Sample Category Title

US: Inflationary Pressures Turn Sharply Gigher in January

The Consumer Price Index (CPI) rose 0.5% month-on-month (m/m) in January, an acceleration from December's 0.4% m/m gain. On a twelve-month basis, CPI was up 3.0% (from 2.9% in December).

- Energy prices rose 1.1% m/m, led by a further gain in gasoline prices (+1.8% m/m), though energy services (+0.3%m.m) were also higher. Food prices (+0.4% m/m) also came in on the hotter side – posting its largest monthly gain since February 2023.

Excluding food and energy, core inflation rose 0.4% m/m, ahead of the consensus and the strongest monthly gain since March 2024. The twelve-month ticked up to 3.3% (from 3.2% in December), while the three-month annualized rose to a nine-month high of 3.8%.

- The January release also included revised seasonal adjustment factors, through the impact on the monthly pattern for 2024 was relatively negligible.

- Moreover, the outsized gain in core inflation last month suggests that residual seasonality could still be a factor biasing the early-year readings of inflation higher.

Price growth on core services was up 0.5% m/m, or double the monthly gain recorded in December. On a year-ago basis, services prices remain at an elevated 4.3%.

- Primary shelter costs rose 0.3% m/m, slightly softer than the 0.4% m/m gain averaged over the prior twelve months. On a 12-month basis, shelter costs are up 4.5%.

- Non-housing services inflation (aka "supercore") accelerated sharply, rising 0.7% m/m or its strongest monthly gain since last January. Price gains were relatively broad based, with vehicle insurance (2.0% m/m), recreational services (+1.4% m/m) and travel costs (including airfares, car rentals and hotels) all recording sizeable gains last month.

Core goods prices also came in on the hotter side, rising 0.3% m/m, thanks to a further increase in used vehicle prices (+2.2% m/m), medical goods (+1.2% m/m), and recreational goods (+0.3% m/m).

Key Implications

This report is probably the last thing the Federal Reserve and new Administration wanted to see.

The first CPI reading for 2025 showed core inflation rising at its fastest pace in nearly a year, amid a further uptick in goods prices and ongoing stickiness in services inflation. In the best of case, it's chalked up to residual seasonality (i.e., the inability of seasonal adjustment factors to capture regular calendar moves) and some reversal shows up in the coming months. This effect was apparent in the January/February readings in each of the last two-years.

Following this morning's release, futures markets sold-off sharply while the 2-year Treasury yield was jolted higher by approximately 8 basis points to 4.37%. Fed futures have pushed out the timing of next rate cut to December (yesterday, September was fully priced).

