Sample Category Title

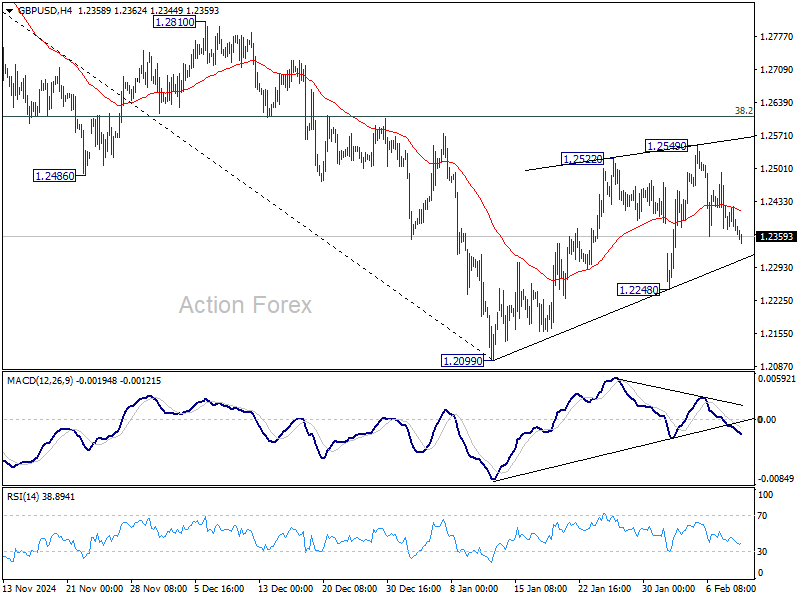

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2341; (P) 1.2381; (R1) 1.2408; More...

Intraday bias in GBP/USD remains neutral and outlook is unchanged. While corrective rebound from 1.2099 might still extend, upside should be limited by 38.2% retracement of 1.3433 to 1.2099 at 1.2609. On the downside, break of 1.2248 support will bring retest of 1.2099 low. Firm break there will resume whole fall from 1.3433. However, decisive break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

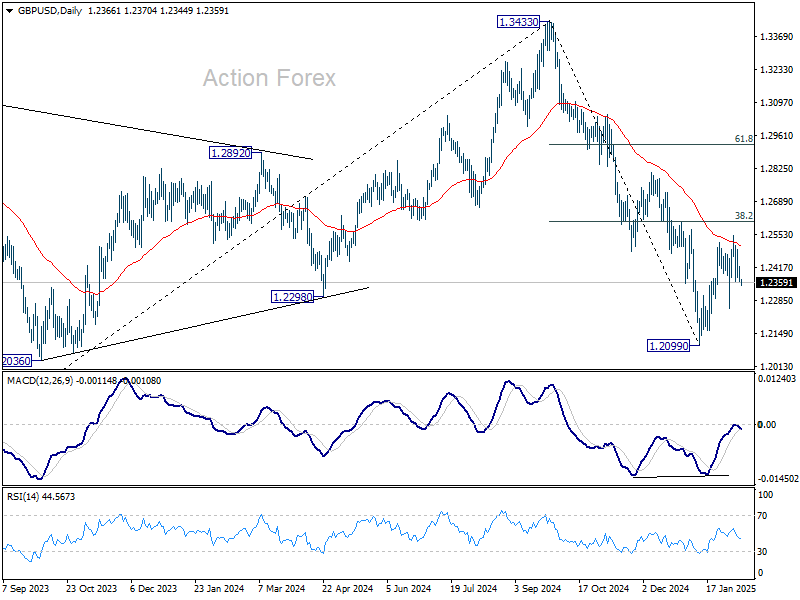

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

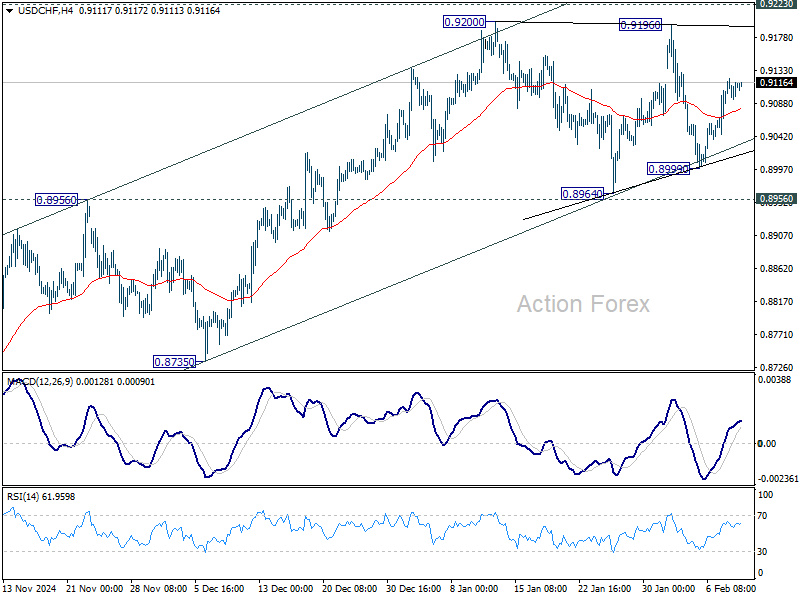

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9098; (P) 0.9110; (R1) 0.9127; More…

