Sample Category Title

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7614; (P) 0.7657; (R1) 0.7687; More...

AUD/USD is still holding in range above 0.7624 support and intraday bias remains neutral at this point. More consolidation could still be seen. But after al, near term outlook stays bearish with 0.7896 resistance intact and deeper fall is expected. Decisive break of 0.7624 will resume whole decline from 0.8124. And, AUD/USD should target next key cluster level at 0.7322/8 next.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

Dollar Pared Gains on Rumor of Delay to Corporate Tax Cut

Dollar weakens overnight on report that Senate Republicans are considering to delay corporate tax cut by a year. The greenback pared back some of this week's gains and turned mixed for the week. EUR/USD led the way down yesterday but breaking 1.1574 support. But equivalent move was not seen in other dollar pairs. USD/CHF was held below 1.0037 near term resistance. USD/JPY also failed to sustain above 114.44/9 zone. And even AUD/USD is held above 0.7624 support. Dollar is still waiting for inspiration for a firm breakout from consolidations. Meanwhile, Sterling and Yen remains the strongest one for the week so far.

House and Senate versions tax bill could differ significantly

In the US, House Ways and Means Committee Chairman Kevin Brady, Republican, said that the tax bill will be brought to floor next week and "our goal is to pass it next week out of the House". Meanwhile, Senate Republicans are expected to unveil their own version of the tax bill at the end of the week. The Senate version is expected to be drastically different from the House version. In particular, it's reported, with no named source, that Senate Republicans are considering to delay the implementation of corporate tax cut by one year to comply with Senate rules. In the coming days, markets' attention will be on how far apart the versions are, and thus, the work to reconcile them.

Separately, rating agency Fitch predicted that the tax plan would pass in both chambers. However, Fitch warned that "Such reform would deliver a modest and temporary spur to growth. ... However, it will lead to wider fiscal deficits and add significantly to U.S. government debt." And Fitch is reviving up medium-term US government debt forecast.

Trump's new Fed Governor Quarles wants "fresh look at everything"

New Fed Governor Randal Quarles made his first public remarks yesterday. He urged to have a "fresh look at everything" and pledged to make regulatory process more transparent "in a very short period of time". He added that "one of the reasons for transparency is part of the basic view of the relationship between the government and the governed. If there are going to be rules, we should probably let the people know what they are." And for example, stress testing is "on the front burner" and the "tenor of supervision" to changes. Quarles is US President Donald Trump's first appointment to the Fed board and there are still three remaining vacancies.

Fed chair Yellen urged high ethical standards

Fed chair Janet Yellen was honored with former Fed chair Ben Bernanke with this year's Paul H. Douglas Award for Ethics. In the ceremony yesterday, she emphasized that "the Federal Reserve's very effectiveness in setting monetary policy depends on the public's assured confidence that we act only in its interest". And he urged Fed officials to "demonstrate our ethical standards in ways that leave little room for doubt." She pointed out that Douglas was the first public officials in the US who published a full accounting of his own personal finances back in 1939. And, she noted Douglas believed that "the public's trust was so fundamental to the effectiveness of government that such steps were appropriate."

BoC Poloz: No de-anchoring of inflation expectations

BoC Governor Stephen Poloz there is no evidence of "de-anchoring" of inflation expectations but reiterated that the central bank wold be cautious in further interest rate moves. Also, he pledged to monitory the developments in the economy after two rate hikes earlier this year. Meanwhile, he pointed to encouraging signs of wage growth in October's job report. But he emphasized that "a lot of pieces need to fall into place before we can be certain that the economy has made it all the way home."

ECB splits on pledge to maintain asset purchases

In October ECB meeting, the central bank announced to half monthly asset purchase to EUR 30b and extend the program by nine months till September. Euro responded negatively to the pledge that the program will continue until "a sustained adjustment in the path of inflation consistent with its inflation aim". It's now reported that Executive Board member Benoit Coeure, Bundesbank Head Jens Weidmann and Bank of France Governor Francois Villeroy de Galhau objected to maintaining that language. Instead, they pushed for tying the overall level of monetary stimulus, rather than the asset purchase program alone, to economic outlook. The main implication to the change is that ECB could end the asset purchase program even if inflation doesn't pick up. However, it's opposed by ECB chief economic Peter Praet. The report is mainly seen as a confirmation of the split ECB officials regarding the path forward in 2018, at this juncture of stimulus exit.