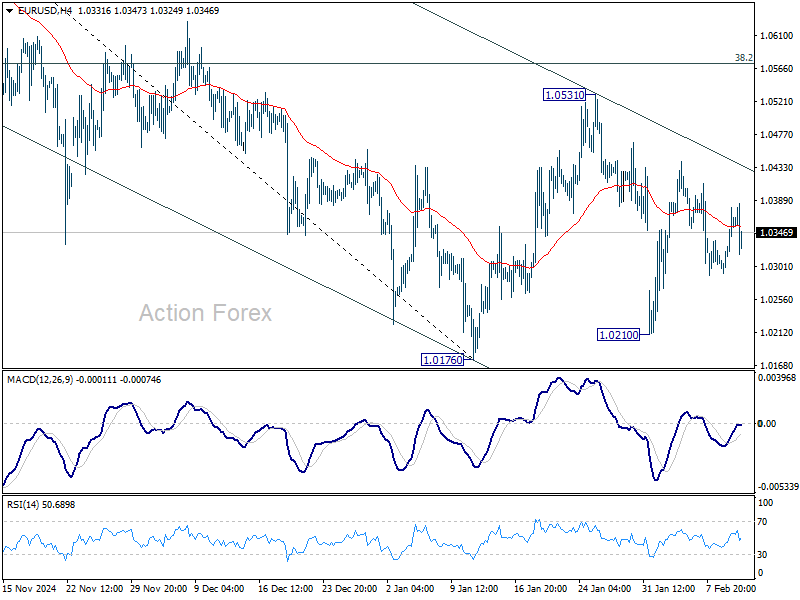

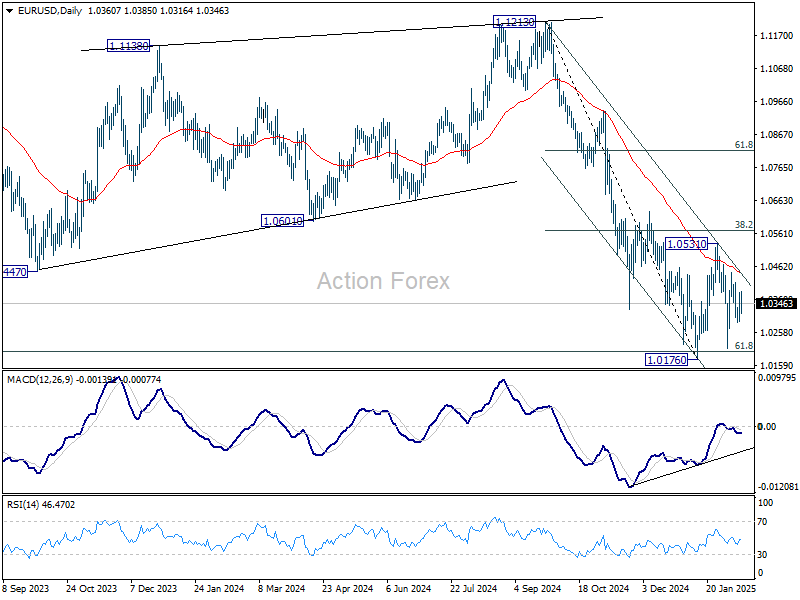

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0309; (P) 1.0345; (R1) 1.0398; More...

EUR/USD weakens mildly today but stays in range above 1.0176. Intraday bias remains neutral for the moment. Outlook will remain bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

