Sample Category Title

Trade Idea: GBP/USD – Hold short entered at 1.3170

GBP/USD – 1.3101

Original strategy :

Sold at 1.3170, Target: 1.3000, stop: 1.3230

Position: - Short at 1.3170

Target: - 1.3000

Stop: - 1.3230

New strategy :

Hold short entered at 1.3170, Target: 1.3000, stop: 1.3190

Position: - Short at 1.3170

Target: - 1.3000

Stop:- 1.3190

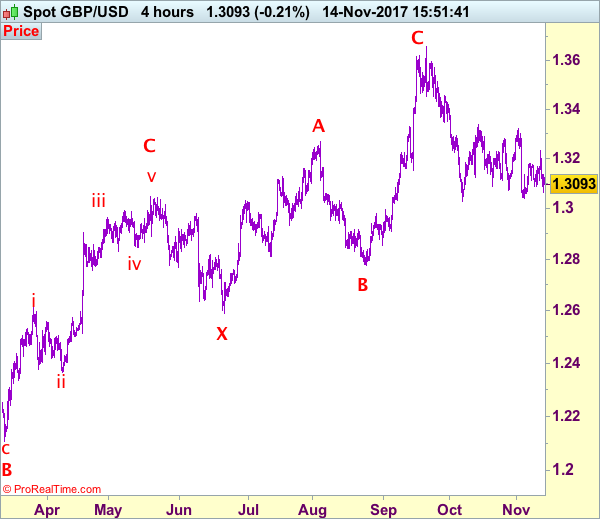

As indicated resistance at 1.3230 did cap cable’s upside and the pair has retreated again, retaining our bearishness for the fall from 1.3658 top to resume after consolidation, below 1.3062 support would extend weakness to 1.3039, however, break of previous support at 1.3027 is needed to confirm the aforesaid decline from 1.3658 top has resumed for weakness to psychological support at 1.3000, break there would encourage for subsequent decline towards 1.2950-60.

In view of this, we are holding on to our short position entered at 1.3170. Only above said resistance at 1.3230 would defer and prolong choppy consolidation, risk rebound to 1.3250-60 but resistance at 1.3299 should limit upside and price should falter below last week’s high at 1.3321, bring another retreat later. Our preferred count is that (pls see the attached chart) the wave IV is unfolding as a complex double three (ABC-X-ABC) correction with 2nd wave B ended at 1.2774, hence 2nd wave C could have ended at 1.3658.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

Currencies: Euro Holds The Lead As Risk Rally Slows

Sunrise Market Commentary

- Rates: Bearish sentiment on bond market remains in place

Today's eco calendar heats up, but (US) eco data might be overshadowed by tomorrow's CPI and retail sales. A speech by Atlanta Fed Bostic will be closely monitored. He's relatively new on the Fed, but votes on policy next year. If he indicates willingness to hike rate 3 times next year, we might get more repositioning (bear flattening US yield curve). - Currencies: Euro holds the lead as risk rally slows

USD/JPY again held up well yesterday even as risk sentiment turned less buoyant. EUR/USD kept a cautious upward bias. Today's eco calendar heats up. Especially US PPI might move the dollar, but the focus remains on tomorrow's US CPI and retail sales. Sterling traders will keep a close eye at UK CPI and at the debate on the Brexit withdrawal bill

The Sunrise Headlines

- US stock markets closed with small gains after a weak opening. Overnight, Asian stock markets trade mixed with Japan slightly outperforming this time.

- Theresa May bowed to pressure from pro-European Conservatives by offering the British parliament a full vote on a final divorce deal, the latest sign of how political turmoil within her government is taking a toll on her Brexit plans.

- China's economy cooled further last month, with industrial output, fixed asset investment and retail sales missing expectations as the government extended a crackdown on debt risks and factory pollution.

- Venezuela was declared in default by S&P Global Ratings after missing two interest payments on its debt. The nation owed investors about $200 million and failed to pay by the end of a 30-day grace period.

- Treasury Secretary Mnuchin said the Trump administration wouldn't support tax legislation with a corporate tax rate of more than 20% as part of any future compromise between the House and the Senate.