On the data front

China trade surplus widened to USD 38.2b in October, or CNY 254b. The calendar remains light as Canada housing starts and building permits will be featured.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7614; (P) 0.7657; (R1) 0.7687; More...

AUD/USD is still holding in range above 0.7624 support and intraday bias remains neutral at this point. More consolidation could still be seen. But after al, near term outlook stays bearish with 0.7896 resistance intact and deeper fall is expected. Decisive break of 0.7624 will resume whole decline from 0.8124. And, AUD/USD should target next key cluster level at 0.7322/8 next.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 3:45 | CNY | Trade Balance (CNY) Oct | 254B | 275B | 193B | |

| 3:45 | CNY | Trade Balance (USD) Oct | 38.2B | 39.5B | 28.5B | |

| 5:00 | JPY | Leading Index Sep P | 106.6 | 107.2 | ||

| 13:15 | CAD | Housing Starts Oct | 220K | 217K | ||

| 13:30 | CAD | Building Permits M/M Sep | -5.50% | |||

| 15:30 | USD | Crude Oil Inventories | -2.4M | |||

| 20:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% |

Market Morning Briefing: Dollar-Yen Again Rose Above 114.00

FOREX

Dollar Index (94.83) has come off a bit from a high near 95.15 yesterday. We can still look for further rise towards 95.50 (medium term) and even 97.00 (long term) while the Supports at 94.50 and 94.00 remain intact.

Similarly, the Euro (1.1595) saw some short-covering from 1.1553, just above our target region of 1.1550-30. Resistance at 1.1620 is still valid. Need to see if it can push the Euro down to lower levels.

Dollar-Yen (113.78) again rose above 114.00 yesterday to a high of 114.34, but has come off again from there. It is running into sustained selling every time it rises past 114.00. This is because the US-Japan 10Yr Spread (2.28%) has been coming down and has broken a near-term rising trendline.

Dollar-Yuan (6.6393) has risen afresh and Dollar-Rupee has opened higher near 65.15. If the rise sustains, we may have to look for 65.40 as well.

INTEREST RATES

The German-US 10Yr Spread (-1.98%) has been rising from -2.05% since 30th Oct, but has Resistance near -1.95% and may be seen as bearish while below -1.95%.

Next week's US CPI release on 15th Nov will be important to see how much it reflects the recent increase in Crude, as that will influence the US Yields.

The US 10Yr (2.31%) has Support at 2.24%, but maybe there can be a near-term dip to test that Support, before a bounce takes place later in Nov. We also need to see if the US 5Yr (1.98%) will dip towards 1.80% or not. But, the US 30Yr (2.77%) may have a Support near current levels. Let us see if it bounces or not.

The Japanese 5Yr (-0.14%) has come down to test Support and should be a candidate for a bounce. The Japanese 10Yr (0.03%) too might have Support near 0.01%.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD attempted to push lower yesterday slipped below 1.1580 support area but still unable to stay consistently below that area and hit 1.1606 earlier today in Asian session. The bias is neutral in nearest term. Overall I remain bearish as a part of the “head and shoulders” bearish reversal scenario as you can see on my daily chart below but need a clear break below 1.1580 to continue the bearish scenario targeting 1.1500 – 1.1450 region. Immediate resistance is seen around 1.1650/70. A clear break above that area could trigger further bullish pressure testing 1.1725 but as long as stay below 1.1900 I remain bearish and any upside pullback should be seen as a good opportunity to sell.

GBPUSD

The GBPUSD was indecisive yesterday. Price attempted to push lower bottomed at 1.3108 but closed higher at 1.3165. The bias is bullish in nearest term testing 1.3270 but key resistance remains at 1.3330. Immediate support is seen around 1.3130. A clear break below that area could lead price to neutral zone in nearest term testing 1.3075/50 area but key support remains at 1.3000. Overall I remain bullish.

