Sample Category Title

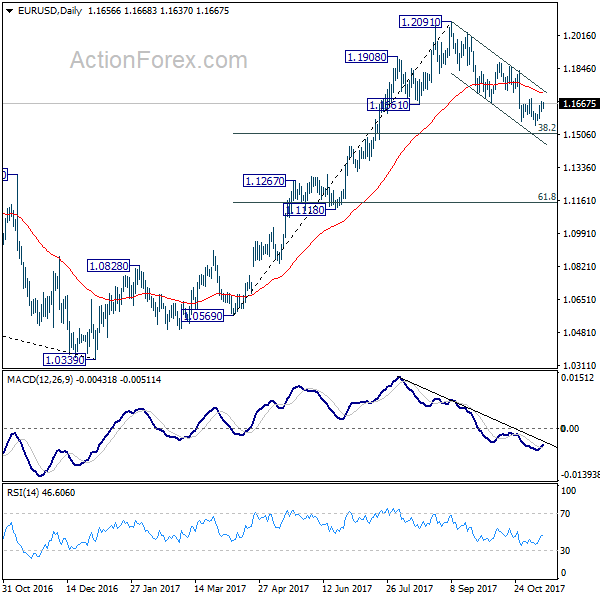

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1630; (P) 1.1654 (R1) 1.1685; More...

EUR/USD is still staying below 1.1689 resistance and intraday bias remains neutral. As long as 1.1689 resistance holds, deeper decline is in favor. Below 1.1553 will resume whole fall from 1.2091 and target 38.2% retracement of 1.0569 to 1.2091 at 1.1510. We'd be cautious on strong support from there to bring rebound. But sustained break of 1.1510 will pave the way to next support zone at 1.1118/1267. On the upside, break of 1.1689 resistance will now indicate short term bottoming and turn bias back to the upside for 1.1836 resistance instead.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1346) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

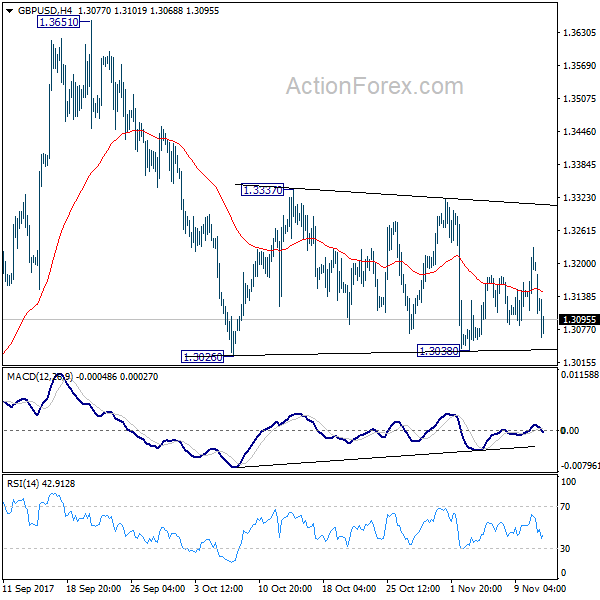

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3124; (P) 1.3177; (R1) 1.3241; More....

At this point, GBP/USD is still holding above 1.3038 support and bounded in established range. Intraday bias remains neutral first. In case of another recovery, upside should bel limited below 1.3337 resistance to bring fall resumption. Break of 1.3038 will now resume decline from 1.3651 to 1.2773 key support level. However, decisive break of 1.3337 will indicate that pull back from 1.3651 is completed and medium term rise from 1.1946 is resuming.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Sterling Stays Weak on Political Turmoil, Central Bankers Dominate Slow Day

Sterling continues to trade as the weakest currency on political turmoils in UK. But so far, downside is limited. GBP/USD is holding above 1.3038 near term support. EUR/GBP below 0.9032 near term resistance. These two pairs are regarded as staying in sideway consolidation. More notable movement is seen in GBP/JPY. While GBP/JPY is also staying in range of 146.92/151.92, the break of 148.42 minor support now suggests fall from September high at 152.82 is ready to resume. Elsewhere, Yen and Swiss Franc are trading broadly higher on risk aversion. The economic calendar is light today but dominated by central bankers' comments. Many important data, including inflation, growth and sentiments, will be released around the world in the days ahead.