Intraday bias in USD/CHF remains neutral as consolidations continue below 0.9200. Outlook stays bullish with 0.8956/64 support zone intact. On the upside, firm break of 0.9200/9223 will resume the whole rally from 0.8374 and carry larger bullish implication. However, sustained break of 0.8964 will be a sign of reversal and turn bias back to the downside.

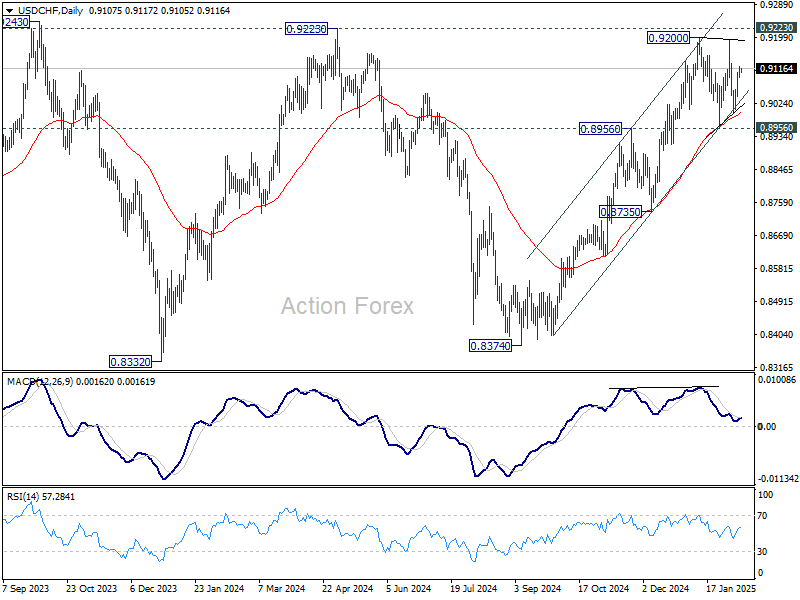

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

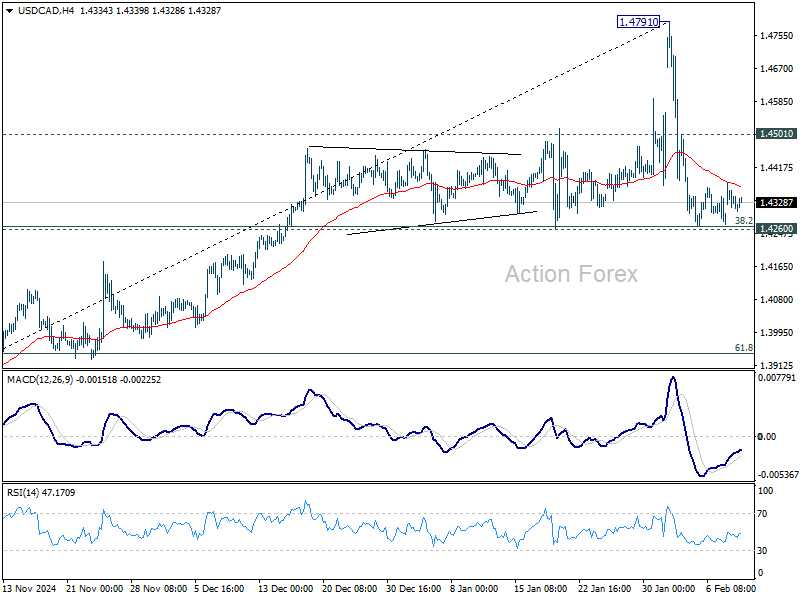

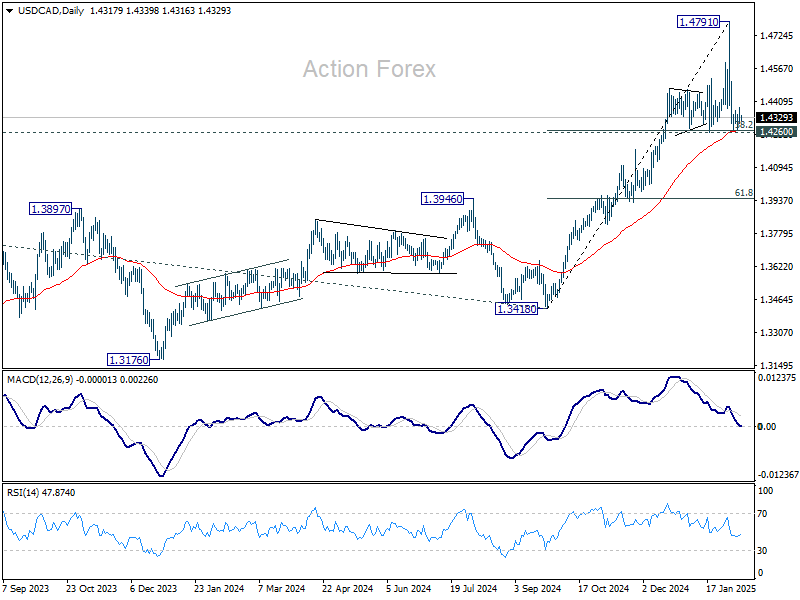

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4287; (P) 1.4334; (R1) 1.4363; More...

