Sample Category Title

EUR/CHF Weekly Outlook

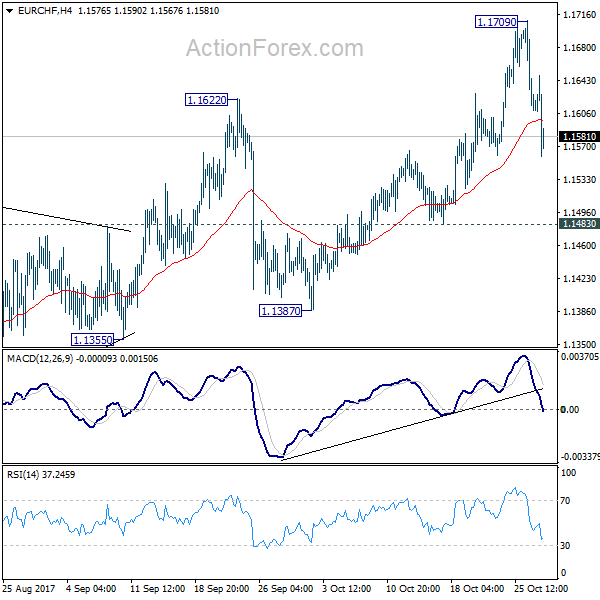

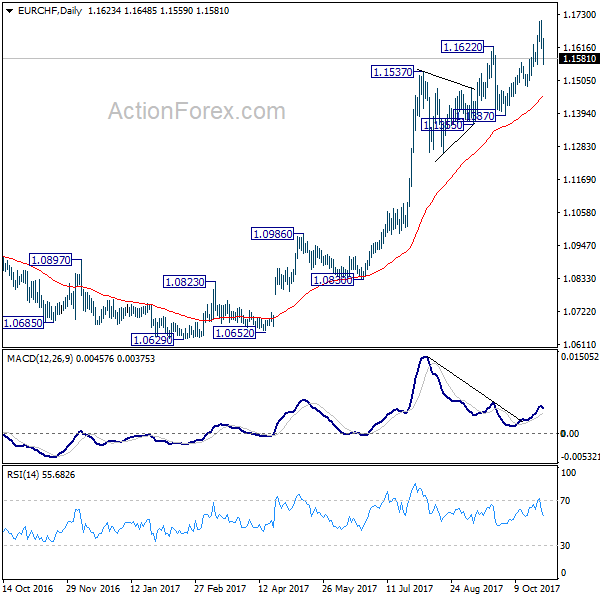

EUR/CHF jumped to as high as 1.1709 last week but dropped sharply since then. Initial bias is neutral this week first. As long as 1.1483 minor support holds, we'd expect further rally ahead. Break of 1.1709 will target 1.2 key level. However, break of 1.1483 will be an early sign of reversal. In that case, deeper decline should be seen back to 1.1355 support.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1067) and possibly below.

Dollar to Look to Non-Farn Payroll to Solidify Momentum for Bullish Reversal

Dollar closed broadly higher last week, and closed as the strongest as boosted by a couple of factors. Firstly, House approved Senate's version of budget blueprint, and cleared an important procedural step for getting the tax cuts done by the end of the year. Secondly, markets responded positively to news that Fed chair Janet Yellen is out of the race for a renewal. Instead, Fed Governor Jerome Powell and Stanford University economist John Taylor are now the front runners. Powell is reported to be slightly more favored by US President Donald Trump and is seen as a less hawkish candidate. But after all, there is still a possibility of Powell/Taylor combination for chair/vice of Fed. And either one seems to be more welcomed by the markets than Yellen. Thirdly, Q3 GDP came in at an impressive 3% annualized growth, despite the impacts of hurricanes.

Dollar, yields and stocks took the news positively. Dollar index's strong break of 94.14 key resistance now confirm medium term reversal. 10 year yield broke 2.396 key resistance decisively and it's taken as a sign of medium term up trend resumption. Meanwhile, DOW, S&P 500 and NASDAQ all hit records highs last week, with late strengths seen in the latter two. Nonetheless, the late rebound in bonds after Catalonia declared independence could cloud the outlook initially this week. In particular, the pull back in yield also supported Japanese Yen, which closed as the second strongest. And that kept USD/JPY below 114.49 key resistance.

