Sample Category Title

Market Morning Briefing: The Pound Dipped To 1.3061

STOCKS

Dow (23439.70, +0.07%) has very near term support at 23320 and has some chances of moving up from here towards 23500 and higher. A break below 23320 would take it lower towards 22800 in the near term.

Dax (13074.42, -0.04%) moved into our support zone of 12900-13000 as mentioned yesterday and bounced back sharply from the intra-day low of 12960. Note that 12900 is likely to act as an immediate support and while that holds, the index may either trade sideways above 12900 or rise back towards 13200 and higher.

Nikkei (22441.24, +0.27%) has formed near term top at 23382 and it does not seem very likely that the index would get back to those levels in the coming sessions. Rather we may expect a test of 22170 in the near term followed by a small rise. Keep an eye on the Dollar Yen which could find some support near 113.40/50 and if the currency pair rises back towards 114, Nikkei could gain a bit this week.

Shanghai (3437.97, -0.29%) has come off after testing 3450 on the upside. While 3450 holds, a downside test of 3440-3420 is possible; else if the rise sustains above 3450, we may target 3500 in the medium term. A rise in the index could be boosted by the rise in Copper (3.1165) as the metal is also rising from support levels and looks bullish for the near term.

Nifty (10224.95, -0.94%) has been falling in line with our expectation and while the fall continues, the index may come down to test 10125-10100 levels in the coming sessions. Note that 10100 is a decent support and could produce a bounce taking the index back towards 10200-10250 in the medium term. Near term looks bearish.

COMMODITIES

Gold (1275.74) likely to trade quietly in the 1290-1260 region for some time before moving up sharply to levels above 1300. While long term looks bullish, the price lacks momentum just now and needs some trigger from movement in the US Dollar Index as well.

Brent (62.97) is likely to move down towards 62-61 as mentioned yesterday. Upside room towards 65 is still open for another attempt but the price action looks bearish for the coming sessions.

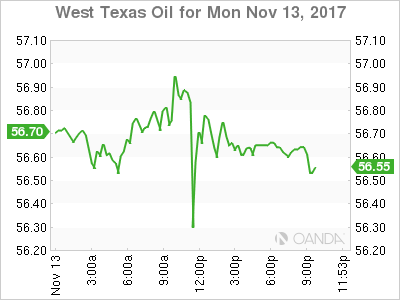

WTI (56.64) is almost stable, trading below important resistance near 58.50. Medium to long term looks bearish. Initial target could be seen at 55 on a break below 56.

Copper (3.1165) has bounced from immediate support near 3.05and could now be headed towards 3.20/25. Near term looks bullish while above 3.00-3.05 levels.

FOREX

Although the Euro (1.1671) trades a little higher and might even try to test 1.1725-45 on the upside, the Dollar Index (94.49) continues to have Support in the 94.35-20 region, with chances of new rise towards 95+ in the next couple of weeks, as mentioned yesterday.

This suggests limited upside for the Euro, but keep an eye on the trajectory of German yields (see Interest Rates below).

In the meanwhile, Dollar-Yen (113.64) remains biddish. With Support at 113.00, we have to see whether there will be a strong rise past 114.00 now or not. The Euro-Yen (132.64) trades a tad higher than yesterday. If it tries to rise towards 134, it might pull Dollar-Yen up with it also.

The Pound (1.3115) dipped to 1.3061 yesterday but did not test 1.3000. Look for an overall range of 1.30-32 over the next few days with chances of fresh bullishness. The Aussie (0.7634) may have potential for a rise towards 0.77 if the immediate Support at 0.7600 continues to hold. Else, in case of a break below 0.76, it can dip to 0.75 first.

Dollar-Yuan (6.6418) seems to be hesitating a bit in rising past 6.65. Let us see if it continues to remain above 6.6250 over the next few days.

Dollar-Rupee (65.4250) might dip a little towards 65.30-20 over the course of the week.

INTEREST RATES

Keep an eye on the German 30Yr (1.31%) to see whether it will be able to rise past Resistance at current level and whether the German 10Yr (0.42%) will try to rise past 0.50%. Our preference is for the downside. Should the yields rise instead, it will call for a reassessment of the market.

Looking at the German yield Curve, the 30-5Yr Spread (1.627%) may also have limited upside from here.

