Sample Category Title

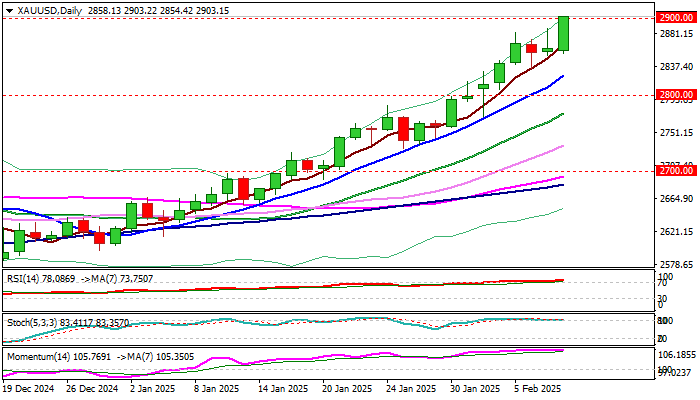

Gold: How Far Can the Bulls Go?

- Gold extends record bull run, touches $2,900 psychological level.

- Overbought signals are evident, but there is support at $2,850-$2,870.

Gold has been on a relentless bull run, posting only eleven days of minor losses since the ongoing upleg began in mid-December.

The price is currently testing the $2,900/ounce round level after opening the week with a bang, but the real challenge would be to maintain support above the channel’s upper band at $2,870 and the $2,850 base. If that proves to be the case and the bulls successfully claim the $2,900 ceiling too, the rally could continue towards the $2,950-$2,970 region where the 161.8% Fibonacci extension of the previous downfall and the resistance line, which joins the April and October 2024 highs, are sitting.

However, a warning note from the technical indicators should not be ignored. The RSI and stochastic indicators are both firmly in overbought territory, signaling that the road ahead could get choppy. Nevertheless, only a dive beneath $2,850-$2,870 could activate selling orders towards Thursday’s low near $2,830 or closer to the channel’s lower band currently seen near $2,813. Then, October’s peak of $2,790 and the 20-day simple moving average (SMA) near $2,770 could be the next destination. A break lower would neutralize the medium-term picture.

In summary, gold seems poised for another potential surge, but the key to a continuation higher lies in holding above $2,850-$2,870. If the bulls can maintain their grip here, a fresh wave towards higher levels could be on the cards.

XAU/USD: Gold Hits New Record High Above $2,900

Gold was top performer during early Monday trading after new tariff threats from President Trump fueled fears about global trade war and sparked fresh safe haven demand.

Bulls cracked psychological $2900 barrier and hit new record high, in 1.5% advance during Asian / early European trading.

Technical picture remains firmly bullish, although overbought conditions on daily chart warn that the price action may slow for consolidation.

Dips are likely to be shallow, as bullish sentiment remains strong.

Sustained break above $2900 to generate fresh signal and expose targets at $2946 and $2983 (Fibo projections), en route towards key barrier at $3000 (psychological).

Res: 2916; 2946; 2983; 3000.

Sup: 2886; 2865; 2850; 2825.

XBRUSD: Technical and Fundamental Outlook

Crude oil starts the week with moderate gains after three consecutive weeks of losses. Tensions in the Middle East have escalated after the U.S. imposed new sanctions on individuals and vessels involved in exporting Iranian crude to China, which could impact global supply. However, gains are limited by concerns that Trump’s tariffs on steel and aluminium may slow global economic growth and reduce energy demand. Additionally, a stronger U.S. dollar is adding downward pressure on the market.

Key factors to monitor this week:

- Sanctions on Iran: Increased pressure on Iranian exports could tighten global supply.

- U.S.-China trade tensions: New tariffs may impact economic growth and energy demand.

- Strength of the U.S. dollar: A stronger dollar makes crude more expensive for international buyers.

- Russia-Ukraine negotiations: Any progress in talks between the U.S. and Russia could influence the market.

Outlook: The market remains uncertain. A decisive move will depend on the evolution of sanctions and the real impact of trade tariffs on demand.

