Sample Category Title

Dollar Holds Strong Despite Fitch Raising Debt Ratio Forecasts; Euro Dips Further

Expectations that the Fed will proceed with a rate hike in December and an encouraging report on JOLTS job openings pushed the dollar higher during European trading hours, although Fitch raised its US medium-term debt-to-GDP forecasts. On the other hand, the euro was unable to find support on better-than-expected retail sales figures and despite the news that some key ECB officials opposed the central bank's decision to continue buying assets until inflation improves.

Fitch said on Tuesday that it expects a version of tax plans to pass the US Congress and push the federal deficit to 4% of GDP by next year, while it also anticipates US debt to reach 120% of GDP from the current 77% by 2027, questioning whether the tax cuts will pay for themselves.

Regarding data releases out of the US, figures on JOLTS job openings came in flat as expected, showing that 6.093 million positions were created in September compared to 6.090 million seen in August.

In the meantime, the US President, speaking at a news conference with the South Korean President Moon Jae-in in Seoul, used a milder rhetoric towards North Korea, calling the regime to "come to the table and make a deal", while he also admitted that there was progress on issues having to do with North Korea.

The dollar index rose to 95.14 before slipping back to 95, being 0.28% up on the day. Dollar/yen gained 0.26%, rising to 113.95, while dollar/loonie jumped by 0.80% to 1.2800.

Gold pulled back by 0.58% to $1,274.20 per ounce.

In the Eurozone, retail sales expanded by 0.7% m/m in September after a contraction of 0.1% in August (revised upwards from -0.5%), beating forecasts of a 0.6% growth. On a yearly basis, the measure rose by 3.7%, above the expected 2.7% and August's 2.3%. Despite improvements in Eurozone's household spending, the euro stretched its downleg near a four-month low of $1.1553 on the back of a stronger dollar.

In other news, sources familiar with ECB matters revealed that in October's meeting top ECB policymakers including board member Benoit Coeure, the President of the Bundesbank, Jens Weidman, and the Governor of the Bank of France, Francois Villeroy, recommended to tighten the central bank's quantitative easing program even if inflation fails to rise towards the target. Note that, the ECB announced on October 26 to continue buying bonds until price pressures increase. The ECB chief, Mario Draghi, did not comment on monetary policy at the second ECB Forum on Banking Supervision on Tuesday, while the ECB board member Sabine Lautenschlaeger said she "would have liked a clear exit" from the asset purchase program.

The pound posted mild gains in the first trading hours before falling back to $1.3135 after British house price growth gauged by the Halifax Community Bank came in more or less as anticipated. Particularly, October house prices rose by 0.3% m/m, below September's 0.8% and slightly above the 0.2% projected. Year-on-year, the Halifax index increased by 4.5%, matching expectations. However, uncertainties around Brexit developments pressured the currency with investors waiting for discussions to enter the next stage of negotiations on Thursday, whereas earlier on the day, the UK Prime Minister, Theresa May, said she would submit to the parliament on Tuesday a legislation permitting Britain to pursue an independent trade policy after the divorce from the EU.

Today's global dairy auction showed prices declining by 3.5% down compared to a contraction of 1.0% two weeks ago, adding further losses to the kiwi and pushing it to $0.6906 (-0.56%) despite the new government pledging to not target the foreign exchange as part of the RBNZ's monetary policy.

The aussie continued its downtrend, retreating to $0.7650 (0.52% down) after RBA policymakers held rates steady at a record low of 1.5% on Tuesday and retained their concerns on the path of inflation and overloaded household debt.

The USD is Keeping Balance

In October, the Non-Farm Payrolls added 252K, although it was expected to expand by 313K. However, the September report was revised upwards (+15K) and sort of wore off the first impression of the statistics. The Average Hourly Earnings didn't change; on YoY, it's still 2.4%. This report also got investors' attention: the predicted reading was 2.7% y/y. There was a similar situation this year, when the capital market focused on this very parameter and prevented the USD from being supported by other reports, which were pretty good. Another labor market report, the Unemployment Rate, managed to keep balance between pessimists and optimists among investors. The indicator decreased from 4.2% to 4.1%, which is the lowest reading over the last 16 years. Is it good? Sure thing.

