Sample Category Title

Market Update – Asian Session: China Industrial Production Comes In Lower

Headlines/Economic Data

Japan

(JP) Bank of Japan (BOJ) Gov Kuroda: we continue to pursue powerful monetary easing to make sure that positive inflation developments are not cut short - comments in Zurich

(JP) Japan MoF sells ¥1.8T v ¥2.2T indicated in 0.10% 5-yr bonds; avg yield -0.107%; bid-to-cover 4.19x

Korea

(KR) North Korea will continue its pursuit of nuclear missiles in the wake of the United States' rare deployment of three aircraft carrier groups near the Korean Peninsula - letter from North Korea's top envoy to the UN Ja Song-nam to UN Secretary-General Antonio Guterres

China/Hong Kong

(CN) CHINA OCT INDUSTRIAL PRODUCTION Y/Y: 6.2% V 6.7%E ; YTD Y/Y: 6.7% V 6.3%E

(CN) CHINA OCT RETAIL SALES Y/Y: 10.0% V 10.5%E; YTD Y/Y: 10.3% V 10.4%E

(CN) China Oct Foreign Direct Investment (FDI): CNY60.1B v CNY70.3B prior; YTD y/y: +1.9% v 1.6% prior

(CN) CHINA OCT YTD URBAN FIXED ASSETS Y/Y: 7.3% V 7.3%E

(CN) China PBoC Open Market Operations (OMO): CNY280B v CNY180B injected in 7, 14 and 63-day reverse repos prior; Net injection CNY140B v CNY150B prior

USD/CNY (CN) PBOC sets yuan reference rate at 6.6299 v 6.6347 prior

(CN) China National Stats Bureau (NBS): Jobless rate below 5%; CPI is at ideal level

(CN) Former SAFE Official (fx regulator) Guan Tao: China reforms of its mechanism for determining the exchange rate should include FX market development and loosening of controls

(CN) China State Researcher Zhu sees 2018 GDP growth of 6.5% and CPI at 3% - China Financial News (yesterday)

(CN) China Premier Li Keqiang said to tell Japan PM Abe that both countries should boost cooperation on trade

(HK) According to Credit Suisse analysts Macau Nov 1-12th gaming Rev +20-22% y/y v 15%e

(CN) China 10-year bond yield trades at 4%, first time since 2014

(HK) Macau Gaming Regulator's Chan: To continue existing regulations on junkets, have banned over 200 people entering casino this year

Australia/New Zealand

(AU) Australia Oct NAB Business Conditions: 21 v 14 prior (record high); Confidence: 8 v 8 prior

(AU) Australia sells A$150M v A$150M indicated in Aug 2035 indexed bonds; avg yield 0.9732%; bid-to-cover 2.93x

(NZ) Reserve Bank of New Zealand (RBNZ) confirms dashboard approach to quarterly bank disclosures

US

(US) US Treasury Sec Mnuchin: Looks forward to successful House tax vote this week; Imposes 183.4-194.9% duties on China plywood imports

Levels as of 23:00ET

Nikkei +0.5%, Hang Seng -0.0%; Shanghai Composite -0.5%; ASX200 -0.9%, Kospi -0.2%

Equity Futures: S&P500 -0.1%; Nasdaq100 -0.1%, Dax -0.1%; FTSE100 -0.2%

EUR 1.1676-1.1662; JPY 113.73-113.57; AUD 0.7638-0.7609;NZD 0.6903-0.6860

Dec Gold -0.2% at $1,276/oz; Dec Crude Oil -0.2% at $56.63/brl; Dec Copper -0.3% at $3.12/lb

Narrative

Asian equity markets opened today's trading session mixed. Australia's equity market has declined by over 0.9%. The S&P ASX 200 Materials and Energy indices have each lost over 1% on the session. Shares of Woodside Petroleum have declined by over 3%. On Monday, Shell announced that it would sell down shares in the Australian energy producer.

Besides this, the ASX 200 Financials index has lost over 0.6%. In Japan, large bank Mizuho Financial has declined on the session, as the company reported better than expected Q2 results and affirmed its FY forecast. Later today, mega banks Mitsubishi UFJ and Sumitomo Mitsui are due to issue their financial reports. In Hong Kong, the Hang Seng Financials index has traded little changed. China Oct M2 money supply and new yuan loans data, which were released on Monday, missed market expectations.

Property shares in Hong Kong have traded generally lower. Sunac China has declined by more than 5%. In Oct, China's Home Sales Value declined by over 3%, which was the largest y/y drop in over 2 years.

The Hang Seng Information Technology index has risen by over 0.6%, amid gains in shares of Tencent. In South Korea, shares of chipmaker Hynix have risen by over 0.5%. Shares of Micron rose by over 1.5% during Monday's NY session. Toshiba has gained over 7% amid speculation that the firm could reach a settlement agreement with Western Digital.