The US yields continue to rise, especially at the short-end of the Curve with the 2Yr now at 1.69% and no signs of fatigue. The Yield Curve continues to flatten, with the 30-5 (0.80%) and 30-10 Spread (0.47%) trading below long-term Resistances.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD didn't make significant movement yesterday. The bias remains neutral in nearest term. Price has been moving sideways for the last two weeks between 1.1670/90 – 1.1555 as you can see on my H1 chart below suggests a consolidation phase. A clear break above 1.1670/90 would expose 1.1725 or higher but as long as stay below 1.1900 I remain bearish as a part of the “head and shoulders” bearish scenario on daily chart. On the downside, a clear break and daily close below 1.1555 would expose 1.1450 region.

GBPUSD

The GBPUSD attempted to push lower yesterday bottomed at 1.3061 but closed a little bit higher at 1.3114 after bounced-off the trend line support as you can see on my daily chart below. The bias is neutral in nearest term but as long as stay above 1.3000 I remain bullish and any downside pullback should be seen as a good opportunity to buy. Immediate resistance is seen around 1.3150. A clear break above that area could trigger further bullish pressure testing 1.3200/25 area but key resistance remains at 1.3330 which need to be clearly broken to the upside to resume the major bullish scenario.

USDJPY

The USDJPY didn't make significant movement yesterday. The bias remains neutral in nearest term. Price has been moving sideways between 114.50 – 113.20 range area for the last three weeks suggests a consolidation phase. The bearish pin bar scenario on daily chart remains valid, but need a clear break below 113.20 to continue the bearish scenario testing 112.50 – 111.65 support area. On the upside, 114.50 remains a key resistance and good place to sell with a tight stop loss. Overall I remain neutral.

USDCHF

The USDCHF was indecisive yesterday. There are no changes in my technical outlook. The bias remains neutral in nearest term and price is still trapped between 1.0037 – 0.9940 range area as you can see on my daily chart below. Overall I remain bullish but need a clear break above 1.0037 to resume the bullish trend testing 1.0100 or higher. On the downside, a clear break below 0.9940 would expose 0.9835 support area.

A Case Of The Doldrums

A Case of the Doldrums

Other than a few idiosyncratic storylines, for the most part, G-10 trade remains listless and unable to shake a severe case of the doldrums. And while there have been a couple of fidgets but with few dollar-related news headlines to start the week G-10 trade has driven by a hodgepodge of events. The Pound is floundering as UK Leadership continues to be challenged, EUR and JPY are flat while the Antipodeans trade lower.

The lethargic start to the week has offered few clues, and with all the second-guessing going on surrounding the events in Washington, investors continue to reduce rather than add to exposures.

Bond market quandary remains in full swing as bear flattening 2’s vs 10’s ( UST’s) remains the flavour de jour. While a potpourri of explanations for this phenomena is on offer, but the timing of the move suggests the market is just not buying into the GOP hoopla that the US tax cuts will boost medium to long-term economic growth.

Then again in a forex market long on theory but lacking a comprehensive blueprint for trading the US dollar in a bear flattening cycle. However, if the shift higher in short-term bond yields can be explained away by Fed tightening, then it gives reasons why carry trades will be an open target while haven currencies and gold should underperform.

The Fed goal posts for inflation are still miles away, but even the slightest glean from this week’s CPI has the potential to supercharge the dollar as investors are likely to start pricing a faster pace of monetary tightening by the Federal Reserve into 2018.

There is no fewer than 13 central bank speaker today, and while it’s easy to draw parallels to Sintra, where last year the gathering of central bankers surprised the markets by adopting a more aggressive stance.The fact is most of the global CB’s are coming off dovish policy meetings and unlikely to break rank. However, given the flip-flopping nature of Carney and Draghi who make habits of throwing monkey wrenches into the works, an element of headline risk must be respected.

In the Asia-Pacific region, the diary is dominated by China, which will release key activity data for October.

The Australian Dollar

The Australian dollar is testing the bottom end of recent ranges as commodity prices wobble, and two-year US Treasury yields are moving higher suggesting to some the market is underpricing the FED pace of tightening in 2018.

Unless there some major calamity in the US, a December rate hike is a foregone conclusion. But with the towering US economic data returns adding conviction to the Feds 3 rate hike scenario for 2018 mantra, investors may not be that far behind playing yield curve catch up.