BoE Haldane: Inflation to stay above target for the next few years

BoE chief economist Andy Haldane warned in a blog post published today that "price rises across the whole economy are currently running well above the 2 percent inflation target and are expected to remain above-target for the next few years." And, he added that the rate hike by BoE earlier this month was just "small adjustments". And the move is "unlikely to have a significant impact" on people's lives. Meanwhile, he also noted that "the rise in inflation through this year has already generated such a squeeze on many households' purchasing power." And, "this is not something the bank, or anyone else, should wish to see continuing for years to come - hence the nudge up in interest rates."

40 Conservatives MPs ready to channel PM May

It's reported that the Conservatives are getting more impatient with Prime Minister Theresa May. And, up to 40 Conservative MPs are ready to challenge May's leadership by signing a letter of no confidence. If eight more MPs are going to join, the letter would trigger a vote of no confidence, which could eventually leader to a leadership contest. Situation for May worsened sharply since the shambolic Conservative conference speech. And the list against her grew week by week after loss of Michael Fallon and Priti Patel in the cabinet.

Brexit Davis warned EU: No number or formula on divorce bill

Regarding Brexit negotiations with EU, Brexit Secretary David Davis dismissed the two-week deadline set of EU's chief negotiator Michel Barnier. Davis said that "in every negotiation each side tries to control the timetable. The real deadline on this, of course, is December. It's the December council. One of the key sticky point of the negotiation is that according to EU, "sufficient progress" is needed before moving on to the next stage in trade agreement talks. The divorce bill has to be settled before calling the progress "sufficient". But Davis said that the EU "invented this phrase" and "it's in their control what it really is". Also, he warned EU that "you won't have a number or a formula before we move on to the next stage".

ECB Constancio: Positive developments should not lead to complacency.

ECB Vice President Vitor Constancio warned today that "positive developments should not lead to complacency." He pointed out that "inflation, which is the core of our mandate, is still below our target after four years of growth supposedly above potential." And, he emphasized that "we are not yet fulfilling our mandate and that is why monetary policy will have to continue to be very accommodative, assuring favorable financial conditions to foster growth and spur wages and prices,

Fed Harker: "Lightly penciled in" a December rate hike

Philadelphia Fed Patrick Harker said today that he has "lightly penciled in" a December rate hike. He noted in Tokyo that "removing accommodation is the right next step". He forecast that unemployment will "drop below 4% probably late 2018 or early 2019". And that should "p[ut pressure on wages", thus, lift inflation back to target. But he emphasized the word "should" as "we've been predicting this for a while and it hasn't happened".

BoJ Nakata: Fed policies have no direct linkage to Japan

BoJ International Department Director-General Yoshinori Nakata said today that Fed's monetary policies will not have direct linkage to BoJ's. In particular, he noted that "we're confident the Fed will steer the U.S. economy and financial conditions in a correct, positive way so that global spillovers would be quite minimal."

RBA Debelle: Solid upward trajectory in non-mining business investment

RBA Deputy Governor Guy Debelle said "there has been a solid upward trajectory in non-mining business investment over the past couple of years." Also, there is starting to be a "change in mindset from the corporate sector around the willingness to invest, around the willingness to hire." And, that "gives you some hope that eventually we might get into a world where we start to see those wage price pressures emerge." But he also reiterated the central bank's stance to stand pat until upward pressure in wages or inflation starts to emerge.

