Sample Category Title

USD/CAD Canadian Dollar Flat Awaiting US Retail Sales And Inflation Data

The Canadian dollar was appreciating against the US dollar in Tuesday morning trading, only for the tables to be turned after the release of the Producer Price Index (PPI) in the United States. The price that producers pay rose higher than expected in October. The rise of inflation expectations did little for the USD against other currencies, specially the EUR with Europe posting strong GDP data earlier in the day. The loonie had no economic data to counter the rise in US producer prices and gave back the gains from earlier in the day. Near the close of trading the USD/CAD is back to where it all started and looking ahead at the release of the US retail sales and consumer price index (CPI) data on Wednesday.

The US Bureau of Labor Statistics will publish the change in consumer prices on Wednesday, November 15 at 8:30 am EST. At the same time the US Census Bureau will release the monthly retail sales data. Core inflation is forecasted to come in at 0.2 percent on a monthly basis adding up to a 1.7 percent year to year comparison. Core retail sales are expected to have gained 0.2 percent in October.

NAFTA negotiations will resume in Mexico City this week in what could prove a decisive meeting between Canada, Mexico and the United States. The US tax overhaul has stolen the spotlight and with two proposals ready to go the Trump Administration needs the support of the Republican party. Trade friendly republicans could negotiate their support for tax reforms if some progress is made on the NAFTA renegotiation. Canada launched a NAFTA challenge on the softwood lumber duties imposed by the US.

The USD/CAD was flat on Tuesday. The currency pair is trading at 1.2732 after the release of a positive PPI data beat expectations and validates the anticipated December rate hike by the U.S. Federal Reserve. The gap between the US and Canadian benchmark interest rates will grow as the Bank of Canada (BoC) has a lower probability of lifting interest rates than the US central bank.

The BoC has already hiked twice in 2017 after a hawkish turn in summer, only to pump the brakes before the end of year. The Canadian interest rate is 1.00 percent, back to its 2015 levels where the BoC cut twice to avoid a deeper impact of the fall in crude prices. The Fed has hike twice and is looking to finish the year with a 25 basis points raise in December.

NAFTA negotiations will weigh in the currency market as Canada export 75 percent of its production to the United States and the threat by President Trump to rip it in half could end up being more than hard negotiating tactics.

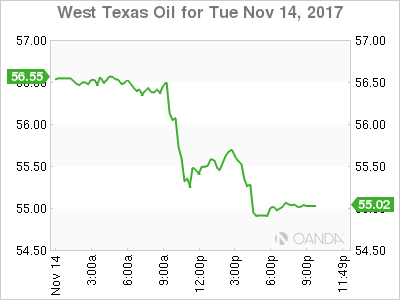

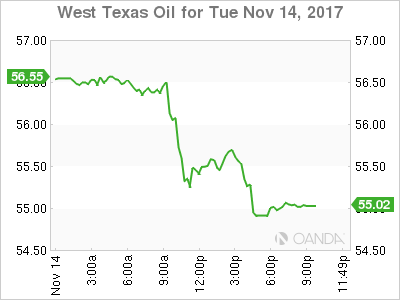

The price of crude fell 2 percent on Tuesday. West Texas Intermediate is trading at $55.54 after the International Energy Agency lowered its crude demand forecast and earlier weaker than expected economic data out of China gave credibility to the demand downgrade. Oil had risen after the arrest two weeks ago in Saudi Arabia and optimistic forecasts by the Organization of the Petroleum Exporting Countries (OPEC) as well as a pledge to extend its production cut agreement with other major producers.

The IEA cut its growth forecast by 100,000 daily barrels due to warmer weather and in contrast still sees some producers taking advantage of current prices to increase production levels. Brazil, Canada and the United States are big producers not part of the OPEC deal and are expected to ramp up their supply levels. Investors sold off crude positions on the back of the news and ahead of the weekly release of US crude inventories. After the surprise buildup last week, stocks are expected to show a 2.1 million barrel drawdown on Wednesday, at 10:30 am EST when the Energy Information Administration (EIA) releases the report.