Japan's Fast Retailing has traded marginally higher. The S&P 500 Consumer Discretionary sector gained 0.3% on Monday's trading session.

Shares of Samsonite have traded higher by over 3% in Hong Kong following the company's Q3 results and the overall Hang Seng Consumer Goods index has gained over 0.7%. In Australia, the ASX Consumer Discretionary index has declined by over 0.8%. Shares of JB Hi-Fi (home products retailer) have declined by over 3%, while HT&E (media company) and Harvey Norman (consumer retailer) have lost over 2%.

At the same time, the interest rate sensitive sectors are declining in Australia. The ASX 200 Utilities index has declined by over 1.4%, while the REIT index is off by more than 0.9%. Australia's 3-year bond yield has risen by more than 4bps on the session. In Oct, Australia's NAB business conditions index rose to a record high.

Following the data the Aussie moved slightly higher, but has since pared some of its gains amid the release of China's Oct data points.

China Retail Sales in Oct rose at the slowest pace since Jan, while Industrial Production growth slowed to 6.2% y/y (from 6.6% prior). Monthly, power output growth slowed to 2.5% vs 5.3% prior. Despite the data, China's 10-year bond yield has risen to 4%, for the first time since 2014.

US Treasury Futures are currently little changed. However, USD/JPY volatility has hit 3-week highs. Looking ahead, the US House of Representatives may vote on its tax reform bill by as early as this Thursday, according to press reports.

In the corporate bond market, Resolute Energy withdrew its proposed high-yield offering of $550M in 2025 notes citing broader market conditions. Recall, at the end of last week NRG Energy withdrew a $870M 2028 high-yield offering, citing a similar reason.

In emerging market sovereigns Venezuela, which held a meeting with bondholders on Monday, had its credit rating cut to ‘SD' from ‘CC' at S&P on the expectation that another debt payment could be missed.

Japanese companies due to report earnings later today: include Ai Holdings, Amada, DIC Corp, Daido Metal, Dentsu, Ferrotec, Fukui Computer Holdings, Heiwa Corp, Idemitsu Kosan, Hikari Tsushin, Japan Post Bank, Japan Post Holdings, Japan Post Insurance, Kajima, Kansai Urbank Banking, Kyushu Financial Group, Mitsubishi UFJ, Nippon Paint Holdings, Okumura Corp, Open House, Otsuka Holdings, Recruit Holdings, Seiko Holdings, Showa Denko, Sumitomo Mitsui Financial, Sumitomo Realty & Development, Takamatsu Construction Group, The Dai-ichi Insurance, Yokohama Rubber, Toei, Tokyo Seimitsu; Tsubaki Nakashima and Unipres Corp.

Japan's Q3 preliminary GDP data is due to be released on tomorrow's session, along with Australia's Q3 wage price index.

Equities notable movers

Australia/New Zealand

TWR.AU Reports FY17 (A$) underlying net 18M v 201M y/y; Net earned premium 256.9M v 253.8M y/y; To launch NZ$70M rights issue priced at NZ$0.42/shr; -10.5%

SDA.AU Awarded fully managed communications contract for Nabors in South America; no terms disclosed; +7%

Japan

9984.JP No final agreement on investment into Uber, may not make investment if terms are not satisfactory; -0.4%

382.JP Weakness due to being removed from MSCI Japan Index; -12%

China/Hong Kong

1316.HK Added to MSCI China Index; +7%

US

BWLD Reportedly receives >$150/shr takeover offer from Roark Capital – press; +27.9% afterhours