Technical Analysis

XBRUSD, H2

- Supply Zone (Sell): 76.00

- Demand Zones (Buy): 74.51 and 74.91

Last week, the price formed a double bottom around 74.00, with the most recent validated intraday resistance at 76.47. This suggests that the bearish bias remains intact unless this level is broken.

The recent upside followed a moderate bearish reaction from Thursday’s supply zone near 74.70, leading to a bullish gap at the open this week. This triggered a correction, leaving two local demand zones at 74.51 and 74.91. As long as the price stays above these levels, a rebound toward the volume node around 76.00 is likely.

Selling pressure may resume near 76.00, targeting intraday levels at 74.00 and 73.11, with potential for a broader decline toward 73.00 and 72.55 in a swing move.

Technical Summary:

- Corrective Bullish Scenario: Buying above 74.51 (waiting for the gap to be filled) with targets at 76.00.

- Bearish Continuation Scenario: Selling below 76.00 (waiting for a new rebound) with targets at 74.00, 73.71, 73.00, and 72.55.

Uncovered POC: POC = Point of Control: The level or zone where the highest volume concentration occurred. If a downward move followed this level, it is considered a selling zone and forms resistance. Conversely, if an upward move followed, it is a buying zone, usually located at lows and forming support areas.

Can. Dollar Shrugs After Strong Can. Jobs Report

The Canadian dollar is drifting on Monday. In the European session, USD/CAD is trading at 1.4334, down 0.11% on the day.

Canada’s employment blows past market estimate

Canada posted stronger-than-expected growth on Friday, but the Canadian dollar showed little reaction. The economy created 76 thousand jobs in January, crushing the market estimate of 25 thousand and following a December gain of 90 thousand. This marked the sixth straight monthly increase as the labor market remains strong despite a weak ecconomy. The unemployment rate dipped to 6.6%, down from 6.8% and below the market estimate of 6.7%.

The jobs numbers were positive but hanging over the report is the risk of a trade war with the United States, which was narrowly avoided last week, when the US imposed and then suspended tariffs against Canada. President Trump suspended the tariffs for 30 days and the Bank of Canada’s next rate decision on March 12 will depend on economic data and whether the tariffs are reinstated.

US nonfarm payrolls miss estimate

US nonfarm payrolls eased to 143 thousand in January, shy of the market estimate of 175 thousand. Still, there weres signs of strength in the labor market – nonfarm payrolls were revised by 100 thousand in the previous two months and the unemployment rate ticked lower to 4% from 4.1%, below the market estimate of 4.1%. Average hourly earnings rose 0.5%, up from 0.3% in December and above the market estimate of 0.5%. Annually, average hourly earnings rose 4.1%, unchanged from the revised December reading and above the market estimate of 3.8%. The generally positive employment report supports the case for the Federal Reserve continuing to hold rates, possibly until the third quarter.

USD/CAD Technical

- USD/CAD is testing support at 1.4333. Below, there is support at 1.4304

- There is resistance at 1.4375 and 1.4404

Eurozone Sentix rises to -12.7, but inflation keeps ECB in check

Eurozone investor sentiment showed signs of improvement in February, with the Sentix Investor Confidence Index rising from -17.7 to -12.7, surpassing expectations of -16.4. This also marks the highest reading since July 2024, signaling a tentative shift in market sentiment. Current Situation Index also improved, climbing from -29.5 to -25.5, while Expectations Index made an even more notable leap from -5 to 1, also reaching its highest level since July last year.

Sentix noted that the Eurozone economy is "trying to emerge from the crisis," with some early signs of stabilization. However, Germany’s economic struggles continue to act as a drag on the broader region, described as a "lead weight" on the bloc's recovery. Despite this, optimism is growing that a potential shift in German leadership could usher in a more pro-business policy stance, which could help lift economic prospects in the months ahead.

One key takeaway from the report is the diminishing likelihood of aggressive monetary easing from ECB. With investor sentiment improving and the economic outlook brightening, "hopes of more significant support measures from the ECB are also dwindling."