USDJPY

The USDJPY attempted to push higher yesterday topped at 114.34 but closed lower at 114.00 and hit 113.71 earlier today in Asian session. The bias remains bearish in nearest term testing 113.20 support area as a part of the bearish pin bar scenario as you can see on my daily chart below. A clear break and daily close below that area would expose 112.25 – 111.65 region. Immediate resistance is seen around 114.00 but key resistance remains at 114.50 which remains a good place to sell with a tight stop loss. Overall I remain neutral.

USDCHF

The USDCHF had another insignificant movement yesterday. The bias remains neutral in nearest term. Price is still trapped inside a 100-pip range area between 1.0037 – 0.9940 as you can see on my daily chart below and we need a clear break from that range area to see clearer direction . Overall I remain bullish but need a clear break above 1.0037 to resume the bullish trend testing 1.0100 or higher. On the downside, a clear break and daily close below 0.9940 would expose 0.9835 support area.

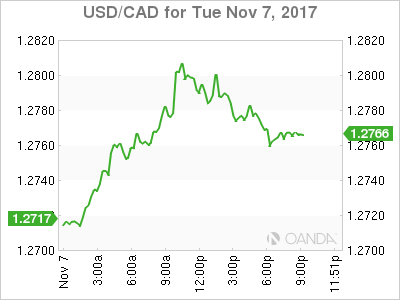

USD/CAD Canadian Dollar Lower After USD Resurgence

The Canadian dollar depreciated on Tuesday with little support from Bank of Canada (BoC) Governor Stephen Poloz who gave a speech in Montreal. U.S. Federal Reserve officials Randal Quarles and Fed Chair Janet Yellen did not provide any new insights to markets on the plans of the central bank. The geopolitical risk that was triggered by the arrests in Saudi Arabia over the weekend has faded and the US dollar has reassumed the upward move that was interrupted by the low wage growth data released with the U.S. non farm payrolls (NFP) on Friday.

Inflation was the main topic of Governor Poloz speech where he reiterated the central bank objective is to monitor wage growth, economic capacity and inflation and adjust the interest rate accordingly. The BoC has lifted interest rates twice in 2017 after a surprise growth in the first half of the year. The two rate hikes have cancelled the cuts of 2015 leaving the benchmark rate back at 1.00 percent. A cool down of the economy has been expected and so far the BoC has turned dove with the market further discounting the probability of another rate hike this year.

NAFTA talks will resume on November 15 with the hope of having a working plan before the elections in Mexico and the United States almost abandoned. The uncertainty on the outcome of the negotiations has given traders a headache in trying to value what the potential impact of various scenarios will have on the affected currency pairs.

The USD/CAD gained 0.55 percent on Tuesday. The currency pair is trading at 1.2777 with the USD regaining some of the losses from Monday. The currency pair has been erratic in the start of the week with little economic data to trade on.

The USD continued to be supported by a tightening monetary policy by the U.S. Federal Reserve who has hiked twice in 2017 and is on track to raise rates once again in December. Fed Chair Janet Yellen is set to step down in February, with president Trump already nominating her successor in Jerome Powell, currently a Fed Governor .

Political uncertainty surrounding the fate of the tax reform bill is keeping the USD in a tight trading range as both sides of the spectrum continue to argue on who will benefit the most form the proposed tax cuts.

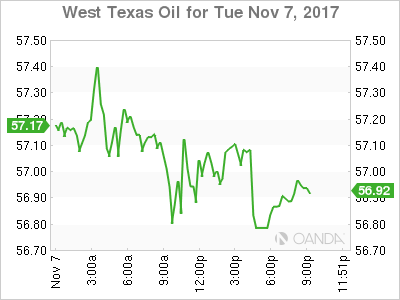

The price of energy was caught in a tight trading range on Tuesday. West Texas Intermediate is trading at $57.07 after the events in Saudi Arabia saw the price of crude rise, but as the week progresses and more economic indicators are expected the price of oil has been stable.