But the logic does not only fall on the US side of reason. The RBA is on hold indefinitely which suggests whatever support from yield premiums the Aussie has been living on will evaporate. Look for the Aussie dollar to remain under pressure as AUD bears pencil in .7500 as the next target

With bullish NZD expectation post, RBNZ getting quashed by overtly pessimistic views from the local Finance Minister, the NZD could also plumb new depths.

Japanese Yen

It has been an arduous task of screen gazing the last 24 hours waiting for something to give. The markets apparently do not want to engage the tug of war between equities and yields suggesting that traders are waiting for some tier one US data that could be decisive in breaking the tedium. CPI remains the central point of convergence, and we should expect the markets to continue tight ranged until then.But it certainly feels like the proverbial calm before the storm scenario.

The Euro

There appeared to be a good argument for the EUR to move higher this week based on robust EU economic data and a tax reform depressed dollar. And while the Eur has climbed higher post ECB meeting fall out, the Dovish ECB guidance continues to hold back any forward topside momentum.

The big question is will the ECB hold firm to their clear dovish guidance or will the data convince them otherwise.

Market positioning is purportedly skewed short, so a push above 1.1725 could cause a bit of a rukus on a squeeze.

EM Asia

Outside of the individual EM storylines in ZAR( downgrade) and TRY ( Geopolitical) in general, EM currencies are going through a mini revaluation despite favourable longer-term macro setups as the markets start to reprice the US rate curve. ON the more extended end of the yield curve, supply uncertainty in the face of a massive budget shortfall has created some waves. While on the short end of the curve, the markets remain massively underpriced vs the FOMC dot plots. As such, EM investors remain caution knowing that at some point something has to give an indeed the market pricing in a faster than expected pace of monetary tightening by the Federal Reserve is one of the significant headwinds for local Asia EM

In the meantime, we are sitting tight awaiting the regional knock-on effects from the China data dump

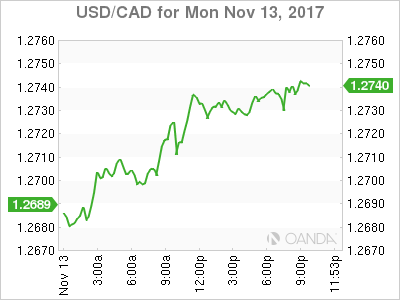

USD/CAD Canadian Dollar Lower As US Dollar Mounts Comeback

The Canadian dollar depreciated on Monday with a flat oil price and little economic data to drive the market. The US dollar rebounded from last week's losses caused by the concerns surrounding the tax reform. The biggest story in the forex market was the lack of confidence in some sections of the conservative party, putting in jeopardy Prime Minister May's tenure. The GBP fell 0.56 percent as the group is 8 signatures short of calling a no confidence vote.

NAFTA talks will reassume on November 17 in Mexico City. The length of the meetings has been extended in an effort to cover more ground ahead of the end of the year. Negotiators have admitted that the original year end deadline to avoid Mexican presidential elections and US primaries from affecting the talks is not realistic. Concerns about NAFTA not reaching a new agreement are rising and putting pressure on the CAD and MXN currencies.

Inflation data will be the highlight this week with figures from the UK, US and Canada on the economic calendar. Canadian inflation will be released by Statistics Canada on Friday, November 17 at 8:30 am EST. Forecasts call for a slight gain of 0.1 percent in November.

The USD/CAD gained 0.34 percent on Monday. The currency pair is trading at 1.2728. The loonie was on the back foot since the Asian market open and it continues to give ground until it closed above the 1.27 price level. The issues with the US tax overhaul have not been resolved, but the USD was oversold ahead of the weekend and is now just appreciating as more traders come back into the market after the memorial day weekend.

US shares rose in anticipation of more details on the difference between the US House and Senate tax reform proposals. The Canadian dollar has been lifted by the problems of the Trump administration to live up to the promises after the election. The market was expecting tax reform and infrastructure spending earlier in the year. The political capital needed for such an undertaking has been squandered and is now a race against time even with a Republican controlled House and Senate.

The gap between the US and Canadian benchmark rates is expected to remain as the U.S. Federal Reserve delivers its final hike of 2017 in December, while the BoC is probably going to sit out the rest of the year after the central bank assessment has become less optimistic.