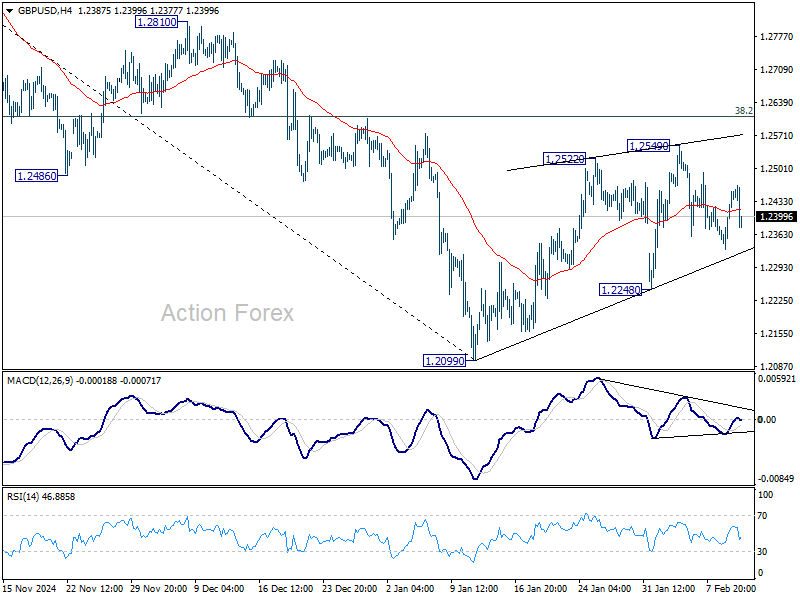

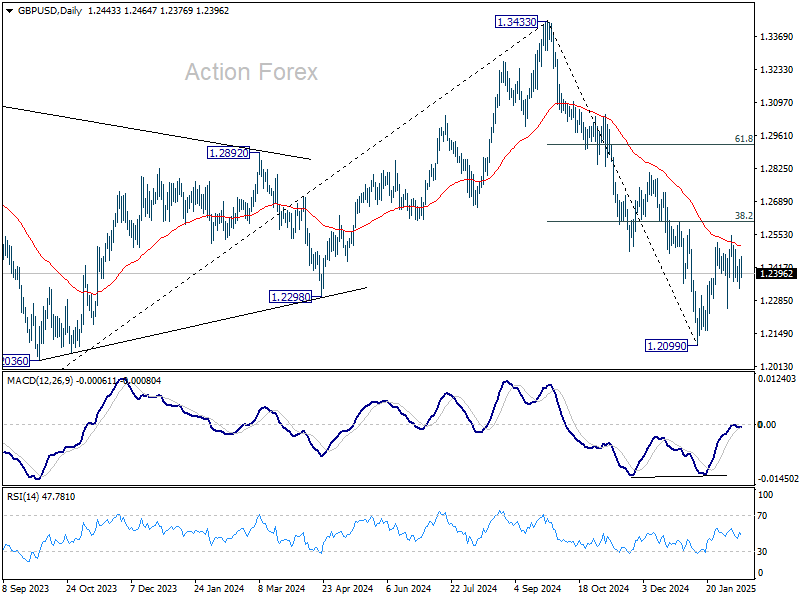

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2368; (P) 1.2411; (R1) 1.2491; More...

GBP/USD dips notably in early US session but stays above 1.2248 support. Intraday bias remains neutral at this point. Corrective pattern from 1.2099 could extend with another rebound. But upside should be limited by 38.2% retracement of 1.3433 to 1.2099 at 1.2609. On the downside, break of 1.2248 support will bring retest of 1.2099 low. Firm break there will resume whole fall from 1.3433. However, decisive break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

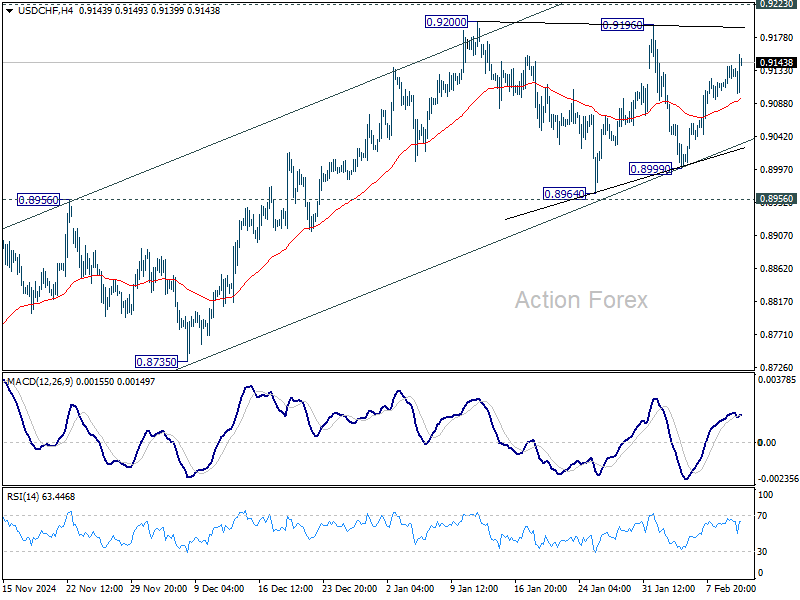

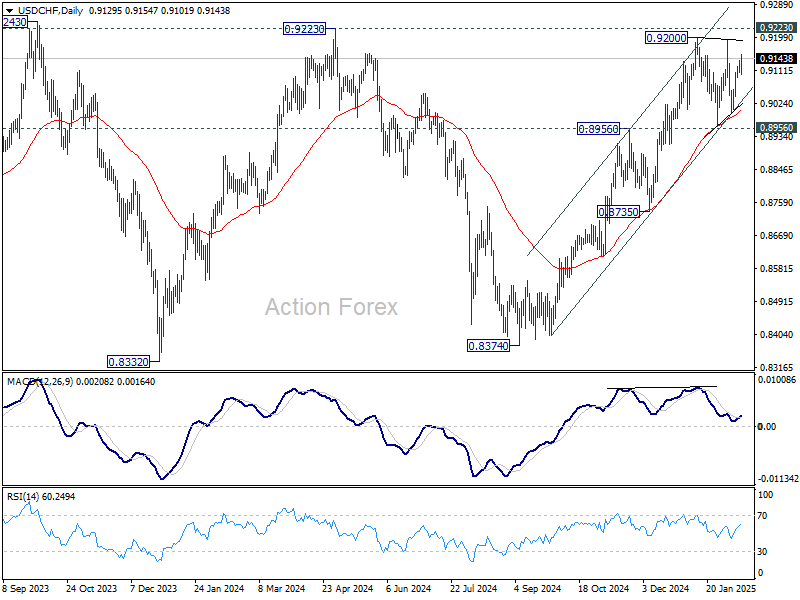

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9108; (P) 0.9126; (R1) 0.9150; More…