The arrests of prominent Saudi politicians and businessmen comes at a time when the kingdom is opening too many fronts. The embargo against Qatar, the military offensive in Yemen and the diplomatic/ideological fight with Iran have crown prince Mohammed Bin Salman in common as he is pushing for reform at home and abroad.

The Organization of the Petroleum Exporting Countries (OPEC) released its 2017 World Oil Outlook today and the group is forecasting a rise in shale production and growing demand in the following two years. OPEC and other major producers agreed to cut production to rebalance the energy markets after heavy falls and are now looking at extending for a second time the length of the agreement.

The public statements from producers that are part of the cut agreement have all been positive to the idea of extending the timeline past the March 2018 deadline. Oil rigs in the US have not grown in numbers despite the rise in oil prices, in some cases affected by adverse weather with technological advances increasing productivity.

The showdown between US production, which OPEC is conceding will grow and may eclipse its own members who are committed to reducing supply will continue well into next year. The implications of Saudi Arabia’s leadership will also have far reaching impact as the OPEC itself could end up being fractured as Iran and Saudi Arabia escalate their war of words.

Market events to watch this week:

Wednesday, November 8

11:30 am USD Crude Oil Inventories

4:00 pm NZD Official Cash Rate

4:00 pm NZD RBNZ Rate Statement

5:00 pm NZD RBNZ Press Conference

Thursday, November 9

9:30 am USD Unemployment Claims

8:30 pm AUD RBA Monetary Policy Statement

Friday, November 10

5:30am GBP Manufacturing Production m/m

Gold Slips On Sharp US Employment Report

Gold has posted considerable gains in the Tuesday session. In North American trade, the spot price for an ounce of gold is $1275.19, down 0.53% on the day. On the release front, JOLT Job Openings edged up to 6.09 million, easily beating the estimate of 5.98 million. Later in the day, Fed Chair Janet Yellen will speak at an event in Washington.

President Donald Trump suffered a humiliating defeat with his failed health care proposal, and the President has now set his sights on tax reform. If Trump is successful, it would mark the first major tax reform since President Reagan was president. Trump wants new legislation in place before the end of the year, but that will be a tall order, as most Democrats have come out against the proposal and not all Republicans are on board. The bill would cut corporate taxes from 35% to 20%, but predictably, Democrat and Republican lawmakers are at odds as to whether the bill will lower taxes for the middle class. Expectations that Trump will cut taxes has been the catalyst for a stock market rally over the past year, and if the bill does become law, investor risk appetite could increase and send gold prices downwards.

The Federal Reserve was in the spotlight last week, as President Trump nominated Jerome Powell to replace Fed Chair Janet Yellen. The changing of the guard will take place in February, when Yellen’s 3-year term expires. Powell is expected to maintain the Fed’s cautious monetary policy, which entails small, incremental rate hikes. Coming on the heels of that announcement, FOMC member William Dudley announced that he will retire in mid-2018. This move could have implications for monetary policy, depending on who will replace Dudley. A possible candidate is Kevin Warsh, who made the short list for the successor to Fed Chair Janet Yellen. Warsh is in favor of higher rates and favors less regulation of the banking sector, and if he would certainly support a more hawkish stance on monetary policy.

USD Off On Reports Of Tax Delay

The US dollar falling off its Tuesday highs and equity futures are off (SPY -6, DOW Futures -35) on Wahington Post report that US Senate Republicans may delay the corporate tax cuts by 1 year. But details could change ahead of Thursday's formal release of the bill by the Senate Finance Committee. The euro slumped again Tuesday but a late-day bounce showed the next move could be drawn out. The US dollar was the top performer on the day while the New Zealand dollar lagged. The Asia-Pacific calendar is light but Trump is in South Korea and could stir up geopolitical risk. The EURUSD and FTSE trades were stopped out befor a new trade has been posted in a major index (before the Tax story broke).

EUR/USD touched 1.1553 before bouncing 30 pips to finish narrowly lower on the day. At the lows, it was the worst level since July 19. Most importantly, it helps to reaffirm the head-and-shoulders top on the chart.