Market events to watch this week:

Wednesday, November 15

4:30am GBP Average Earnings Index 3m/y

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

8:30am 10:30am USD Crude Oil Inventories

7:30pm AUD Employment Change

Thursday, November 16

4:30am GBP Retail Sales m/m

8:30am USD Unemployment Claims

Friday, November 17

8:30am CAD CPI m/m

8:30am USD Building Permits

US Dollar Stumbles Ahead Of Inflation And Retail Sales

German data surprise boosts EUR

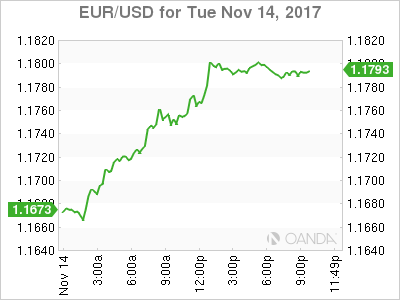

The US Dollar is trading lower against a mix of major currencies on Tuesday. Positive data out of Germany has boosted the single currency. The better than expected advance German gross domestic product (GDP) reading at 0.8 percent is further proof that the largest economy in the EU is firing in all cylinders. The Eurozone's GDP met the estimate at 0.6 percent with the market now awaiting inflation and retail sales data out of the United States.

The US Bureau of Labor Statistics will publish the change in consumer prices on Wednesday, November 15 at 8:30 am EST. At the same time the US Census Bureau will release the monthly retail sales data. Core inflation is forecasted to come in at 0.2 percent on a monthly basis adding up to a 1.7 percent year to year comparison. Core retail sales are expected to have gained 0.2 percent in October.

The EUR advanced more than 1 percent versus the USD even though the US Producer Price Index (PPI) released in the US beat expectations with a 0.4 gain in October. The rise in producer price inflation failed to spark a dollar recovery as the U.S. Federal Reserve December rate hike is already priced in, and the data just validates the telegraphed decision by the central bank.

The EUR/USD gained 1.07 percent on Tuesday. The single currency is trading at 1.1792 and threatening the 1.18 price level. The growth story in the EU pushed the EUR ahead of the USD. The eurozone could beat the US for the second time in a row driven by strong German GDP growth, but also a stable pace from the rest of the member states. The economic recovery hasn't convinced the European Central Bank (ECB) to fully remove its stimulus spending, but after announcing its tapering plans an end to negative rates could be close.

The US tax overhaul remains shrouded in uncertainty as the market digests the different versions and its impact on the economy. There is vote planned for Thursday by House Republicans with the idea that there will be two bills that could pass before they are reconciled. The year end deadline could be reached if this strategy is used as there is still plenty of resistance to some part of the tax proposals. The US senate would be ready to approve their version after US Thanksgiving.

The price of crude fell 2 percent on Tuesday. West Texas Intermediate is trading at $55.54 after the International Energy Agency lowered its crude demand forecast and earlier weaker than expected economic data out of China gave credibility to the demand downgrade. Oil had risen after the arrest two weeks ago in Saudi Arabia and optimistic forecasts by the Organization of the Petroleum Exporting Countries (OPEC) as well as a pledge to extend its production cut agreement with other major producers.

The IEA cut its growth forecast by 100,000 daily barrels due to warmer weather and in contrast still sees some producers taking advantage of current prices to increase production levels. Brazil, Canada and the United States are big producers not part of the OPEC deal and are expected to ramp up their supply levels. Investors sold off crude positions on the back of the news and ahead of the weekly release of US crude inventories. After the surprise buildup last week, stocks are expected to show a 2.1 million barrel drawdown on Wednesday, at 10:30 am EST when the Energy Information Administration (EIA) releases the report.