USD/CHF's rise from 0.8990 continues today but stays below 0.9200 resistance. Intraday bias remains neutral first. Outlook stays bullish with 0.8956/64 support zone intact. On the upside, firm break of 0.9200/9223 will resume the whole rally from 0.8374 and carry larger bullish implication. However, sustained break of 0.8964 will be a sign of reversal and turn bias back to the downside.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

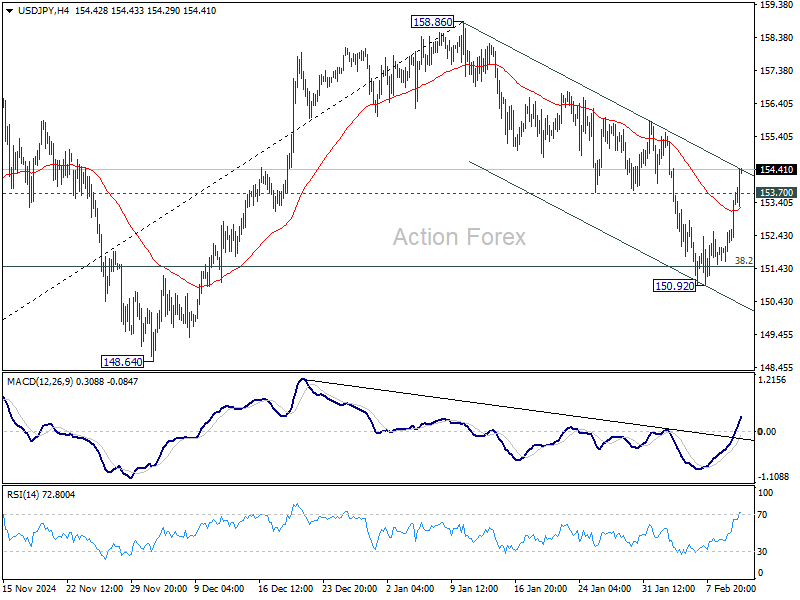

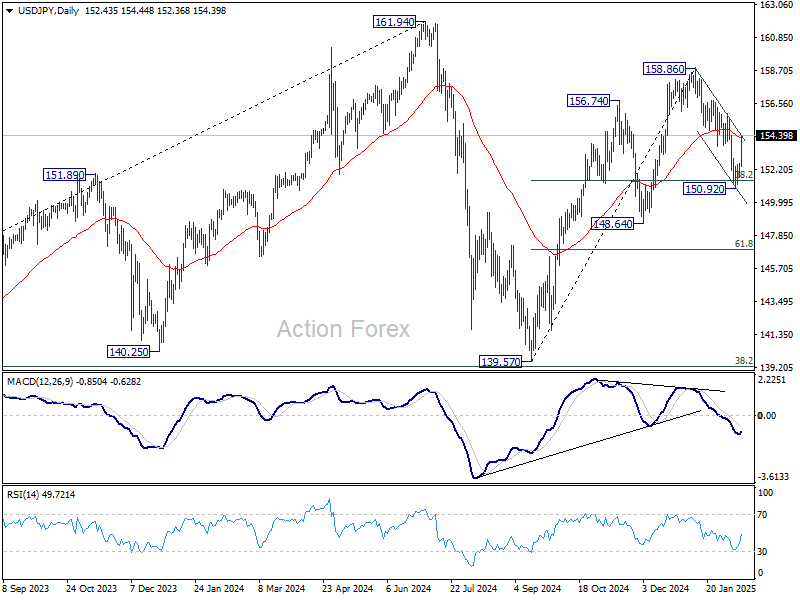

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.90; (P) 152.25; (R1) 152.86; More...