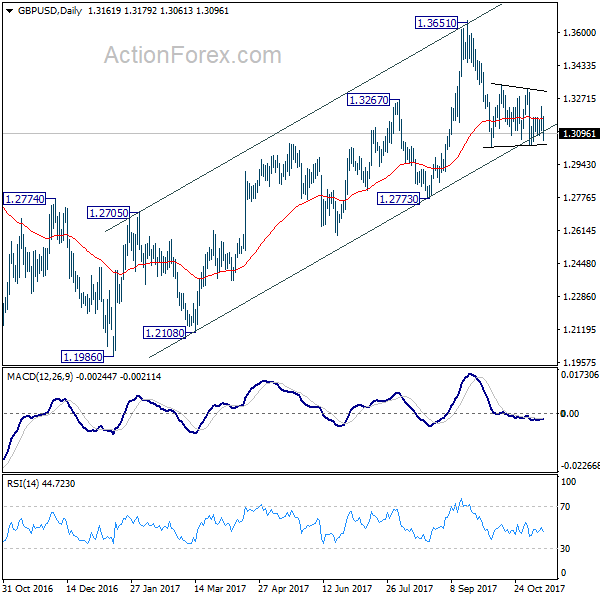

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3124; (P) 1.3177; (R1) 1.3241; More....

At this point, GBP/USD is still holding above 1.3038 support and bounded in established range. Intraday bias remains neutral first. In case of another recovery, upside should bel limited below 1.3337 resistance to bring fall resumption. Break of 1.3038 will now resume decline from 1.3651 to 1.2773 key support level. However, decisive break of 1.3337 will indicate that pull back from 1.3651 is completed and medium term rise from 1.1946 is resuming.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Oct | 3.40% | 3.10% | 3.00% | 3.10% |

| 0:01 | GBP | Rightmove House Prices M/M Nov | -0.80% | 1.10% | ||

| 6:00 | JPY | Machine Tool Orders Y/Y Oct P | 49.90% | 45.00% | ||

| 7:00 | EUR | German Wholesale Price Index M/M Oct | 0.00% | 0.40% | 0.60% | |

| 19:00 | USD | Monthly Budget Statement Oct | -58.2B | 8.0B |

Vicious Cycle For The Yen?

Japan: BoJ Governor Kuroda to speak in Zurich

Kuroda, the Bank of Japan Governor, is set to speak today in Zurich. Each one of its intervention are well regarded by financial markets. Indeed, it is still very interesting to know how he will address the lack of inflation in one decade. The truth is that strategy remains absolutely the same and can be sum-up in two words: all-in.

On the data side, the recent the PPI – Producer Price Index - for October has increased 3.4% y/y from 3.1% and September data has been revised up to 3.1%. GDP for Q3 is expected tomorrow and is nonetheless expected lower than Q2 04 q/q versus 0.6 q/q.

We consider that the due to the amount of money injected in the market, this should translate at some point in inflation. And this inflation is highly needed to kill the debt that was first needed to create… inflation. Then it is very easy to imagine than Japanese central bankers hope that inflation will soon run and kill the massive debt which currently represents officially 250% of the GDP.

Inflation data such as the National CPI is on the rise for last data available, in September with 0.7% y/y. Tokyo CPI excluding fresh foods in also on a growing momentum. And retail sales increase as well. In other words the demand for good increase. We may be at the inflection point for Japan. Only time will tell. But from a virtuous circle to a vicious circle, the border is very thin.

Bankfurt summit to boost USD

Tomorrow will see central banking's heavy hitters up to bat in Frankfurt. Janet Yellen of the US Federal Reserve, Mario Draghi of the European Central Bank, Mark Carney of the Bank of England and Haruhiko Kuroda of the Bank of Japan are scheduled to address ‘communication challenges' at a conference held at the ECB's headquarters. We think the upshot will be a bullish outlook for the USD, based on policy divergence and yield steepening. A low-yielding G10 and high-beta emerging market currencies look especially exposed.

Central bank guidance is as clear as mud. Economic outlook remains positive: favourable macro conditions with subdued inflation suggest that tightening money won't happen yet except in the USA, which likely has an increase coming in December. Yellen and her successor Jerome Powell must remain ahead of the inflation curve. Meanwhile, headlines over a struggling US tax plan will likely weigh on stocks and negatively affect sentiment on the dollar.

Pound Plummets On U.K Political Woes

Monday November 13: Five things the markets are talking about

After a quiet week on the economic front, the pace of fundamental releases picks up this week.

