Sample Category Title

Chinese Leadership Reshuffle: Xi Tightly Grips Power as He Refuses to Identify Successor

The 19th National Congress of the Chinese Communist Party culminated with the announcement of the new Politburo Standing Committee (PSC) - the group of officials leading the country in the coming five year. Five out of seven members of the previous PSC were replaced, with only President Xi Jinping and Premier Li Keqiang staying in power. The five new members are Li Zhanshu, Wang Yang, Wang Huning, Zhao Leji and Han Zheng. As we mentioned in the previous report, Li Zhanshu, Zhao Leji, Wang Huning and Chen Min'er have very strong link with President Xi. We are surprised that Chen is not chosen to be the core team. Derailing from the usual practice that has been in place since 1990s, Xi refrained from revealing who his successor is. This suggests that he refuses to step down after the coming 5-year term.

Previous PSC

| Rank | Name | Year of Birth | Position |

| 1 | Xi Jinping | 1953 | General Secretary |

| 2 | Li Keqiang | 1955 | Premier |

| 3 | Zhang Dejiang | 1946 | Chairman of the Standing Committee of the National People's Congress (NPC) |

| 4 | Yu Zhengsheng | 1945 | Chairman of the Chinese People's Political Consultative Conference (CPPCC) |

| 5 | Liu Yunshan | 1947 | The first-ranked Secretary of the Secretariat, President of the Central Party School |

| 6 | Wang Qishan | 1948 | Secretary of the Central Commission for Discipline Inspection |

| 7 | Zhang Gaoli | 1946 | The first-ranked Vice Premier |

New PSC

| Rank | Name | Year of Birth | Position |

| 1 | Xi jinping | 1953 | General Secretary |

| 2 | Li Keqiang | 1955 | |

| 3 | Li Zhanshu | 1950 | |

| 4 | Wang Yang | 1955 | |

| 5 | Wang Huning | 1955 | The first-ranked Secretary of the Secretariat |

| 6 | Zhao Leji | 1957 | Secretary of the Central Commission for Discipline Inspection |

| 7 | Han Zheng | 1954 |

Other evidence that Xi has used this twice-in-a-decade congress to enormously upgrade his status and authority is the inclusion of "Xi's thought on Socialism with Chinese characteristic for a new era" in CCP's constitution. The act has made Xi the most powerful leader after Mao Zedong, even surpassing Deng Xiaoping. While names of both Mao and Deng are enshrined in the constitution, Xi is the only person, besides Mao, whose name is printed in the document before death.

While receiving limited media coverage, the head of the NDRC at the Congress affirmed that China was on track to achieve its 2017 growth target of 6.5%. We believe this affirmation intends to ease market concerns over potential growth slowdown in 2H17, amidst decline in productivity growth as the government curtail heavy industry, such as coal, steel and aluminum production, and construction to reduce pollution, as well as slowdown in housing price growth. With GDP growth at +6.9% in 1H17 and +6.8% in 3Q17, we also expect Chinese full year growth would meet target this year.

Notwithstanding leadership reshuffle, the economic policy would stay unchanged. Indeed, the National Congress is for clarification of CCP's ideology and leadership reshuffle, rather than setting of economic policies. The key aspects of the monetary and fiscal policies have already been lain down at the National Financial Work Conference in July. Meanwhile, any new economic target or related policy should be revealed at the Economic Working Conference usually scheduled in December.

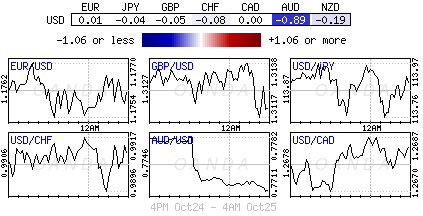

GBPUSD Strongly Bullish Above 1.3228

The British pound has moved sharply higher against the U.S dollar, hitting 1.3255, after United Kingdom third quarter GDP came in better than expected, rising 0.4 percent. The GBPUSD pair currently trades around the session high's, as investors await the release of Core Durable Goods Orders data from the United States economy.