No change in USD/CAD's outlook and intraday bas stays neutral. Strong support is expected from 1.4260 cluster support (38.2% retracement of 1.3418 to 1.4791 at 1.4267), which is also close to 55 D EMA (now at 1.4267), to bring rebound. On the upside, above 1.4501 minor resistance will turn bias back to the upside for retesting 1.4791 short term top. However, firm break of 1.4260 will indicate that deeper correction is underway, and turn bias to the downside.

In the bigger picture, long term up trend is tentatively seen as resuming with breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

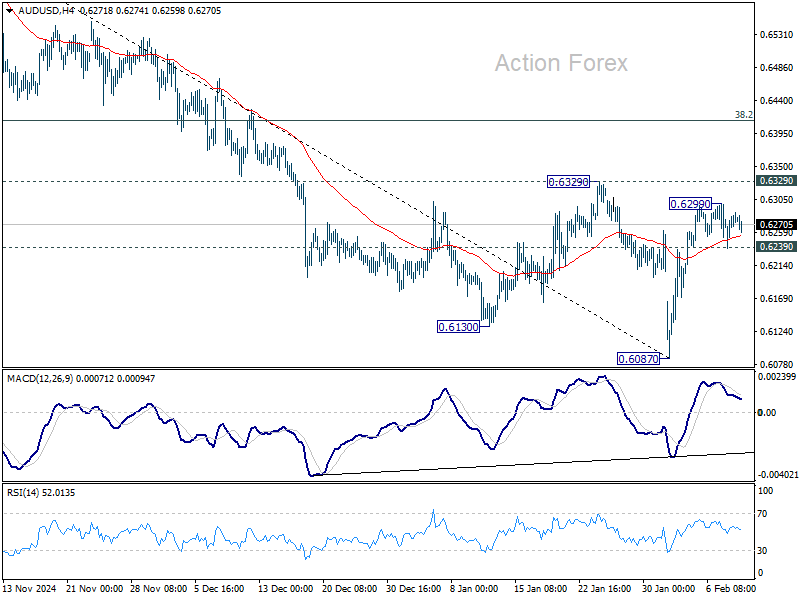

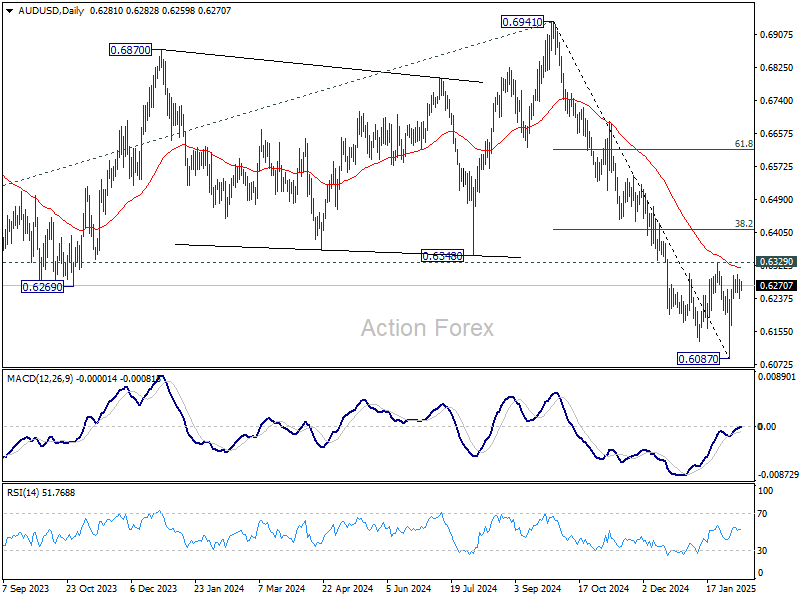

AUD/USD Daily Report

Daily Pivots: (S1) 0.6245; (P) 0.6267; (R1) 0.6299; More...