Japan, the Eurozone and Germany will release preliminary Q3 GDP.

In the U.K, British assets are expected to be in for a choppy ride as key consumer and producer price data along with the latest data on the labor market and retail sales tops the agenda, as too does a threat to PM May's leadership.

Stateside, U.S inflation and growth numbers will take priority, as they could be key to the Fed's determination to hike rates in December. Talks on tax legislation will also be playing into market thinking.

From China, a raft of closely watched economic releases is due this evening, including industrial production, fixed-asset investment and retail sales.

1. Stocks mixed results

In Japan, the Nikkei dropped to a two-week low overnight as many sectors weakened after recent rallies, offsetting gains in companies with strong results. The Nikkei ended -1.3% lower, the lowest closing level since Oct. 31 and its fourth straight daily decline. The broader Topix dropped -0.9%.

Down-under, gains by mining stocks weren't enough to offset two of Australia's big banks trading ex-dividend as the S&P/ASX 200 fell -0.1% following a choppy overnight session. In South Korea, the Kospi index was down -0.5%.

In Hong Kong, stocks rose slightly overnight, reflecting general market caution as investors wait for details on whether U.S Republicans could pass a tax reform deal quickly. The Hang Seng index added +0.2%, while the Hong Kong China Enterprises Index lost -0.5%.

In China, stocks extended their climb, powered by banks on financial deregulation. The blue-chip CSI300 index rose +0.4%, while the Shanghai Composite Index also gained +0.4%.

In Europe, regional indices are giving up most of their early with U.S tax reform uncertainty as well a question over the U.K PM May's leadership weighing on stocks.

U.S stocks are set to open unchanged.

Indices: Stoxx600 -0.4% at 387.3, FTSE +0.2% at 7449, DAX -0.1% at 13111, CAC-40 +0.3% at 5368, IBEX-35 -0.2% at 10075, FTSE MIB -0.5% at 22436, SMI +0.3% at 9165, S&P 500 Futures flat

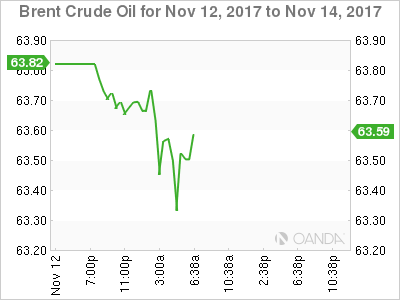

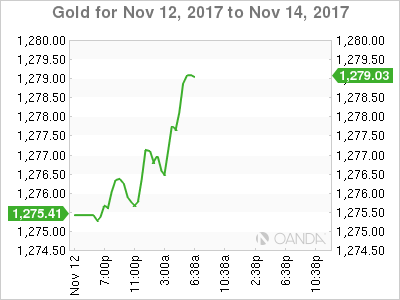

2. Oil markets cautious on Middle East tensions, gold lower

Oil trading remains cautious amid ongoing tensions in the Middle East and after a rising rig count in the U.S suggested producers there are preparing to increase output.

Brent crude futures are at +$63.57 per barrel, up +5c from Friday's close. U.S West Texas Intermediate (WTI) crude is at +$56.78 per barrel, up +4c.

Crude prices have generally being well supported as ongoing output cuts led by the OPEC and Russia have contributed to a significant reduction in excess supplies that have been pressuring markets over the past three-years.

On the supply side, tensions in the Middle East is raising the prospects of disruptions, along with yesterday's strong earthquake that hit Iran and Iraq – the market is still accessing the impact on the region's oil production.

Last week, U.S drillers added nine oilrigs in the week to Nov. 10, the biggest jump since June, bringing the total count up to 738 according to Baker Hughes.

Gold prices continue to drift in a narrow range overnight, but held near the previous session's low, pressured by a firmer dollar and expectations of a series of interest rate hikes by the Fed. Spot gold is nearly unchanged at +$1,276.61 per ounce.

Note: On Friday, gold dropped -0.7% for its biggest intraday percentage fall since Oct. 26, weighed down by a rise in U.S. Treasury bond yields.

