day. Oil prices were seen trading mixed as OPEC reported that crude oil supply declined 0.46% during the month of October. The report showed that demand for oil could increase in 2017 and 2018. However, oil prices were little changed towards the end of the day.

Looking ahead, the UK's monthly inflation figures will be published today. According to the median estimates, headline inflation rate is expected to surpass the 3% rise seen last month to 3.2% while core inflation rate is also expected to have increased 2.9%.

Among the central bank speeches lined up today, the ECB President Mario Draghi, BoE's Carney and BoJ's Kuroda are expected to speak over the day culminating with the speech from the Fed chair Janet Yellen.

If Bonds Are Right, A Steep Equity Correction Is Underway

2017 has seen many hedge fund and portfolio managers send warning signals that an equity market correction is overdue. Overstretched valuations, tighter monetary policies, geopolitical risks, a slowdown and high debt levels in China and low inflation, are some of the factors that could potentially trigger a market correction. However, all of these warnings are being ignored, and stocks continue to score new highs.

'Buy the dip' mentality has been in play throughout the year, especially because many investors don't want to miss the opportunity of a potential rally when the U.S. lowers the corporate tax rate, however the sharp differences between the House and the Senate suggest there are still many barriers to overcome.

When investors start feeling nervous, volatility tends to spike and a shift is realized from high-risk assets to safer investments. The CBOE's Volatility Index (VIX) although having appreciated 25% the past six trading days, it is still trading at 11 which isn't a sign of serious nervousness. The S&P also declined in the past week but it is still 0.5% away from its record high; this is another indicator that investors are not worried. However, bond markets are sending a totally different signal.

Junk bonds or high yield bonds are a proxy to risk, and the correlation between junk bonds and equities tends to be too close. ETF's such as iShares iBoxx High Yield Corporate Bond and SPDR Bloomberg Barclays High Yield Bond, have both fallen to an eight-month low; meanwhile equity investors remain complacent. With divergence now apparent, the question to be asked is who's right? The bonds or equities markets?

Emerging bond markets are also providing similar signals, diverging from equity performance, and I am certain that such a negative correlation may not last for long. Even the U.S. Treasury yield curve has flattened the most since 2007. The spread between U.S. 2-year note yields and 10-year notes declined to 67 basis points last week. No doubt expectations of tighter U.S. monetary policy, ECB's bond-buying program, debt issuance and supply and demand, were all factors that influenced the shape of the U.S. yield curve, but the longer this trend continues, the more worried investors should become. A flattening yield curve is an early sign of a recession or at least an economic slowdown - that shouldn't be ignored. If the yield curve inverted, then bond markets will be screaming 'SELL'.