- The number of banks deemed systemically important and subjected to extra regulation in the US would drop by two-thirds under plans to roll back Obama-era reforms (Dodd-Frank) that have attracted bipartisan support.

- Today's eco calendar heats up with UK inflation data , EMU Q3 GDP, EMU industrial production, German ZEW investor sentiment and US NFIB small business sentiment and US PPI. Several central bankers speak including ECB Draghi, Fed Yellen, BoE Carney and BoJ Kuroda in Frankfurt

Currencies: Euro Holds The Lead As Risk Rally Slows

Dollar holds tight ranges ahead of key US data

Yesterday, EUR/USD and USD/JPY trading was similar to what happened at the end of last week. Core yields hardly declined in European risk aversion. EUR/USD traded with a slightly positive bias intraday. High core yields prevented any substantial losses in USD/JPY. Risk sentiment improved in US dealings. It supported USD/JPY, but the dollar remained in the defensive against the euro. EUR/USD finished the day little changed at 1.1667. USD/JPY closed the session off the intraday lows at 113.62.

Asian equities are mostly trading in negative territory. Japan this time is the exception to the rule. Chinese retail sales and production data were a touch softer than expected. USD/JPY is holding in the 113.60 area after yesterday's intraday rebound, but the pair is still locked in tight ranges. Changes in EUR/USD (1.1675) also remain small, but the pair nears 1.1690 resistance.

German ZEW investor sentiment and the details/composition of the EMU Q3 GDP will be published today. We don't expect a big impact on the euro. US PPI is expected to rise 0.1% M/M and 2.5% Y/Y after a bigger rise last month (0.4% M/M and 2.6% Y/Y). The focus remains on tomorrow's US CPI and retail sales, but interest rates and the dollar might react to the PPI's, especially in case of a negative surprise. There were will be many headlines from the ECB conference on Central Bank communication, attended by ECB president Draghi, Fed Chair Yellen, BoE governor Carney and BoJ governor Kuroda. The meeting might yield interesting ‘theoretical' insights, but we don't expect CB heads to address actual monetary policy. The US tax bill also remains a wildcard for global trading. Basically, we expect more technical, sentiment-driven trading. A soft US PPI or a more pronounced risk-off sentiment might tilt the balance slightly against the dollar. Tomorrow's US retail sales and CPI have most potential to move interest rates and FX markets this week. We started the week with a cautious bias on the dollar as the US currency recently was more vulnerable to negative news than the euro. We maintain that USD caution. That said, we don't expect any USD setback to go very far though.

From a technical point of view, EUR/USD dropped below 1.1670/62 support, but subsequent follow-through price action occurred very slowly. The pair dropped to a new post-ECB low on Tuesday last week. A sustained break would confirm that the recent EUR/USD uptrend is broken. EUR/USD 1.1423 (38% retracement of 2017 rise) is the next downside target on the charts. A return north of 1.1690, would question recent downside momentum. Next resistance stands at 1.1837/80. USD/JPY's momentum was positive in past months. The pair regained 110.67/95 resistance and tested the 114.49 MT range top. The attempt failed. A sustained break would improve the technical picture. We remain cautious to preposition for further USD/JPY gains. Last week's price action was unconvincing despite a solid interest rate support.

EUR/USD: rebound off recent low. 1.1690 resistance under test ahead of key US eco data

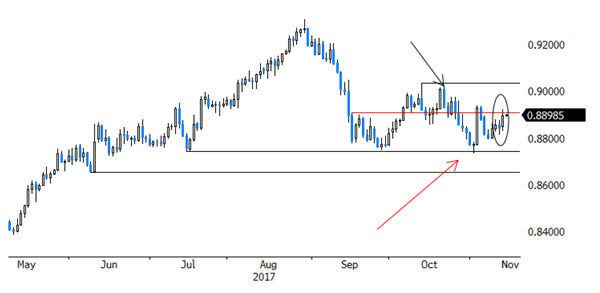

EUR/GBP

UK CPI to rise north of 3%?