The British pound remains intraday bullish against the U.S dollar while trading above the 1.3228 level. Further advancement can be expected towards the 1.3268 and 1.3307 levels, while price-action holds above the key 1.3228 level.

If price-action falls below the 1.3228 level for a sustained period, a further decline should be expected towards the 1.3201 level. Extended intraday GBPUSD support is located at 1.3157.

USDJPY Intraday Bullish Above 113.89

The U.S dollar has moved to new monthly trading high against the Japanese Yen, hitting 114.25 during today's European session. The current risk-on environment in global stocks and bonds is helping to underpin intraday strength in the USDJPY. The pair currently trades around the 114.20 level, ahead of the release of high impact U.S economic data.

The USDJPY pair remains further bullish on an intraday basis while holding price-action above the 113.89 technical level. Buyers will likely target the 114.33 and 114.50 levels while the pair continues trades above the 113.90 level.

If USDJPY sellers can push price-action below the 113.89 level for a sustained period, a further decline can be expected towards 113.40 and 113.23 levels.

Canadian Dollar Under Pressure Ahead of BoC Decision

The Canadian dollar continues to lose ground this week, and has moved lower in the Wednesday session. Currently, USD/CAD is trading at 1.2701, up 0.21% on the day. On the release front, the Bank of Canada will set the benchmark rate and also release its quarterly monetary policy report. In the US, we'll get a look at durable goods reports and New Home Sales. On Thursday, the US releases unemployment claims and Pending Home Sales.

The Canadian dollar slipped 1.3 percent last week against the greenback, and the downward trend has continued this week. Currently, the currency is at its lowest level since mid-August. Will the BoC rate decision end the slide? The markets are not expecting any move at the Wednesday meeting, and only a 33% chance of a rate hike by the end of 2017. If, as expected, the Federal Reserve raises rates in December, the BoC will be under pressure to keep pace and also hike rates.

Will Janet Yellen bid adieu to the Federal Reserve? Yellen's 3-year term concludes in February 2018, and President Trump has said he will nominate a new Fed in the next few days. The front runners are economist John Taylor and Federal Reserve Governor Jerome Powell. Taylor advocates a rule in which rates which be as high as 3 percent, given current economic conditions. Powell is more closely aligned to Fed Chair Janet Yellen's monetary stance which advocates an incremental increase in rates. With the two candidates representing sharply differing views on interest rate levels, Trump's choice for the new Fed chair could have a significant effect on monetary policy and the strength of the US dollar. If Taylor gets the nod, the US dollar could respond with gains of 3 percent or more.

China: New Leadership Points to Continuation – But No Successor for Xi Jinping

China has this morning presented its new leadership in the Standing Committee (SC) of the Politburo. The line-up was as expected following the news reports yesterday as outlined in our Flash Comment China: Xi gets name in Constitution, Wang Qishan steps down. The new SC points to continuation as the number of members is unchanged at seven and the five new members represent different factions of the Communist Party. The '7 up, 8 down' informal rule was also respected. Hence, Xi Jinping did not aim for a strengthening of power in the SC. However, the new SC has no successor to Xi Jinping as President in 2022, which will add to speculation that he may stay on after his second term. By striking a balance on power and keeping to informal rules, it may also increase party support for Xi Jinping staying on after 2022. But only time will tell.

With the Party Congress now behind him and a team Xi Jinping has been forming, we believe focus will turn to a further reform push in 2018.

The key takeaways from the new Standing Committee:

In our preview to the Party Congress Research: Why the Party Congress is key for China's road ahead, 3 October 2017, we highlighted a number of things to look out for. Below, we look at how they have turned out:

Number of people in the Standing Committee. It turned out the number was unchanged at seven. Had it been reduced, it would have been a sign of stronger power for Xi Jinping. But this turned out not to be the case.

