Sample Category Title

USD/CAD Canadian Dollar Lower After BoC Holds Interest Rate

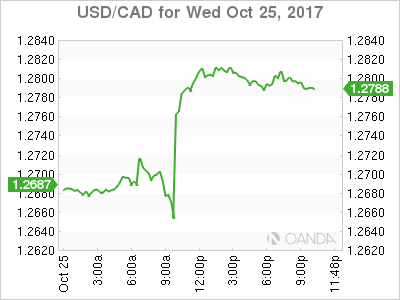

The Canadian dollar traded at a three month low after the Bank of Canada (BoC) kept the benchmark interest rate intact as expected and delivered a dovish assessment of the economy and NAFTA uncertainty.

The Canadian central bank had hiked rates twice in 2017 and given the pace of growth in the first half of the year a third rate hike was a probability near the end of the year. Now the BoC seems unsure about how solid that growth really is, in stark contrast of their views in July and September. The bank also mentioned the possible impact higher rates could have on Canadians, who now hold record levels of debt.

The BoC was not all doom in their report with a positive outlook for the future but gone is the urgency on raising rates replaced by a data dependency that Fed watchers will recognize. Stephen Poloz mentioned that every monetary policy meeting is a live one, but from watching Chair Yellen and the FOMC investors are now expecting a more cautious Canadian central bank going forward. Trade decisions and other factors outside of its control could put the BoC in a different path form the one it was on a month ago.

The USD/CAD rose 0.96 percent on Wednesday. The currency pair is trading at 1.2796 and briefly went over the 1.28 price level after the Bank of Canada (BoC) held the interest rate unchanged and delivered some concerns about the economy prompting investors to discount the probability of a rate hike coming this year.

The Bank of Montreal was one of the first to push back their forecast for the next rate hike to come in March of 2018. The U.S. Federal Reserve is anticipated to lift the Fed funds rate in December widening the gap between Canadian and US borrowing costs.

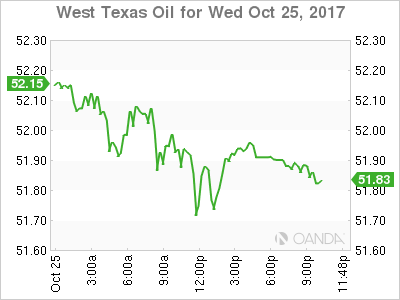

West Texas Intermediate is trading at $51.91. The price of crude fell on Wednesday with a surprise rise in weekly US crude inventories. The first buildup in oil inventories showed a rise of 900,000 barrels. The forecast was calling a fourth consecutive drawdown of 2.2 million barrels.

The rise in inventories undid some of the work of Saudi Arabia whose efforts to extend the Organization of the Petroleum Exporting Countries (OPEC) and other producers agreement to cut production have kept oil prices stable. The increase in US oil rigs have offset the cuts in production, with only geopolitical and other disruptions pushing prices higher throughout the year.

Market events to watch this week:

Thursday, October 26

7:45 am EUR Minimum Bid Rate

8:30 am EUR ECB Press Conference

8:30 am USD Unemployment Claims

Friday, October 27

8:30 am USD Advance GDP q/q

EUR/USD Dollar Lower Against Euro Awaiting ECB Decision

European Central Bank Anticipated to Taper But Extend Duration

The US dollar is mixed against major pairs on Wednesday. The greenback is weaker against the pound, euro, yen and Swiss franc and appreciated versus the commodity pairs (kiwi, aussie and the loonie). The Bank of Canada (BoC) kept rates unchanged and provided dovish comments that took the CAD to a three month low after the press conference hosted by Governor Stephen Poloz. The USD could not contain the rise of the EUR even with a higher than expected durable goods indicator and the single currency will keep trading near 1.18 ahead of the central bank announcement.

The European Central Bank (ECB) monetary policy meeting on Thursday, October 26 at 7:45 am EDT will be the highlight of the week for the EUR/USD pair. President Mario Draghi will host a press conference at 8:30 am EDT. The ECB is expected to announce the tapering of its QE program, but at the same time extend the actual bond buying by 12 months or more. The amount of bonds for purchase could be halved to 30 billion but the program could remain in effect until December 2018.