USD/JPY's strong break of 153.70 support turned resistance should confirm that corrective pull back from 158.86 has completed at 150.92. That came after drawing support from 38.2% retracement of 139.57 to 158.86 at 151.49. Intraday bias is back on the upside for retesting 158.86. Firm break there will resume whole rally from 139.57 to retest 161.94 high. For now, risk will stay on the upside as long as 150.92 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Dollar Surges as Hot Inflation Data Solidifies Prolonged Fed Pause, Yields Surge

Dollar rallied sharply in early US trading after inflation data came in hotter than expected, reinforcing expectations that Fed will maintain its restrictive policy stance for longer than previously anticipated. 10-year Treasury yield surged past 4.6%, extending its strong rebound from earlier in the week. US equity futures plunged, with DOW futures down around -1% as traders reassessed the likelihood of near-term rate cuts. The report shattered market hopes that the Fed might move forward with another rate cut by mid-year, instead strengthening the case for a prolonged pause.

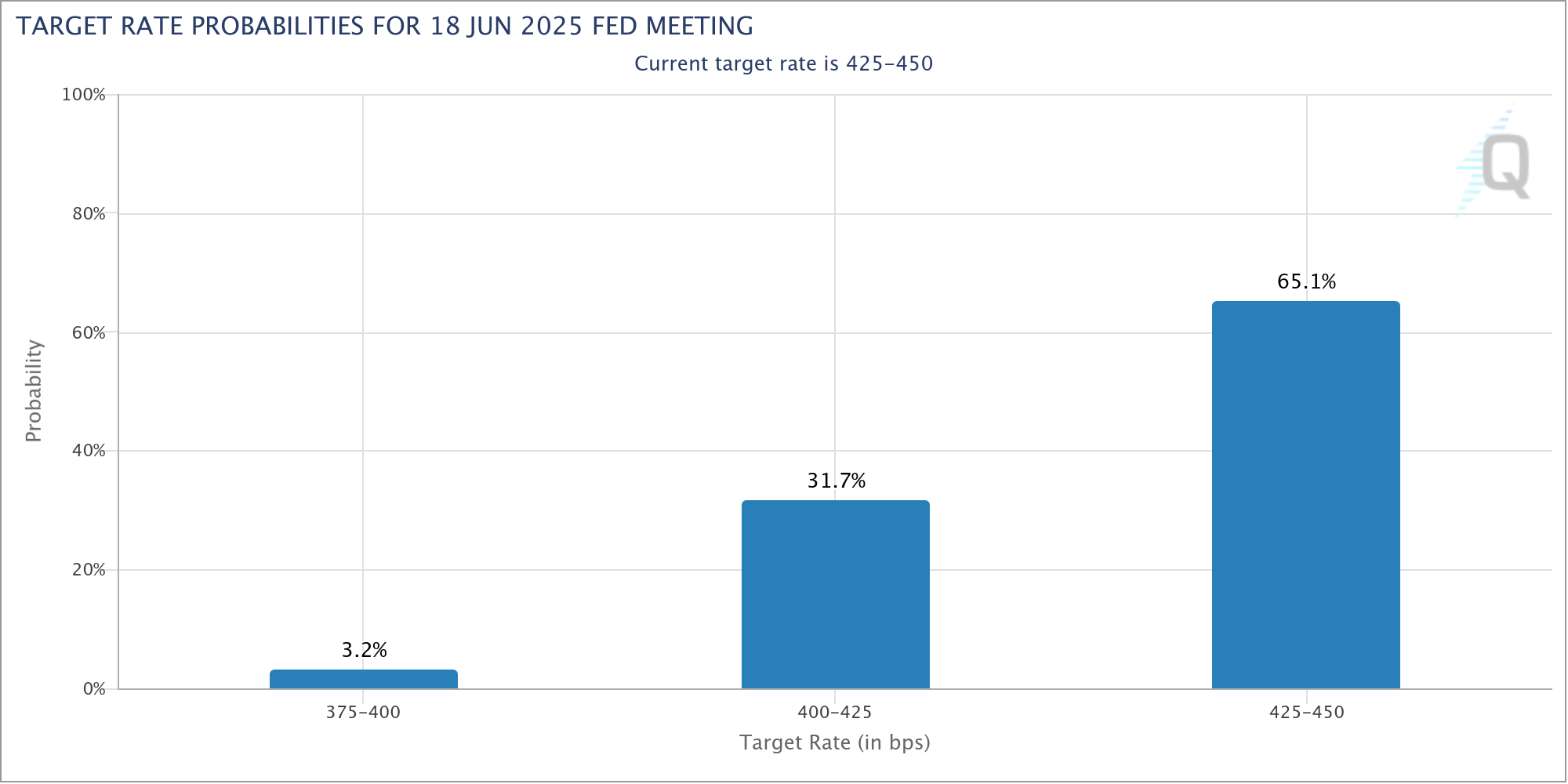

Both headline and core CPI surpassed forecasts, rising more than expected on both a monthly and annual basis. This marks a clear warning sign that inflation pressures remain persistent. Fed fund futures now imply a nearly 65% probability that Fed will keep rates unchanged through June, a notable increase from 50% just a day earlier. While it is still premature, it couldn't be totally ruled out that another rate hike could be back on the table if inflationary pressures intensifies further.

US trade policy is another key wildcard for future price pressures. President Donald Trump’s tariff war is still in its early stages. Reports indicated that his administration is finalizing details for reciprocal tariffs. Trade analysts suggest that structuring these tariffs might be more challenging than anticipated, potentially delaying their rollout. However, if implemented aggressively, these tariffs could drive further price increases, creating additional inflationary risks that Fed would have to contend with.

The currency markets reacted decisively, with Dollar emerging as the strongest performer for the day, followed by Swiss Franc and Euro. Yen, however, is the worst performer, struggling under the weight of rising US yields. Australian and New Zealand Dollars also faced significant pressure, caught in the wave of risk aversion triggered by inflation fears and concerns over global trade tensions. Meanwhile, Canadian Dollar and British Pound traded with a more neutral stance, positioning in the middle of the performance spectrum.