Inflation outlook remains a lingering concern, preventing ECB from committing to deeper rate cuts. Sentix’s "Inflation" theme index remained at -11 points, signaling persistent price pressures.

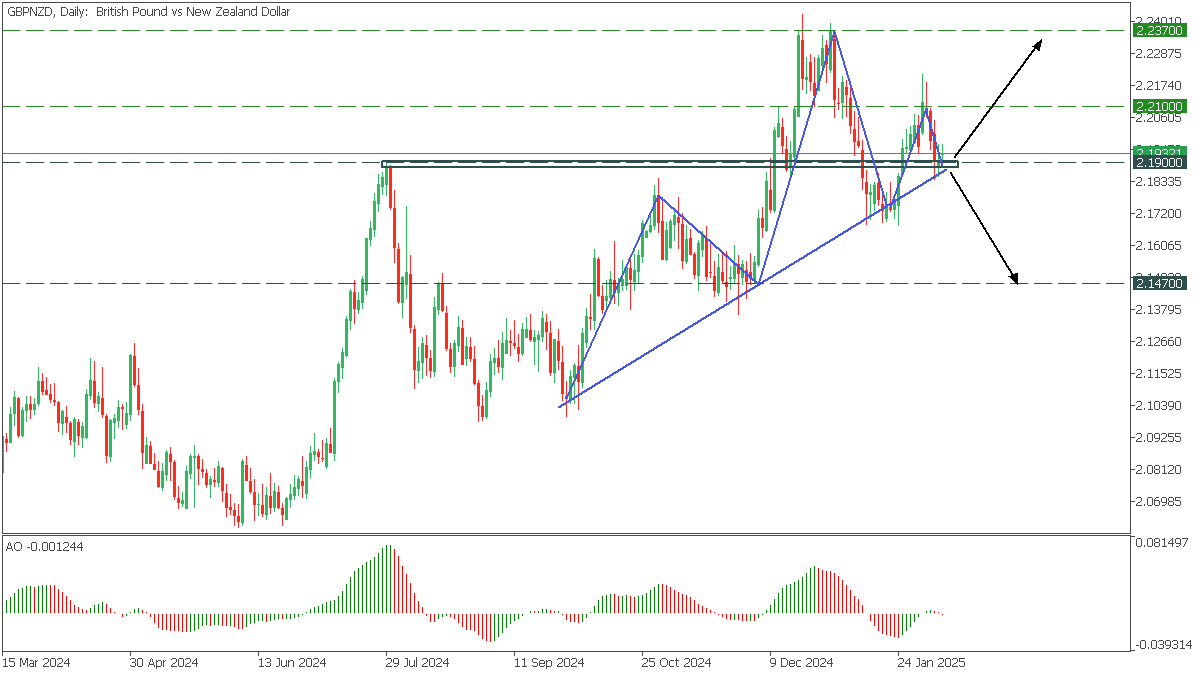

GBPNZD: Head and Shoulders

GBPNZD, Daily

In the Daily timeframe, GBPNZD has formed a head and shoulders pattern. Price has fallen towards the neckline, testing a substantial support area, with the AO again indicating a rising bearish sentiment.

- A break of support below 2.1900 will drop the price to 2.1470;

- A rebound from support will take GBPNZD back to 2.2100 and further to 2.2370;

AUD/USD & NZD/USD Rebound: Signs of Trend Shift?

AUD/USD started a decent increase above the 0.6200 and 0.6240 levels. NZD/USD is also rising and might aim for more gains above 0.5700.

Important Takeaways for AUD USD and NZD USD Analysis Today

- The Aussie Dollar rebounded after forming a base above the 0.6100 level against the US Dollar.

- There was a break below a connecting bullish trend line with support at 0.6255 on the hourly chart of AUD/USD at FXOpen.

- NZD/USD is consolidating gains above the 0.5600 zone.

- There is a key declining channel forming with resistance at 0.5680 on the hourly chart of NZD/USD at FXOpen.