Euro weighed down by ECB and Catalonia

Euro, on the other hand, suffered deep selling after ECB policy decision. And it closed as the second weakest ECB announced to half monthly asset purchase to EUR 30b start January, and extends the program by 9 months to end of September 2018. That was indeed in line with consensus. But Euro bulls were unhappy that ECB left the options open for extending and even expanding the asset purchase program again. Stocks, on the other hand, responded positively with German DAX hitting new record high while French CAC 40 hit the highest since 2008. However, Catalonia's declaration of independence dragged Euro further lower before weekly close. We might see European markets in risk averse mode in initial trading this week.

Aussie and Canadian Dollar suffered deep selling

Commodity currencies ended generally lower, with Aussie as the weakest and Canadian Dollar as the third weakest. Australia CPI came in below market expectations and basically ruled out the chance for any RBA rate hike in near term. Meanwhile, BoC gave the markets a rather cautious statement after leaving interest rates unchanged. BoC noted that "Governing Council will be cautious in making future adjustments to the policy rate". Nonetheless, some support is seen for the Loonie as WTI crude oil surged to close at 54.19, setting the stage for testing 55.24 key resistance. There is room for Canadian Dollar to recover this week.

BoJ, Fed, and BoE to meet, non-farm payroll a highlight

Looking ahead, BoJ, Fed and BoE will meet this week. The key focus in on BoE rate hike and vote split. Sterling has been very resilient because of expectation of a 25bps rate hike by BoE. And that was supported by the above expectation 0.4% GDP growth in Q3 released last week. However, the Pound could suffered some steep selling if what BoE delivers this week is seen as a dovish high. Also, it's Super Thursday time and BoE's quarterly inflation report will also be closely watched.

Dollar, on the other hand, will look into a string of key economic data, in particular October non-farm payroll. Strong NFP number and wage growth will bolster the case for December Fed hike. And more importantly, Fed is projection three more hikes next year, WITHOUT tax cuts taken into consideration. Solid growth data, come back of inflation, and positive news on tax cuts in the upcoming weeks solidify the cases for Fed.

Dollar index confirmed medium term reversal

Technically, Dollar index's strong break of 94.14/26 resistance zone confirms medium term reversal on bullish convergence condition in daily MACD. That also came after drawing support from 91.91/93 key long term support (38.2% retracement of 72.69, 2011 low, to 103.82, 2016 high). It's too early to take about long term up trend resumption. But even if rise from 91.01 is the second leg of the corrective pattern from 103.82, further rebound would now be seen back to 61.8% retracement of 103.82 to 91.01 at 98.92 and above. This will be the favored case as long as 93.47 near term support holds.

10 year yield resuming medium term up trend

Dollar's rally was accompanied by sharp rally in 10 year yield too. TNX finally took out 2.396 key resistance decisively last week. That should confirm that correction from 2.621 has completed at 2.034 already. It's now very likely that medium term rise from 1.336 is resuming. Near term outlook stays bullish as long as 2..273 support holds. TNX should target a test on 2.621 key resistance first. Break will confirm our bullish view and target 61.8% projection of 1.336 to 2.621 from 2.034 at 2.827. Such development would help lift Dollar.

Trading strategy

Regarding trading strategy, our CAD/JPY long (bought at 89.90) was stopped out at 88.50 last week. More dovish than expected BoC statement was a favor. And Catalonia independence was another factor. We'll stay away from CAD/JPY first.

Meanwhile, we bought USD/JPY at 114.50 at open last week. 114.49 key resistance is so far proving to be strong. Nonetheless, there is no change in our bullish view on Dollar and yield. Hence, we'll stay long in USD/JPY with a stop at 112.50.