In Europe, at the time of writing, FTSE flat. DAX is up 0.06%. CAC is down -0.18%. UK 10-year yield is up 0.071 at 4.583. Germany 10-year yield is up 0.043 at 2.477. Earlier in Asia, Nikkei rose 0.42%. Hong Kong HSI rose 2.64%. China Shanghai SSE rose 0.85%. Singapore Strait Times rose 0.36%. Japan 10-year JGB yield rose 0.0406 to 1.347.

US CPI rises to 3% in Jan, core CPI up to 3.3%

US headline CPI rose 0.5% mom in January, exceeding expectations of 0.3% mom and marking the fastest monthly pace since August 2023. Core CPI, which strips out food and energy prices, also outpaced forecasts (0.3% mom) at 0.4% mom, the highest since March 2024.

Key inflation drivers for the month included a 0.4% mom increase in shelter costs, a 1.1% mom jump in energy prices, and a 0.4% mom rise in food prices.

On an annual basis, CPI accelerated from 2.9% yoy to 3.0% yoy, beating expectations of 2.9% yoy and extending its upward streak for the fourth consecutive month.

Core CPI also climbed, rising from 3.2% yoy to 3.3% yoy, surpassing the projected 3.1% yoy. Energy prices rose 1.0% yoy, while food costs were up 2.5% yoy.

ECB’s Villeroy warns of negative impact from US tariffs

French ECB Governing Council member Francois Villeroy de Galhau cautioned that US President Donald Trump’s tariffs will "very likely" have a "negative effect" on the economy.

Speaking on France Culture radio, Villeroy criticized "protectionism is a seductive short-term policy, but in the long term it is a losing strategy."

Despite trade tensions, Villeroy maintained an optimistic view on France’s economic resilience. He reaffirmed that the country is likely to avoid a recession in 2025.

Bank of France indicated on Tuesday that French GDP is on track to expand by 0.1% to 0.2% in the first quarter.

ECB’s Holzmann: Inflation risks rising, rate cuts require patience

Austrian ECB Governing Council member Robert Holzmann emphasized caution regarding rate cuts, citing renewed inflation risks from tariffs.

Speaking to CNBC, Holzmann noted that while inflation pressures had previously "somewhat dissipated," the latest developments, particularly increased trade frictions, pose fresh threats to price stability. As a result, policymakers must be careful in their approach on policy easing.

Holzmann explained that while increased trade barriers may reduce economic growth, they also contribute to inflationary pressures. "We will have to be more patient," he stated.

Addressing speculation about a larger 50 basis point rate cut, Holzmann dismissed the idea, arguing that ECB’s mandate is to manage inflation, not stimulate growth.

"Using the interest rate in order to initiate a higher growth is not the way how we should work," he stated.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.90; (P) 152.25; (R1) 152.86; More...