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair started a fresh increase from the 0.6090 support. The Aussie Dollar was able to clear the 0.6170 resistance to move into a positive zone against the US Dollar.

There was a close above the 0.6240 resistance and the 50-hour simple moving average. Finally, the pair tested the 0.6300 zone. A high was formed near 0.6301 and the pair recently saw a minor pullback.

There was a move below the 0.6300 level. The pair declined below the 23.6% Fib retracement level of the upward move from the 0.6088 swing low to the 0.6301 high. Besides, there was a break below a connecting bullish trend line with support at 0.6255.

On the downside, initial support is near the 0.6240 level. The next major support is near the 0.6195 zone or the 50% Fib retracement level of the upward move from the 0.6088 swing low to the 0.6301 high.

If there is a downside break below the 0.6195 support, the pair could extend its decline toward the 0.6170 level. Any more losses might signal a move toward 0.6090.

On the upside, the AUD/USD chart indicates that the pair is now facing resistance near 0.6270. The first major resistance might be 0.6300. An upside break above the 0.6300 resistance might send the pair further higher.

The next major resistance is near the 0.6335 level. Any more gains could clear the path for a move toward the 0.6380 resistance zone.

NZD/USD Technical Analysis

On the hourly chart of NZD/USD on FXOpen, the pair started a steady increase from the 0.5515 zone. The New Zealand Dollar broke the 0.5600 resistance to start the recent increase against the US Dollar.

The pair settled above 0.5630 and the 50-hour simple moving average. It tested the 0.5700 zone and is currently correcting gains. The pair corrected lower below the 0.5660 level. However, the bulls are active above the 0.5630 level.

The NZD/USD chart suggests that the RSI is now moving higher toward 50. On the upside, the pair might struggle near 0.5660. The next major resistance is near the 0.5680 level. There is also a key declining channel forming with resistance at 0.5680.

A clear move above the 0.5680 level might even push the pair toward the 0.5700 level. Any more gains might clear the path for a move toward the 0.5750 resistance zone in the coming days.

On the downside, immediate support is near the 0.5630 level. The first key support is near the 50% Fib retracement level of the upward move from the 0.5516 swing low to the 0.5702 high. The next major support is near the 0.5560 level.

If there is a downside break below the 0.5560 support, the pair might slide toward the 0.5515 support. Any more losses could lead NZD/USD in a bearish zone to 0.5440.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Hang Seng Index Hits Four-Month High Amid DeepSeek’s Success

As shown in the Hang Seng (Hong Kong 50 on FXOpen) chart today, the index has risen above the 21,500 mark for the first time since October 2024.

According to Reuters, bullish sentiment is fuelled by optimism surrounding the success of the DeepSeek startup. Leading gainers include tech stocks:

→ Chipmaker Cambricon Technologies surged 6.2%;

→ AI firm CloudWalk Technology hit the 20% upper limit;

→ Major telecom operators China Mobile, China Unicom, and China Telecom also saw gains after announcing their collaboration with DeepSeek’s open-source model to "promote the inclusive adoption of cutting-edge AI technologies."

Analysts at China Securities believe the uptrend could persist until the second half of March.

Technical Analysis of the Hang Seng Chart

Applying Fibonacci retracement levels using the August low (A) and the October 2024 high (B), we can see how these levels acted as temporary support (marked with arrows) as the price retraced to the January low (C).

In the most optimistic scenario:

→ The rally over the past three weeks may signal the resumption of the A→B uptrend;

→ Based on Fibonacci proportions, bulls may target the 1.618 extension of the initial move, implying a potential price level 61.8% higher than the previous peak.