The fact that the salaries didn't change may interfere with the way the inflation is growing, at least as the Federal Reserve and the government expect it to. This is why the USD plummeted right after the statistics had been published. However, both the Federal Reserve and the White House are very careful in their predictions and they are not worried that the CPI is a bit behind the target they specified. No one is waiting for a miracle here.

If we link all key statistics parameters together, an average employment reading is a little bit lower than expected. But it is unlikely to stop the Federal Reserve, which is going to raise the benchmark interest rate one more time in December. According to the CME futures, investors' expectations of the rate hike are 100%.

The US Dollar remains strong and the EUR/USD pair still have chances to get stabilized close to 1.1600 by the end of the first decade of November.

From the technical point of view, the EUR/USD pair is moving inside the descending channel. The current downside target is the support area between 1.1508 and 1.1486. After reaching this area, the price is highly likely to return to the upside border of the current channel at 1.1672. If the instrument rebounds from the resistance level, it may start a new descending impulse with the target at 1.1328.

Tax Reform Bill, Strong US Job Report Pushes Dollar Higher

USD/JPY has posted gains in the Tuesday session, erasing the gains seen on Monday. In North American trade, USD/JPY is trading at 114.09 up 0.34% on the day. On the release front, Japanese Average Cash Earnings remained unchanged at 0.9%, above the forecast of 0.6%. In the US, JOLT Job Openings edged up to 6.09 million, easily beating the estimate of 5.98 million. Later in the day, Fed Chair Janet Yellen will speak at an event in Washington.

Investors can expect more of the same from the Bank of Japan regarding its ultra-accommodative stimulus package. The minutes from the October meeting indicated that many of the board members were satisfied that the inflation target of around 2 percent would be met under current policy, even though inflation has persistently remained well below the target. BoJ Governor Kuroda echoed the message in the minutes, expressing optimism that the improving economy will boost inflation. Kuroda called the economic expansion "highly sustainable", and the markets took his optimism as a sign that the BoJ has no plans to inject further stimulus in the near future.

The markets are wishing President Trump godspeed, as he tries to pass his tax reform bill through Congress. If Trump is successful, it would mark the first major tax reform since President Reagan was president. Trump suffered a humiliating defeat with his failed health care proposal, and the President has now set his sights on tax reform. Trump wants new legislation in place before the end of the year, but that will be a tall order, as most Democrats have come out against the proposal and not all Republicans are on board. The bill would cut corporate taxes from 35% to 20%, but predictably, Democrat and Republican lawmakers are at odds as to whether the bill will lower taxes for the middle class. Expectations that Trump will cut taxes has been the catalyst for a stock market rally over the past year, and if the bill does become law, the US dollar will likely gain ground.

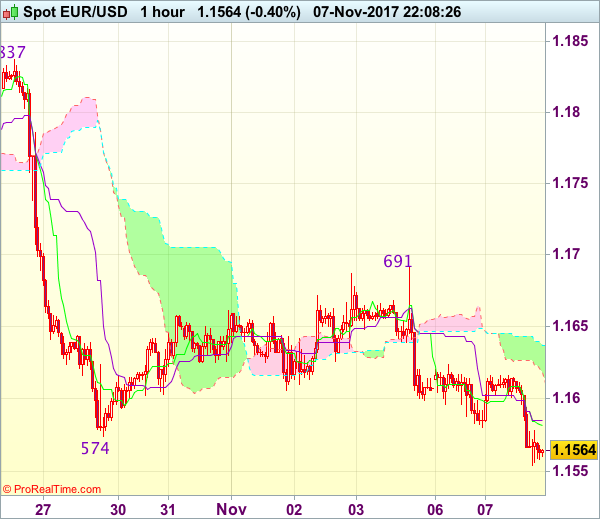

Euro Keeps Falling Against Dollar

The EUR/USD price continued its downward trajectory over growing concerns that the European Central Bank's decision to extend the asset purchasing programme into next year will negatively impact the euro. The bears received further justification from the German industrial production which fell 1.6% for September, missing the expected drop of only 0.7%. ECB President Mario Draghi's speech didn't make much impact on the market today though some positive data did come in from the retail sales report with grew by 0.7% in September, 0.1% over the forecast. The focus for the rest of the day will be on Fed Chair Janet Yellen's speech at 19:30 GMT.