Sterling came again under pressure yesterday as press articles indicated that a growing number of Conservative MP's wants a vote on PM's May leadership, illustrating the deep division within the Conservative party. Several sterling selling waves pushed EUR/GBP to the 0.8920 area. Cable dropped to the 1.3062 area, but the ST range bottom (1.3040/27) was left intact. Later, UK Brexit minister Davis said that Parliament will have a final say on a Brexit deal. The pressure on sterling eased slightly. EUR/GBP finished the session at 0.8896 (from 0.8841).

The October UK price data will be published today. Headline CPI is expected at 0.2% M/M and 3.1% Y/Y. A rise above 3% was anticipated by the BoE. The BoE expects it to be temporary as price rises due to sterling's decline will gradually ease. If inflation prints above 3%, Governor Carney has to write an explanation to the Chancellor of the Exchequer. Carney will probably argue that the peak in inflation is (almost) reached. Sterling might be slightly supported if Carney stresses that some modest further tightening is still possible. Markets will also keep a close eye at the debate on the ‘EU Withdrawal Bill' in Parliament. This debate will probably create plenty of political noise. Fortunes for sterling probably won't improve as long as political uncertainty stays as high as it is now.

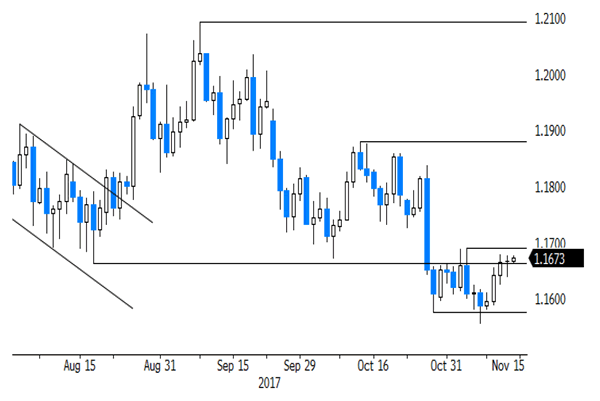

MT technical: Sterling rebounded in September as the BoE prepared markets for a rate hike. This rebound ran into resistance as markets anticipated that any rate hikes would be very gradual and limited. This view was confirmed at this month's BoE policy meeting. EUR/GBP currently trades in a 0.8733/0.9033 consolidation range. A downside test of this range was rejected. We assume that the 0.8733-0.8652 support will be tough to break. A EUR/GBP buy-on-dips approach for return action to the EUR/GBP 0.9023/33 ST range top is favoured

EUR/GBP: CPI and Brexit bill to guide GBP trading today

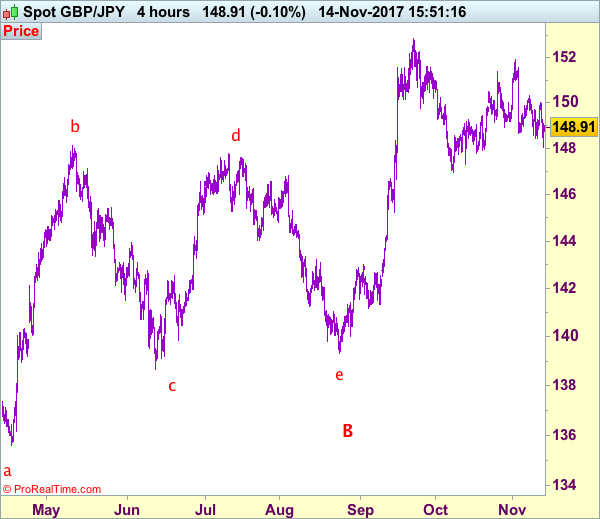

Trade Idea: GBP/JPY – Target met and stand aside

GBP/JPY - 148.90

Original strategy:

Sold at 150.20, met target at 148.20

Position: - Short at 150.20

Target: - 148.20

Stop: -

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Although sterling did resume recent fall from 151.90 top and indicated downside target at 148.20 was met, lack of follow through selling and current rebound from 148.05 suggest consolidation would be seen and corrective bounce to 149.50 cannot be ruled out, however, reckon 150.00 would limit upside and price should falter below resistance at 150.30, bring another decline later this week.