Market events to watch this week:

Wednesday, November 15

4:30am GBP Average Earnings Index 3m/y

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

8:30am 10:30am USD Crude Oil Inventories

7:30pm AUD Employment Change

Thursday, November 16

4:30am GBP Retail Sales m/m

8:30am USD Unemployment Claims

Friday, November 17

8:30am CAD CPI m/m

8:30am USD Building Permits

Pound Subdued as British CPI Unchanged at 3.0%

The British pound has ticked higher in the Tuesday session. In North American trade, GBP/USD is trading at 1.3121, up 0.04% on the day. On the release front, British CPI remained unchanged at 3.0%, just below the estimate of 3.1%. Other inflation indicators were also within expectations. In the US, inflation indicators were stronger than expected. PPI gained 0.4%, above the estimate of 0.1%, while Core PPI also came in at 0.4%, beating the forecast of 0.2%. There are a host of key events on Wednesday. The UK releases wage growth and Claimant Count Change, while the US will publish CPI and retail sales numbers.

The pound is under pressure this week, as the currency dipped below the 1.31 line on Monday and Tuesday. Investors are nervous as Prime Minister May's leadership is showing large cracks. Two ministers have been forced to resign from May's cabinet in recent weeks, and Foreign Secretary Boris Johnson has been heavily criticized for comments about a British citizen who is on trial in Iran. May appears to have lost control over her cabinet, with senior ministers openly attacking each other and questioning government policy. On Monday, British media reports said that 40 MPs have signed a letter of no confidence in May's leadership – a worrisome sign that her days at 10 Downing Street could be numbered.

The Brexit talks remain deadlocked, with large gaps between the sides, such as the size of Britain's divorce bill. Theresa May's woes at home haven't helped matters. Her cabinet remains divided on Brexit policy, with senior ministers quarreling in the open. May hasn't been able present a coherent Brexit policy to the Europeans or to the voters at home, raising doubts as to whether May can deliver the goods on Brexit. On Monday, Brexit Secretary David Davis said he would introduce legislation that would allow MPs to vote on the final Brexit deal, but lawmakers would not be able to amend the legislation. The UK is scheduled to leave the European Union in March 2019.

Euro Rises Amid Strong GDP Growth Figures from Germany

The EUR/USD price has shown a powerful upward movement due to uncertainty around planned tax reforms in the US going through and also thanks to strong macro statistics reported in the Eurozone. German GDP growth in the third quarter accelerated up to 0.8% which is 0.2% above the forecast. Germany is the largest economy not only in the Eurozone, but in the whole of Europe. At the same time, Italian GDP grew by 0.5% during the same period and the Eurozone's economy expanded by 0.6%, in line with the forecast.

Speeches by the heads of the central banks of the US, Eurozone, Japan and the UK had limited impact on the course of trading today. The focus of the market tomorrow will be on the consumer price index report in the US that traditionally has a significant impact on the future decisions of the FOMC on monetary policy settings.

The aussie price has resumed growing. The weakening of the greenback was able to offset the worse than anticipated statistics from China where industrial production growth slowed to 6.2% which is 0.1% short of the predicted figure. Today, the impact on the course of AUD/USD trading will come from the Westpac report on consumer sentiment in Australia at 23:30 GMT. Another important event today worth paying attention to is the GDP data release from Japan for the third quarter.

EUR/USD

The EUR/USD price started to grow after some consolidation above 1.1650. As a result, the quotes were able to pass through the resistance at 1.1730 and the upper limit of the descending channel. The next targets in case of further growth will be located at 1.1850 and 1.1925. The RSI on the 15-minute chart is in the overbought zone which points to a possible price rollback with potential target at 1.1700.

GBP/USD

The pound is consolidating today despite the publication of the consumer price index that remained at 3.0% in October which is 0.1% below the forecast. Slower than expected inflation will restrain the Bank of England from raising interest rates, especially on the background of week macro data in the UK. In case of breaking through the support at 1.3050, the next targets will be at 1.2950 and 1.2840. Growth today is likely to be limited by the resistance at 1.3150.

AUD/USD

The AUD/USD price has not been able to fix under the strong level of 0.7640 and the current upward impulse has broken through the upper limit of the local descending trend. This has become a basis for the bulls to push the price higher with potential goals at 0.7700 and 0.7740. The fall potential has reduced recently and it is restricted by the horizontal support line at 0.7600.