AUD/USD is bounded in sideway trading in tight range and intraday bias remains neutral. With 0.6329 resistance intact, outlook will stay bearish. On the downside, break of 0.6239 minor support will turn bias back to the downside for retesting 0.6087 low. However, firm break of 0.6329 will bring stronger rebound to 38.2% retracement of 0.6941 to 0.6087 at 0.6413, even just as a corrective move.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6516) holds.

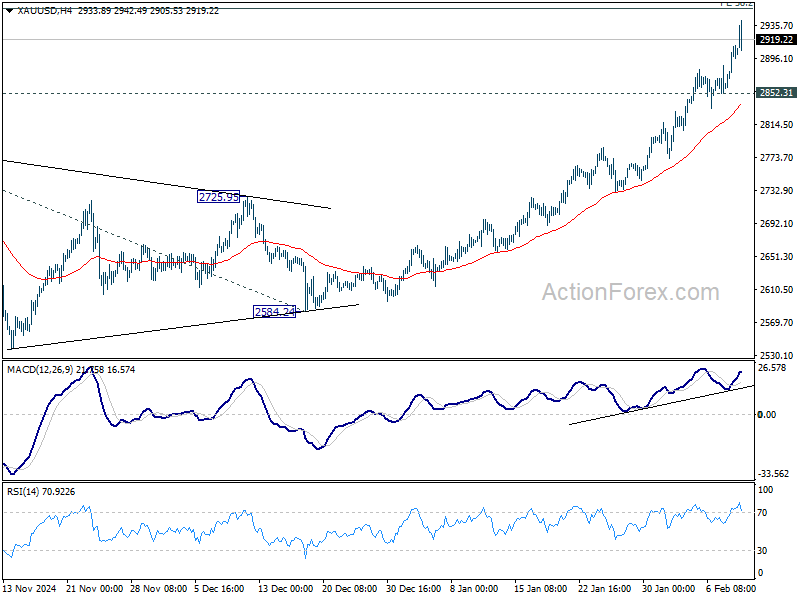

Gold Nears 3000 as Muted Reaction to Metal Tariffs Fades, Fed Powell in Focus

Dollar is trading is a mildly firmer tone while Gold inches closer to the key 3000 psychological level after US President Donald Trump officially raised tariffs on aluminum and steel imports. However, the broader market reaction has been relatively subdued. Major US equity indexes managed to post modest gains overnight, and 10-year Treasury yield also recovered. Investor sensitivity to trade war escalations has somewhat diminished. The next test will be whether Trump's upcoming reciprocal tariff announcement will trigger a similar lackluster response.

In his proclamation on Monday, Trump lifted tariff rate on aluminum to 25% from the previous 10% and eliminating previous country-specific exemptions, including quota agreements and product-specific exclusions for both metals. The measures are set to take effect on March 4.

Although Trump insisted there would be “no exceptions,” he later softened the tone and indicated the possibility of an exemption for Australia, citing that nation’s trade deficit with the US. As a result, uncertainty remains over how many countries or products may ultimately be exempt from the higher tariffs.

Markets are now awaiting further details on Trump’s reciprocal tariff plan, expected to be unveiled between Tuesday and Wednesday. The plan could impose new duties on a range of imports to match tariffs levied by trading partners, with the EU particularly at risk due to its 10% tariff on American cars—much higher than the US's 2.5% tariff on imported vehicles.

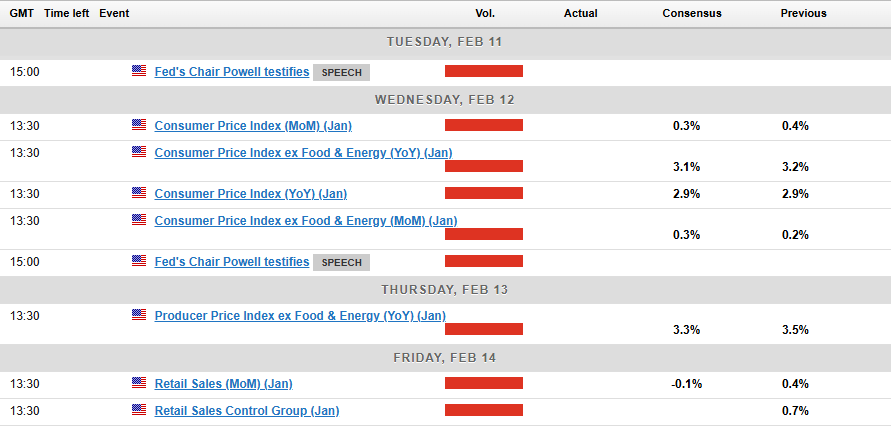

In addition to trade policy developments, the focus is also on Fed Chair Jerome Powell’s Congressional testimony later today, followed by release of key US CPI data tomorrow. Powell’s remarks could provide further insight into the Fed’s rate outlook, particularly whether policymakers are shifting toward an even longer pause in monetary easing given recent strength in the labor market and lingering inflation risks.