This suggests a possible target around 25,520, though this appears somewhat ambitious for the Hang Seng (Hong Kong 50 on FXOpen) given:

→ Rising inflation in China—today’s data shows the annual CPI climbed from 0.1% (previous reading) to 0.5%;

→ The prospect of escalating tariff tensions with the US after China retaliated against Trump’s 10% tariffs on Chinese imports.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Announcements on New Tariffs Subject to Law of Diminishing Returns

Markets

Friday’s US payrolls solidified the Fed view that it can sit back and wait as the US economy is in a good place. Headline US job growth at 143k was slightly softer than expected (175k), but came with a cumulative upward revision (Nov and Dec) of 100k. The household survey also was strong. The unemployment rate declined from 4.1% tot 4.0% even as the participation rate rose to 62.6% from 62.5%. Wage growth was stronger than expected, jumping 0.5% M/M to 4.1%. Later, the U. of Michigan consumer confidence declined modestly, but inflation expectations measures reaccelerated with especially the 1-y head measure jumping sharply from 3.3% to 4.3%! The release only reinforced the post-payrolls rebound in US yields. Yields closed between 7.7 bps (2-y) and 5.6 bps (30-y) higher. The move aborted a tentative downside drift in US yields (fear for US growth) of late. US money markets now fully discount a next Fed rate cut in September with only 50% of a second step priced for December. The ECB study on the potential level of a neutral policy rate didn’t yield much news. It is still estimated between 1.75% and 2.25%, but the report downplays its relevance in making day-to-day decision on monetary policy. German yields closed the session with changes of less than 2.0 bps across the curve. Higher yields, especially after the U. of Michigan inflation expectations, release weighed on equities. US indices declined between 1.0% (S&P/Dow) and 1.36% Nasdaq. The dollar gained, albeit modestly (DXY close 108.04, EUR/USD 1.033), leaving the recent range intact. The yen again slightly outperformed (close USD/JPY little changed 151.4).

Market headlines this morning are ‘dominated’ by US president Trumps’ intention to impose tariffs of 25 % on all imports of steel and aluminum to the US. However, it is still uncertain when the duties will take place. Apparently, announcements on new tariffs also are becoming subject to the law of diminishing returns as the market reaction remains guarded and orderly. US yields are little changed, even marginally softer this morning. Asian equities are trading mixed. US and EMU futures even gain marginally. The dollar gains modestly (DXY 108.23, EUR/USD 1.0315).

The eco calendar in the US and EMU is thin today. Later this week, we look out for the US CPI (Wednesday) and retail sales (Friday). Fed Chair Powel will appear before Congress on Tuesday and Wednesday. For now, there is no reason for him to leave the wait-and-see, higher for longer bias. The US Treasury with also execute the early month 3-y, 10-y and 30-y auction series during the week. US yields, especially at the short end of the curve, remain well supported. The USD reaction function looks like becoming a bit more stoic, especially on trade war headlines and to a lesser extent on strong US data. EUR/USD is looking for direction in a 1.02/1.05 ST trading range.

News & Views

Rating agency Fitch affirmed the Belgian credit rating at AA-, but sticks with its negative outlook which is already in place for two years. The outlook reflects the ongoing uncertainty regarding the new government’s ability to reduce the deficit as planned and stabilize the debt path. The rating agency cites two potential triggers for a rating downgrade. First, failure to formulate a credible fiscal consolidation strategy that would lead to stabilisation of government debt-to-GDP over the medium term. Second, evidence that diverging labour costs from trading partners will lead to a persistent deterioration in international competitiveness, putting pressure on Belgium's medium-term growth prospects. Fitch maintains its budget deficit forecast of 4.8% of GDP in 2025 and 4.7% in 2026, but medium-term projections have slightly improved. The debt ratio is estimated at 103.7% of GDP end-2024 and expected to keep rising to 107.9% of GDP by 2026. The Belgian economy is expected to grow by 1.2% this year and by 1.4% in 2026 but downside risks persist, particularly from US tariff hikes. Rating agencies Moody’s (Aa3, negative outlook) and S&P (AA, stable outlook) give their first updates of the year on April 11 and April 25.

Chinese January inflation rose for the first time since August 2024. The 0.7% M/M gain pushed the annual inflation figure up from 0.1% to 0.5% Y/Y, slightly above consensus (+0.4%). Core inflation, stripping out food and energy prices, rose from 0% Y/Y to 0.6% Y/Y with services rising by 1.1% Y/Y. The pick-up in inflation was likely driven by a temporary spending boom around the Lunar New Year celebrations and is not the start of a turnaround. More volatility (and a setback) is likely next month because of the high comparison base related to the (later) timing of Lunar NY in 2024. Chinese producer prices remain mired in deflationary territory (unchanged at -2.3% Y/Y) since September 2022.