Who has been appointed? The people in the new SC represent different factions of the party, which points to continuity. It includes reformers like Wang Yang, who has also been connected to the Youth League - a faction that Xi Jinping has generally given less influence. A strong theorist like Wang Huning with no administrative experience (as normal for SC members) also made it to the SC. It indicates that Xi Jinping will continue to focus on a strong theoretical backbone in the leadership. Zhao Leji will take over the leadership of the corruption campaign from Wang Qishan. Li Zhanshu is a strong administrator and is Xi Jinping's man. Han Zhen has been the Party Secretary of Shanghai and often been linked to Jiang Zemin. Li Keqiang stayed on as Premier as widely expected recently but in contrast to speculation earlier that Xi Jinping would replace him with Wang Qishan and break the informal age rule.

Will the '7 up, 8 down' rule be respected? It was speculated that Xi Jinping would break the '7 up, 8 down' rule that states that a member has to be below 68 when a new term starts. This would have allowed him to keep Wang Qishan, the anti-corruption tsar and generally considered to be China's number two leader after Xi Jinping. However, here also Xi respected the party line and Wang Qishan has stepped down.

Will Xi Jinping designate a successor? As mentioned above, no successor has been designated to succeed Xi Jinping as China's leader when his second term expires in 2022. None of the members of the new SC are young enough (57 or younger) to be able to serve one five-year term on the SC and after that be a leader for two five-year terms if the '7 up, 8 down' rule is to be respected. It may be that Xi Jinping wants more time to find his successor. But it clearly raises the probability that he could stay on for a third term. The emphasis of 'a new era' and need for strong leadership in the new era could point in this direction. However, we are likely to have to wait a few years to see if a successor evolves.

What will Xi Jinping put in the Constitution? It became clear yesterday that Xi Jinping got his name in the Constitution with his new thinking: 'Socialism with Chinese characteristics in a new era'. It clearly underlines the power of Xi Jinping. Only Mao Zedong and Deng Xiaopeng have their names in the Constitution while the two previous leaders Jiang Zemin and Hu Jintao did not achieve this. Also, Deng Xiaopeng only got his name in the Constitution after his death. In this respect, Xi Jinping can be seen as the strongest leader since Mao.

What will the work report say? The Work Report was read on the first day of the Congress in a 3½ hour speech. It also points to continuity and further focus on reforms and innovation. It indicates a rising focus on quality of life and economic growth rather than explicit growth targets. Xi Jinping stated that China is on its way to reaching the goal of a 'moderately prosperous society' by 2020 and stated a longer goal of by 2050 becoming a 'great modern socialist country that is prosperous, strong, democratic, culturally advanced, harmonious and beautiful'. He highlighted two stages on this journey - a first stage from 2020 to 2035 and a second stage from 2035 to 2050. He did not attach new growth targets to the next stage, though, which further indicates less focus on growth targets and more on raising living standards, more broadly including limiting pollution.

To sum up, Xi Jinping ended up striking a balance between respecting continuity and following tradition and party rules while at the same time strengthening his power by getting his name in the Constitution and not designating a successor.

GBPUSD: Reverses Losses On A Rally, Eyes 1.3300 Zone

GBPUSD: The pair took back its Tuesday losses on a rally on Wednesday. This development has opened the door for more strength towards the 1.3300 zone. Support lies at the 1.3200 level where a break will turn attention to the 1.3150 level. Further down, support lies at the 1.3100 level. Below here will set the stage for more weakness towards the 1.3050 level. Conversely, resistance stands at the 1.3300 levels with a turn above here allowing more strength to build up towards the 1.3350 level. Further out, resistance resides at the 1.3400 level followed by the 1.3450 level. On the whole, GBPUSD continues to face further upside threats on recovery.