On the currency front, Dollar is currently the strongest major currency so far this week, followed by Aussie and then Swiss franc. Kiwi is the worst performer, trailed by Sterling and then Yen. Euro and Loonie are trading in the middle.

Technically, immediate focus in on Gold's reaction from 3000 psychological level, as well as 38.2% projection of 1810.26 to 2789.92 from 2584.24 at 2958.47. Strong resistance could be seen from there to limit upside on first attempt. Break of 2852.31 support would indicate that pullback is underway back to 2789.92 resistance turned support and possibly below. However, sustained break of 3000 would pave the way to next target at 61.8% projection at 3189.66 before topping.

In Asia, Japan is on holiday. Hong Kong HSI is down -0.72%. China Shanghai SSE is down -0.16%. Singapore Strait Times is down -0.41%. Overnight, DOW rose 0.38% S&P 500 rose 0.67%. NASDAQ rose 0.98%. 10-year yield rose 0.006 to 4.493.

Australia's Westpac consumer sentiment ticks up, RBA to start cutting this month

Australia's Westpac Consumer Sentiment Index rose slightly by 0.1% mom to 92.2 in February. While consumer mood improved significantly in the second half of 2024, the past three months have shown stagnation.

Westpac noted that financial pressures on households persist and a more uncertain global economic climate has also played a role in dampening optimism.

RBA is likely to begin policy easing at its next meeting on February 17–18. Westpac highlighted that recent economic data on core inflation, wage growth, and household consumption indicate that inflation is "returning to target faster" than previously expected.

These factors provide RBA with the confidence to initiate a 25bps rate cut this month, marking the first step in what is expected to be a "moderate" easing cycle through 2025.

Australian NAB business confidence rebounds to 4, but conditions remain weak

Australia's NAB Business Confidence index made a strong recovery in January, rising from -2 to 4 and returning to positive territory. However, despite this uptick in sentiment, underlying business conditions deteriorated.

Business Conditions index dropped from 6 to 3, marking a notable slowdown. Within this, trading conditions slipped from 10 to 6, while profitability conditions turned negative, falling from 4 to -2. On a more positive note, employment conditions edged up slightly from 4 to 5.

Cost pressures remained a key concern for businesses. Purchase cost growth eased to 1.1% on a quarterly equivalent basis, down from 1.4%. Labor cost growth picked up slightly to 1.8%. Meanwhile, final product price growth held steady at 0.8%, while retail price inflation inched up to 0.9%. Businesses are struggling to fully pass on rising costs to consumers.

NAB Chief Economist Alan Oster noted that while confidence improved, it is uncertain whether this momentum will be sustained. Elevated cost pressures, particularly on wages and input costs, continue to weigh on overall business conditions.

BoE’s Mann: Larger rate cut needed to send clear market signal

BoE MPC member Catherine Mann explained her unexpected vote for a 50bps rate cut last week. Speaking to the Financial Times, she emphasized that "Demand conditions are quite a bit weaker than has been the case", prompting a reassessment of her stance on inflation risks.

She now sees inflationary pressures easing faster, with pricing trends aligning closely to 2% target in the year ahead. This marks a notable shift from her previously hawkish position, which had consistently supported maintaining restrictive monetary policy.

A key reason for her preference for a larger cut was the need to deliver a stronger signal to financial markets. She argued that a half-point move would help "cut through the noise" and provide clearer guidance on the need for looser financial conditions in the UK.

“To the extent that we can communicate what we think are the appropriate financial conditions for the UK economy, a larger move is a superior communication device," she noted.

Mann’s stance aligns her with Swati Dhingra, the most dovish member of the MPC, who also advocated for a 50bps cut to 4.25% at last week’s meeting. The final decision was a more measured 25bps reduction to 4.50%.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6245; (P) 0.6267; (R1) 0.6299; More...

AUD/USD is bounded in sideway trading in tight range and intraday bias remains neutral. With 0.6329 resistance intact, outlook will stay bearish. On the downside, break of 0.6239 minor support will turn bias back to the downside for retesting 0.6087 low. However, firm break of 0.6329 will bring stronger rebound to 38.2% retracement of 0.6941 to 0.6087 at 0.6413, even just as a corrective move.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6516) holds.