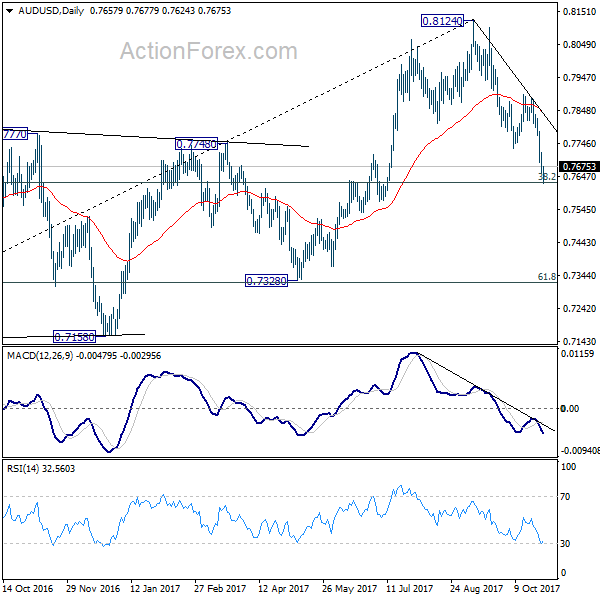

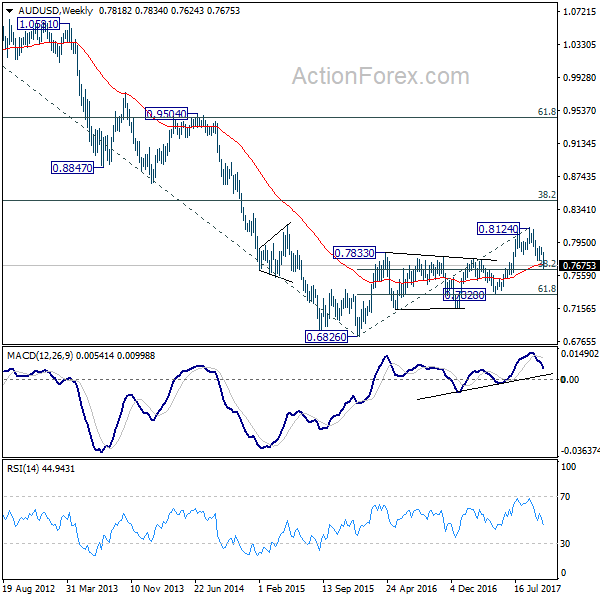

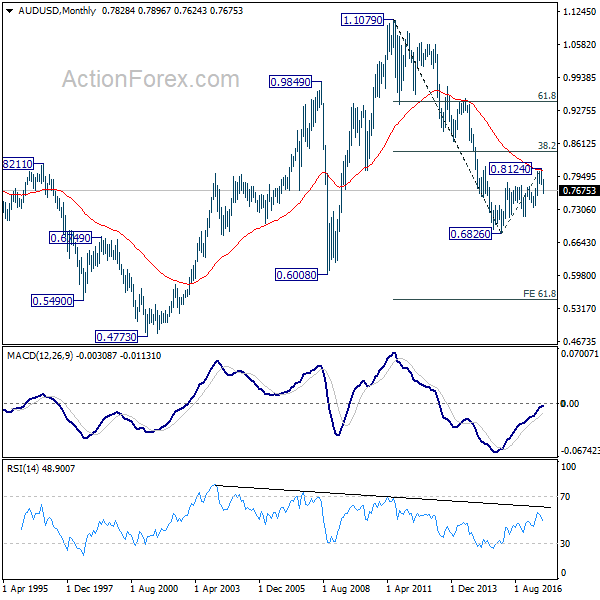

AUD/USD Weekly Outlook

AUD/USD's decline from 0.8124 resumed last week by taking out 0.7732 already. A temporary low is formed at 0.7624 after hitting 0.7628 fibonacci level. Initial bias is neutral this week for consolidations first. But upside of recovery should be limited well below 0.7896 resistance to bring fall resumption. Firm break of 0.7624 will target next key cluster level at 0.7322/8.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

In the longer term picture, 0.6826 is seen as a long term bottom. Rise from there could either reverse the down trend from 1.1079, or just develop into a corrective pattern. At this point, we're favoring the latter. And, as long as 38.2% retracement of 1.1079 to 0.6826 at 0.8451 holds, we'd anticipate another decline through 0.6826 at a later stage. But strong support should be seen between 0.4773 (2001 low) and 0.6008 (2008 low).

Summary 10/30 – 11/3

Monday, Oct 30, 2017

[php_everywhere] [/php_everywhere]

Tuesday, Oct 31, 2017

[php_everywhere] [/php_everywhere]

Wednesday, Nov 1, 2017

[php_everywhere] [/php_everywhere]

Thursday, Nov 2, 2017

[php_everywhere] [/php_everywhere]

Friday, Nov 3, 2017

[php_everywhere] [/php_everywhere].