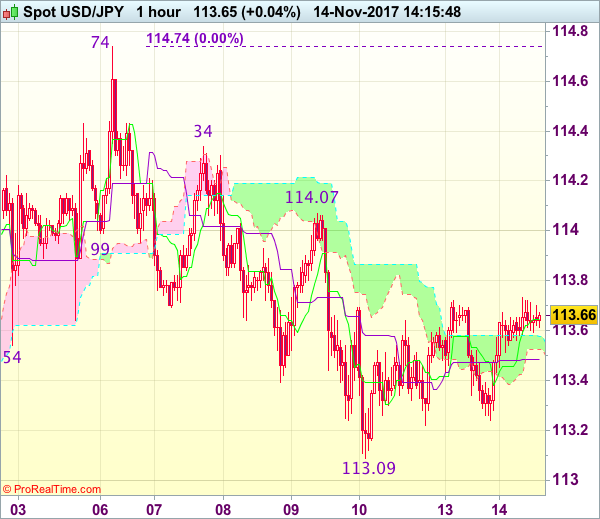

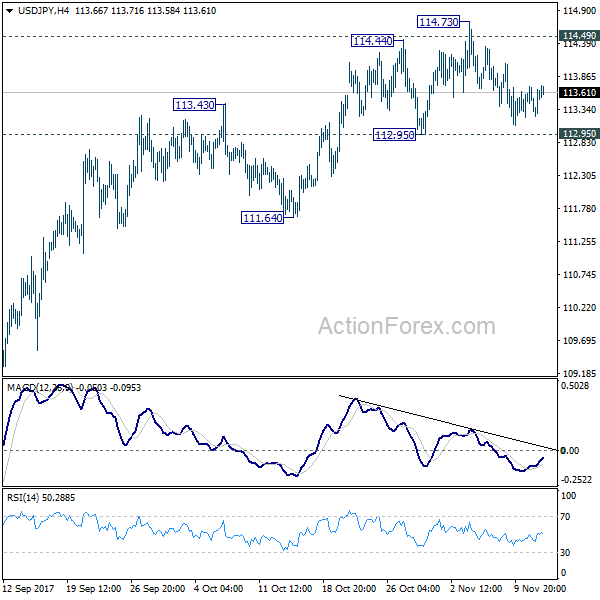

Trade Idea : USD/JPY – Hold short entered at 114.00

USD/JPY - 113.47

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 113.65

Kijun-Sen level : 113.49

Ichimoku cloud top : 113.58

Ichimoku cloud bottom : 113.52

Original strategy :

Sold at 114.00, Target: 113.00, Stop: 113.70

Position : - Short at 114.00

Target : - 113.00

Stop : - 113.70

New strategy :

Hold short entered at 114.00, Target: 113.00, Stop: 113.70

Position : - Short at 114.00

Target : - 113.00

Stop : - 113.70

Although the greenback recovered again after finding support at 113.24 and further consolidation would be seen, as long as 113.70 holds, bearishness remains for another decline, below said support at 113.20-24 would bring a retest of last week’s low at 113.09, break there would extend the fall from 114.74 top to previous support at 112.96, below there would bring further subsequent selloff to 112.60 but support at 112.30 should hold from here due to near term oversold condition.

In view of this, we are holding on to our short position entered at 114.00. Only above resistance at 114.07 would abort and signal the retreat from 114.74 has ended instead, bring a stronger rebound to 114.34, then retest of this level, above there would revive bullishness and extend recent rise from 107.32 to 115.00.

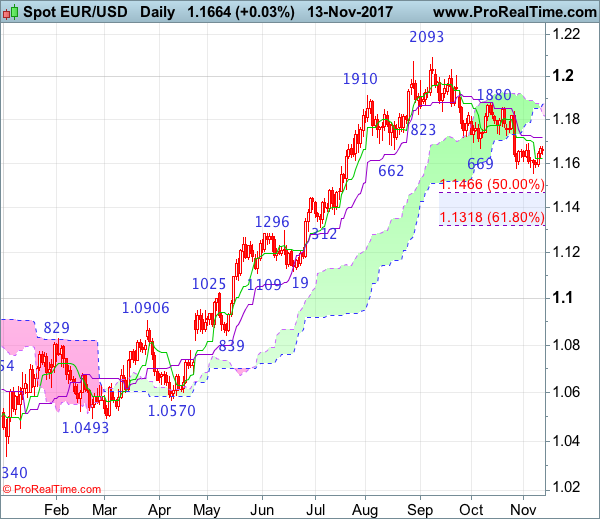

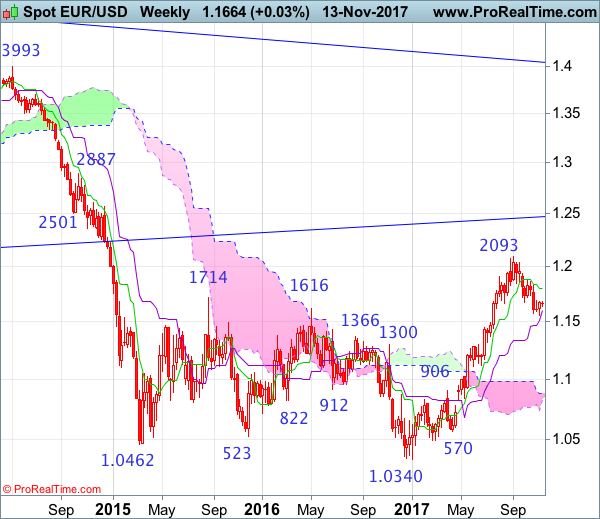

EUR/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 31 Jul 2017

• Trend bias: Near term up

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 2 Aug 2017

• Trend bias: Up

EUR/USD – 1.1674

As the single currency has rebounded after falling to 1.1554 (with a hammer candlestick reversal pattern on the daily chart), suggesting consolidation above this level would be seen and recovery to the Kijun-Sen (now at 1.1717) cannot be ruled out, however, reckon previous support at 1.1725 would limit upside and bring another decline later, below said support at 1.1554 would extend the fall from 1.2093 top to 1.1500 and later towards 1.1465-66 (50% Fibonacci retracement of 1.0839-1.2093) but reckon 1.1370 support would hold and price should stay above 1.1312-18 (previous support and 61.8% Fibonacci retracement).