The AUD/USD is falling today despite the anticipated decision of the Reserve Bank of Australia to keep interest rates at the historically low level 1.50%. According to the central bank, the pace of annual economic growth rate within the next few years will remain near 3%. At the same time, consumer inflation is likely to be below 2.0% due to the slow increase in labour costs. Traders are waiting for the release of the trade balance in China at 02:00 GMT tomorrow. As China is Australia's largest trading partner, this is a particularly sensitive indicator for the aussie dollar.

The USD/JPY resumed positive dynamics after the end of the recent price correction. Traders ignored positive statistics on the average cash earnings in Japan which increased by 0.9% on an annualised basis, which was 0.3% better than expected. Those trading the gopher will be keeping an eye on the release of the Japanese leading index for September which is due to be published at 00:00 GMT.

EUR/USD

The single currency continued the descending movement after some consolidation under 1.1620. Recently the RSI on the 15-minute chart touched the oversold zone, which points to a possible price correction after the recent powerful movement. On the other side, the chance of further falls, with immediate objectives at 1.1550 and 1.1500, is high.

AUD/USD

The aussie quotes crossed the SMA100 on the 15-minute chart and may soon reach strong support at 0.7635. Breaking through this may become a trigger for the drop to accelerate to 0.7600 and 0.7500. Within the rising correction, quotes may return to 0.7700, and overcoming this mark may result in the trend change to positive.

USD/JPY

The USD/JPY price crossed the 114.00 mark but was not able to hit the local high near 114.70. In case of gaining a foothold above this level, we are likely to see further price increases up to 115.50 and 117.00. The RSI on the 15-minute chart has stepped back from the overbought territory and after testing 114.00 we may see growth resume.

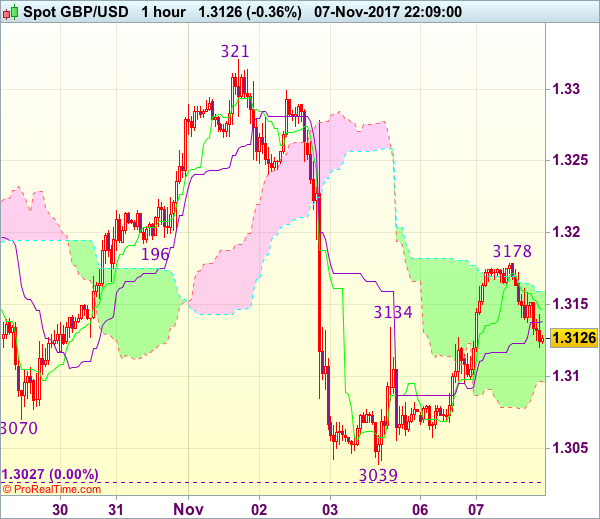

Elliott Wave Analysis: GBPUSD and Cocoa

Good day traders!

GBPUSD is steadily approaching the lower channel line and the lower swing low at 1.31002 level, where a break would indicate even more weakness. Maybe a five-wave fall can follow.

GBPUSD, 1H

Cocoa made a three-wave bearish move down from 2156 level. We labeled it as a three-wave a)-b)-c) move that is now regarded as completed, because of a sharp, impulsive rise in five-waves. Resistance for the unfolding red wave i) can be found a little above the upper channel line, from where later a new minor three-wave correction can follow, into wave ii).

Cocoa, 1H

EUR/USD Sets (Minor) Post-ECB Low

- European equities opened strong, but gradually slid lower, currently trading with minor losses. US equities open little changed.

- Production across German industry declined in September (-1.6% M/M) after a strong rise in the previous month (2.6% M/M), with steep falls reported in both capital goods and energy. Given the strong order intake of recent months, the decline should be a one-off.

- Eurozone retail sales easily beat expectations in September, pushing the annual growth rate to the highest level since July 2015 in the latest sign of improving conditions across the currency bloc. Retail sales rose by 3.7% Y/Y in September beating expectations (2.9% Y/Y) and the previous month's result (2.3% Y/Y).

- The ECB's chief banking supervisor, Nouy, said that about 20 banks have applied for European banking licences in the wake of the UK's decision to quit the European Union.

- France has called for tax havens to be stripped of any right to seek help from the IMF and other global financial institutions in response to the "Paradise Papers" revelations.

- Mario Draghi has called on banks to cut costs instead of blaming the ECB's monetary policy for poor profitability. "There is little evidence that negative rates are undermining banking profitability."