As we have taken profit on our short position entered at 150.20, would not chase this fall here and would be prudent to stand aside for now. Below said support at 148.05 would extend the aforesaid erratic fall from 151.90 top to previous support at 147.80 but oversold condition should limit downside and support at 147.30 should remain intact.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

Comparing the House and Senate Tax Plans

Executive Summary

Last week marked a key milestone in Congressional Republicans' efforts to pass a tax overhaul plan in advance of next year's midterm elections. The House Ways and Means Committee passed its version of a tax package, which we expect to pass a full House vote. In the other chamber, the Senate Finance Committee released the details of its tax plan, which differed in several key ways from the House package. The Senate plan is still more fluid and is likely to change as it winds its way through the mark-up process this week. In this report, we summarize the key differences between the House and Senate tax packages and discuss some of the key policy sticking points that we foresee as the major challenges to the completion of a final tax package.

We remain comfortable with our call for passage of a tax package in the first quarter of next year, with the cuts retroactive to January 2018. Our view is that the final package will need to be smaller and less permanent than what is currently being proposed in order to 1) comply with Senate rules for passage through budget reconciliation and 2) be politically viable in both the House of Representatives and the Senate, where the priorities and political incentives are somewhat different.

Comparing the House and Senate Tax Plans

For a full summary table comparing the House and Senate tax plans see Appendix A.

Individual Side of the Tax Code

Tax Brackets

House: Collapses the current seven brackets into four brackets of 12, 25, 35 and 39.6 percent. The marginal rate on the top bracket is left unchanged and would kick in at income in excess of $500,000 for single filers and $1,000,000 for married filers, up from $418,400 and $470,700 currently. The tax brackets (and other inflation-adjusted tax parameters) would be indexed for inflation using chained CPI rather than CPI-U.

Senate: Leaves the number of tax brackets at seven but modifies the rates and income thresholds. The marginal rate on the top bracket is reduced to 38.5 percent and would kick in at income in excess of $500,000 for single filers and $1,000,000 for married filers. The tax brackets (and other inflation-adjusted tax parameters) would be indexed for inflation using chained CPI rather than CPI-U.

Standard Deduction

House: Nearly doubles the standard deduction for single and married filers.

Senate: Same as House plan.

Personal Exemption

House: Eliminates the personal exemption.

Senate: Same as House plan.

Alternative Minimum Tax

House: Eliminates the Alternative Minimum Tax (AMT).

Senate: Same as House plan.

Estate Tax

House: Doubles the estate tax exemption to $10.98 million, indexed to inflation, then permanently repeals the estate tax in 2024.

Senate: Preserves the estate tax and doubles the exemption to $10.98 million, indexed to inflation. Keeping the estate tax on a permanent basis is likely to be a point of contention for the most conservative House and Senate members, who have long championed eliminating the estate tax.

Retirement Plans

House: No major changes.

Senate: Eliminates catch-up contributions for high-wage (>$500,000) workers 50 and over and consolidates contribution limits for 457(b)s to match 401(k)s and 403(b)s. These are much smaller changes than initially considered in the House, but they do represent another potential politically sensitive topic for policymakers.

Child/Family Tax Credits

House: Increases child tax credit to $1,600 from $1,000 and increases income threshold for phase-out. Creates a new $300 per-person family tax credit for other non-child dependents. This new credit expires after 2022. The temporary nature of this tax credit could be a possible point of contention. Sun setting this provision helps save money from a budget score perspective, but it has raised questions from some about how this will effect families' tax bills down the road. Given how politically popular a family tax credit could prove to be, policymakers are likely banking that the credit would be extended past 2022 when the time eventually comes.

Senate: Increases child tax credit to $1,650 and increases income threshold for phase-out to a greater extent than the House plan. Creates a $500 nonrefundable credit for qualifying dependents other than children.

Itemized Deductions

House: Eliminates the deduction for state & local income/sales taxes, but retains the state & local property tax deduction with a cap of $10,000. Caps mortgage interest deduction at $500,000 of debt (down from $1 million under current law), eliminates the interest deduction for second homes and home equity debt. Eliminates the medical expense deduction.

