Sample Category Title

EURGBP – Bears Eye Key Technical Supports

The cross remains in red for the third straight day and extends weakness below 0.8800 handle on Tuesday.

Pullback from 0.8938/34 peaks, where strong 1.75% rally last Thursday was capped by daily cloud base, so far retraced over 61.8% of 0.8732/0.8938 upleg, turning near-term focus lower.

Daily studies returned to full bearish setup on fresh weakness after recovery rally stalled, eyeing key supports at 0.8762 (200SMA) and 0.8732 (01 Nov low).

Break below 0.8732 would spark fresh extension of descend from 0.9306 (29 Aug peak) towards next strong support at 0.8692 (Fibo 61.8% of 0.8312/0.9306, Apr-Aug rally).

Broken daily Tenkan-sen (0.8844) marks solid resistance which is expected to limit upticks.

Res: 0.8821; 0.8844; 0.8882; 0.8921

Sup: 0.8791; 0.8762; 0.8745; 0.8732

U.S Tax Reform Optimism Fuels Markets

Tuesday November 7: Five things the markets are talking about

It's a very light week for the economic calendar.

In the U.S, today's JOLTS data will update job openings, which have been far exceeding hiring's. This is strong evidence that the U.S economy is at full employment.

Aside from a couple of central bank speeches (BoE's Carney 12:55 pm EDT and Fed Chair Yellen at 2:30 pm EDT), investors' focus returns to geopolitics as President Trump continues his tour of Asia and Saudi Arabia's ongoing crackdown on corruption.

The U.S. president is currently in S. Korea for the second leg of his five-nation Asia trip, with North Korea's nuclear threat at the heart of his agenda, which includes a bilateral meeting and joint press briefing with President Moon Jae-in and an address to South Korea's parliament.

1. Stocks record highs continue

Continued optimism over the prospect of U.S tax reform is feeding into global sentiment.

In Japan, the Nikkei index jumped to a near 26-year-high overnight, as foreign investors piled in on expectations of strong earnings from Japanese corporations, while Wall Street's strength supported this sentiment. The Nikkei share average closed +1.7% higher, while the broader Topix rallied +1.2%.

Down-under, commodities helped drive the Aussie stock indexes through its 2015 highs overnight. The S&P/ASX 200 rose +1%. While in South Korea, the market pulled back a bit further as Trump arrived. Early gains had faded and the Kospi closed out down -0.2%.

In Hong Kong, stocks hit a decade high on global optimism. The Hang Seng index rose +1.4%, while the China Enterprises Index gained +1.1%.

In China, blue chips scale a two- high, banking and energy firms lend support. The blue-chip CSI300 index rose +0.9%, the highest level since August 2015, while the Shanghai Composite Index closed up +0.7%.

In Europe, regional indices trade mixed coming off the earlier highs after a strong showing in Asia. Corporate earnings remain the dominant theme.

U.S stocks are set to open little changed (Flat).

Indices: Stoxx600 flat at 396.6, FTSE -0.2% at 7551, DAX +0.2% at 13491, CAC-40 flat at 5508, IBEX-35 -0.3% at 10291, FTSE MIB +0.2% at 23036, SMI -0.3% at 9258, S&P 500 Futures flat

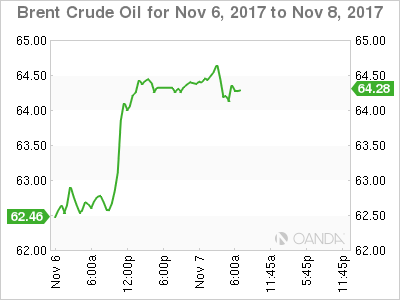

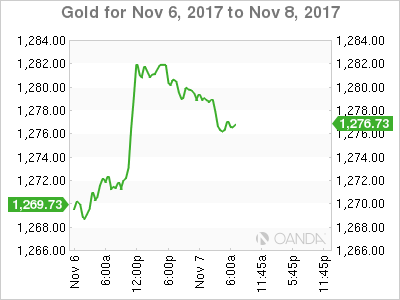

2. Oil hits highest level in two-years, gold lower

Oil prices hit their highest levels since July 2015 overnight as markets tightened, while Saudi Arabia's crown prince tightened his power through an anti-corruption crackdown that included high-profile arrests.