The EUR/USD rose 0.35 percent on Wednesday. The single currency is trading at 1.1803 ahead of the ECB monetary policy statement to be released on Thursday. The market is waiting in anticipation on how exactly the central bank will accomplish being hawkish and dovish at the same time. The ECB has hinted that it is ready to taper its quantitative easing program down from the current 60 billion euros on monthly purchases down to 30 billion. To avoid a “taper tantrum” Mario Draghi and company is also expected to extend the duration of the program by 9 months. In short an aggressive cut, but with a longer period to keep accumulating bonds.

ECB President Mario Draghi already made clear that rates will continue to be lower, but for now the reduction of the QE bond purchases could boost the Euro despite the expected longer duration of the program. The last time the central bank cut its program was by 20 billion euros in December 2016.

The wishes of the ECB will be hard to accomplish as a central bank can hardly act without causing volatility. There are obvious signs of strong growth in the Eurozone, but also the rising trend of geopolitical risks is a cause for concern.

Earlier today MarketPulse Analyst Kenny Fisher outlined the positive impact of German business climate, but pointed out that the Catalan crisis in Spain continues:

The German economy continues to fire on all cylinders, with much of the credit going to a robust manufacturing sector. The global appetite for German exports remains strong and consumer spending has been steady. On Tuesday, German Manufacturing PMI posted a strong reading of 60.5, beating expectations. There was more positive news on Wednesday, as German Ifo Business Climate jumped to 116.7, an all-time high. This thumbs-up from the business confidence suggests that the German economy will enjoy a strong fourth quarter.

Spain's constitutional crisis has been on simmer all week, but the temperature could rise dramatically on Friday, when the Spanish Senate steps into the fray. The Senate is expected to authorize the central government to invoke Article 155 of Spain's constitution and apply direct rule over Catalonia. This would allow Madrid to dismiss the Catalan government and take control of the regional police and radio and television stations. This drastic clause has never been invoked, and it remains unclear what steps the central government will take under Article 155. Another question mark is how the Catalan parliament will respond. Catalan President Carles Puidgemont has so far avoided explicitly declaring independence from Spain, but could choose to pre-empt a move by the central government to remove him from office. The continuing uncertainty could lead to further unrest and instability. Still, Caixabank, the third largest bank in the country, does not expect the Catalonia issue to affect Spain's GDP, which the bank projects will expand 2.7 percent in 2018.

Market events to watch this week:

Thursday, October 26

7:45 am EUR Minimum Bid Rate

8:30 am EUR ECB Press Conference

8:30 am USD Unemployment Claims

Friday, October 27

8:30 am USD Advance GDP q/q

Gold Shrugs As Durable Goods Sparkles

Gold is unchanged in the Wednesday session. In North American trade, the spot price for an ounce of gold is $1276.71, up 0.01% on the day. On the release front, US numbers impressed as durable goods orders accelerated in September. Core Durable Goods Orders gained 0.7%, above the estimate of 0.5%. Durable Goods Orders soared 2.2%, crushing the estimate of 1.0%. As well, New Home Sales jumped to 667 thousand, well above the forecast of 555 thousand. On Thursday, the US releases unemployment claims and Pending Home Sales.

Gold prices remain steady this week, after the metal slipped 1.9 percent last week. The sharp drop was in response to solid data last week, as employment, manufacturing and housing data beat their estimates. On Friday, the US releases Advance GDP for the third quarter, and the markets are expecting a strong gain of 2.5 percent. If the GDP reading is not within expectations, we could see some strong movement in gold prices.

Who will take over at the Federal Reserve? The markets are keeping close tabs on the central bank, as Janet Yellen’s 3-year term expires in February. President Trump has said he will nominate a new Fed head in the coming days, and the front runners are economist John Taylor, Federal Reserve Governor Jerome Powell, and Yellen. Taylor advocates a rule in which interest rates could be as high as 3 percent, given current economic conditions. Powell is more closely aligned to Fed Chair Janet Yellen’s monetary stance which advocates an incremental increase in rates. With the two candidates representing sharply differing views on interest rate levels, Trump’s choice for the new Fed chair could have an effect on monetary policy and the strength of the US dollar. Still, most economists are of the view that monetary policy will be largely driven by the performance of the US economy. Inflation levels remain weak and may not reach Fed’s target of 2 percent before 2020, but that has not dampened expectations of a December rate hike. According to CME FedWatch, the odds of a raise in December stand at 96 percent.