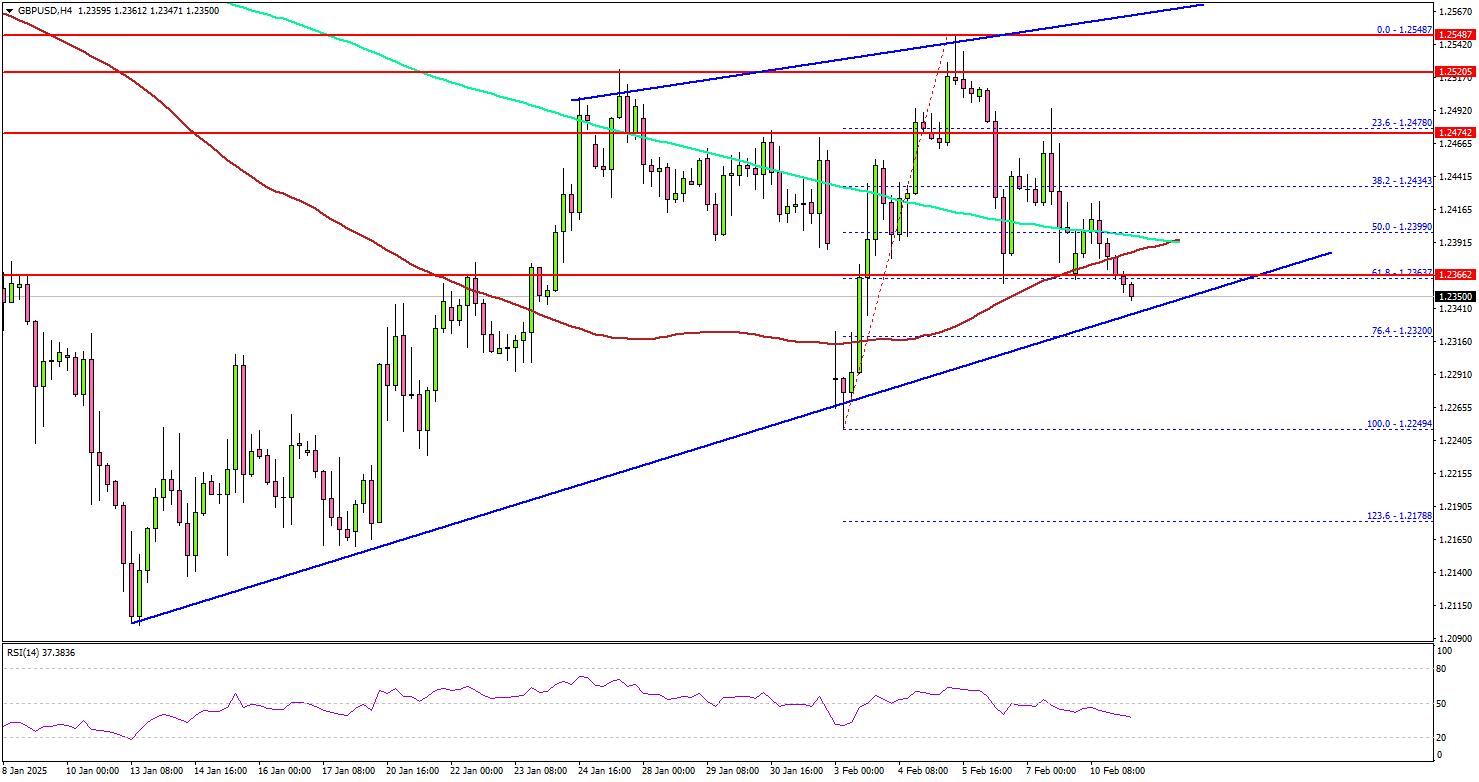

GBP/USD Sets Sight on Fresh Gains, Gold Sets New Record

Key Highlights

- GBP/USD started a consolidation phase above the 1.2320 zone.

- A key rising channel is forming with support at 1.2340 on the 4-hour chart.

- EUR/USD could struggle to gain momentum above the 1.0365 resistance.

- Gold prices surged to a record high and cleared the $2,900 level.

GBP/USD Technical Analysis

The British Pound started a fresh increase above 1.2320 against the US Dollar. GBP/USD tested the 1.2550 level before there was a downside correction.

Looking at the 4-hour chart, the pair corrected gains and traded below the 1.2480 level. The pair even declined below the 50% Fib retracement level of the upward move from the 1.2249 swing low to the 1.2548 high.

The pair is now consolidating above the 1.2340 level and near the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

On the downside, immediate support sits near the 1.2360 level. It is near the 61.8% Fib retracement level of the upward move from the 1.2249 swing low to the 1.2548 high. The next key support sits near the 1.2320 level. Any more losses could send the pair toward the 1.2250 level.

On the upside, the pair seems to be facing hurdles near the 1.2450 level. The next major resistance is near the 1.2500 level. The main resistance is now forming near the 1.2550 zone.

A close above the 1.2550 level could set the tone for another increase. In the stated case, the pair could even clear the 1.2600 resistance.

Looking at EUR/USD, the pair remained stable, but the bears are likely to remain active near the 1.0365 resistance zone.

Upcoming Economic Events:

- BoE's Governor Bailey speech.

- Fed's Chair Powell testifies.

BoE’s Mann: Larger rate cut needed to send clear market signal

BoE MPC member Catherine Mann explained her unexpected vote for a 50bps rate cut last week. Speaking to the Financial Times, she emphasized that "Demand conditions are quite a bit weaker than has been the case", prompting a reassessment of her stance on inflation risks.