On the upside, whilst an initial recovery to 1.1700 cannot be ruled out, reckon the Kijun-Sen (now at 1.1717) would limit upside and price should falter below 1.1725 (previous minor support), bring another decline to aforesaid downside targets. A daily close above previous support at 1.1725 would defer and suggest low is possibly formed instead, risk rebound to 1.1790-00, then test of resistance at 1.1837 but break there is needed to add credence to this view, bring another bounce to indicated previous resistance at 1.1880 first.

Recommendation: Sell at 1.1715 for 1.1515 with stop above 1.1815.

On the weekly chart, as euro found support at 1.1554 (just held above the Kijun-Sen) and has recovered, a white candlestick was formed last week, hence consolidation would be seen and recovery towards 1.1715-25 cannot be ruled out, however, reckon upside would be limited to 1.1750-55 and price should falter well below the Tenkan-Sen (now at 1.1795) and bring another retreat later, below said support at 1.1554 would extend the retreat from 1.2093 top for retracement of recent rise to 1.1500, then 1.1466 (50% Fibonacci retracement of 1.0839-1.2093) but reckon downside would be limited to 1.1400 and 1.1312-18 (previous support and 61.8% Fibonacci retracement) should hold, price should stay above previous minor resistance at 1.1296, bring rebound later.

On the upside, expect recovery to be limited to 1.1700 and renewed selling interest should emerge around (1.1715-25), bring another decline later. Above 1.1790-00 would risk test of indicated resistance at 1.1837 but only break of resistance at 1.1880 would shift risk back to the upside and suggest the pullback from 1.2093 top has ended, bring further gain to 1.1935-40, then towards 1.2035-40. Having said that, break there is needed to provide confirmation, bring retest of 1.2093.

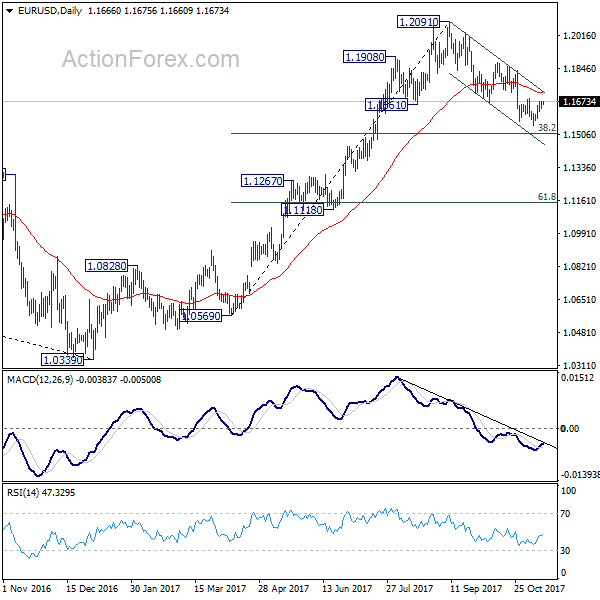

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1584; (P) 1.1631 (R1) 1.1708; More...

Intraday bias remains neutral at this point. Also, As long as 1.1689 resistance holds, outlook stays bearish and deeper decline is in favor. Below 1.1553 will resume whole fall from 1.2091 and target 38.2% retracement of 1.0569 to 1.2091 at 1.1510. We'd be cautious on strong support from there to bring rebound. But sustained break of 1.1510 will pave the way to next support zone at 1.1118/1267. On the upside, break of 1.1689 resistance will now indicate short term bottoming and turn bias back to the upside for 1.1836 resistance instead.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1346) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

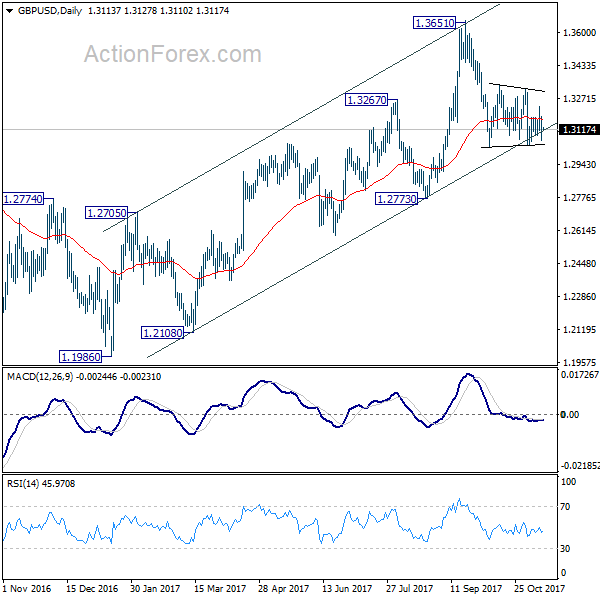

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3088; (P) 1.3159; (R1) 1.3259; More....