Brent crude futures are currently down -19c at +$64.08, having closed +3.5% higher yesterday, marking the biggest percentage gain in about six weeks. U.S West Texas Intermediate (WTI) crude is down -7c at +$57.28 a barrel.

Saudi Crown Prince Mohammed bin Salman has tightened his grip on power through an anti-corruption purge by arresting royals, ministers and investors. In the short term, no immediate change is expected in the oil policy of Saudi Arabia, which is the world's biggest exporter of crude oil. The Prince seems strongly committed to anchoring the OPEC agreement deep into 2018.

Elsewhere, there are ongoing signs of tightening market conditions. In the U.S, energy companies cut eight oilrigs last week, to 729, in the biggest reduction since May 2016. While there seems to be growing consensus amongst OPEC members to extend their pledge to hold back about -1.8m bpd beyond next March's deadline.

Ahead of the U.S open, gold prices have inched down as investors sell the 'yellow' metal to lock in some profits after it gained nearly +1% in yesterday's previous session on safe-haven buying following concerns over the arrests of some Saudi royal family members and ministers on corruption charges. Spot gold is down -0.2% at +$1,278.75 per ounce.

3. Sovereign yields in a tight range

NY Fed President Dudley (FOMC voter) is to retire in mid-2018 (as speculated over weekend). His 10-year term was scheduled to end in Jan 2019 and it now leaves four potential vacancies in 2018.

President Trump announced last week that Fed Governor Jerome Powell would be nominated to replace Janet Yellen when her term expires in February.

Note: Vice-Chairman Stanley Fischer retired in mid-October.

The yield on U.S 10-years has fallen-1 bps to +2.32%, the lowest in more than two weeks. In Germany, the 10-year Bund yield fell -2 bps to +0.34%, the lowest in eight weeks, while in the U.K, the 10-year Gilt yield declined – 2bps to +1.245%, the lowest in more than seven weeks.

4. Dollar rises on Tax optimism

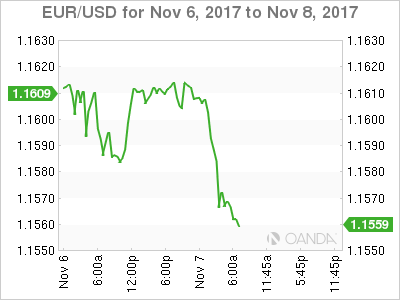

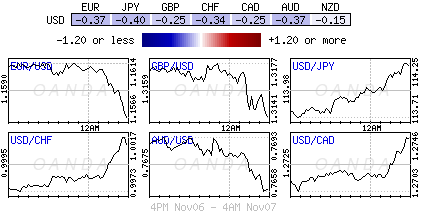

The 'mighty' USD continues to find support aided by investor optimism over the prospect of U.S tax reform. The EUR/USD hit a four-month low as the pair tested below €1.1570 as dealers cited low euro zone bond yields as one factor weighing upon the 'single' unit.

Note: Last month's the ECB decided to extend bond buying until at least September 2018, while the Fed by contrast is expected to raise interest rates next month.

USD/JPY is trading North of ¥114.25 aided by the highest close in the Nikkei in over 25-years.

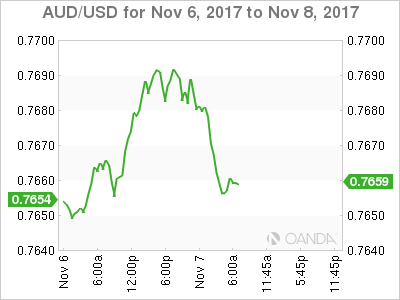

Down-under, the AUD (A$0.7656) ultimately weakened after last nights RBA statement. As expected, they left the O/N Cash Rate Target unchanged at +1.50%. Rates are continuing to support the economy, but higher exchange rate is expected to contribute to continued subdued price pressures – inflation is likely to remain low for some time. The RBA remains in wait-and-see mode.

5. Eurozone retail sales stronger than expected

Data this morning shows that Eurozone retail sales came in stronger than expected in September, up +0.7% on the month and +3.7% on the year.

Digging deeper, there was also a big revision that left July and August essentially flat, having previously been quite a bit lower.

Today's print is further proof that consumer spending is once again supporting robust growth in Q3. However, despite a long period of rising spending, there are as yet few signs of a sustained pickup in inflation, which again is confounding most Tier I Central Banks.