The danger sign for the pair is bonds. US 10-year yields edged lower to 2.31% as they continue to fall away from the key 2.40% level. The low was just below the 200-day moving average. Economic data was limited to JOLTS at 6.093m, slightly better than the 6.075m consensus.

On the whole, the US economic calendar is light this week but the political calendar is busy. The House is aiming to pass the tax cut bill this week. The headlines are likely to be positive for the US dollar but the mood may quickly shift if it encounters problems in the Senate.

Oil is also a key focus as Saudi Arabia continues to crack down. On Tuesday, dozens of bank accounts were frozen but the oil market retraced a portion of Monday's big gain in part because of higher US inventories and a warning from OPEC that shale production could ramp up once again.

Trump will be a risk in the day ahead as he meets South Korean President Moon. Initial dialogue and comments were more constructive on the possibility of a deal with North Korea but the mood could shift any moment.

Trump Tax Plan Likely to be Dollar Positive But Hurdles Remain Before Passage

The House Republicans will be meeting this week to revise the Trump administration's tax plans announced last week as aspects of the bill is facing significant opposition by some Republicans. The bill also falls short of the Senate's budget rules, suggesting that President Trump's hopes for the passage of the tax reform legislation by Christmas may be too optimistic.

It is expected that the House Ways and Means Committee, which is responsible for scrutinizing all bills relating to taxation, will complete its review on Thursday, with a vote on the revised bill planned before the Thanksgiving holiday on November 23.

While financial markets have broadly welcomed the much-anticipated tax reforms, it has drawn a lot of criticism from both Republicans and Democrats alike. Key issues for lawmakers are the elimination of many tax breaks such as the state and local tax deduction (SALT), the student-loan-interest deduction and the home-mortgage-interest deduction.

Changes to the home-mortgage-interest deduction has already led to a sharp sell-off in shares of homebuilders on fears that the lowering of the threshold on loans from $1 million to $500,000 would make it too expensive for middle-class Americans to buy a house.

There are also concerns that the tax plan favours the rich even though the Republicans have been touting the reforms as beneficial for the middle-class. Plans to eliminate the estate tax (which only applies to estates worth more than $5.6 million) and the alternative minimum tax, as well as the lifting of the top income tax bracket of 39.6% to earnings above $1 million for married couples have not gone down too well either by the critics.

However, the tax bill proposes massive tax cuts for both business and individuals. The highlight is the cut in the corporate tax rate from the current 35% to 20%. Despite rumours that the cut would be phased in, Republicans are pushing for the reduction to come into effect in one go. Such a big cut is sure to further energize shares on Wall Street if approved. Major US indices such as the Dow Jones, the S&P 500 and the Nasdaq have been setting record highs all year and a large cut in corporations' tax bill would boost earnings, extending this year's impressive rally into 2018.

Changes to the income tax brackets also promise major tax deductions for individuals. In addition, families stand to gain from an increase in the size of the child tax credit, while other reliefs include a new 25% rate for pass-through businesses, which would benefit individuals who own their own business.

The size of the tax reductions is estimated to amount to $1.41 trillion and is likely to have a notable impact on growth as the cuts would increase spending by both individuals and businesses. Higher growth has the potential to inflate price and wage pressures at a time when the US economy is already near full employment. Higher inflation would in turn prompt the Fed to raise rates at a faster pace than they otherwise would have without the tax cuts.

A shift in the Fed's rate hike path from the current gradual to a more aggressive one could be the trigger the dollar needs to resume its Trumpflation rally after almost a year of consolidating.

Apart from the direct fiscal stimulus boost, the greenback also stands to gain from another key tax policy – the repatriation tax. If approved, the new repatriation rate of 12% would be a one-time but mandatory tax on the overseas assets of US companies. Such a measure could temporary boost dollar demand as companies 'repatriate' their overseas cash earnings to the US.

Also worrying for financial markets would be the potential impact of the tax reforms on the bond market. It is estimated that the tax reforms will add $1.49 trillion to the US deficit over the next 10 years. If the tax bill passes in its current form and Congress does not find ways to trim spending elsewhere, the massive increase to the national debt could pressure Treasury Notes, leading to a steeper yield curve and this would be positive for the dollar.