Senate: Fully repeals the state & local deduction for both income and property taxes. Repeals the deduction for interest on home equity debt but otherwise leaves mortgage interest deduction unchanged. Retains the medical expense deduction. Broadly speaking, the Senate plan takes a less aggressive approach to eliminating deductions in the individual side of the tax code, but helps make up some of the lost revenue through a full repeal of the state & local deduction. The more aggressive state & local deduction approach is likely to cause problems in the House, where Republican members from high-tax, high cost-of-living areas have raised concerns over full elimination.

Pass-Through Income

House: Creates a 25 percent rate for income derived from pass-through entities, which under current law is taxed through individual income tax brackets. To try and prevent abuse of the system, the plan proposes treating 70 percent of income as wage income (subject to the individual tax brackets) and 30 percent as business income (subject to the 25 percent rate). Some "specific service activities," such as income derived from financial services, law, engineering and other similar fields, are excluded from the special pass-through rate to create additional anti-abuse guardrails.

Senate: Allows a deduction of 17.4 percent of qualified business income from their total income. Also excludes some "specific service activities" from taking advantage of this provision for antiabuse reasons. Policymakers have been vexed by the competing desires to provide a tax cut for small businesses who file through the individual income tax system while also preventing people from gaming the system and passing off wage income as pass-through income. The House and Senate each take much different approaches that will need to be reconciled before final passage.

Corporate Side of the Tax Code

Corporate Tax Brackets

House: Reduces the current 35 percent top statutory rate down to 20 percent with an effective date of January 1, 2018.

Senate: Reduces the current 35 percent top statutory rate down to 20 percent like the House plan but delays the implementation until January 1, 2019 in order to save room under the revenue reduction cap of $1.5 trillion over 10 years. The one year delay of the corporate tax rate reduction is a possible point of contention not just with the House of Representatives but also with the White House. The reduction of the corporate rate to 20 percent creates the biggest decrease in revenues in the House and Senate plans, reducing revenues by $1.46 trillion and $1.33 trillion, respectively, over 10 years on a static basis according to the Joint Committee on Taxation.

Capital Investment

House: Allows for full expensing of certain capital investment for 5 years.

Senate: Same as House plan.

Tax Treatment of Interest

House: Limits net interest expense deductibility to 30 percent of earnings before interest, taxes, depreciation, and amortization (EBITDA).

Senate: Limits net interest expense to 30 percent of earnings before interest and taxes (EBIT).

Net Operating Loss Provisions

House: Eliminates net operating loss (NOL) carryback while allowing for net operating loss carryforwards (adjusted for inflation and the real return to capital) but restricts the deduction to 90 percent of current year taxable income.

Senate: Eliminates net operating loss (NOL) carryback but restricts the deduction to 90 percent of current year taxable income. The senate version does not make an adjustment for inflation and the real return to capital.

Business Credits and Deductions

House: Eliminates many tax credits including those for orphan drugs, energy, private activity bonds, real estate rehabilitation, and contributions for capital.

Senate: Makes adjustments to the real estate rehabilitation credit and the orphan drug credit while retaining certain other credits eliminated in the House version.

Alternative Minimum Tax

House: Eliminates the corporate AMT.

Senate: Same as House plan.

International Income

House: Establishes a territorial tax system in which foreign-source dividends and profits of U.S. companies are not subject to U.S. tax upon repatriation. However, 50 percent of excess returns (those greater than a routine return, defined as the applicable federal rate plus 7 percent) earned by controlled foreign corporations (CFCs) are included in U.S. shareholders' gross income.

Senate: Moves to a territorial system with a minimum tax of the excess of 10 percent of modified taxable income over an amount equal to the firm's regular tax liability.

Deemed Repatriation

House: Enacts a deemed repatriation of deferred foreign profits at a rate of 14 percent for cash and cash-equivalent profits and 7 percent for reinvested foreign earnings over a period of eight years.

Senate: Enacts a deemed repatriation of deferred foreign profits at a rate of 10 percent for cash and cash-equivalent profits and 5 percent for reinvested foreign earnings over a period of eight years.