Market Update – European Session: UK Q3 GDP Data Support Case For BOE Rate Hike

Notes/Observations

German Business Survey reading of 116.7 hits its highest level since German reunification

UK Q3 Advance GDP data registers a slight beat (QoQ: 0.4% v 0.3%e); support case for BOE rate hike

Overnight

Asia:

Australia Q3 Consumer Prices (CPI) misses expectations (Q/Q: 0.6% v 0.8%e; Y/Y: 1.8% v 2.0%e; remained below the lower end of the RBA’s 2-3% inflation target

China Xi Jinping renamed as Head of Communist Party and Chairman of Central Military Commission (as expected); The overall Politburo Standing Committee has 7 members

Europe:

Bank ECB's Weidmann (Germany) might agree to an extension of time and reduction of ECB bond purchases at monetary policy meeting on Thursday. Not demanding a fixed end date for the QE program in order to get his vote. One potential scenario would be for ECB to cut the bond purchases in half to 30B/month and extending the earliest end date by 9 months

Americas:

John Taylor reportedly won informal straw poll among GOP senators for Fed Chair appointment at lunch with President Trump

Energy:

Weekly API Oil Inventories: Crude: +0.5M v -7.1M prior

Economic Data

(CH) Swiss Sept UBS Consumption Indicator: 1.56 v 1.50 prior

(ES) Spain Sept PPI M/M: +0.5% v -0.1% prior; Y/Y: 3.4% v 3.3% prior

(DE) Germany Oct IFO Business Climate: 116.7 v 115.1e (record high); Current Assessment: 124.8 v 123.5e; Expectations Survey: 109.1 v 107.3e

(CH) Swiss Oct Credit Suisse Expectations Survey: 32.0 v 28.0 prior

(UK) Q3 Advance GDP Q/Q: 0.4% v 0.3%e; Y/Y: 1.5% v 1.5%e

(UK) Sept BBA Loans for House Purchases: 41.6K v 41.8Ke

Fixed Income Issuance:

(IN) India sold total INR110B vs. INR110B indicated in 3-month, 6-month and 12-month Bills

(SE) Sweden sold SEK10B vs. SEK10B indicated in 3-month Bills; Avg Yield: -0.7460% v -0.6964% prior; Bid-to-cover: 2.43x v 2.47x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -flat at 389.4, FTSE -0.4% at 7498, DAX flat at 13010, CAC-40 +0.2% at 5405, IBEX-35 +0.4% at 10241, FTSE MIB flat at 22629, SMI -0.1% at 9183, S&P 500 Futures -0.2%]

Market Focal Points/Key Themes:

European Indices trade mixed this morning, with focus on the ECB rate decision tomorrow. Strong German IFO reading did little to move the markets, while a slighly stronger UK GDP figure has helped lift Cable and consequently put pressure on the FTSE100.

On the corporate front earnings continued to be the predominent theme, with notable risers including Kering, CapGemini and Air Liquide, while Valeo, Kesko, PSA Group and Lufthansa are some of the notable fallers. Refresco trades higher in the Netherlands after receiving an improved offer; Bawag IPO marked Austria's largest IPO valued at over €4B and will make around 4% of the ATX Index.

Looking ahead Visa, Coca Cola and Boeing are some the notable names expected to report.

Equities

Consumer discretionary [Kesko [KESKOB.FI] -1.8% (Earnings), Lufthansa [LHA.DE] -0.7% (Earnings), Kering [KER.FR] +7.4% (Earnings), Heineken [HEIA.NL] -2.5% (Earnings), BATS [BAT.UK] +2.6% (Outlook ahead of capital markets day)]

Consumer Staples [Refresco [RFRG.NL] +2.4% (Improved takeover offer)]

Materials: [Antofagasta [ANTO.UK] -3.7% (Production, initial FY18 outlook) ,

Industrials: [PSA Group [UG.FR] -1.2% (Earnings), Air Liquide [AI.FR] +2.8% (Earnings), Dassault Systems [DSY.FR] -0.9% (Earnings), Valeo [FR.FR] -3.1% (Earnings), Alfa Laval [ALFA.SE] -2.% (Earnings)]

Financials: [Lloyds [LLOY.UK] -1.9% (Earnings)]

Technology: [CapGemini [CAP.FR] +1.6% (Earnings)]