GBP/USD is staying in range of 1.3038/3337 and intraday bias remains neutral. In case of another recovery, upside should be limited below 1.3337 resistance to bring fall resumption. Break of 1.3038 will now resume decline from 1.3651 to 1.2773 key support level. However, decisive break of 1.3337 will indicate that pull back from 1.3651 is completed and medium term rise from 1.1946 is resuming.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

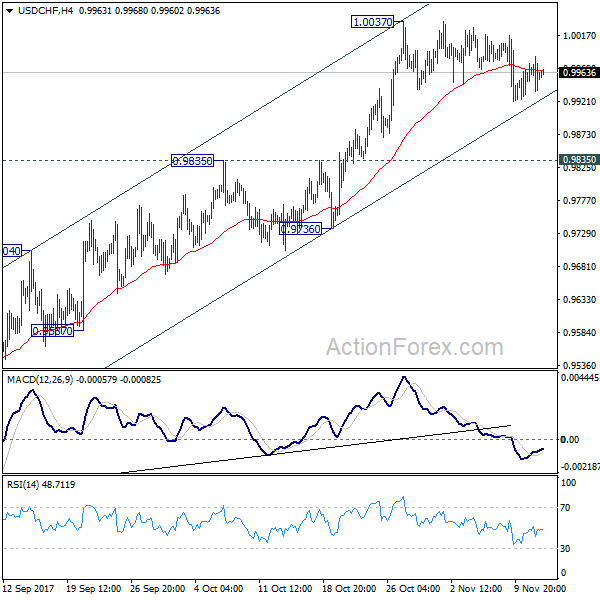

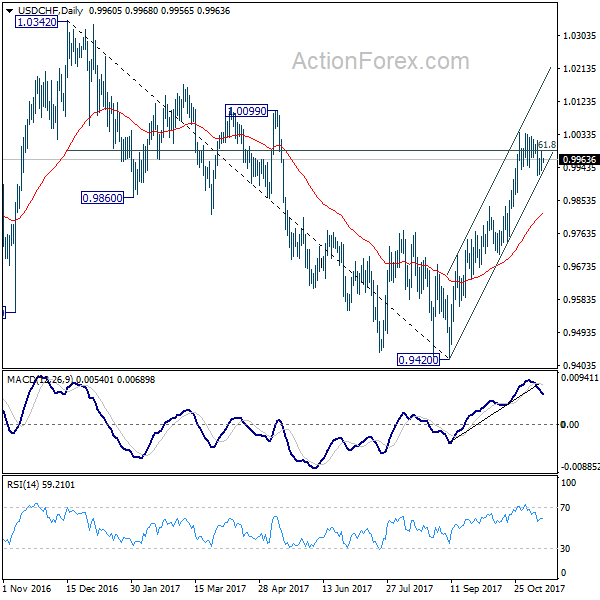

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9908; (P) 0.9968; (R1) 1.0015; More....

No change in USD/CHF's outlook. It is still staying in consolidation from 1.0037 and intraday bias remains neutral first. We'd continue to expect downside to be contained above 0.9835 resistance turned support and bring rally resumption. On the upside break of 1.0037 will resume whole rally from 0.9420. And with sustained trading above 61.8% retracement of 1.0342 to 0.9420 at 0.9990, USD/CHF should then target a test on 1.0342 key resistance.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

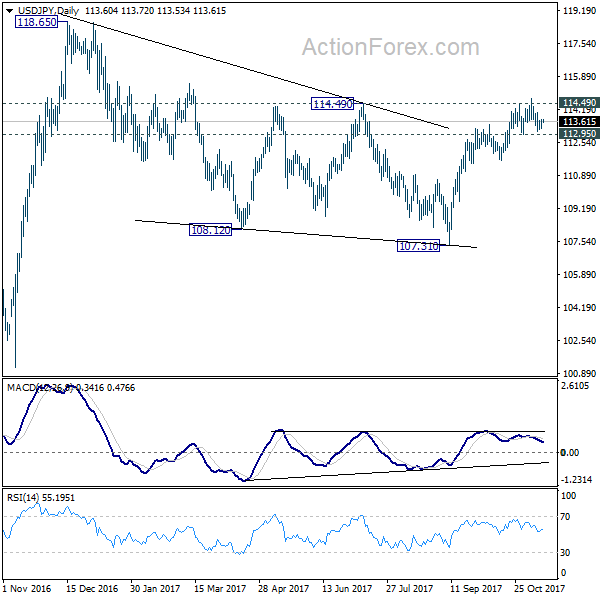

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.82; (P) 113.77; (R1) 114.47; More...