The Bank-Of-Can’t Decide

The Bank of Canada put a screeching halt to interest rate hikes Wednesday after two quick hikes in succession. The Canadian dollar was the top performer on the day while the pound surged to lead the way. The ECB decision is up next.

It has been a bizarre year for the Bank of Canada, who is quickly earning a reputation for doing the right thing… only after all the other options are exhausted. Through most of the first half of the year, the BOC was stubbornly dovish, hinting at rate hikes and keep rates low despite months of very strong economic data. Then, days before the July decision, deputy governor Wilkins dropped a hint about a hike.

Despite a weak CPI report afterwards, the BOC surprised markets with a hike. The Bank then hit the mute button and didn't have a single statement or interview until the September meeting when they caught markets largely by surprise with another hike.

Back-to-back hikes are unheard of in the post-crisis era and the message from those actions was that policymakers were worried about inflation. Poloz tried to emphasize data dependence and that cooled expectations for a hike Wednesday but still left the markets expecting something hawkish.

Instead, the BOC delivered a dovish hike saying the Governing Council will be “cautious in making future adjustments”. They cited NAFTA, mortgage rules changes and the Canadian dollar as reasons. None of that will be cleared up by year-end so a 50/50 chance of Dec hike is closer to zero and that's why USD/CAD jumped above 1.28.

At the same time GBP/CAD jumped more than 300 pips as it was also fueled by strong UK GDP numbers and the expectation that Carney will hike UK rates next week. Technically, that pair exploded above the Aug/Sept highs to a test of 1.70. It will likely rise to 1.75 if Carney delivers a hike with a hint of hawkishness.

Before that, the ECB is on deck. Expectations are centered around a taper to 30 billion euros per month of QE from 60 billion starting in December. Many market watchers are also talking about an extension in buying until September but it's highly unlikely that the ECB gives that much clarity. Draghi loves to add a measure of uncertainty and flexibility. Locking himself in with a timeline would be out of character.

The market could interpret the flexibility as dovish and send the euro lower. In addition, the large net-long EUR position could be waiting to 'sell the fact' on a taper announcement. A 3rd euro trade in the Premium Insights will be added ahead of the ECB.

Bank of Canada Leaves Key Rates Unchanged

The euro price was supported by the report on the German business climate index from the Ifo that grew to 116.7, which is 1.5 above the forecasted figure. Investors are in no hurry to open new positions ahead of the statement by ECB President Mario Draghi tomorrow. The upward movement may also be explained by the covering of short positions. On the other side of the ledger, the greenback received support from a number of factors among which are the growth of durable goods orders in the US by 2.2% in September versus the 1.0% forecasted and new home sales increase to 667,000 against the 555,000 anticipated. Hints that the new Fed Chair may be more hawkish than the incumbent, Janet Yellen, have been positive for the US dollar. Another fact that will restrain traders from active actions is the expected release of US GDP data on Friday.

The British pound has shown a sharp rising impulse after the publication of the preliminary report on GDP in the UK for the third quarter which expanded by 0.4% against the 0.3% forecasted. This is giving additional stimulus for an interest rate hike by the Bank of England during the next meeting. Monetary tightening in the UK is highly anticipated due to rising inflation and hawkish statements by the officials of the Bank of England.

The price of the Canadian Dollar experienced an increase in volatility after the release of the decision of the Bank of Canada to leave the interest rate at the 1.00% level. Disappointing retail sales data published in the last week was one of the reasons to hold the rates at the current level.

EUR/USD

The EUR/USD demonstrates a positive movement after some consolidation above 1.1750. The closest objective within the current impulse is 1.1825 and near the inclined resistance line. On the opposite side, there is a high probability of further price consolidation between the support at 1.1730 and angled resistance line. Volatility is forecasted to increase and stay high until the end of the week.

GBP/USD

The GBP/USD price has shown a significant rising movement and was able to break through the resistance lines at 1.3150 and 1.3250. Fixing above 1.3250 may become the basis for continued growth with the next targets at 1.3400 and 1.3600. A rollback is possible to 1.3200 and the angled resistance line. The RSI recently touched the oversold zone, which is the basis for a correction soon.