Eco Data 11/2/17

[php_everywhere] [/php_everywhere]

Eco Data 11/3/17

[php_everywhere] [/php_everywhere]

Eco Data 11/1/17

[php_everywhere] [/php_everywhere]

Eco Data 10/31/17

[php_everywhere] [/php_everywhere]

Eco Data 10/30/17

[php_everywhere] [/php_everywhere]

The Weekly Bottom Line: U.S. Economy Steams Ahead at 3% Pace

U.S. Highlights

- U.S. equities this week managed to recover from earlier losses following strong earnings and a series of upbeat economic data. Durable goods orders and new home sales surprised to the upside, while the House approved a budget plan, adding to the upbeat tone.

- The advance estimate for third quarter GDP growth of 3% (annualized) came in better than expected despite hurricane impacts weighing on domestic demand.

- The ECB announced a reduction in its pace of asset purchases and extended its bond-buying program through September 2018 or beyond if necessary, acting to affirm a growing policy divergence between the ECB and the Fed.

Canadian Highlights

- Economic data was generally constructive this week, with wholesale trade up in August and a solid payrolls report.

- Finance Minister Morneau delivered his fall economic and fiscal update, which sees an improved budget balance resulting from recent strong economic growth. He elected to 'split the difference', with about one-third of the gain used for new initiatives and the remainder allowed to flow through to a reduced deficit profile.

- The Bank of Canada maintained its policy rate at 1.00%. The accompanying discussion took a dovish bent, but the growth outlook remains consistent with further monetary tightening. 'Data dependency' likely means that the Bank will seek confirmation of the growth path before further tightening, making January 2018 the most likely trigger point for another hike..

U.S. - U.S. Economy Steams Ahead at 3% Pace

Stocks gained this week on the back of strong earnings reports and on upbeat economic data. Durable goods orders rose 2.2% (m/m) in September - more than double the expected rate, while new home sales surged an impressive 18.9%. Although the latter can be partially attributed to a rebound in hurricane-hit areas, improvements were recorded in all regions, as activity was likely boosted by significant inventory shortages in the existing home market. The passing of a budget plan in the House, another step forward toward tax reform, added to the upbeat tone and proved particularly beneficial to Treasury yields and the U.S. dollar.

The most anticipated report of the week, BEA's advance GDP estimate, reflected this positive momentum. Growth for the third quarter came in much better than anticipated, with the economy expanding at 3% (Q/Q annualized) despite hurricane impacts. The latter did appear to weigh on a few categories, such as services spending and both residential and non-residential construction, all of which dragged on domestic demand (Chart 1), although inventory restocking helped provide some offset. Net trade also contributed positively to growth, but likely reflected a hurricane-related fall in imports, suggesting some giveback ahead. Still, with rebuilding likely to lift fourth-quarter economic growth via a rebound in domestic demand, another print of around 3% appears to be in the cards. Given estimated trend growth of 2.0%, another quarter of above trend growth is consistent with a continuation of the current interest rate hiking cycle. As such, a December rate hike appears very likely, provided that we also see some cooperation from inflation metrics.

Beyond 2017 however, the interest rate path is more uncertain. This is not only due to evolving growth and inflation dynamics, but also a possible radical makeover of the Fed, which has a number of open Board of Governor positions and may soon get a new Chair. Among the frontrunners for the top position, former Fed Governor Kevin Warsh and Stanford professor John Taylor are regarded as somewhat of a challenge to the status quo, given their apparent preference for a more rules-based approach to setting interest rates. The current Fed under Chair Yellen views monetary policy rules more as guideposts and argues against a mechanical approach, the shortcomings of which include the failure to capture current cycle dynamics and the difficulty in measuring the input variables. The latter can lead to significantly different paths (Chart 2). Nevertheless, in the event that a strict rules based approach to monetary policy is implemented, it would point to a faster pace of interest rate normalization.