USD/JPY's strong break of 153.70 support turned resistance should confirm that corrective pull back from 158.86 has completed at 150.92. That came after drawing support from 38.2% retracement of 139.57 to 158.86 at 151.49. Intraday bias is back on the upside for retesting 158.86. Firm break there will resume whole rally from 139.57 to retest 161.94 high. For now, risk will stay on the upside as long as 150.92 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

US CPI rises to 3% in Jan, core CPI up to 3.3%

US headline CPI rose 0.5% mom in January, exceeding expectations of 0.3% mom and marking the fastest monthly pace since August 2023. Core CPI, which strips out food and energy prices, also outpaced forecasts (0.3% mom) at 0.4% mom, the highest since March 2024.

Key inflation drivers for the month included a 0.4% mom increase in shelter costs, a 1.1% mom jump in energy prices, and a 0.4% mom rise in food prices.

On an annual basis, CPI accelerated from 2.9% yoy to 3.0% yoy, beating expectations of 2.9% yoy and extending its upward streak for the fourth consecutive month.

Core CPI also climbed, rising from 3.2% yoy to 3.3% yoy, surpassing the projected 3.1% yoy. Energy prices rose 1.0% yoy, while food costs were up 2.5% yoy.

ECB’s Holzmann: Inflation risks rising, rate cuts require patience

Austrian ECB Governing Council member Robert Holzmann emphasized caution regarding rate cuts, citing renewed inflation risks from tariffs.

Speaking to CNBC, Holzmann noted that while inflation pressures had previously "somewhat dissipated," the latest developments, particularly increased trade frictions, pose fresh threats to price stability. As a result, policymakers must be careful in their approach on policy easing.

Holzmann explained that while increased trade barriers may reduce economic growth, they also contribute to inflationary pressures. "We will have to be more patient," he stated.

Addressing speculation about a larger 50 basis point rate cut, Holzmann dismissed the idea, arguing that ECB’s mandate is to manage inflation, not stimulate growth.

"Using the interest rate in order to initiate a higher growth is not the way how we should work," he stated.

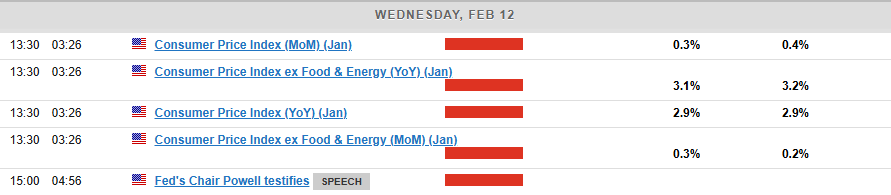

US CPI Release Today: What to Expect and Market Reactions

- US CPI inflation data for February 2025 is being released today, and markets are closely watching due to recent increases in inflation expectations.

- Economists expect headline inflation to rise by 0.3% for the month, keeping the yearly rate at 2.9%.

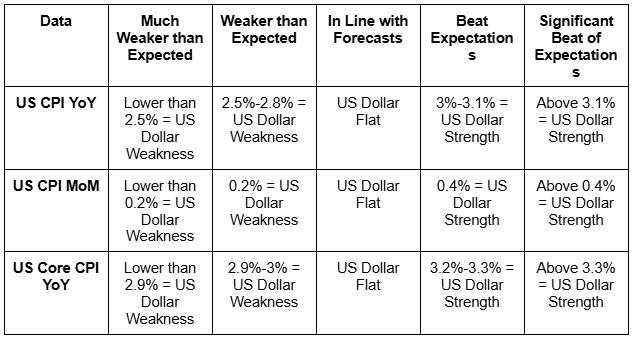

- The article provides a table outlining potential market impacts based on different CPI scenarios on the US Dollar.

US CPI inflation data will be released today at 13h30 GMT time. Markets are paying close attention to today’s release following a significant uptick in inflation expectations revealed in last week’s Michigan Sentiment Index.

The incoming US administration of Donald Trump and his tariff and economic policies have made stoked inflation fears. I still think this inflation print will be too early to see any effects from President Trump’s tariff policies.

Having said that, any significant uptick in inflation could definitely add to market concerns around the trajectory of inflation moving forward, especially when the impact of tariffs begin to have an effect.