- President Trump toned down his harsh rhetoric toward North Korea during a visit to Seoul, telling reporters the Pyongyang regime should "come to the table" to make a deal and refusing to rule out direct talks.

Rates

Dull core bond trading session

Core bonds moved sideways (Bund: 30 ticks band) in an uneventful session devoid of key economic data. At the time of writing, German yield changes vary between -0.3 and +0.5 bp. US yields are flat (2-yr) to 0.4 bp higher. On intra-EMU bond markets, 10-yr yield spreads versus Germany narrowed substantially by 2 to 6 bps. Traders reported strong buying in the peripherals, but we are not aware of a particular driver.

The Bund tried to rally towards the end of the morning session, aiming to test the contract high at 163.42, but the attempt missed dash. The Bund returned south when a "source" article on the ECB (see below) suggested that some ECB heavyweight governors objected to the APP proposal that was ultimately accepted last week. US Treasuries didn't show more vigour. European equities gradually slid lower during the entire session after a strong opening, but there was little impact on bonds. US investors prepare to the first leg of the three-part refunding operation concerning a $24B 3-yr Note auction later today.

According to a "sources" article, three ECB heavyweights pushed at the last ECB meeting to alter a commitment to keep buying bonds until the "council sees a sustained adjustment in the path of inflation consistent with its inflation aim." ECB governors Couere, Weidmann and Villeroy recommended tying the overall level of monetary stimulus rather than just asset purchases to the outlook of prices. The broadening of the language would have potentially meant the ECB could terminate the bond purchases even if inflation failed to pick up. The change of the guidance didn't make it, but it suggests that opinions on the APP are far from unanimous. A fourth ECB member, board member Lautenschlaeger, revealed she wanted a "clear exit" from the programme and ECB Weidmann already expressed his opposition to the outcome the day after the ECB decision.

Currencies

EUR/USD sets (minor) post-ECB low

Trading in EUR/USD and USD/JPY was again technical in nature. There were no important data in EMU or in the US. Interest rate differentials and/or equities were also unable to give guidance. EUR/USD finally set a new post-ECB correction low, but follow-through losses were modest. USD/JPY still doesn't go anywhere holding near the 114 pivot.

Overnight, several Asian equity indices including the Nikkei traded at multi-year highs. Higher oil and commodity prices supported energy and materials' stocks. USD/JPY returned north of 114, but a retest of the 114.49/73 resistance didn't occur. So, the USD/JPY performance remained mediocre given the stock market rally. EUR/USD was little changed in the 1.1605/10 area.

The EMU eco data were mixed. German September production data and the retail PMI's from several EMU member states were weaker than expected. Later in the session, the 'official' September EMU retail sales printed very strong at 0.7% M/M and 3.7% Y/Y. We didn't see a direct impact from thee data on EUR/USD. The pair drifted gradually south from the start of the EMU trading session. Recent inability to move away from the post-ECB low finally caused some additional EUR/USD longs to throw in the towel. EUR/USD set a minor new correction low. Still, the move developed in a very gradual way.

Euro selling slowed in early US dealings. EUR/USD trades currently in the 1.1570 area. USD/JPY was again unable to go for a retest of the 114.49/73 resistance. There was no additional interest rate support for the dollar. US and European equities were also unable to maintain the positive Asian momentum, preventing a further decline of the yen. USD/JPY is little changed in the 114.10/15 area.

Sterling follows broader euro and USD trends

Sterling also showed a diffuse trading pattern today. The UK currency ceded ground against the dollar but gained a few ticks against an overall soft euro. The UK eco data were in line (Halifax house prices) to weaker than expected (very poor BRC retail sales). The impact of the data was not big, but the poor BRC sales, probably aborted the sterling rebound on Friday and yesterday. EUR/GBP dropped temporary below 0.8800 but trades again in the 0.8815 area. The loss in cable is more substantial (1.3130 from 1.3075 at the open overnight). In the end, the intraday swings in cable and in EUR/GBP were primarily USD and euro moves rather than sterling inspired price action.