Legislative Outlook: A Long Road Ahead

What are the next steps in getting a tax package passed through Congress and sent to the President's desk for signature? The next couple of weeks will be dominated by the House trying to pass its package via a full floor vote while the Senate Finance Committee marks up its package to garner enough votes for passage through both the committee process and a full Senate floor vote. While it is likely that the House will pass their package rather quickly, we are skeptical that the Senate will move as quickly. As was on display during the Senate Republican efforts to repeal and replace the Affordable Care Act, the legislative progress in the Senate is much more challenging due to a combination of ideological differences and a very tight vote margin for legislation passing with only Republican votes.

Complicating the process in the Senate is an impending deadline to fund the government beyond December 8. Senate leadership has indicated that they may delay a planned recess for the week of November 20 in order to pass their tax package. That plan, however, assumes that the Senate Finance Committee is able to finish its work and get a bill to the Senate floor. There are two different ways in which a tax package can be enacted from this point forward. First, the Senate can make changes to its package that are acceptable to the House. The House could then take up the Senate plan as is, vote on it and send it to the president upon passage. Alternatively, the House and Senate could pass their own plans and then go to conference committee to work out the differences.

Taking a step back, it is important to understand why the procedural hurdles are likely to slow the process down. In order to use the privileged reconciliation process to pass legislation with just 51 votes in the Senate, Republicans must subject themselves to a series of Senate rules that essentially require them to pick just two of the following three options: enact sizable gross tax cuts, maintain popular tax breaks and achieve permanence for the changes. It is possible, for instance, to pass sweeping tax cuts while maintaining popular tax breaks such as the mortgage interest deduction and the deduction for state & local taxes, but Senate rules would almost certainly make it so that these tax cuts must have an expiration date, be phased-in, or some combination of the two. Alternatively, policymakers could choose the permanent/maintain big tax breaks combination, but this would mean the gross tax cuts that have been proposed would have to be scaled back.

The most recent scores from the Joint Committee on Taxation, the official scorekeeper for Congress on revenue matters, estimate the FY 2027 budget deficit (the last year of the budget window) would be $155.6 billion under the House plan and $216.7 billion under the Senate plan. These deficit estimates suggest budget deficits will continue past the budget window, a violation of Senate reconciliation rules and an elephant in the room that policymakers have still yet to address.

As can be seen, the two pieces of legislation are quite far apart on a number of key policy issues. Regardless of whether these differences are resolved in the final Senate package or through a conference committee, we maintain the view that the final package will contain smaller and less permanent tax cuts than what is currently being proposed. In addition, we still expect the timeline to be final passage of a tax package in Q1 2018, with the cuts retroactively beginning in January 2018.

Appendix A in pdf.

Australia’s Business Conditions Sharply Improved In October

For the 24 hours to 23:00 GMT, the AUD declined 0.44% against the USD and closed at 0.7618.

LME Copper prices declined 0.4% or $29.0/MT to $6768.0/MT. Aluminium prices rose 0.5% or $10.0/MT to $2100.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7629, with the AUD trading 0.14% higher against the USD from yesterday's close, following upbeat Australian economic data.

Overnight data indicated that Australia's NAB business conditions index jumped to a record high level of 21.0 in October, suggesting that businesses are growing much more confident about the nation's improving economic conditions and strengthening labour market. In the prior month, the index had registered a level of 14.0. Also, the nation's NAB business confidence index remained unchanged at a level of 8.0 in October.

Elsewhere, in China, Australia's largest trading partner, industrial production advanced less-than-anticipated by 6.2% on an annual basis in October, pointing to a slowdown in the nation's industrial sector. Markets had anticipated industrial production to gain 6.3%, compared to a rise of 6.6% in the prior month.

Moreover, the nation's retail sales rose 10.0% YoY in October, undershooting market expectations for an increase of 10.5%. Retail sales had recorded a rise of 10.3% in the prior month.

The pair is expected to find support at 0.7604, and a fall through could take it to the next support level of 0.7579. The pair is expected to find its first resistance at 0.7660, and a rise through could take it to the next resistance level of 0.7691.