What is the Expected CPI Print?

Inflation continues to be a concern, even though the U.S. economy is still strong. In December 2024, prices went up by 0.4% compared to the previous month, leading to an annual inflation rate of 2.9%. Core inflation, which leaves out food and energy prices, increased by 0.2% in December and reached 3.2% over the year.

These numbers show how difficult it is to lower inflation to the Federal Reserve’s target of 2%. Fed Chair Jerome Powell reiterated yesterday that there is no rush for further rate cuts as the Fed will wait and see the impacts of President Trump policies.

Economists predict that headline inflation for January will go up by 0.3% compared to the previous month, keeping the yearly rate at 2.9%. Core inflation, which leaves out food and energy, is also expected to rise by 0.3% for the month, with the yearly rate easing slightly to 3.1% from December’s 3.2%.

This would show a continued gradual slowdown since inflation peaked in 2022.

The January inflation increase is expected to be driven by higher auto insurance rates and consistent rises in housing-related costs, which have been big drivers of core inflation. However, slightly lower energy prices, especially gasoline, may help balance out some of the increase. While housing expenses are still rising, they might start to show slower growth, following the broader pattern of easing price pressures in the rental market.

Potential Market Impact

Looking at the potential scenarios from today’s CPI release, I have created a table that may help. Now this of course is no guarantee as to how the market may react but rather my take on the potential movements that could materialize.

Source: Table created by Zain Vawda, Data from LSEG, TradingEconomics

The above table provides an insight into what I expect will happen depending on the CPI prints released later in the day.

My personal expectations are that the data will land quite close to expectations which could lead to some short-term volatility and whipsaw price action before markets settle down.

Technical Analysis

From a technical standpoint, the dollar has enjoyed a positive start to the week but struggled to continue its bullish momentum yesterday.

The 108.49 resistance level continues to hold firm for now and CPI is unlikely to change this unless we have a significant beat or miss of the forecasts.

Immediate support rests at 107.50 and 107.00. Resistance on the other hand rests at 108.49, 109.52 before the psychological 110.00 handle comes into focus.

I do not see today’s data providing any impetus for a break of the recent trading range between the 107.00 and 108.49 handles.

US Dollar Index (DXY) Daily Chart, February 12, 2025

Source: TradingView.com (click to enlarge)

Support

- 107.50

- 107.00

- 106.13

Resistance

- 108.49

- 109.52

- 110.00

NZ Dollar Eyes US and New Zealand Inflation Data

The New Zealand dollar is in negative territory on Wednesday. NZD/USD is trading at 0.5636 in the European session, down 0.31% on the day.

US CPI expected to tick lower to 0.3%

The markets are keeping a close eye on the January inflation report, which will be released later today. Headine inflation is expected to remain unchanged at 2.9% y/y, while monthly it is expected to dip to 0.3% from 0.4%. The core rate, which excludes food and energy, is projected to dip to 3.1% y/y from 3.2%. Monthly core CPI is projected to rise to 0.3% from 0.2%.

The Federal Reserve is expected to cut rates once or twice this year, sharply lower than the Fed’s December forecast of four rate cuts. The US economy is performing well and there isn’t much pressure on the Fed to lower rates right now. The markets have priced in a rate hold at the March meeting at 95%, according to the CME’s FedWatch.

Fed Chair Powell reiterated in testimony before a Senate Banking committee on Tuesday that the Fed “does not need to be in a hurry” to adjust policy. Powell said that rate policy remains restrictive but the Fed would be careful not to lower rates too quickly or too slowly. Powell deflected a question about Trump’s tariffs and US trade policy but acknowledged that tariffs could lift inflation and complicate the Fed’s ability to lower rates.

New Zealand releases inflation expectations early Thursday. The forecast for the first quarter stands at 1.8% q/q, compared to 2.1% in Q4 2024. Inflation remained unchanged at 2.2% in the fourth quarter, close to the Reserve Bank of New Zealand’s target of 2%. The RBNZ meets next week and the money markets have fully priced in a rate cut, with about a 50/50 probability of quarter-point or half-point cut.

NZD/USD Technical

- NZD/USD has pushed below support at 0.5648 and is testing support at 0.5636. Below, there is support at 0.5549

- There is resistance at 0.5668 and 0.5680