A number of humdrum central bank meetings took place this week, with Canada, Sweden and Norway keeping rates on hold. In contrast, the ECB meeting was more eventful as it announced an open-ended extension of its asset purchase program through September 2018 and a reduction in its pace of asset purchases to €30B/month starting in January 2018 from the present €60B pace. However, monetary policy is likely to remain loose in the Euro Area for some time as it lags the U.S. on both the inflation and employment front. This divergence in monetary policy is likely to remain a key driver of exchange rate moves for the foreseeable future.

Canada - Morneau Splits The Difference, Poloz Pauses

The past week saw limited, but generally positive economic data. Wholesale trade gained 0.5% in August, driven largely by rising volumes (+0.4%), while the lesser-known payroll employment report showed a rise of 38.9k net positions. The report also pointed to a small climb in average hours worked, a positive sign for economic output, although earnings growth remained somewhat soft.

The main events of the week were not to be found in Statistics Canada data, but rather on or near Parliament Hill. Minister Morneau delivered the fall economic and fiscal update late Tuesday afternoon. The robust performance of the Canadian economy of late translated into an improved fiscal position, reducing the deficit outlook by about $9bn per year through fiscal 2021-22 - a marked improvement, although not enough to bring balanced budgets into view. What's more, rather than 'banking' this improvement, a number of initiatives will use up part of the space. These include reduction in the small business tax rate to 9%, as well as the inflation indexation of the Canada Child Benefit next year (two years earlier than planned), and the expansion of the Working Income Tax Benefit. All told, over a five-year horizon, about one-third of the improvement in the fiscal outlook is expected to be absorbed by these measures (Chart 1), leaving small (<1% of GDP) deficits across the horizon.

Wednesday morning saw the Bank of Canada's interest rate decision and publication of its quarterly Monetary Policy Report. In the event, Governor Poloz elected to maintain the Bank's overnight interest rate at 1.00%, with an accompanying statement and report that were, on their face, fairly dovish. Four key areas of concern were again emphasized: potential labour market softness, as seen in wages, the higher sensitivity of the economy to interest rates given elevated debt levels, the impact of the digital economy on inflation, and the impacts of capacity building. On top of this, the Bank sees changes to mortgage underwriting, uncertainty around U.S. trade policies, and other issues removing about 0.3 p.p. from the growth outlook.

As is often the case, it is important to read between the lines. Despite all of the headwinds and concerns, the outlook for near-term growth has been upgraded (Chart 2), with the 2019 change likely reflecting a return to Canada's potential growth rate following more robust than anticipated near-term growth. Indeed, the Bank now sees the output gap (a key measure of economic slack) as effectively closed, which, when combined with an outlook for above-potential economic growth, has traditionally been a recipe for mounting inflationary pressures. Squaring this with the caution expressed on Wednesday seems to get to the heart of what Governor Poloz means by "intense data dependent mode". With risks skewed to the downside, it appears that the Bank is going to want to see confirmation of its outlook before moving rates, happy to trade the risk of higher inflation against the materialization of negative outcomes. Ultimately then, this week's pause is not likely to last, with the key rate likely to be bumped higher in January, assuming a constructive path for the Canadian economy.

U.S.: Upcoming Key Economic Releases

U.S. FOMC Rate Decision

Release Date: November 1, 2017

Previous Result: 1.25%

TD Forecast: 1.25%

Consensus: 1.25%

The November FOMC meeting is likely to be uneventful, with rates unchanged and no substantive changes in language. That said, we see two-sided risks: more cautious language on the inflation outlook (dovish), and a signal about an incoming rate hike (hawkish). Given current market pricing for a December hike, we expect any hawkish tone in the statement to have a more modest impact than a dovish bias.

U.S. ISM Manufacturing Index - October

Release Date: November 1, 2017

Previous Result: 60.8

TD Forecast: 60.0

Consensus: 59.1

TD expects the ISM manufacturing PMI to slip back to 60.0, preserving some of its hurricane-induced strength as rebuilding efforts continue. Any correction is likely to be led by the supplier deliveries index, which surged after the hurricanes, and employment, which has been running at multi-year highs. Scope for a large correction is limited given the strength registered across regional surveys in October, notably the Philly Fed index.