Euro Jumps to 3-Week High on Upbeat GDP; Pound Slips on Inflation Miss

The euro enjoyed its strongest daily gain in a month as upbeat GDP numbers out of Europe lifted sentiment for the region. The pound came under pressure though after UK inflation missed expectations, while the US dollar remained below session highs despite US producer prices rising more than anticipated.

Stronger-than-expected growth in Europe's largest economy during the third quarter set the tone for today's European session as investors were once again drawn to the improving outlook for the region. German GDP was up 0.8% between the second and third quarters, beating forecasts of 0.6% growth. The year-on-year rate was in line with estimates at 2.3%. Italian GDP also came in above expectations and strong growth in central and eastern European countries added to the overall positive tone, lifting the euro.

The single currency jumped to a near three-week high of $1.1764, and was last trading up 0.7% on the day at $1.1753. It was also up sharply against the yen and the pound at 133.45 and 0.8968 respectively.

The pound's losses were broad based as the British currency dipped after weaker-than-expected inflation data. Headline inflation in the UK was unchanged at 3.0% y/y in October, below forecasts that it would rise to 3.1%. Core CPI missed estimates too, coming in at 2.7%, the same rate as in September, instead of the expected 2.8%. Producer prices also rose less than expected, suggesting that inflation in the UK has peaked as the effects of last year's depreciation of the pound start to fade.

Sterling hovered around $1.31 after reclaiming the level yesterday. Its losses from the data were limited with traders cautious as British MPs began debating the EU Withdrawal Bill. The legislation is crucial to ensure a smooth transition after Brexit but with only a small working majority, the prime minister, Theresa May, could struggle to pass the bill as up to 10 Conservative MPs are reportedly planning to vote against it. The bill has a long way to go however with the parliamentary scrutiny expected to take weeks.

There was little reaction in forex markets to a panel discussion by the world's four most important central bank chiefs at an ECB conference in Frankfurt today. Fed Chair Janet Yellen, ECB President Mario Draghi, Bank of England Governor Mark Carney and Bank of Japan Governor Haruhiko Kuroda did not comment on monetary policy but defended their communications policy, with Draghi saying "Forward guidance has become a full-fledged monetary policy instrument". Draghi and Carney will be speaking again separately later in the week.

Fed speakers also failed to attract much attention. In an interview with the Financial Times, Dallas Fed President and voting FOMC member, Robert Kaplan, said he was "actively considering" supporting a rate hike in December. In contrast, St. Louis Fed President James Bullard, who does not get to vote until 2019, was typically dovish, saying current rates are likely to remain appropriate in the near term.

The greenback had a lacklustre session as the US currency retreated after briefly touching a high of 113.91 yen. Better-than-expected producer prices only managed to briefly halt the dollar's slide, with dollar/yen steadying around 113.50 before resuming downwards to hit an intra-day low of 113.31. Declining US treasury yields weighed on the dollar but boosted gold which spiked above $1280 an ounce.

US PPI for final demand rose by a bigger-than-forecast 0.4% month-on-month in October versus estimates of 0.1%. The annual rate accelerated to 5½-year high of 2.8% from 2.6% in September. The core rate also beat expectations, rising by 2.4% y/y instead of the anticipated 2.3%. Attention now shifts to tomorrow's CPI and retail sales figures.

In other currencies, the Australian and New Zealand dollars remained pressured against the greenback. The aussie was stuck near its earlier 4-month low of $0.7607, while the kiwi was on track for a fourth straight day of losses, hitting a 2-week low of $0.6843.

Bears Taking Over 10 Year US Notes and GBPUSD

Good day traders. Hope everybody is having a good time.

Todays focus is on the 10 Year US Notes and gbpusd.

10 Year Us notes are trading sharply lower, unfolding a nice impulsive structure, which we see it as sub-wave (1) and now upcoming wave (2). We know that wave (2) is a correction, which means a three-wave rally may unfold within it.

10 Year US Notes, 1H

GBPUSD

GBPUSD can be trading at the end of a corrective wave ii, which can see limited upside near the Fibonacci ratio of 61.8. From there price can sharply unfold lower into wave three.

Have a nice evening.