The Bank of Canada (BoC) has gone from hiking twice in a short span of time (July and September) to a dovish turn in the last rate statement and other speaking engagements by governor Stephen Poloz. Kenny Fisher MarketPulse Analyst wrote earlier today about the BoC Governor:

After staying on the sidelines in October, the Bank of Canada has left the markets guessing regarding a December rate hike. Last week, BoC Governor Stephen Poloz downplayed concerns about low inflation levels, as the inflation target of 2 percent remains elusive. The BoC will have to keep a close eye on developments south of the border. The Federal Reserve is almost certain to raise rates in December, and if the BoC does not match the hike, the Canadian dollar will likely weaken against the greenback. Another headache for the BoC is the threat from the US administration to pull out of the NAFTA agreement, which is a cornerstone of Canada's economy. On his Asian trip, US President Trump has reiterated that he favors bilateral trade agreements, rather than multilateral arrangements. If Trump applies this stance to relations with Canada and Mexico, NAFTA could be in trouble, and this could bode badly for the Canadian dollar.

Oil remains near 2 year highs and is trading near $56.64 on Monday. The price of West Texas Intermediate varied throughout the day but settled when the Organization of the Petroleum Exporting Countries (OPEC) raised its energy demand forecasts. The production cut agreement by the organization and other major producers has been a huge factor in the stability of energy prices in the last two years, and with an extension in the works the market has reacted to lower supplies being added.

Oil prices have also risen after the events in Saudi Arabia, where Crown Prince Mohammed bin Salman has put corruption charges against influential princes and tycoons in his effort to reform the Kingdom away from oil revenues.

The Iran/Saudi Arabia conflict is expected to escalate after an attack in Bahrain was attributed to Iran with Saudi facilities enhancing security. Mohammed bin Salman has been a vocal critic of Iran and has already put an economic embargo on Qatar for its ties to Iran.

The rise of oil rigs in the US is keeping the price of energy from getting too high with two increases in three weeks as the US shale industry recovers from weather related disruptions and ramps up production. The risk of the OPEC production cut is that the Brazil, Canada and the US can increase their activity as they are not bound by any agreement.

Market events to watch this week:

Monday, November 13

9:00pm CNY Industrial Production y/y

Tuesday, November 14

4:30am GBP CPI y/y

8:30am USD PPI m/m

Wednesday, November 15

4:30am GBP Average Earnings Index 3m/y

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

8:30am 10:30am USD Crude Oil Inventories

7:30pm AUD Employment Change

Thursday, November 16

4:30am GBP Retail Sales m/m

8:30am USD Unemployment Claims

Friday, November 17

8:30am CAD CPI m/m

8:30am USD Building Permits

Gold Edges Higher, Markets Eye Tax Reform

Gold has started the week with slight gains. In Monday's North American trade, the spot price for an ounce of gold is $1278.37, up 0.23% on the day. On the release front, the only event is the Federal Budget Balance, with a deficit of $58.2 billion expected. On Tuesday, the US publishes Core CPI and CPI.

US consumer confidence levels remain high, but a key indicator lost ground in October. UoM Consumer Sentiment was unexpectedly soft on Friday, coming in at 97.8, missing the forecast of 100.8 points. Last week's unemployment claims were a disappointment at 239 thousand, climbing to a 4-week high. Investor sentiment will not fall after one soft employment report, but there are some concerns with the US labor market. Nonfarm payrolls rebounded in October with a gain of 261 thousand, after a rare decline a month earlier. Still, this reading was well off the forecast of 312 thousand. Wage growth remains a problem, reflective of chronically low inflation. In October, Average Hourly Earnings posted a flat 0.0%, the first time wages have not increased since November 2016.

Investors are keeping close eye on developments with President Trump's tax proposal. There are some differences in the House and Senate bills, with some Republicans opposed to eliminating federal deductions of state and local taxes. The Republicans hope to present Trump with a new tax code by the end of the year, but with Democrats putting up fierce resistance, it's unclear whether the bill will have enough votes to get through Congress. If the proposal is successful, the resulting economic growth could lead to higher interest rates, which would hurt gold prices.

Pound Slips as May’s Woes Worsen

The British has posted considerable losses in the Monday session. In North American trade, GBP/USD is trading at 1.3108, down 0.61% on the day. On the release front, British Rightmove HPI declined 0.8%, its third decline in four releases. In the US, the sole event is the Federal Budget Balance, with a deficit of $58.2 billion expected. On Tuesday, the UK releases a host of inflation indicators, led by CPI. The US will publish Core CPI and CPI.