Speakers

Spain PM Rajoy: Catalonia elections is the only way out

German IFO Economists noted that the domestic economy was full steam ahead. Economy unaffected by political development as coalition talks following national election not causing any uncertainty

Brexit Min Davis testified in Parliament that was aiming for an agreement on everything by March 2019. Aiming for tariff-free comprehensive trade agreement; most complex Brexit issues fell outside the FTA remit. The transition status would be close to status quo. Expected transition outline to be agreed upon in Q1Sought free movement with registration during transition period and expected passporting to be included in transition. Sought to keep 3rd party deals during transition

Italy Senate to hold final vote on new electoral bill on Thursday, Oct 26th

Czech Central Bank Vice Gov Hampl: prefers gradual rate hikes by 25bps

Indonesia Fin Min Indrawati saw 2018 GDP growing improving aided by better purchasing power and would maintain prudent fiscal policy in 2018

Japan Cabinet Office (Govt) Monthly Economic Report for Oct: Maintains overall economic assessment with domestic economy experiencing a moderate recovery

Currencies

EUR/USD was little changed in the session with focus on ECB policy meeting on Thursday. Pair showed little reaction despite German Oct IFO Business Climate survey hitting a fresh German reunification high. ECB widely expected to outline plans to scale back bond purchases under its quantitative easing program with tapering expectations shifted towards a "lower for longer" approach. Reports circulated that even German Bundesbank Gov Weidmann could possibly agree to an extension of time and reduction of ECB bond purchases and not demand any fixed end date

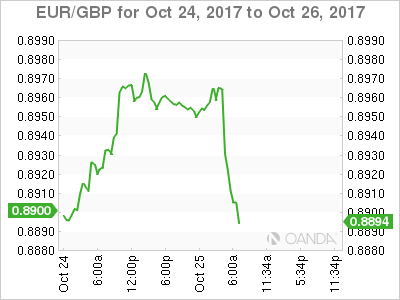

The GBP currency (Cable) was slightly higher after UK Q3 Advance GDP data registered a slight beat (QoQ: 0.4% v 0.3%e) and keeping expectations that BOE could hike rates in the near future. Dealers noted chances of a BOE hike next month remain above 80%

USD/JPY was back at 3-month highs above the 114 handle.The USD was firmer after John Taylor reportedly won informal straw poll among GOP senators for Fed Chair appointment at lunch with President Trump on Tuesday.

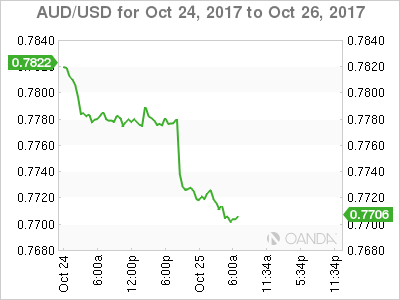

Softer CPI data out of Australia weighed upon the AUD/USD pair as inflation remained below the lower end of the RBA’s 2-3% inflation target. AUD/USD off 0.7% at 0.7710 area

Fixed Income

Bund futures trade at 160.97 down 23 ticks, with the focus on Thursday’s ECB rate decision and the announcement to changes on the QE program. Support lies at 161.00, followed by 160.38. Resistance stands initially at 162.75, followed by 163.51.

Gilt futures trade at 123.67 down 45 ticks following beat in UK GDP data. Continued downside eyeing 123.26. Upside targets 124.90 then 125.24.