Going forward, Australia's Westpac consumer confidence index for November, due to release overnight, will be on investors' radar.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

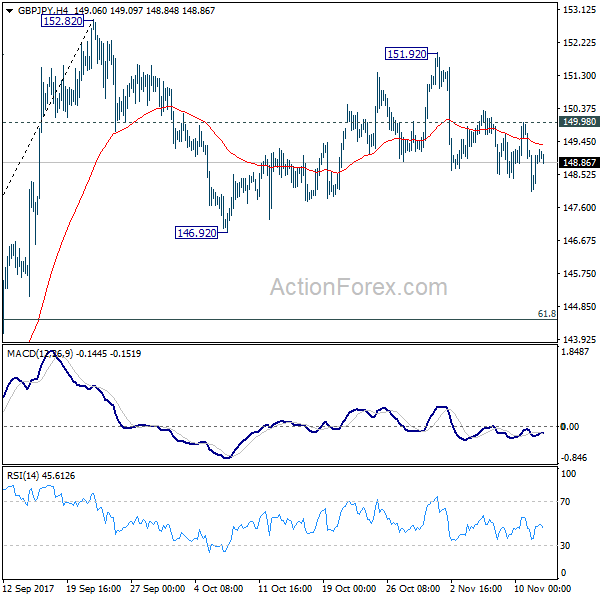

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.61; (P) 149.46; (R1) 150.54; More

At this point, intraday bias in GBP/JPY remains mildly on the downside for 146.92 support and below. Fall from 151.92 is seen as the third leg of the corrective pattern from 152.82. We'd expect strong support from 61.8% retracement of 139.29 to 152.82 at 144.45 to contain downside and bring rebound. On the upside, break of 149.98 resistance will turn bias back to the upside for 151.92/152.82 resistance zone instead.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

Euro Trading A Tad Higher, Ahead Of ECB President’s Speech

For the 24 hours to 23:00 GMT, the EUR rose 0.13% against the USD and closed at 1.1665.

On the data front, Germany's wholesale price index rose 3.0% on a yearly basis in October, following a rise of 3.4% in the prior month.

Macroeconomic data showed that the US posted a budget deficit of $63.2 billion in October, higher than market expectations for the nation to register a deficit of $50.0 billion. In the previous month, the nation had recorded a budget surplus of $8.0 billion.

In the Asian session, at GMT0400, the pair is trading at 1.1671, with the EUR trading marginally higher against the USD from yesterday's close.

The pair is expected to find support at 1.1647, and a fall through could take it to the next support level of 1.1624. The pair is expected to find its first resistance at 1.1685, and a rise through could take it to the next resistance level of 1.1700.

Ahead in the day, market participants would focus on the release of flash 3Q GDP and ZEW economic sentiment index across the Euro-zone. Moreover, comments from the European Central Bank (ECB) Chief, Mario Draghi as well as the Federal Reserve Chair, Janet Yellen, will be closely monitored by investors.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

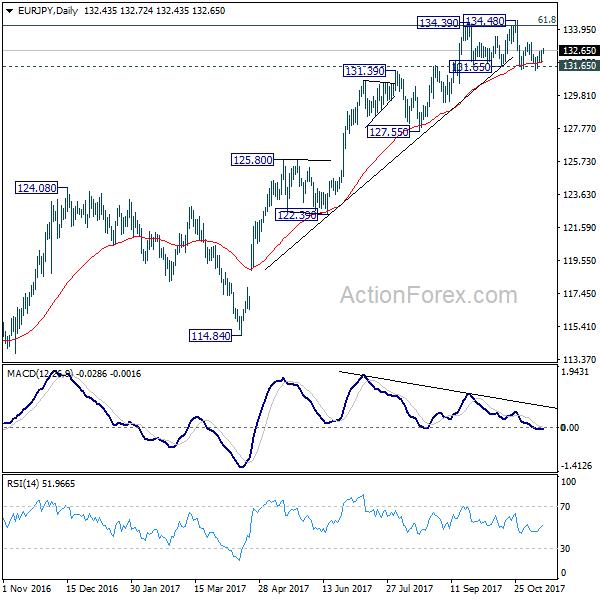

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.48; (P) 132.29; (R1) 133.20; More....