The pound has started the week on a sour note, dropping close to the 1.31 level. Investors are wary as Prime Minister Theresa May is facing serious challenges. Two ministers have been forced to resign from May's cabinet in recent weeks, and Foreign Secretary Boris Johnson is been criticized for comments about a British national currently in detention in Iran. May appears to have lost control over her cabinet, with senior ministers openly attacking each other and questioning government policy. On Monday, British media reports said that 40 MPs have signed a letter of no confidence in May's leadership – a worrisome sign that her days at 10 Downing Street could be numbered.

The Brexit talks are moving slowly, and one major sticking point is the size of Britain's divorce bill. The European Union is demanding EUR 60 billion, while Britain has countered with an offer for EUR 20 billion. Britain wants to move on to discussing a trade deal with the continent, but the Europeans are insisting on more progress on the divorce bill as well as on other non-trade issues. If the sides still remain deadlocked in December without no deal in sight, hardliners on both sides could derail the talks completely, which would send shivers up the spines of investors and hurt the British pound. The Europeans are also wary about the ability of Theresa May to deliver the goods, given her continuing struggles at home. Two ministers have been forced to resign from May's cabinet in recent weeks, and May hasn't been able to present a coherent Brexit policy to the Europeans or to the voters at home, further eroding confidence in her leadership.

UK Inflation Spike Could Put Carney’s Hand on Paper and Push Pound Higher

Following encouraging evidence on Britain's industrial output on Friday, the upcoming data on consumer prices on Tuesday are expected to show that British inflation continues to grow above the BOE's target and likely pushing the pound higher. However, inflation drivers are not demand-led but a result of exchange rate weakness, challenging the BOE Governor, Mark Carney, who will be forced to write a letter to the chancellor, Philip Hammond, in case readings appear higher than the upper band of 3.0%, explaining what went wrong in constraining inflation.

Analysts project headline CPI to rise by 0.1 percentage points to 3.1% y/y in October, while the monthly gauge is expected to slow down from 0.3% to 0.2%. Excluding food and energy, the core CPI is forecasted to pick up by 2.8% y/y compared to the 2.7% seen previously. In September, inflation matched expectations, touching a five year high of 3.0% y/y as increases in energy prices and the currency's depreciation since the Brexit vote in 2016 has lifted import prices. In addition, insufficient progress in Brexit negotiations has restricted investment activities as business leaders lack clarity on how and under what conditions their operations will run despite the UK Prime Minister, Theresa May, pledging to arrange a transitional period of two years.

With global demand supporting net trade, consumers' confidence remaining resilient and amid a tightened labour market, the BOE decided to raise interest rates after a decade by a percentage quarter to 0.50% to return inflation back to the target despite sluggish wage growth and Brexit uncertainties lingering in the background. Moreover, the MPC members flagged that two additional quarter of a percentage point rate increases would be needed over the next two years, highlighting that any future rate hikes will be "gradual and to a limited extent". Yet, markets considered the statement as a dovish message, driving the pound lower following the monetary policy statement.

Should headline inflation indeed surprise to the upside on Tuesday, pound/dollar, which has been moving sideways between 1.3024 and 1.3336 since the beginning of October, might target the area around the 50-day simple moving average (1.3247).

Alternatively, weaker-than-expected readings could fully reverse the uptrend from 1.2770 to 1.3656 (August 24 – September 20), shifting the focus to the lower band of the range, a level which has been repeatedly tested in the past.

Following the data, a speech given by the BOE Governor, Mark Carney at a policy panel organized by the ECB in Frankfurt could also bring some volatility to the market.

Sterling Performs Worst Among Majors on Added Cloud of Uncertainty; Dollar Higher

In the absence of major economic releases during today's European session trading, forex markets were focused on upcoming data, a central banking conference set to take place tomorrow and developments on the political front, in particular Brexit and the US tax reform. Sterling was the worst performing major currency.

The dollar's index against a basket of currencies was 0.1% higher at 1520 GMT. On Friday, it hit 94.26, its lowest since October 26 as developments on the US tax front failed to please market participants. Beyond the tax story, Tuesday's producer prices and Wednesday's inflation and retail sales figures (all for the month of October) will be gathering attention in the US. Rising yields have provided some support to the greenback. The 10-year Treasury yield last stood at 2.39%. Last week, it fell to 2.30% at its lowest, a level not seen since October 19.