US Futures Flat Ahead of Fed Speeches

- EUR Continues Decline as Draghi Avoids Offering New Clues;

- Will Traders Be As Receptive to Yellen Commentary as Term Comes to an End?

- Traders Eye Poloz Comments For BoC Rate Clues.

After another day in which US equity markets set new records, futures are pointing to another flat open on Wall Street in the absence of much direction from Europe.

We'll hear from a variety of central bankers throughout the day, including the heads of three of the most closely followed at the moment, the Federal Reserve, ECB and Bank of Canada. All three central banks have been actively engaged in tightening monetary policy over the course of this year, to different extents, which makes these interviews and speeches all the more important.

Mario Draghi, the ECB President, was first up this morning but his speech was more focused on banking supervision. Draghi did touch on negative interest rates but not in the context of how it will impact monetary policy decisions going forward. The euro is coming under a little pressure this morning but it's unlikely to be related to Draghi's words or the data we've had, for that matter, with retail sales having actually exceeded expectations in September. This morning's moves in the euro simply appear to be an extension of the initial post-ECB meeting decline, following a brief period of consolidation. The euro may run into further support around 1.1450 – 1.15 against the dollar in the near term but further downside could follow in the weeks and months ahead.

Two Fed policy maker are due to make an appearance today, Janet Yellen the outgoing Chair and Randal Quarles, who recently joined the Board of Governors. Typically it would be Yellen's comments that would be of most interest but under the circumstances, it may be Quarles that most are interested in hearing from. Yellen's term will end in February and a rate hike in December is almost entirely priced in, leaving us with little to potentially take from her message, especially given the number of positions still to be filled on the board.

The BoC's decision to raise interest rates at two consecutive meetings in July and September and follow this with, what was at least perceived to be, a dovish stance after the meeting last month has raised many questions about how many further rate hikes we can expect going forward. While the central bank has stressed its data dependent stance due to the sensitivity of the economy to different factors, Governor Stephen Poloz may today offer some insight into how things have progressed since and how many rate hikes we can expect over the coming 12 months, if the economy performs as expected.

Once again the week is looking a little quieter from a data perspective and the same is certainly true today. The only notable release from the US will be JOLTS job openings, although given recent moves in oil markets, API crude inventory data will also likely be closely monitored.

USDJPY Still Bullish Above 114.25 Level

The U.S dollar has recovered upside momentum against the Japanese yen, after briefly dipping to the 113.68 level on Monday. Price-action currently trades around the key 114.24 level, as the U.S dollar index starts to erase early week trading losses. The USDJPY pair should now be driven by global stock markets and technical trading, as we see a lack of high-impact economic data releases on the United States trading docket this week.

The USDJPY pair remains intraday bullish while trading above the 114.24 technical level, further upside toward the 114.50 and 114.75 levels seems most likely.

Should price-action fail to break above the 114.24 level, sellers will likely push the pair towards the 113.90 and 113.68 levels. Extended intraday support is found at the 113.33 and 112.90 levels.

EURUSD Strongly Bearish Below 1.1572 Level

The euro has further weakened against the U.S dollar during Tuesday's European trading session, hitting a new four-month price-low against the greenback, at 1.1558. The EURUSD pair broke below the key 1.1572 support level earlier, as Mario Draghi choose to focus on the European banking sector rather than monetary policy in his opening remarks in Frankfurt, Germany. Traders will now look to a key-note speech from FED Chair Janet Yellen, during the U.S trading session later today.

The EURUSD pair remains strongly bearish while trading below the 1.1572 technical level. Further losses are expected towards the 1.1533 and 1.1509 levels.

Should price-action break back above the 1.1572 technical level, further upside towards 1.1598 and 1.1640 seems most likely.

GBP/NZD Cup With Candle Pattern on H1 Chart

The GBP/NZD is consolidating within the cup with handle pattern and we might see a breakout as there is also a trend line confluence. If the price spikes above the trend line/ EMA89 /D H4 / ATR pivot -1.9035 and/or we see a 4h close above the level the price might continue its move towards 1.9095 and 1.9145. Below 1.8970 (D H1, atr pivot, trend line) we might see 1.8920, 1.8886 and 1.8825. Watch for camarilla levels and have in mind that this pair - the GBP/NZD (also know as "The Beast") is very volatile so once you are in profit, you should protect it by using profit stops.