Intraday bias in EUR/JPY remains neutral at this moment. On the upside, decisive break of 134.39/48 resistance zone is needed to confirm up trend resumption. Otherwise, even in case of rebound, near term outlook is neutral at best. On the downside, decisive break of 131.65 will confirm rejection from 134.20 fibonacci level and confirm near term reversal. And, in such case, intraday bias will be turned to the downside for 127.55 key support level.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will argue that the medium term trend has reversed and will turn outlook bearish for deeper fall back to 114.84/124.08 support zone at least.

Pound Trading Marginally Lower, Ahead Of Britain’s Crucial Inflation Data

For the 24 hours to 23:00 GMT, the GBP marginally declined against the USD and closed at 1.3114, weighed by profound concerns over whether the British Prime Minister, Theresa May still has the political clout to govern the nation and deliver a good Brexit deal.

In the Asian session, at GMT0400, the pair is trading at 1.3113, with the GBP trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.3072, and a fall through could take it to the next support level of 1.3030. The pair is expected to find its first resistance at 1.3145, and a rise through could take it to the next resistance level of 1.3176.

Going ahead, traders would direct their attention to UK's consumer price index for October, slated to release in a few hours.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

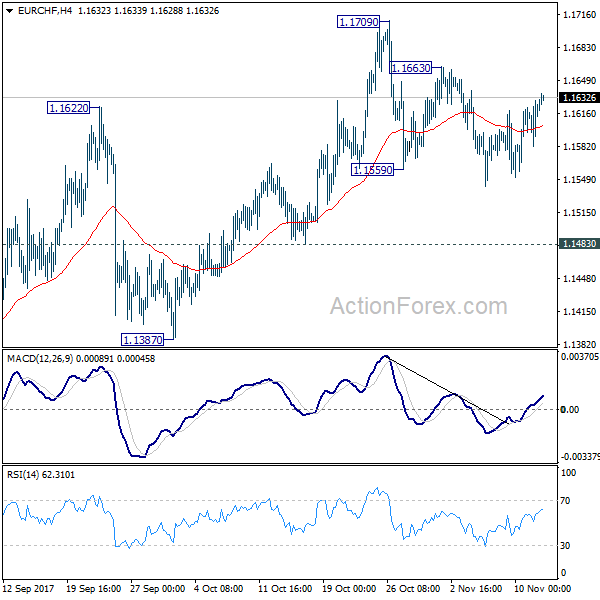

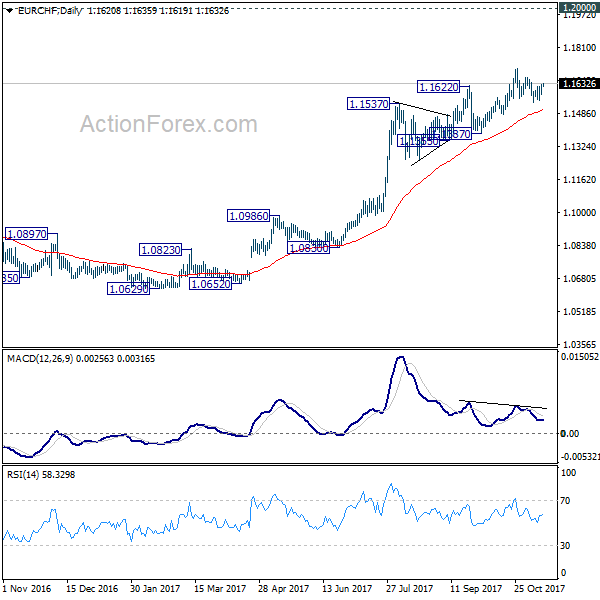

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1557; (P) 1.1598; (R1) 1.1655; More...

Intraday bias remains neutral in EUR/CHF and outlook is unchanged. With 1.1483 support intact, further rally is expected. On the upside, above 1.1663 minor resistance will turn bias back to the upside for 1.1709 high. Break will resume medium term rally to 1.2 key level. However, break of 1.1483 will be an early sign of reversal. In that case, deeper decline should be seen back to 1.1355 support.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1105) and possibly below.