Wednesday’s liquidity report showed Tuesday’s excess liquidity fell to €1.791T from €1.794T and use of the marginal lending facility stayed at €417M

Corporate issuance saw $11.5B come to market via 4 issuers, headlined by Goldman Sach’s $7B debt offering

Looking Ahead

(CO) Colombia Sept Retail Confidence: No est v 17.5 prior; Industrial Confidence: No est v -1.9

(TR) Iraq PM Abadi in Turkey

05:30 (EU) ECB allotment in 3-month LTRO (€3Be)

05:30 (DE) Germany to sell €3.0B in 0.50% Aug 2027 Bunds

05:30 (PL) Poland to sell Bonds

06:00 (BR) Brazil Oct FGV Consumer Confidence: No est v 82.3 prior

06:30 (CL) Chile Central Bank's Traders Survey

06:45 (US) Daily Libor Fixing

07:00 (RU) Russia to sell combined RUB30B in OFZ bonds

07:00 (US) MBA Mortgage Applications w/e Oct 20th: No est v 3.6% prior

07:00 (UK) PM May weekly question time in House of Commons

07:30 (TR) Turkey Oct Capacity Utilization: 79.0%e v 79.0% prior

07:30 (TR) Turkey Oct Real Sector Confidence (Seasonally Adj): No est v 110.8 prior; Real Sector Confidence (unadj): 109.0e v 111.6 prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Sept Preliminary Durable Goods Orders: 1.0%e v 2.0% prior; Durables Ex Transportation: 0.5%e v 0.5% prior

09:00 (US) Aug FHFA House Price Index M/M: 0.4%e v 0.2% prior

09:00 (MX) Mexico Aug Retail Sales M/M: 0.2%e v 0.3% prior; Y/Y: 0.5%e v 0.4% prior

10:00 (CA) Bank of Canada (BOC) Interest Rate Decision: Expected to leave Interest Rates unchanged at 1.00%

10:00 (CA) Bank of Canada (BOC) October Monetary Policy Report

10:00 (US) Sept New Home Sales: 554Ke v 560K prior

10:30 (US) Weekly DOE Crude Oil Inventories

11:00 (IT) Italy Debt Agency (Tesoro) announces specifics bonds in upcoming BTP auction on Monday, Oct 30th

11:15 (CA) Bank of Canada (BOC) Gov Poloz and Wilkins hold post rate decision press conference

11:30 (US) Treasury to sell 2-Year Floating Rate Notes

13:00 (US) Treasury to sell 5-Year Notes

16:00 (BR) Brazil Central Bank (BCB) Interest Rate Decision: Expected to cuts Selic Target Rate by 75bps to 7.50%

CAC Moves Higher, ECB Stimulus Decision Looms

The CAC index has posted slight gains in the Wednesday session. Currently, the CAC is trading at 5,409.80, up 0.35% on the day. On the release front, there are no French or eurozone events on the schedule. On Thursday, the ECB publishes its rate statement.

The CAC continues to move upwards, and on Wednesday, the index climbed to 5413, its highest level since mid-May. Investors are keeping a close on the ECB, which holds a policy meeting on Thursday. Mario Draghi and Co. will have to maneuver carefully, as the ECB decides whether to start unwinding its asset purchases program, which is currently pegged at EUR 60 billion/month. Back in the summer, the ECB said it would trim the program in the “autumn”, but didn’t make any moves at the September meeting. Germany is strongly in favor of quickly removing the stimulus program, but other eurozone members want to see a gradual phase-out of the plan. Expectations of a significant reduction in stimulus, perhaps to EUR 30 billion/mth, has sent bond yields higher this week, which in turn could push European stock markets downwards.

France’s economy has improved in 2017, and service and manufacturing reports on Wednesday suggest that fourth quarter growth will be strong. Manufacturing and Services PMIs came in at 56.7 and 57.4 points respectively, both of which beat expectations. The French government is determined to overhaul the economy and has targeted public spending, with plans to cut 120,000 civil servants. The government also expects that the deficit will drop below 3 percent of GDP in 2017, in keeping with EU guidelines. Last year, the deficit stood at 3.4 percent of GDP.

DAX Yawns As German Business Confidence Jumps

The DAX is almost unchanged in the Wednesday session, as the index remains close to the symbolic 13,000 level. Currently, the DAX is at 13,013.50, unchanged from the Tuesday close. On the release front, German Ifo Business Climate continued to accelerate with a reading of 116.7, well above the forecast of 115.3 points. On Thursday, the ECB releases its rate statement.