GBPUSD, 1H

WTI OIL – Fresh Bearish Acceleration Probes Below 10SMA

WTI oil was sharply lower in early US session as strong fall US stock indexes after Wall St opening inflated the dollar.

Fresh weakness probes through pivotal rising 10SMA support ($56.23), generating another bearish signal for reversal which was indicated by overextended daily studies. Close below 10SMA would trigger further easing and extend correction towards $54.53 (Fibo 38.2%/rising 20SMA).

Daily RSI emerged from overbought territory and is heading south, reinforcing negative signal.

Res: 56.75; 57.02; 57.51; 57.90

Sup: 55.82; 55.00; 54.53; 53.88

The Euro is Consolidating Under Fresh Three-Week High at 1.1764

The Euro was up 0.75% on Tuesday on strong bullish acceleration after solid EU data. The rally peaked at 1.1764, the highest since 26 Oct, denting Fibo 61.8% pivot at 1.1755 and shifting focus towards 55SMA (1.1796) and daily cloud base (1.1815). Bulls are taking a breather under 1.1764 high as better than expected US PPI data temporarily inflated the greenback. Pullback was so far shallow and holding well above initial support at 1.1731 (100SMA), keeping near-term bullish bias intact. We expect extended dips to remain above 1.1700 handle (ideally above rising 100SMA) before resuming higher. With no further data scheduled today, focus turns towards tomorrow's release of US CPI/Retail Sales which could influence Euro's near-term action.

Res: 1.1770; 1.1796; 1.1815; 1.1836

Sup: 1.1731; 1.1716; 1.1685; 1.1661

GBP/USD Fibonacci Confluence at D3 Camarilla

The GBP/USD is making a continuation trade possible with the consolidation below the D H3 camarilla pivot with strong fibonacci confluence. Session Recap webinar presented more than 50 pips on the table with the GBP/USD setup. At this point the POC zone ( 50.0 fib, D H3, EMA89, ATR pivot) 1.3125-1.3145 could reject the price towards 1.3080. If the price breaks 1.3080, further bearish momentum could target 1.3050, 1.3020 and 1.2995. For this scenario to succeed the price needs to stay below 1.3180.

- H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

- W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

- D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

- D L3 - Daily Camarilla Pivot (Daily Support)

- D L4 - Daily H4 Camarilla (Very Strong Daily Support)

- PPR - Progressive Polynomial Channel

- POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Yen Dips Lower as US Inflation Beats Estimate

USD/JPY has edged lower in the Tuesday session. In North American trade, USD/JPY is trading at 113.63, down 0.22% on the day. In the US, inflation indicators were stronger than expected. PPI gained 0.4%, above the estimate of 0.1%, while Core PPI also came in at 0.4%, beating the forecast of 0.2%.Later in the day, Japan releases Preliminary GDP, with an estimate of 0.4%.

US Producer Price Index reports were stronger than expected in October. Core PPI and PPI remained unchanged at 0.4%, beating their estimates. PPI increased at an annualized rate of 2.8%, its fast gain since February 2012. Is inflation on the rise? We could get an answer as early as Wednesday, with the release of CPI and Core CPI reports. Inflation levels are being closely monitored by the Federal Reserve, as stronger inflation levels would likely result in a rate hike in early 2018. The markets are very bullish on higher rates, with a December hike priced in at 91% and a January raise priced in at 89%.

Prime Minister Shinzo Abe cruised to victory in the October election, and is expected to maintain his 'Abenomics' economic program. The program is based on three prongs – ultra-loose monetary easing, fiscal spending and structural reforms to the economy. The scheme has been in place since 2012, and is finally showing some results, as the Japanese economy continues to expand. However, inflation remains stubbornly low, and a strong labor market has not led to higher wages, which would help boost inflation. Companies continue to look for ways to spend their cash, such as buying foreign companies, but are reluctant to plow more funds into wages. Business confidence in the economy remains lukewarm, and businesses are reluctant to add to their fixed costs. The BoJ has urged companies to increase wages, but this is unlikely to occur until the business sector is convinced that the current economic rebound will be long-lasting.