3. Sovereign yield curves flatten

Eurozone bond yields have slipped from recent highs this morning, but are to be tested this week by a series of government bond sales, starting with today's Italian auction.

Yields across the region rallied towards the end of last week, triggered by a large seller of Bund futures on Thursday. This curbed a rally that began after the ECB's October policy meeting, when it extended its bond-buying scheme until at least September 2018.

Note: More than €30B EUR's of new bonds are set to enter the market this week.

Stateside, uncertainty around tax reforms in the U.S pushed Treasury yields higher on Friday. This week's U.S inflation numbers are expected to move markets again, as investors look for clues on future Fed rate increases.

The yield on U.S 10-years has declined -3 bps to +2.37%, the largest drop in more than a week. In Germany, the 10-year Bund yield fell -2 bps to +0.39%, the biggest fall in a week, while in the U.K, the 10-year Gilt yield fell -4 bps to +1.305%, the largest drop in more than a week.

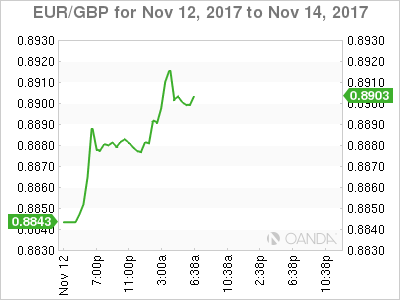

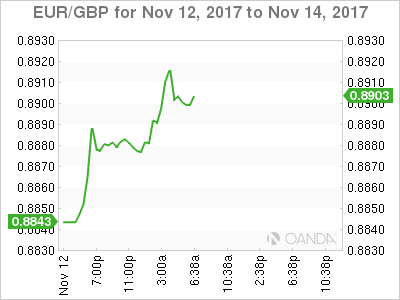

4. Sterling folds under political pressure

The pound (£1.3083) starts the week under pressure as 40 MP's supposedly have agreed to sign a letter of ‘no confidence' in PM May's leadership.

Note: Only eight more MP's are required to start a formal leadership challenge.

Any U.K political turmoil is likely to dent any clarity on Brexit negotiations. Tech analysts note that a break below £1.30 would suggest more downside momentum. EUR/GBP cross testing above the €0.89 level as a result.

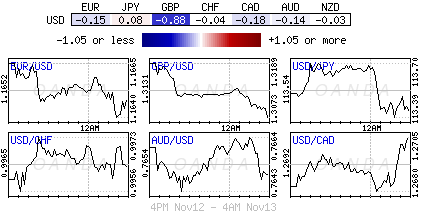

Elsewhere, the USD is trading somewhat mixed against G10 currency pairs. The EUR/USD is lower by -0.2% at €1.1640, USD/JPY remains little changed at ¥113.35.

5. Fed's Harker leaning toward an interest rate hike

Federal Reserve Bank of Philadelphia President Patrick Harker said overnight that he is still leaning toward supporting an interest-rate increase at next month's Fed meeting.

Fed Harker stated “pressing forward with rate rises and reducing the balance sheet is the right path for the Fed” and that he still “has another +25 bps rate increase penciled in for this year, although perhaps I should say, lightly penciled in.”

Note: Strong job growth and solid activity gains support the case for a rate increase, but weak price pressures complicate the outlook, and some believe boosting the cost of short-term borrowing is a mistake in the current environment.

Euro Inches Lower, German And Eurozone GDP Reports Next

The euro has started the trading week quietly. Currently, EUR/USD is trading at 1.1648, down 0.19% on the day. In economic news, there are no major German or Eurozone indicators. German Wholesale Price Index slowed to 0.0%, missing the forecast of 0.4%. On Tuesday, Germany and the eurozone release GDP reports, and Germany will publish ZEW Economic Sentiment. As well, Mario Draghi and Janet Yellen will participate in a panel at an event organized by the ECB.