No change in USD/JPY's outlook. It continues to stay in range above 112.95 and intraday bias remains neutral at this point. As long as 112.95 support holds, near term outlook remains bullish and further rise is expected. On the upside, sustained break of 114.49 key resistance will pave the way to retest 118.65 high. However, break of 112.95 support will now indicate rejection from 114.49 and turn bias to the downside for 111.64 support and below.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

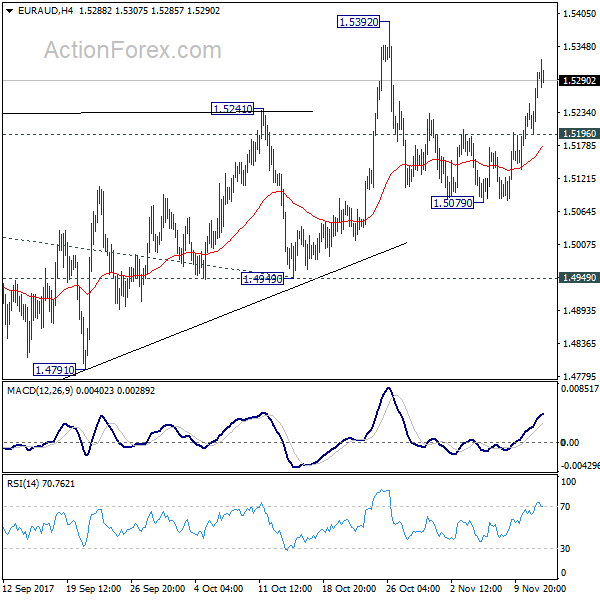

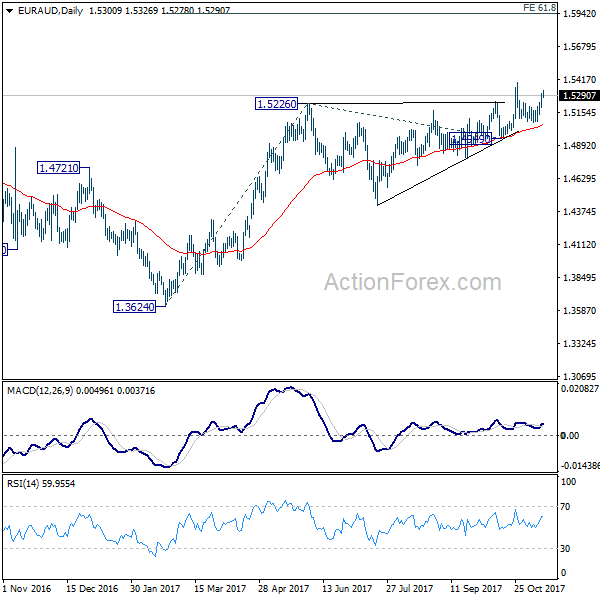

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5122; (P) 1.5178; (R1) 1.5277; More....

EUR/AUD's strong rebound argues that pull back from 1.5392 could have completed at 1.5079 already. Intraday bias is turned back to the upside for 1.5392 first. Break there will resume medium term rise from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. On the downside, below 1.5196 will turn intraday bias neutral again and extend the consolidation from 1.5392. But overall, as long as 1.4949 support holds, outlook remains bullish and further rise is in favor.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. However, break of 1.4949 support will dampen our view and argue that rise from 1.3624 has completed. In that case, EUR/AUD would turn southward for retesting 1.3624 low.