But a more immediate concern about the cost of the tax plan is whether it breaches Senate rules. The budget resolution for fiscal year 2018 approved by the Senate earlier in October allows the national debt to rise by no more than $1.5 trillion over the next 10 years. Although the cost of the tax bill falls just under that limit, some argue that unless the reforms succeed in generating more revenue, the Republicans would need to find ways to reduce a projected shortfall if they want to avoid some of the cuts being reversed after 10 years.

Republicans are now aiming for the House Ways and Means Committee to complete its review of the tax plan by Thursday and for the House to vote on the revised bill before the Thanksgiving break. In the meantime, the Senate is working on its own version of the plan. The Senate's version will likely be unveiled at the end of next week with a vote expected in early December after the two versions have been reconciled.

Should a final bill manage to make its way to President Trump's desk before the end of the year, it would signal the first big legislative win for Trump and his Republican party since coming into office. The failed attempts at repealing and replacing Obamacare had dented investors' confidence in the Trump administration's ability to see through a major tax reform program, contributing to the dollar's decline earlier in the year.

The risk of a defeat of the bill in either the Senate or the House shouldn't be underestimated as the plan doesn't appear to have impressed voters, with many Americans not convinced that they will benefit from the tax cuts. This could sway Republican lawmakers in Democratic-leaning states to vote against the plan. However, If the tax legislation is able to overcome opposition in Congress, the successful passage of the bill could provide markets with an early Christmas present, lifting equities to fresh record highs and bringing the 116 yen level into view.

The US dollar turned bullish again in September as the tax plan starting moving forward and odds of a third rate hike this year strengthened. Looking ahead into 2018, while tax cuts, if approved, would at the very least reinforce the current uptrend, the longer-term prospect for the dollar would depend on whether wage growth – a key factor for Fed policymakers – starts to show convincing signs of a pickup and the scale to which any fiscal stimulus would lead the Fed to revise up its rate path projections.

Persistently Overshooting the Fed Funds Rate

Attempting to predict future increases in the federal funds rate has proven to be a challenge for decision makers from both the public and private sides during this business cycle. A pattern of over-forecasting the fed funds rate has become apparent. Likewise, and somewhat unsurprisingly, this trend of over-shooting is also associated with predicting the future value of the 10-year Treasury, as its value is influenced by federal funds rate expectations. In this special report we present several possible contributing factors as to why this business cycle, in particular, has given forecasters so much trouble predicting the level of the fed funds rate.

Factor One: Stubbornly Low Inflation

Lower-than-expected inflation during this economic cycle has certainly loomed large in the minds of the FOMC members. Persistently below two-percent inflation is not consistent with the goals of the Federal Reserve's dual mandate, one of which aims for price stability at two percent. The PCE deflator, the Fed's preferred measure of price pressures in the economy, averaged 1.82 percent for 2010-14, and has averaged just 0.98 percent since early 2015. Despite its positive sign, inflation remains well below the Fed's 2 percent target.

Where does inflation go from here? Recently, much of the discussion on Capitol Hill has surrounded the potential for an overhaul of the U.S. tax system, which would include tax cuts for both the corporate and personal side. A tax cut, if it in fact happens, may boost inflation in the short-term on the back on increased consumer/business spending during the late stages of the business cycle. However, this inflation implication is largely dependent on the nature of the tax cuts as well as the performance of the overall economy.

Factor Two: Muted GDP Growth

Average real GDP growth (YoY) remains relatively lackluster compared to past economic expansions, averaging only 1.7 percent between Q2 2009 and Q3 2017. This represents the smallest average gain in an economic cycle in the post-WW-II era. Again, given the current late cycle readings, along with rising labor costs and interest rates, as well as declining profits, it would be hard to imagine economic growth accelerating in the near future.

A complete discussion of the underlying components of GDP and the reasons for their relatively muted growth is beyond the scope of this report. It bears emphasizing, however, that the slow pace of GDP growth this cycle has restrained price pressures from building and thereby lowered the path of the fed funds rate relative to expectations.