- H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

- W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

- D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

- D L3 - Daily Camarilla Pivot (Daily Support)

- D L4 - Daily H4 Camarilla (Very Strong Daily Support)

- PPR - Progressive Polynomial Channel

- POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

DAX Unchanged on Mixed German Reports

The DAX has ticked lower in the Tuesday session. Currently, the DAX is at 13,472.75, down 0.02% on the day. On the release front, German Industrial Production plunged 1.6%, much weaker than the forecast of -0.7%. Eurozone consumer spending numbers were mixed. Retail PMI slowed to 51.1, down from 52.3 in the previous reading.

German Industrial Production surprised the markets with a dismal reading in September. The indicator declined 1.6%, its worst reading in 2017. This release comes on the heels of Factory Orders, which posted a gain of 1.0%, compared to a decline of -0.1%. Eurozone retail sales reports were mixed on Tuesday. Retail PMI came in at 51.1 in October, pointing to muted expansion in the retail sector. There was much better news from September retail sales, as gain of 0.7% came after two straight declines, and was the strongest gain since February. The markets are hoping for strong euorozone consumer spending in the fourth quarter, given the robust German economy and stronger economic conditions in the eurozone.

German coalition talks are moving slowly, although the unhurried pace has not adversely impacted the robust German economy. However, preliminary talks between Angela Merkel's conservative bloc and two small parties have not shown much progress, with sharp disagreements over immigrant policy and other issues. Merkel has her work cut out for her, but she is a seasoned negotiator, and will likely be able to cobble together a coalition.

Donald Trump suffered a humiliating defeat with his health care proposal, and the President has now set his sights on tax reform. Trump wants Congress to pass legislation overhauling the tax code before the end of the year, but that will be a tall order, as most Democrats have come out against the proposal, and not all Republicans are on board. The bill would cut corporate taxes from 35% to 20%, but predictably, Democrat and Republican lawmakers are at odds as to whether the bill will lower taxes for the middle class. Expectations that Trump will cut taxes has been the catalyst for a stock market rally over the past year, and if the bill does become law, the US dollar will likely gain ground.

Euro Dips To 14-Week Low On Soft German Mfg. Report

The euro has recorded losses in the Tuesday session. Currently, EUR/USD is trading at 1.1566, down 0.37% on the day. The pair remains under pressure, and has dropped to its lowest level since mid-July. On the release front, German Industrial Production plunged 1.6%, a sharper drop than the forecast of -0.7%. Eurozone consumer spending numbers were mixed. Retail PMI slowed to 51.1, down from 52.3 in the previous reading. Retail Sales rebounded with a gain of 0.7%, edging above the forecast of 0.6%. In the US, today’s highlight JOLTS Job Openings, which is expected to soften to 5.98 million. As well, Fed Chair Janet Yellen will deliver remarks at an event in Washington.

Eurozone retail sales reports were mixed on Tuesday. Retail PMI came in at 51.1 in October, pointing to muted expansion in the retail sector. There was much better news from September retail sales, as gain of 0.7% came after two straight declines, and was the strongest gain since February. The markets are hoping for strong euorozone consumer spending in the fourth quarter, given the robust German economy and stronger economic conditions in the eurozone.

Donald Trump suffered a humiliating defeat with his health care proposal, and the President has now set his sights on tax reform. Trump wants Congress to pass legislation overhauling the tax code before the end of the year, but that will be a tall order, as most Democrats have come out against the proposal, and not all Republicans are on board. The bill would cut corporate taxes from 35% to 20%, but predictably, Democrat and Republican lawmakers are at odds as to whether the bill will lower taxes for the middle class. Expectations that Trump will cut taxes has been the catalyst for a stock market rally over the past year, and if the bill does become law, the US dollar will likely gain ground.

The Greenback Extends Gains Amid Tax Plan Hopes And European Political Jitters

RBA maintains its wait-and-see approach

The US dollar extended gains against all of G10 currencies on Tuesday. The gains were quite limited as investors awaited several key speeches today. Draghi will speak at GMT 9 am, while across the Atlantic Poloz (BoC) will give a press conference this evening. In Australia, the central bank (RBA) held the Cash Rate Target unchanged at record low 1.5%. Governor Lowe made few changes to the statement and maintained its growth forecast of around 3% over the few next year. The RBA also expressed its concerns about the weakness in inflation (CPI eased to 1.8%y/y in the third quarter, down from 1.9% in the previous one) and reiterated its warning that further strength of the Aussie could only worsen the situation.