U.S. ISM Non-Manufacturing Index - October

Release Date: November 3, 2017

Previous Result: 59.8

TD Forecast: 57.5

Consensus: 58.0

ISM Non-Manufacturing Index is expected to pull back to 57.5, led also by a correction in supplier deliveries. That would leave the ISM composite above its Q3 average, consistent with solid above-trend GDP growth in Q4.

U.S. Employment - October

Release Date: November 3, 2017

Previous Result: -33k, unemployment rate 4.2%

TD Forecast: 330k, unemployment rate 4.2%

Consensus: 310k, unemployment rate 4.2%

We expect nonfarm payrolls to almost fully give back its hurricane-induced weakness and post a 330k gain. Uncertainty however is high with scope for surprise in either direction. Our forecast assumes that a 200k-250k drag from the twin hurricanes, which we expect to almost fully recover in October. Previous hurricane episodes, such as Katrina, suggest a full bounce back in payrolls could be delayed, yet we believe this experience is different given the trend in jobless claims which have fully recovered. With labour market indicators consistent with monthly payroll gains of 175-200k, October payrolls could easily print closer to +400k or higher. However, we are more cautious as the full rebound may not be realized until subsequent revisions, as was the case in previous natural disasters. In addition, September payrolls have potential to be upwardly revised.

We expect the unemployment rate to stabilize at 4.2%. Average hourly earnings is expected to print a relatively weak 0.2% m/m increase, though risk for a more modest 0.1% rise taking into account calendar effects and hurricane distortions. That would push the annual pace lower to 2.7% y/y, or 2.6% y/y if downside is realized.

Canada: Upcoming Key Economic Releases

Canadian Real GDP - July

Release Date: October 31, 2017

Previous Result: 0.1% m/m

TD Forecast: 0.1% m/m

Consensus: 0.1% m/m

Industry-level GDP is forecast to rise by 0.1% in August, led by a rebound in the manufacturing industry. Retooling shutdowns at motor vehicle assembly plants single-handedly shaved nearly 0.1% from GDP in July and a partial rebound will provide a tailwind to growth in August. Outside of the manufacturing industry, growth conditions are far more mixed. Energy output may see a modest gain but utilities are likely to be a drag due to weaker demand caused by unseasonably cool weather. The services sector will be weighed down by a pullback in retail sales though broadening job growth suggests activity continues to increase. Our forecast for a 0.1% increase is consistent with Q3 growth in the low-to-mid 2% range, which presents upside risks to the Bank of Canada's 1.8% projection from the October MPR. However, with the Bank focused on the supply side of the economy, we do not expect a modest upside surprise on GDP to change their bias and look for the next rate hike to come in January.

Canadian Employment - October

Release Date: November 3, 2017

Previous Result: 10k, unemployment rate: 6.2%

TD Forecast: 15k, unemployment rate: 6.2%

Consensus: 15k, unemployment rate: 6.2%

TD looks for the economy to add 15k jobs in October though the details may prove more encouraging than the headline print. After jumping to a 15-month high last month, we see more room for wage growth to rise in October due to a combination of favourable base-effects and the continued erosion of labour market slack. The unemployment rate is likely to hold at the current cycle low of 6.2% but the risks lean towards a further improvement to 6.1%. Meanwhile, the composition of job growth will likely skew towards services and private employment after an outsizde gain in public sector employment last month. The full/part-time split is likely to favour the latter given the underperformance so far this year, but we hope that outsized swings are in the past after the 100k swings in the last two reports. Youth participation and unemployment may also get more attention than usual given Poloz's focus on remaining pockets of slack in the labour market.

Canadian International Trade - September

Release Date: November 3, 2017

Previous Result: -$3.4bn

TD Forecast: -$3.0bn

Consensus: -$2.9bn

The goods trade deficit is forecast to narrow to $3.0bn in September, reflecting a moderate rebound in export activity while imports should see little change. Exports are likely to benefit from a rebound in auto production while vehicle replacement in Texas and Florida will add to foreign demand. The hurricane distortion in energy products is less clear cut but we expect an increase in petroleum exports to offset weaker demand from Gulf refineries. However, currency appreciation will continue to pose a risk. This will cap off a very weak quarter for Canadian exports after the soft handoff in June and a sharp decline in July. Even after a modest improvement in September, we look for trade to act as a sizeable headwind to growth in Q3.