She now sees inflationary pressures easing faster, with pricing trends aligning closely to 2% target in the year ahead. This marks a notable shift from her previously hawkish position, which had consistently supported maintaining restrictive monetary policy.

A key reason for her preference for a larger cut was the need to deliver a stronger signal to financial markets. She argued that a half-point move would help "cut through the noise" and provide clearer guidance on the need for looser financial conditions in the UK.

“To the extent that we can communicate what we think are the appropriate financial conditions for the UK economy, a larger move is a superior communication device," she noted.

Mann’s stance aligns her with Swati Dhingra, the most dovish member of the MPC, who also advocated for a 50bps cut to 4.25% at last week’s meeting. The final decision was a more measured 25bps reduction to 4.50%.

Australian NAB business confidence rebounds to 4, but conditions remain weak

Australia's NAB Business Confidence index made a strong recovery in January, rising from -2 to 4 and returning to positive territory. However, despite this uptick in sentiment, underlying business conditions deteriorated.

Business Conditions index dropped from 6 to 3, marking a notable slowdown. Within this, trading conditions slipped from 10 to 6, while profitability conditions turned negative, falling from 4 to -2. On a more positive note, employment conditions edged up slightly from 4 to 5.

Cost pressures remained a key concern for businesses. Purchase cost growth eased to 1.1% on a quarterly equivalent basis, down from 1.4%. Labor cost growth picked up slightly to 1.8%. Meanwhile, final product price growth held steady at 0.8%, while retail price inflation inched up to 0.9%. Businesses are struggling to fully pass on rising costs to consumers.

NAB Chief Economist Alan Oster noted that while confidence improved, it is uncertain whether this momentum will be sustained. Elevated cost pressures, particularly on wages and input costs, continue to weigh on overall business conditions.

Australia’s Westpac consumer sentiment ticks up, RBA to start cutting this month

Australia's Westpac Consumer Sentiment Index rose slightly by 0.1% mom to 92.2 in February. While consumer mood improved significantly in the second half of 2024, the past three months have shown stagnation.

Westpac noted that financial pressures on households persist and a more uncertain global economic climate has also played a role in dampening optimism.

RBA is likely to begin policy easing at its next meeting on February 17–18. Westpac highlighted that recent economic data on core inflation, wage growth, and household consumption indicate that inflation is "returning to target faster" than previously expected.

These factors provide RBA with the confidence to initiate a 25bps rate cut this month, marking the first step in what is expected to be a "moderate" easing cycle through 2025.

Gold (XAU/USD) Outlook: $3000/oz Target Possible as Safe Haven Demand Rises

- Gold (XAU/USD) has broken above $2900/oz, fueled by safe-haven demand amid new tariff announcements.

- The World Gold Council report indicates that geopolitical risks significantly contribute to gold’s rise. Additionally, European ETF inflows have been substantial.

- A sharp rise in US inflation could either push prices down or further increase safe-haven demand, creating a complex market situation.

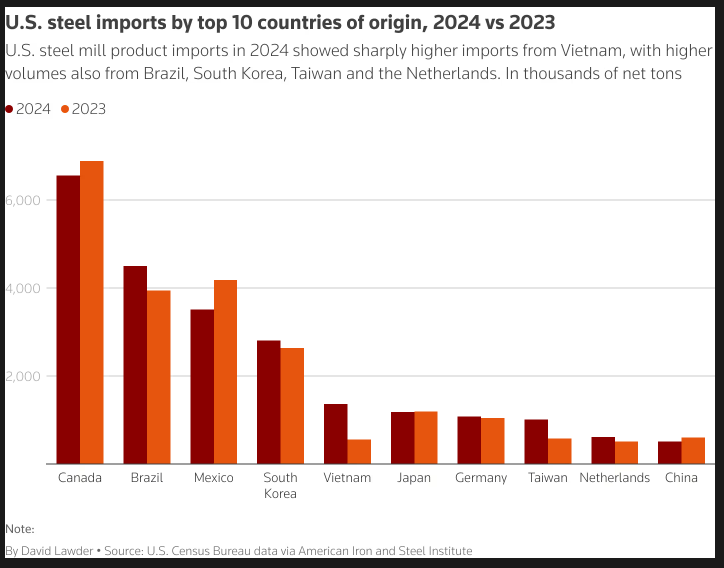

Risk aversion continued at the start of another week following Donald Trump’s pledge of blanket tariffs of 25% on steel and aluminum imports to the US. The markets opened with gaps as a result while safe haven flows continued to gain traction in the face of uncertainty.

Latest Tariff Pledges

President Donald Trump is expected to sign an order on tariffs later on Monday or Tuesday, a source said. This move could raise the chances of a trade war involving multiple countries.