The ECB tends to move cautiously, and in October, the central bank finally tapered its stimulus program (QE), with a “less but longer” setup. Starting in January, the ECB will cut its monthly asset purchases from EUR 60 billion to 30 billion. However, QE is being extended until September 2018, as the Bank is weaning the eurozone off stimulus. With the eurozone economy exceeding expectations in 2017, some policymakers have expressed reservations about the gradual pace of trimming stimulus, arguing that the Bank should cut the asset purchases at a faster rate. Governing Council member Philip Lane, head of the Irish central bank, said last week that if inflation moves closer to 2 percent, the ECB should tighten at a faster pace. The heads of the German and Austrian central banks, who are also on the Governing Council, went even further, saying that the ECB should have indicated a clear intent to end asset purchases, rather than announce an extension. If eurozone indicators continue to point upwards, ECB President Mario Draghi will be under pressure to terminate QE before September, or lower the size of the asset purchases. If that happens, the euro could gain ground.

It’s report card time on Tuesday, as Germany and the eurozone release GDP reports for the third quarter. Both releases are forecast to show respectable gain of 0.6% percent. The German economy has looked sharp in 2017, buoyed by solid consumer demand and a strong global appetite for German products. Germany has been the locomotive for the euorozone, and boosted traditional laggards such as France and Spain. Geopolitical concerns such as Catalonia and Brexit have the potential to crash the party, but in the meantime, eurozone indicators have generally been pointing upwards.

Market Update – European Session: UK Leadership Continues To Be Questioned

Notes/Observations

UK Leadership continues to be questioned; GBP turbulence ahead as more members of Parliament want Prime Minister May to resign; could dent any clarity on Brexit negotiations

Overnight

Asia:

APEC summit statement: Agreed to address ‘unfair trade practices’; called for removal of ‘market distorting’ subsidies

Japan PM Abe: Agreed with China President Xi to deepen cooperation on response to North Korea. To hold Japan/China/South Korea summit at earliest possible date

Europe:

Reports that 40 MPs have agreed to sign a letter of no confidence in PM May, short of number required to force leadership vote (48 required)

EU Parliament President Tajani sees €60B Brexit bill (**Reminder: Renewed speculation that PM May was prepared to increase its offer for the financial settlement of Brexit divorce from £20B)

UK Brexit Min Davis: EU agreed that Britain would not have to give a figure for financial settlement as part of 1st phase of Brexit talks. PM May will be in her position “right through” Brexit (**Note: EU has said the UK needs to give its Brexit payment proposal within the next two weeks)

On Saturday, Nov 11th approx 750K Catalan Independence supporters marched in Barcelona to demand the release of separatist leaders from pre-trial detention (**Note: Spain govt said to be pushing for the release of 8 former Catalan govt officials and expects them to be freed in time to campaign in December’s elections)

Canadian ratings agency DBRS affirms Greece at CCC (high), with trend revised to Positive from Stable

Americas:

Fed's Harker (voter, hawk): Lightly penciled in Dec rate hike; Inflation weakness has been puzzling

Economic Data

(NL) Netherlands Sept Retail Sales Y/Y: 6.6 v 5.4% prior

(JP) Japan Oct Preliminary Machine Tool Orders Y/Y: 49.9% v 45.0% prior

(DE) Germany Oct Wholesale Price Index M/M: 0.0% v 0.6% prior; Y/Y: 3.0% v 3.4% prior

(SE) Sweden Oct PES Unemployment Rate: 3.9% v 4.0% prior

(TR) Turkey Sept Current Account: -$4.5B v -$4.1Be

(SE) Sweden Nov SEB Housing-Price Indicator: 11 v 50 prior

Fixed Income Issuance:

(DK) Denmark sold DKK7.84 in 3-month Bills; Yield: -0.670% v -0.650% prior; bid-to-cover: 1.23x v 1.89x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.4% at 387.3, FTSE +0.2% at 7449, DAX -0.1% at 13111, CAC-40 +0.3% at 5368, IBEX-35 -0.2% at 10075, FTSE MIB -0.5% at 22436, SMI +0.3% at 9165, S&P 500 Futures flat]

Market Focal Points/Key Themes:

European Indices are giving up most of the gains seen this morning with US tax reform uncertainty as well question over UK PM May's leadership weighing on stocks. The French CAC one of the leading decliners being weighed lower by EDF after cutting their 2018 EBITDA outlook. In other corporate news shares of Ultra Electronics trades sharply lower after cutting outlook and the immediate resignation of the CEO, while Ladbrokes Coral and Sonova decline after earnings.