Conspiracy Theories and Tin Foil Hats

Conspiracy Theories and Tin Foil Hats

Instead of policy convergence, the ECB and the Feds are heading for divorce. This week the ECB delivered one of their better changeups catching the markets leaning the wrong way. But in retrospect, perhaps the most significant surprise is the markets failed to pick up on the ECB's well-telegraphed signals that one of their more notable fears is that the firming Euro is hurting Eurozone exporters.

This weeks ECB decision to keep the monetary floodgates open refusing to call an end to central bank largess has weakened the euro and will provide an export-driven boost to EU economies.

A weak euro, of course, is entirely what ECB President Mario Draghi wants. It makes exports cheaper, ensuring the absolute competitiveness of euro-zone countries while simultaneously increasing the price of imports propping up inflation

We should probably be looking for low-risk low-cost strategies to play the stronger dollar narrative into years end instead of dwelling on conspiracy theories, but after this week's sudden G-10 Central Bank policy shifts, a concern may start to creep in that we're back on the cusp of a currency war.

On top of the roller coaster rides offered by the headline-driven game of musical chairs for the Fed Chair nomination. It will be interesting to hear President Trump and company (Mnuchin / Cohn) retort after reviewing this weeks FX charts

With G-10 currencies bleeding a sea of red, it's hard NOT make a case that global central bankers are trying to steal some of the US's economic thunder through overtly guiding their domestic currencies lower. Let's just hope we don't go back to the protectionist highway, but somehow I see that drive coming as the chorus of dovish G10 central banks is far too convincing to ignore

Removing my conspiracy theorist tin foil hat for a moment, in reality, the ECB could be doing little more than playing for time until the political mess in Spain abates and more clarity over the next Fed chair unfolds. Let's see how this plays out in weeks ahead.

The US Dollar

While the USD sparkle looks to extend into next week, the glimmer faded slightly when Fed Chair speculators pointed their Ouiji board to Powell and tempered USD's broader advances after a pinch of salt type headlines suggested Powell was Trump's choice. Indeed, markets are still nervous waiting for the Fed Chair green light before kicking into high gear. But the bottom line is: "The president has not yet decided which of the two front-runners will get which job, the sources said". However, expect Fed Chair headlines to accelerate as we near November 3 and wise to belt in for the expected roller coaster ride.

Not surprisingly given the markets focus on the Fed Chair hullabaloo, A robust US Q3 GDP reading failed to move the dollar dial convincingly as long short-term dollar positions were stretched on Friday and looking to book profit post GDP gap.

Asia FX

In Asia Fx, the higher currency correlation to US bond yields lately suggests we could see an acceleration of local bond hedging activity on a breach of UST 2.50 % level. If localised dollar demand does materialise, there could be a high probability for an overshoot so the Em investors may err on the side of caution and let the dust settle on this broader USD dollar move before aggressively re-engaging. However, given the breadth of G-10 currency moves, the Asian FX complex has held in very well. Global and Regional Macro conditions remain favourable; the geopolitical risk is abating, and China continues to hold up their end of the bargain all underpinning regional sentiment. There's no hint of panic as of yet.

Malaysian Ringgit

In Malaysia, The budget was received positively and geared towards maintaining stability in both the FX and Bond markets through fiscal prudence

Also, the financial burden of lower oil prices in 2017 will be offset by GST receipts where Income tax is anticipated to make up almost half of Malaysian government revenue amid robust economic growth.

But with improving oil prices, this will be viewed positively

Despite the positivity surrounding the budget, the currency and local bond markets remain prone to risk from the prospects of higher US interest rates and the soaring USD after the extremely dovish ECB lean sent the USD higher. But on a positive note, with most G-10 central banks turning dovish this too could suggest a return of investment flows. More so given the trial and error approach the Feds will take to reduce the balance sheet implying that regardless who takes the helm at the Fed, interest rate normalisation may not deviate too far for from the current dot plot

Weekend Risk

The focus will be on Monday EUR open. Difficult to determine if the event risk for an impending ART 155 trigger is fully priced or not as the Euro barely blinked on the plethora of Catalonian headlines in early NY.But as opposed to last weekends event risk, the EURO is on a policy divergence triggered downtrend, and Fund managers may view any negative headlines as an excuse to flush more EUR long positions on the Monday open.