Trump announced on Sunday that he will add a 25% tariff on all steel and aluminum imports to the U.S., in addition to existing duties. He also plans to introduce more tariffs later this week to match the tariffs other countries place on U.S. goods. Trade partners have warned they might retaliate. Details of the order Trump will sign are not yet available.

Source: LSEG

During his first term starting in 2017, Trump set tariffs of 25% on steel and 10% on aluminum. However, he later gave exemptions to some countries like Canada, Mexico, and Australia. He also made deals with Brazil, South Korea, and Argentina to allow certain amounts of steel and aluminum without tariffs, based on their trade levels before the tariffs. Later, President Biden made similar duty-free agreements with Britain, Japan, and the EU.

Gold Council Report and ETF Flows

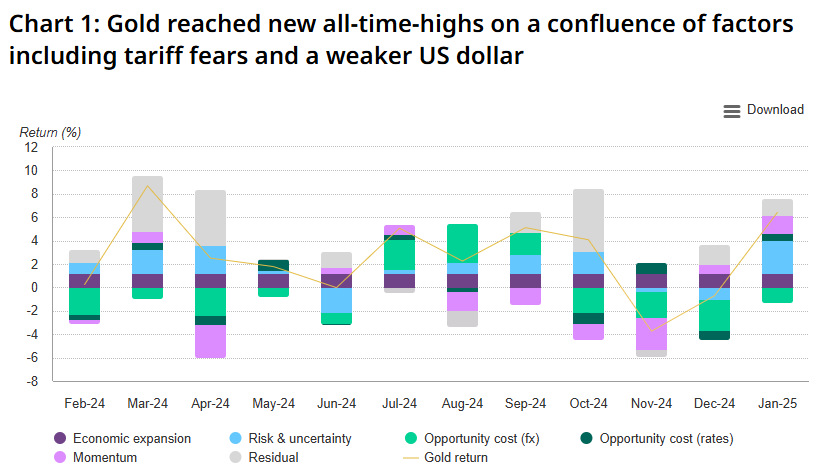

Gold enjoyed a stellar start to 2025 with January seeing the precious metal return gains of around 6.6%. This has continued in the early part of February with safe haven flows remaining strong and keeping Gold prices supported.

The World Gold Council report for January provided some interesting insights into the rise of Gold prices. A lot of which we have discussed but I thought it was worth a look.

The World Gold Councils Gold Return Attribution Model (GRAM) shows that most factors had a positive effect, including a big increase in the Geopolitical Risk Index (GPR). However, the strong US dollar in December held back returns slightly due to its delayed impact.

Source: Bloomberg, World Gold Council

On the ETF front, 2025 kicked off with positive flows, led by Europe, while North America saw outflows. Following the second consecutive monthly inflow and supported by a higher gold price, global gold ETFs’ total AUM rose to US$294bn and holdings bounced to 3,523t.

European ETF flows reached their highest level in years with inflows of +US$3.4bn, 39t which was likely supported by the European Central Bank (ECB) rate cut, causing bund yields to drop sharply throughout the month.

These developments look set to continue and thus why many are now pricing and upgrading their Gold forecasts for 2025. $3000/oz now seems within reach, with the question being when will it be reached?

US CPI Data This Week

On the data front, US inflation is the biggest data event this week which could have an impact on Gold prices. However, despite last week’s uptick in inflation expectations as revealed by the Michigan Sentiment Index, I think it may be too soon for a significant change in inflation.

I do not expect a significant uptick or shot yet, as it will require more time before the impacts of tariffs are fully felt and absorbed by the US economy.

If there is a significant uptick in inflation this could send Gold prices lower. Market participants will be concerned about an uptick in inflation before the impact of tariffs has been felt and this could spook markets.

This could work both ways though as a rise in inflation could spook markets and also lead to increased demand for safe havens. This could then net-off and keep Gold prices elevated.

Technical Analysis – Gold (XAU/USD)

Gold prices have continued their advance and breached above the $2900/oz handle. The issue at present is that there is no historical price action to look at and find areas of resistance where price could potentially pullback.

As i mentioned in last weeks piece, pullback may prove short-lived at this stage with round numbers potentially key at this stage.

Gold (XAU/USD) Daily Chart, February 10, 2025

Source: TradingView (click to enlarge)

Looking at the four-hour chart below and Gold remains around overbought territory with immediate support resting at 2886 which was the Friday high.

A pullback here may provide potential bulls an opportunity to join the trend. A break of this level opening up a retest of the 2870 support before the 2850 handle comes into focus.

As mentioned, the upside does not have a lot to look at except today’s high at 2911 which could serve as resistance. A break of this level will bring focus to 2925, 2950 and 2975 as potential areas where price may experience a pullback.

Gold (XAU/USD) Four-Hour H4 Chart, February 10, 2025

Source: TradingView (click to enlarge)

Support

- 2900

- 2886

- 2770

Resistance

- 2911

- 2925

- 2950