Looking ahead notable earners include Tyson Foods and Aecom Tech.

Equities

Consumer discretionary [Ladbrokes Coral [LCL.UK] -1.5% (Earnings)]

Industrials: [Dragerwerk [DRW3.DE] -15% (Earnings)]

Financials: [Senior [SNR.UK] +1.2% (Trading update, contract win), Deutsche Pfandbriefbank [PBB.DE] -3.8% (Earnings)]

Technology: [Ultra Electronics [ULE.UK] -17% (Trading update, CEO resigns), Sonova Hlds [SOON.CH] -6.6% (Earnings)]

Energy: [EDF [EDF.FR] -8.5% (Cuts outlook)]

Real Estate: [Patrizia Immobilien [P1Z.DE] +7% (Earnings)]

Speakers

ECB's Constancio (Portugal): Policy will have to remain accommodative as mandate is not fulfilled; must be patient and persistent (in-line with Draghi press conference)

IMF: Emerging Europe should prepare for policy tightening as the European recovery was spilling over into the rest of the world

Chancellor Hammond reportedly weighing Stamp Duty cut for 1st time buyers

German Deputy Fin Min Steffen noted that Germany did not share criticism of ECB NPL guidance **Reminder: On Oct 4th ECB proposed new guidance for banks’ bad-loan provisioning (NPL) and would ask euro area banks to set aside more cash to cover bad loans from next year)

Poland Central Bank's Sura: March staff projections could be the turning point for rate outlook; would need to see if CPI is above target persistently. Would back a 2018 debate on rate hikes if CPI was above the 2.5% target. Labor market seen as main risk for rate policy

Turkey Central Bank (CBRT) commented on non-deliverable forwards and noted that it would not lose FX reserves due to NDF auctions

City of London Corporation: “Disorderly Brexit” is now seen as almost inevitable by the world’s biggest banks

BOJ board member Sato (dissenter): BOJ should be more flexible with 2% inflation target

OPEC Sec Gen Barkindo: Global production cuts are the only viable option to restore stability. Oil demand growth to stay above 1.5M bpd in 2017-18 period

UAE Oil Min Mazrouei: Potential for production cuts to be extended. No talks of letting production cuts expire in March

Oman Oil Min stated that he did not believe there would be deeper production cuts

Currencies

The GBP currency was under pressure as 40 MPs had agreed to sign a letter of no confidence PM May. Analysts noted that only eight more MPs were required to start a formal leadership challenge. GBP/USD off 0.7% in session and probing below 1.31 level as the political turmoil likely could dent any clarity on Brexit negotiations. Dealers noted that break below 1.30 would suggest more downside momentum. EUR/GBP cross testing above the 0.89 level as a result.

Overall the USD was mixed against the major pairs. EUR/USD lower by 0.2% at 1.1640 area while USD/JPY was little changed at 113.35

Fixed Income

Bund futures trade at 162.51 up 29 ticks, as Euro Finance Week conference begins in Frankfurt. Support lies at 162.00, followed by 161.50. Resistance stands initially at 163.51, followed by 164.25.

Gilt futures trade at 124.70 up 38 ticks as pressure mounts on UK Prime Minister May. Continued upside eyeing 125.75 then 126.47. Downside targets include 124.24 then 123.74.