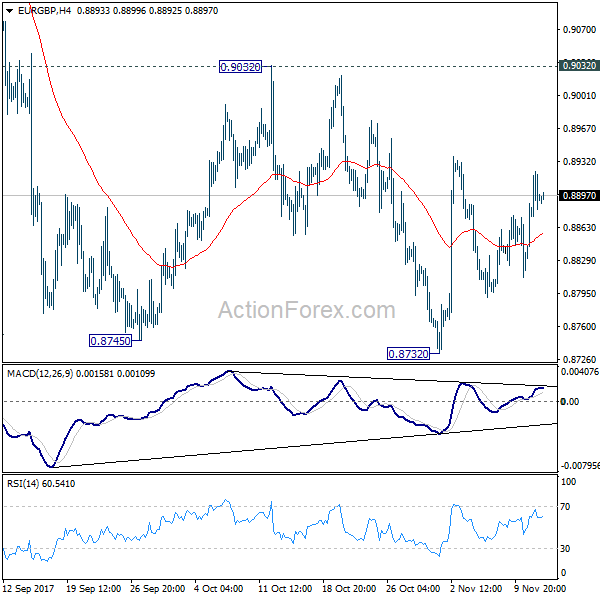

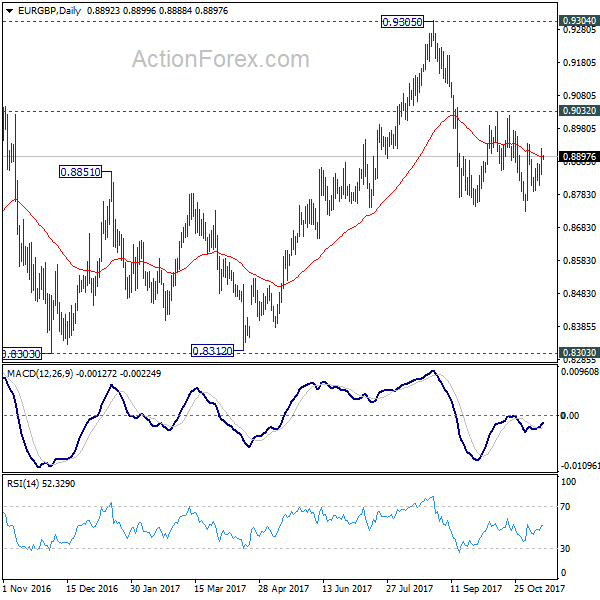

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8792; (P) 0.8840; (R1) 0.8889; More...

EUR/GBP is still bounded in range of 08732/9032 and intraday bias remains neutral. With 0.9032 resistance intact, deeper decline is mildly in favor in the cross. Break of 0.8732 will resume the decline from 0.9305 and target 0.8303 key support level. However, on the upside, decisive break of 0.9032 will confirm completion of the decline from 0.9305. In such case, intraday bias will be turned back to the upside for retesting 0.9305 key resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Pound Stabilizes after Selloff, Focus Stays in UK with CPI Featured

After suffering steep selloff yesterday on political uncertainties, Sterling stabilized and recovers mildly today. But focus will set to stay in the UK with CPI featured in the economic calendar. For the moment, GBP/USD and EUR/GBP are still holding in range. Thus, we're treating the selloff in the Pound as part of a corrective pattern first. Meanwhile, the calendar is getting busy today with Eurozone set to release GDP, industrial production as well as German ZEW economic sentiment. Some volatility could be seen in EUR/GBP. US will also release PPI later today which gives the market a glimpse of the inflation outlook, and as a prelude to Wednesday's CPI release. The greenback is generally staying in consolidation mode and needs fresh inspiration for a breakout.

Treasury Mnuchin: Trump will not accept corporate tax at more than 20%

In the US, Treasury Secretary Steven Mnuchin warned that President Donald Trump's administration will not accept nor support any tax plan with a corporate tax rate of more than 20%. This is in regards to the negotiations between the House and the Senate for reconciliations of their passed bills. The House version of the tax bill will comes to floor later this week. Debate will begin on Thursday. Chairman of the tax-writing Ways and Means Committee Kevin Brady expressed his confidence for passage. Senate Finance Committee started debating their tax bill yesterday. And there could be significant revisions to be announced this week.

Brexit Davis: Parliament will have final vote on Brexit deal

Brexit Secretary David Davis announced in the House of Commons that he will introduce legislation for the parliament to vote on the final Brexit agreement with EU. He noted that "it is clear that we need to take further steps to provide clarity and certainty both in the negotiations and at home regarding the implementation of any agreement into United Kingdom law." And he emphasized that "this agreement will only hold if parliament approves it." The "principal policy aim" will be read by October 2018, which should give enough time for debate and vote before the Brexit date on March 29, 2019. However, under the move, the Parliament will have no say in case of a no-deal, not be able to reverse the decision, and not even be able to reopen talks.

ECB Constancio: Stimulus program "highly successful"

ECB Vice President Vitor Constancio hailed the central bank's massive monetary stimulus as "highly successful" in driving recovery. He pointed out that "the euro-area economy is experiencing a broad-based, robust and resilient recovery." Nonetheless, he maintained a cautious tone and emphasized "we know that this process still relies significantly on our monetary policy support. It is not yet self-sustained and therefore we must be patient and persistent." Meanwhile he also defended the monetary policy measures and emphasized they "were not an 'experiment'" but " in line with the policies previously adopted by other major central banks." Also, despite concerns "about possible collateral consequences of our policy, such concerns have however not materialized in real facts and we can now underline the appropriateness of our monetary policy stance."