Factor Three: Political Uncertainty

2016 was a volatile year for rate hike expectations as Brexit and the U.S. election caught markets and the FOMC off guard. For instance, before the Brexit vote in June of 2016, the fed funds Blue Chip Financial consensus in May looking to the end of 2016 was 0.90 percent; however, in the wake of the Brexit vote, the fed funds rate was estimated to be just 0.55 percent. In other words, the uncertainly caused by the Brexit vote rattled forecasters enough that the consensus estimate removed 1-2 rate hikes by the Federal Reserve for 2016. The subsequent U.S. presidential election swung the inflation expectation pendulum the other way, and thus the forecast for the Fed funds rates rose. Political elections and policy changes certainly have inflation implications, which feed into forecasters' predictions on how the FOMC will react to potential price pressures.

Factor Four: Tapering the Balance Sheet

Another potential factor behind the slower pace of rate hikes is the historically large size of the Fed's balance sheet. In hindsight, it is apparent that caution was required by the Fed as it sought to reduce its balance sheet while simultaneously hiking rates. With the plan to start shedding Treasuries and asset-backed securities in the midst of a tightening cycle, market participants feared disruptions to financial markets. However, in order to prepare markets, the Fed proceeded with caution. The slower pace of rate hikes was perhaps an indication that measures to reduce the balance sheet were on the horizon. Given the continued slow pace of economic growth and lack of inflation, it will be difficult for the FOMC to continue raising rates at their expected pace (as telegraphed via the 'dot-plot') while reducing the balance sheet. The Fed is more likely to reduce its balance sheet at its scheduled pace while raising rates at a more moderate pace.

The Outlook from Here

Most of these factors continue to occupy space in today's economic environment. Thus, we largely expect the FOMC to proceed along their policy tightening path, albeit at a more cautious and restrained pace. A clear disconnect in predicting the fed funds rate exists between the market consensus, as measured by fed funds futures, and the Fed's dot plot, which represents the FOMC members' beliefs of where the fed funds rate should be at the end of a given year. While the market consensus has historically been a better gauge of the actual rate in the future, both forecasts tend to overshoot the actual fed funds figure. As of now, we expect the Fed to raise rates in December, and just two more times in 2018.

RBNZ Unlikely to Reflect a Shift in Policy; Potential Dovish Interpretation for Dual Mandate

The Reserve Bank of Zealand will tomorrow complete its meeting on monetary policy with the interest rate decision and monetary policy statement due at 2000 GMT.

New Zealand's central bank is not expected to deliver a significant shift in monetary policy, maintaining its official cash rate at the record low of 1.75%. Tomorrow's meeting will also be the first with new Acting Governor Grant Spencer, who was assigned the role temporarily as the timing of the appointment coincided with the general elections held in September.

There are reports that the Labour-led government will review the Reserve Bank Act with the intent of proceeding with a dual central bank mandate and decision-making by committee. Should the RBNZ be given a dual mandate, then, similar to the US's Federal Reserve, besides price stability, full-employment will be one of the bank's objectives as well.

The new government today expressed that RBNZ's independence will be preserved and that the existing 1-3% inflation target would be maintained. This eased some market concerns earlier in the day and allowed the New Zealand dollar to advance relative to its US counterpart. However, Finance Minister Grant Robertson added that the rate hikes delivered in 2014 might have not taken place under a dual central bank mandate. Thus, should a dual mandate materialize, it might be perceived as of dovish nature by markets, pushing kiwi/dollar lower with potential support for the pair coming at around 0.6816, this being the one-and-a-half-year low that was recorded in late October.

It should also be mentioned that New Zealand's fundamentals are looking strong. Inflation came in at 1.9% y/y during the third quarter (exceeding expectations of 1.8% as well the previous quarter's 1.7%), while last week's better-than-anticipated jobs data pointed to a robust labor market. If the central bank acknowledges a strong macroeconomic environment in its statement then the kiwi might head higher relative to the greenback. In that case, the range around the 23.6% Fibonacci retracement level of the July 27 to October 27 downleg at 0.6987 might act as a barrier to the upside for kiwi/dollar.