German indicators continue to point upwards, indicative of a robust economy. On Tuesday, German Manufacturing PMI posted a strong reading of 60.5, beating expectations. The manufacturing sector continues to expand, buoyed by strong domestic demand and the global appetite for German exports. There was more good news on Wednesday, as German Ifo Business Climate jumped to 116.7, an all-time high. This thumbs-up from the business confidence suggests that the German economy will enjoy a strong fourth quarter.

The markets are keeping a close eye on the ECB, which will set the benchmark rate on Thursday. Investors are in a positive mood on Tuesday, ahead of the ECB policy meeting on Thursday. ECB President Mario Draghi will have to maneuver carefully, as the ECB decides whether to start unwinding its asset purchases program, which is currently pegged at EUR 60 billion/month. Back in the summer, the ECB said it would trim the program in the “autumn”, but didn’t make any moves at the September meeting. Expectations of a significant reduction in stimulus, perhaps to EUR 30 billion/mth, has sent bond yields higher, which in turn could push European stock markets downwards.

BoC To Set The Loonie’s Tune

Later this morning, the Bank of Canada (BoC) will release its rate statement and quarterly monetary policy report (10 am EDT). No rate change is expected after two consecutive increases (+1%), especially after last Friday's sluggish inflation headlines and disappointing August retail sales print. There is also less certainty about the timing of the next rate increase in Canada due to the negative turn in talks to reshape NAFTA.

Tomorrows European Central Bank (ECB) meeting is expected to see the bank outline its plans for QE in 2018. The responsibility is on President Draghi and fellow members to deliver a monetary policy recalibration that recognizes the improvement in economic conditions. With real growth having acquired reasonable momentum, the same cannot be said of inflation, thus any shift in the ECB's policy stance is likely to be quite measured.

With forward guidance ruling out any rate hike any time soon, the market focus is going to be on the extent to which QE asset purchases will be tapered and the deadline, if any, for the completion of the program.

1. Stocks mixed results

Euro stocks have stalled as the earnings season continues to unfold, while benchmarks in Asia were mostly higher, but Japan's Nikkei finally snapped its record run of gains.

The Nikkei share average dropped for the first time in 17-days in choppy trade overnight as investors took profits on the record run of consecutive daily gains, although higher U.S yields supported financial stocks. The Nikkei 225 declined -0.5%, while the broader Topix fell -0.3%.

Down-under, Australia's S&P/ASX 200 Index rose +0.1% while South Korea's Kospi index was up +0.2%.

In Hong Kong, equities rallied, supported by strong gains by listings in the city of mainland-based companies, and as China's ruling Communist Party revealed its new leadership line-up. The Hang Seng Index climbed +0.4%, while the China Enterprises Index rallied +0.8%.

In China, blue chips stocks extended gains overnight to 26-month highs, supported by robust profits from tech firms and the Communist Party's new leadership line-up. The blue-chip CSI300 index rose +0.5%, while the Shanghai Composite Index gained +0.3%.

In Europe, regional indices trade mixed, with focus on the ECB rate decision tomorrow. A stranger German IFO reading this morning did little to move the market, while a slightly stronger U.K GDP print is supporting the pound (£1.3193) and consequently putting pressure on the FTSE100.

U.S stocks are set to open in the red (-0.2%).

Indices: Stoxx600 -flat at 389.4, FTSE -0.4% at 7498, DAX flat at 13010, CAC-40 +0.2% at 5405, IBEX-35 +0.4% at 10241, FTSE MIB flat at 22629, SMI -0.1% at 9183, S&P 500 Futures -0.2%.