New Week, New Threats

Another week starts with tariff threats. This time, everyone that applies tariffs to the US will be hit back with the same tariffs, and all aluminium and steel imports to the US – no matter from whom – will face a 25% tariff. Mood this Monday in Asia is pretty mixed – to say the least. Aluminum and iron ore futures are slightly down, the US dollar index is up and the commodity currencies like Aussie and Loonie opened the week with a gap but the AUDUSD recovered early losses. The swift recovery in Aussie was certainly due to the encouraging Chinese data that showed that inflation advanced to the highest level in five months thanks to increased spending during the Chinese New Year holiday. Australian equities are not particularly welcoming the fresh tariff news, while FTSE futures are slightly up. The rebound in oil prices on fresh US sanctions on Iranian crude exports and encouraging Chinese inflation data help counterweigh the negative impact of softer metal prices. As per oil, good news from China could throw a solid floor under the US crude selloff after the price of a barrel approached the $70pb psychological level last week and rebounded from there.

Anti-goldilocks

Friday’s jobs data from the US was all but ideal for the so-called goldilocks scenario. The US posted slower-than-expected nonfarm payrolls and acceleration in wages growth in January. The annual revision to the nonfarm employment on the other hand was just less than 600K jobs – as expected. The combination of slower job additions with higher wages didn’t enchant the Federal Reserve (Fed) doves. The US 2-year yield jumped to flirt with the 4.30% mark as the 10-year yield advanced past the 4.50% level. Plus, the share of foreign-born workers in the US kept climbing last year but these jobs are at risk under Trump administration.

Plus, the latest data from the Fed on Friday showed alarming rise in household debt, credit card delinquencies remain strong. As such, it’s hard to guess what’s the best thing to do for the Fed. All eyes will be on Fed Chair Jerome Powell’s semi-annual testimony on Tuesday and Wednesday. For now, the Fed is expected to keep the rates unchanged at least until June – and a June rate cut is a coin toss.

Overall, US’ exceptional growth story is based on exploding private and public debt. Trump’s plans for mass deportation and sizeable tariffs hint at uptick in US inflation in the coming months. Not helping are the California wildfires that are expected to cause a jump in new and used car prices, and the bird flu which is sending egg prices soaring. As a result, a stronger-than-expected set of inflation data this week – and/or a cautious stance from Powell should keep the US dollar in demand and weigh on risk appetite.

Speaking of appetite

Equity indices didn’t like the anti-goldilocks jobs report last Friday. The S&P500 retreated 0.95% while Nasdaq 100 fell 1.30%. Magnificent 7 earnings were robust but not ‘magnificent’ with slowing growth / high AI spending. Mag7 ETF slid 2% on Friday and 2.41% throughout the week.

In Europe, Friday saw the European Stoxx 600 give back some gains too. On the data front, Germany posted a record trade surplus with the US. The timing is bad, as Trump is out and pointing his finger to Europe, as well. Consequently, the tariff threats remain on the back of investors’ minds in Europe and Germany will be on the front line of a potential transatlantic trade war. But that worry is not dominating the price action so far. On the contrary, the convergence trade between Europe and the US remains in full play. The S&P500 is up by a meagre 2% since the year started while the Stoxx 600 was up by almost 7% on Friday’s close. The divergence between the Fed and European Central Bank (ECB) expectations remains supportive of the convergence trade, but doesn’t change the fact that the European companies’ face dull economic outlook and instable political landscape. The EURUSD was aggressively sold on Friday and again at the Asian open. Losses have been mostly reversed at the time of recording but the EURUSD outlook remains negative on the back of diverging Fed / ECB policy outlooks and strong resistance is seen into the 50-DMA, a touch higher than the 1.04 psychological mark.