Monday’s liquidity report showed Friday’s excess liquidity fell from €1.873 to €1.8595T and use of the marginal lending facility dropped to €118M from €532M

Corporate issuance saw primary market finish week with over $47.26B priced

Looking Ahead

(UK) Commons reconvenes after November Recess

(IT) Italy Debt Agency (Tesoro) to sell €4.5-6.0B in 2020, 2024 and 2033 BTPs

(MX) Mexico Oct ANTAD Same-Store Sales Y/Y: No est v 5.6% prior

05:25 (BR) Brazil Central Bank Weekly Economists Survey

05:30 (DE) Germany to sell €2.0B in 6-month BuBills

06:00 (IL) Israel Oct Trade Balance: No est v -$1.6B prior

06:00 (PT) Portugal Oct CPI M/M: No est v 0.9% prior; Y/Y: No est v 1.4% prior

06:00 (PT) Portugal Oct CPI EU Harmonized M/M: No est v 1.0% prior; Y/Y: No est v 1.6% prior

06:00 (IN) India announces details of upcoming bond sale (held on Fridays)

06:30 (TR) Turkey TCMB Survey of Expectations

06:30 (IS) Iceland to sell 6-month Bills

06:45 (US) Daily Libor Fixing

07:00 (IN) India Oct CPI Y/Y: 3.5%e v 3.3% prior

08:00 (PL) Poland Oct Final CPI M/M: No est v 0.5% prelim; Y/Y: No est v 2.1% prelim

08:00 (PL) Poland Sept Current Account: -€0.4Be v -€0.1B prior; Trade Balance: €0.4Be v €0.3B prior

08:00 (RU) Russia Q3 Advance GDP Y/Y: 2.0%e v 2.5% prior

08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming actions (Bills and bonds)

08:05 (UK) Baltic Dry Bulk Index

08:50 (FR) France Debt Agency (AFT) to sell combined €4.3-5.5B in 3-month, 6-month and 12-month Bills

09:30 (EU) ECB announces Covered-Bond Purchases

09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

11:30 (US) Treasuries to sell 3-Month and 6-Month Bills

12:45 (JP) BOJ Gov Kuroda in Zurich

14:00 (US) Oct Monthly Budget Statement: -$58.0Be v -$45.8B prior

16:00 (US) Weekly Crop Progress Report

USD/ZAR 1H Chart: Pair Points To Weakness

USD/ZAR is trading in an up-trend since mid-July; however, the pair has failed to form an ascending channel due to a diminishing trading range. Thus, an ascending wedge is a more accurate representation of its movement. Meanwhile, the US Dollar has managed to hold this pattern for the last two and a half months; thus, it is currently located at a 2017 high of 14.4393. As apparent on the chart, the pair has failed to reach the upside boundary of the aforementioned wedge for two weeks. This factor suggests that this pattern is unlikely to constrain the rate any longer. The subsequent movement therefore should be to the downside. During the following two weeks, the US Dollar might approach the upward-sloping trend-line circa 13.90/14.00—an area which is likewise reinforced by the monthly PP.

USD/NOK 1H Chart: Rate Stranded In Wedge

After reaching the 2016/2017 low of 7.7050 on September 8, USD/NOK started a period of recovery in an ascending channel. If looking at the current situation, the pair’s latest wave down began two weeks ago and it is gradually leading the US Dollar towards the bottom boundary of the previously-mentioned channel. This movement has been stranded in a falling wedge. From a theoretical point of view, all indications point to a soon breakout north. Given that the pair retraced from the 50.0% Fibo, the Greenback might still push slightly lower down to the 8.09 area where the 38.2% Fibo and the weekly S1 are located. However, the rate’s subsequent movement should be to the upside. Meanwhile, the steepness of the channel up is unlikely to hold for long now, and thus the pair could eventually break the bottom boundary of this pattern—most probably during next week. A medium-term upside target is expected to be the weekly R1 at 8.3168.

EUR/USD Analysis: Starts New Week Near 1.1660

Despite a positive perception of ideas expressed by the US President Donald Trump at the ASEAN summit the Dollar is continuing to lose value against the Euro in a one-week long ascending channel. Although the pattern is supported by the rising 55-, 100- and 200-hour SMAs, the upcoming rebound from the 23.6% Fibonacci retracement level at 1.1679 is likely to lead to breakout to the south. This assumption is additionally backed up by the average market sentiment, which is 63% bearish. Moreover, there is a need to take into account that today there are scheduled no fundamental events that might give the pair an impulse strong enough to bypass the above resistance, which has been managing to turnaround the rate for the last two weeks.