Dollar/yen was flat at 113.52, standing at a distance from last Monday's eight-month high of 114.72. Euro/dollar traded marginally higher at 1.1667. The pair rose in the three preceding trading days.

The ECB will tomorrow be hosting a central banking conference in Frankfurt. ECB President Mario Draghi, Fed Chair Janet Yellen, BoJ Governor Haruhiko Kuroda and BoE Governor Mark Carney will be participating in a panel discussion titled "At the heart of policy: challenges and opportunities of central bank communication". The discussion is scheduled to take place at 1000 GMT.

The Sunday Times reported over the weekend that 40 Conservative MPs have agreed to sign a letter of no-confidence in Prime Minister Theresa May. This is eight short of the number needed for a party leadership contest which would put May's position as prime minister in doubt. This latest news comes after the recent resignations of Priti Patel and Michael Fallon, which were seen as weakening May's government and further add to political uncertainty in the UK at a time when Brexit negotiations are at a focal point. Adding to this, foreign secretary Boris Johnson and environment secretary Michael Gove seem to have sent a joint private letter to May, urging her to push towards the direction of a "hard" Brexit. Their action was met with bitterness by those advocating a "soft" Brexit deal with the EU.

Pound/dollar was 0.6% lower at 1.3108. At its lowest it touched 1.3060, a level not experienced since November 6. Sterling was also weaker versus the euro with euro/pound last up by 0.6% and eyeing the 0.89 handle. At its highest the pair reached 0.8923, this being a 10-day peak. The British currency was notably down relative to the yen as well, with pound/yen last trading down by 0.6% at 148.88 after recording a more than three-week low of 148.04 earlier in the day.

Commodity-linked currencies, including the loonie, aussie and the kiwi all lost ground relative to the greenback: dollar/loonie was higher by 0.3% at 1.2715, aussie/dollar was lower by 0.3% at 0.7641 and kiwi/dollar down by 0.35% at 0.6904.

In commodities, gold traded higher by 0.1% at $1,277.87 an ounce. WTI was 0.2% up at $56.87 a barrel and Brent crude lower by 0.2% at $63.40 per barrel, both remaining close to last week's more than two-year high levels.

GBPJPY Retests Key Daily Cloud Top Support as Pound Comes Under Renewed Pressure

The cross probed again key supports at 148.17/22 (daily cloud top/asymmetric H&S neckline) on Monday after sterling came under pressure on concerns about Brexit negotiations and political strength of UK PM Theresa May.

Renewed bearish pressure after bullish end on Friday turned near-term bias with bulls again with main risk on sustained break below 148.17/22 pivots which could trigger significant downside. Bearish scenario would expose 147.77/67 (17 Oct trough/Fibo 38.2% of 139.30/152.85 ascend) with extension lower to look for test of next key point at 146.93 (09 Oct higher low). Meanwhile, the cross may show further hesitation ahead of key supports as today's downside rejection is the third straight in past few sessions. Converged 20/10SMA's offers solid barriers at 149.53/71 respectively which are expected to limit recovery attempts.

Res: 149.44; 149.53; 149.71; 150.00

Sup: 148.44; 148.17; 147.67; 146.93

USDCAD – Reversal Pattern is Forming on Daily Chart

The pair bounced above 1.2700 handle on Monday and signaling reversal after pullback from 1.2916 peak found footstep at 1.2665 where daily Kijun-sen contained dip. Morning Doji star is forming on daily chart as recovery rally surged through thick hourly cloud (1.2689 / 1.2707) with next barrier at 1.2724 (Fibo 23.6% of 1.2914/1.2665 pullback) coming under pressure. Near-term techs turned into bullish setup and support further advance which may extend towards next pivotal barrier at 1.2760 (Fibo 38.2% of 1.2914/1.2665). Broken 20SMA/hourly cloud top offer immediate support at 1.2705, with cloud base marking lower pivot (1.2689) loss of which will soften near-term structure and risk retest of key 1.2665 support.

Res: 1.2740; 1.2760; 1.2790; 1.2819

Sup: 1.2705; 1.2689; 1.2665; 1.2628