Trade Idea Wrap-up: USD/CHF – Hold long entered at 0.9950

USD/CHF - 0.9988

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.0001

Kijun-Sen level : 0.9996

Ichimoku cloud top : 1.0003

Ichimoku cloud bottom : 0.9989

Original strategy :

Bought at 0.9950, Target: 1.0050, Stop: 0.9950

Position : - Long at 0.9950

Target : - 1.0050

Stop : - 0.9950

New strategy :

Hold long entered at 0.9950, Target: 1.0050, Stop: 0.9970

Position : - Long at 0.9950

Target : - 1.0050

Stop : - 0.9970

Although the greenback retreated after rising to 1.0029, reckon downside would be limited to 0.9970-75 and bullishness remains for recent rise to resume after consolidation, above said resistance at 1.0029 would bring retest of 1.0038, break there would confirm the rise from 0.9421 low has resumed and extend further gain to 1.0050-55, then towards 1.0075-80 but price should falter below 1.0100 chart resistance.

In view of this, we are holding on to our long position entered at 0.9950. Only below said support at 0.9938-48 would abort and signal top is formed instead, risk correction to 0.9920-23 (38.2% Fibonacci retracement of 0.9737-1.0038) but 0.9885-90 (50% Fibonacci retracement) should limit downside and support at 0.9869 would remain intact.

Trade Idea Wrap-up: GBP/USD – Hold short entered at 1.3175

GBP/USD - 1.3140

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.3146

Kijun-Sen level : 1.3138

Ichimoku cloud top : 1.3159

Ichimoku cloud bottom : 1.3096

Original strategy :

Sold at 1.3175, Target: 1.3045, Stop: 1.3210

Position : - Short at 1.3175

Target : - 1.3045

Stop : - 1.3210

New strategy :

Hold short entered at 1.3175, Target: 1.3045, Stop: 1.3180

Position : - Short at 1.3175

Target : - 1.3045

Stop : - 1.3180

Although cable staged another strong rebound since yesterday, as this move from 1.3039 is viewed as retracement of last week’s selloff, reckon upside would be limited and mild downside bias remains for weakness to 1.3095-00 but below 1.3065-70 is needed to signal the rebound from 1.3039 has ended and bring retest of recent low at 1.3027. Looking ahead, only a drop below this level would confirm early downtrend has resumed for weakness to psychological support at 1.3000, then towards 1.2970-75.

In view of this, we are holding on to our short position entered at 1.3175. Above 1.3175-80 would risk gain to 1.3200, break there would defer and prolong choppy trading, risk a stronger rebound to 1.3235-40 first.

Trade Idea Wrap-up: EUR/USD – Hold short entered at 1.1620

EUR/USD - 1.1578

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.1582

Kijun-Sen level : 1.1585

Ichimoku cloud top : 1.1637

Ichimoku cloud bottom : 1.1619

Original strategy :

Sold at 1.1620, Target: 1.1520, Stop: 1.1655

Position : - Short at 1.1620

Target : - 1.1520

Stop : - 1.1655

New strategy :

Hold short entered at 1.1620, Target: 1.1520, Stop: 1.1620

Position : - Short at 1.1620

Target : - 1.1520

Stop : - 1.1620

As the single currency recovered after finding support at 1.1580, minor consolidation would be seen, however, reckon upside would be limited to the lower Kumo (now at 1.1619) and bring another decline later to 1.1574-80, break there would extend recent decline to 1.1520-25, then 1.1500 but near term oversold condition should prevent sharp fall below latter level.

In view of this, we are holding on to our short position entered at 1.1620. Above 1.1620-25 would defer and risk test of the upper Kumo (now at 1.1637) would risk another bounce towards 1.1691, however, only break there would abort and suggest further choppy trading above 1.1574 would be seen, bring a stronger rebound to 1.1700-05 but upside should be limited to previous support at 1.1725 (now resistance).

Copper Eases Below Triangle on Stronger Dollar

Copper was sharply lower on Tuesday after rally on Monday was repeatedly capped by bear-trendline which marks the upper boundary of the triangle, formed on daily chart. Fresh weakness, triggered by stronger dollar, offset positive signal on Monday's bullish engulfing pattern and generates bearish signal on probe below the lower boundary of triangle. Close below triangle is needed to confirm and expose immediate support at $3.0915 (daily Kijun-sen), break of which would open way for retest of key near-term support at $3.0725 (27 Oct low).

Overall picture remains bullish but the metal may extend pullback from fresh multi-year high at $3.2580, before broader bulls resume.

Res: 3.1176; 3.1422; 3.1504; 3.1645

Sup: 3.1015; 3.0915; 3.0725; 3.0660