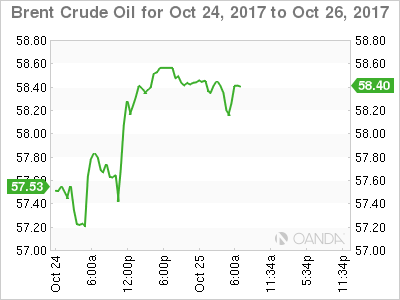

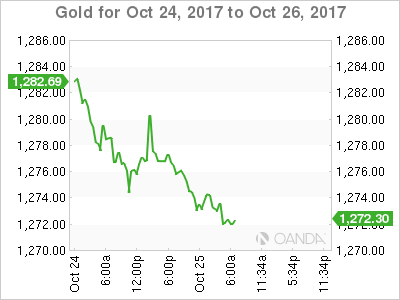

2. Oil hovers near four-week high on Saudi pledge, gold lower

Oil prices are largely steady; hovering near a four-week high after top exporter Saudi Arabia said it was determined to end a supply glut.

Brent crude is up +8c at +$58.41 a barrel, after settling yesterday up +1.7%. U.S West Texas Intermediate (WTI) is trading down -9c at +$52.38.

Earlier today, the Saudi Arabia's Energy Minister Khalid al-Falih said the focus remains on reducing oil stocks in industrialized countries to their five-year average and raised the prospect of prolonged output restraint once OPEC's supply-cutting pact ends.

Note: OPEC plus Russia and nine other producers have cut oil output by -1.8m bpd since January. The pact runs to March 2018, but they are considering extending it.

API data yesterday showed that U.S crude stocks rose by +519k barrels last week. The market was expecting a decline of -2.6m barrels. The U.S Energy Information Administration (EIA) will release official government inventory at 10:30 am EDT.

Ahead of the U.S open, gold prices have edged lower, pressured by a firmer U.S dollar amid speculation over who will be the next Federal Reserve chief. Spot gold is down -0.2% at +$1,273.70 an ounce.

3. U.S Sovereign yields back up

U.S bonds yield continue to edge higher as investors anticipate tighter monetary policies. The yield on the U.S 10-year note has backed up above +2.41% and any signs from the ECB tomorrow that they will be reducing QE should support higher Euro debt yields.

The market is also pricing in a good chance that President Trump could nominate a replacement for Ms. Yellen who would quicken the pace of interest-rate increases. Yellen has indicated that tightening is going to continue and she's the most ‘dovish' of the candidates to lead the Fed over the next four-years.

Also weighing on U.S Treasury prices are upcoming debt auctions that will add to the supply of outstanding bonds. The Treasury Department is scheduled to sell +$34B of five-year notes today and +$28B of seven-year notes Thursday.

Elsewhere, Germany's 10-year Bund yield has dipped -1 bps to +0.47%, while the U.K's 10-year Gilt yield declined -1 bps to +1.349%.

4. Dollar hangs tough

The EUR (€1.1771) is little changed ahead of the U.S open with the market focus on tomorrow's ECB policy meeting. The single unit has shown little reaction to this morning's stronger German October IFO Business Climate survey hitting a fresh reunification high. The ECB is expected to outline plans to scale back its bond purchases under its QE program with tapering expectations shifting towards a “lower for longer” approach.

Sterling (£1.3193) has found support after U.K Q3 Advance GDP data registered a slight beat (see below) and keeps market expectations that the Bank of England (BoE) could hike rates early next month. The futures market is pricing in an 80% chance of a hike in November.

USD/JPY (¥114.19) is back trading atop of its three month high. The USD is firmer after John Taylor supposedly won an informal ‘straw poll' among GOP senators for Fed Chair appointment at lunch with President Trump on Tuesday.

Softer CPI data out of Australia is weighing upon the AUD/USD (A$0.7704) as inflation remains below the lower end of the RBA's +2-3% inflation target.

5. U.K economy accelerates

Data this morning showed that the U.K. economy accelerated in Q3, according to a preliminary estimate, strengthening expectations that the BoE may raise interest rates as soon as next month.

The ONS said U.K GDP expanded +0.4% in Q3 compared with the previous three months, an annualized rate of +1.6%.

The performance marked a small improvement from Q2 when the U.K posted the slowest growth among all 28 countries of the European Union, alongside Portugal, at +0.3%.