BoJ Kuroda to persist with "powerful monetary easing"

BoJ Governor Haruhiko Kuroda reiterated his pledge to persist with "powerful monetary easing". He said in a speech at the University of Zurich in Switzerland that this powerful monetary easing "has been producing remarkable effects." And Japan is "no longer in deflation". He noted "going forward, with the output gap improving steadily, firms' stance is likely to gradually shift toward raising wages and prices." And he's optimistic that "if further price rises come to be widespread, inflation expectations are likely to rise steadily." Therefore, he emphasized that "the Bank will continue to persist with powerful monetary easing to ensure that such positive developments are not cut short."

NAB: Better than expected performance for the economy ahead

In Australia, NAB business conditions jumped 7 points to 21 in October, hitting the highest level the series began back in 1997. It's also nearly four times the historical average. Business confidence, on the other hand, was unchanged at 8. NAB chief economist Alan Oster noted that "this is an extremely strong result and of itself would suggest a better than expected performance for the economy." However, he also warned that "it is unclear just how long conditions can remain at these record levels given that the result was driven by a surprise jump in manufacturing, while some of the leading indicators such as forward orders - which have been giving a more accurate read on the strength of the economy - have actually softened a little in recent months."

China data disappoint

From China, retail sales rose 10.0% yoy in October, below expectation of 10.5% and slowed from prior 10.3% yoy. Fixed asset investment rose 7.3% yoy, inline with expectation but slowed from prior 7.5% yoy. Industrial production rose 6.2% yoy, meeting consensus but also slowed from prior 6.6 yoy.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8792; (P) 0.8840; (R1) 0.8889; More...

EUR/GBP is still bounded in range of 08732/9032 and intraday bias remains neutral. With 0.9032 resistance intact, deeper decline is mildly in favor in the cross. Break of 0.8732 will resume the decline from 0.9305 and target 0.8303 key support level. However, on the upside, decisive break of 0.9032 will confirm completion of the decline from 0.9305. In such case, intraday bias will be turned back to the upside for retesting 0.9305 key resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | NAB Business Confidence Oct | 8 | 7 | 8 | |

| 2:00 | CNY | Retail Sales Y/Y Oct | 10.00% | 10.50% | 10.30% | |

| 2:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Oct | 7.30% | 7.30% | 7.50% | |

| 2:00 | CNY | Industrial Production Y/Y Oct | 6.20% | 6.20% | 6.60% | |

| 7:00 | EUR | German GDP Q/Q Q3 P | 0.60% | 0.60% | ||

| 7:00 | EUR | German CPI M/M Oct F | 0.00% | 0.00% | ||

| 7:00 | EUR | German CPI Y/Y Oct F | 1.60% | 1.60% | ||

| 8:15 | CHF | Producer & Import Prices M/M Oct | 0.50% | |||

| 8:15 | CHF | Producer & Import Prices Y/Y Oct | 0.80% | |||

| 9:00 | EUR | Italian GDP Q/Q Q3 P | 0.50% | 0.40% | ||

| 9:30 | GBP | CPI M/M Oct | 0.20% | 0.30% | ||

| 9:30 | GBP | CPI Y/Y Oct | 3.10% | 3.00% | ||

| 9:30 | GBP | Core CPI Y/Y Oct | 2.80% | 2.70% | ||

| 9:30 | GBP | RPI M/M Oct | 0.20% | 0.10% | ||

| 9:30 | GBP | RPI Y/Y Oct | 4.10% | 3.90% | ||

| 9:30 | GBP | PPI Input M/M Oct | 0.80% | 0.40% | ||

| 9:30 | GBP | PPI Input Y/Y Oct | 4.70% | 8.40% | ||

| 9:30 | GBP | PPI Output M/M Oct | 0.30% | 0.20% | ||

| 9:30 | GBP | PPI Output Y/Y Oct | 2.90% | 3.30% | ||

| 9:30 | GBP | PPI Output Core M/M Oct | 0.20% | 0.00% | ||

| 9:30 | GBP | PPI Output Core Y/Y Oct | 2.20% | 2.50% | ||

| 9:30 | GBP | House Price Index Y/Y Sep | 5.20% | 5.00% | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Sep | -0.60% | 1.40% | ||

| 10:00 | EUR | German ZEW Economic Sentiment Nov | 19.5 | 17.6 | ||

| 10:00 | EUR | German ZEW Current Situation Nov | 88 | 87 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | 29.3 | 26.7 | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | 0.60% | 0.60% | ||

| 13:30 | USD | PPI M/M Oct | 0.10% | 0.40% | ||

| 13:30 | USD | PPI Y/Y Oct | 2.30% | 2.60% | ||

| 13:30 | USD | PPI Core M/M Oct | 0.20% | 0.40% | ||

| 13:30 | USD | PPI Core Y/Y Oct | 2.20% | 2.20% |