The Reserve Bank of Australia finds itself in a tricky place, as the economy kept improving and reducing its dependence to the mining sector, while on the other hand a few indicators such as inflation and retail sales are sending mixed signals. The RBA will wait patiently on the sidelines for a long-time. The market is not pricing any rate hike before at least the end of the summer 2018. Against such a backdrop, the risk is significantly skewed to the downside in AUD/USD. However, upside risk is not zero as an positive surprise in inflation together with another disappointment regarding Trump tax plan could trigger an AUD rally.

AUD/USD is currently testing the key 0.76-0.77 area and has been unable to validate a break of the $0.77 resistance (200dma). The USD rally is losing steam amid a lack of positive news in the US. Therefore, a return towards $0.78 appears likely in the short-term. In the longer-term, we maintain our bearish view.

Political risk rise in Europe

Political risk have again picked up in Europe prompting a stark sell of in Euro. In Italy the center-right coalition led by former Italian Prime Minister Berlusconi solidly won regionals elections in Sicily. With over 90% of the ballot counted, Nello Musumeci took 40% of the vote over 5-Star candidate Giancarlo Cancelleri impressive 35%. The elections was viewed by many as a litmus test for next year’s Italian national elections. The turnout for both antiestablishment parties’ indicates the reactionary vote remain influential. EURUSD bearish momentum continues hitting 1.1566 low.

Clearly the concern is fragmentation of the EU as Italians in poll have shown the highest dislike and preference to leave the EU of any member nation. However, a portion of the move should be attributed to broader FX risk aversion (migrating into USD), while equities continue to power ahead. Yet our midterm view this that European Union convergence has move past the “event horizon”. This unified union will be able to keep Italy in folds and therefore we would fade short-term risk volatility. This view, will be reinforced by further strengthening in the European economy. German Industrial production fell 1.6% in September greater then markets expectations of 0.9%. The slowdown can be attributed to broader weakness in European leading indicators after significant acceleration. We suspect the weak read will be short lived an ECB loose monetary policy and solid outlook for global economy will support output growth.

Switzerland FX Reserves hit record high

This morning has been released the Swiss FX reserves for October. The data increased strongly to $741.5 billion from $724.4billion. The reserves hit a clear record high.

The SNB balance sheet continues to expands, meaning that the SNB still believes the CHF is overvalued, or at least that upside risks on the CHF are strong. The FX reserves are coming from money creation in other words the central bank’s debt. It is clear that as long as global monetary policy remains loose, the Swiss FX reserves will continue climbing and increase the SNB exposure to global economic conditions.

The EURCHF is below 1.16 and the EUR remains the main driver. The strong Quantitative easing from the European Central Bank continues at least until September 2018 and this is still posing threat to the Swiss stability. The inflation, that seems to be back in the US, has slowed unexpectedly in Europe in October preventing a bigger change of the ECB monetary policy. A stronger European inflation would definitely help to clear some pressures off the CHF.

Technical Outlook: Spot Gold Eases After 20 SMA Repeatedly Capped Upside Attempts

Spot Gold price eases on Tuesday on profit taking after nearly 1% rally on Monday on safe-haven buying.

Upside attempts were repeatedly capped by 20SMA (currently at $1281) which marks strong barrier as previous probes above it were short-lived.

Near-term action remains within $1263/84 range which extends into third week, with range floor marking significant support, reinforced by Fibo 61.8% of $1204/$1357 upleg and rising 200SMA.

Mixed daily studies show no clear direction, with today's action holding between 10 and 20SMA's ($1274 / $1281 respectively) which mark initial pivots.

Break below 10SMA is needed to turn near-term bias lower and risk retest of $1263 base.

Conversely, sustained break above 20SMA would improve near-term outlook for stronger upside action towards targets at $1284 and $1289 (Fibo 50% and 61.8% respectively of $1306/$1263 downleg).

Res: 1281, 1284, 1289, 1291

Sup: 1274, 1271, 1266, 1263