USD/CAD

The USD/CAD experienced a high increase of volatility after the publication of the monetary policy statement by the Bank of Canada. The closest objective for growth is at 1.2800 and fixing above it may become the basis for continued growth up to 1.3000. The support is placed at 1.2665 and we do not eliminate a downward price correction after a powerful rising movement.

Pound Jumps as British GDP Beats Estimate

The British pound has posted sharp gains in the Wednesday session. In North American trade, GBP/USD is trading at 1.3295, up 0.95% on the day. On the release front, British Preliminary GDP improved to 0.4%. British High Street Lending and Index of Services both met expectations. US data was sharp, as durable goods orders and housing reports beat the forecasts. Core Durable Goods Orders gained 0.7%, above the estimate of 0.5%. Durable Goods Orders soared 2.2%, crushing the estimate of 1.0%. As well, New Home Sales jumped to 667 thousand, well above the forecast of 555 thousand. On Thursday, the US releases unemployment claims and Pending Home Sales.

British GDP showed the economy expanded 0.4% in the third quarter, its strongest gain since Q4 in 2016. The strong reading has sent the pound sharply higher and raised speculation that the Bank of England will raise rates at its November 2 meeting. Policymakers remain divided over a rate hike, which would be the first in a decade. Proponents of a rate increase point to inflation running at 3.0%, above the Bank's target of 2.0%, but opponents argue that the economy is showing signs of weakness and a rate hike in current conditions would be not be appropriate.

Who will take over at the Federal Reserve? The markets are keeping close tabs on the central bank, as Janet Yellen's 3-year term expires in February. President Trump has said he will nominate a new Fed head in the coming days, and the front runners are economist John Taylor and Federal Reserve Governor Jerome Powell. Taylor advocates a rule in which interest rates could be as high as 3 percent, given current economic conditions. Powell is more closely aligned to Fed Chair Janet Yellen's monetary stance which advocates an incremental increase in rates. With the two candidates representing sharply differing views on interest rate levels, Trump's choice for the new Fed chair could have an effect on monetary policy and the strength of the US dollar. Still, most economists are of the view that monetary policy will be largely driven by the performance of the US economy. Inflation levels remain weak and may not reach Fed's target of 2 percent before 2020, but that has not dampened expectations of a December rate hike. According to CME FedWatch, the odds of a raise in December stand at 96 percent.

Pound Rises on GDP, Hike Speculation; Loonie Declines on BoC Inflation Expectations

The British pound was a notable gainer during today's trading as forex market participants revised upwards their expectations for a quarter percentage point interest rate rise to be delivered by the Bank of England after UK third quarter growth beat expectations. The dollar was gaining ground relative to the loonie, aussie and the kiwi and retreating versus the euro, yen and of course sterling.

At 1542 GMT, the dollar index, which gauges the greenback against the currencies of six major US trading partners, was 0.1% down relative to where it closed yesterday, though not far below the near three-week high that was recorded a couple of days ago. Versus the yen, the dollar was lower by 0.2%, having earlier hit 114.24 yen, its highest since July 11.

Speculation over who's going to be the next Fed chief is mounting (with a Yellen reappointment also a possibility). According to a report by Bloomberg, Trump asked Republican senators at a closed-door lunch on their preference and it was said that Stanford University economist John Taylor emerged as the number-one pick. This has supported the dollar as Taylor is viewed as an inflation hawk, favoring higher interest rates.

September durable goods orders out of the US grew by 2.2% m/m, handily beating expectations of a rise by 1.0%. Core durable goods (which exclude volatile transportation items) over the same month increased by 0.7%, above forecasts of 0.5%. The positive numbers pushed the dollar higher relative to major counterparts including the yen, spurring hopes for a lesser drag on economic activity from the hurricanes that stormed the US in September. The world's largest economy will see the release of Q3 preliminary GDP estimates on Friday.

Later in the day, US September new home sales grew by a whopping 18.9% m/m, reaching a near 10-year high and coming in far above the expected contraction of 0.9% and August's fall of 3.6%. The dollar index advanced within the first minutes of the data release.

According to preliminary estimates, UK GDP grew by 0.4% q/q in the third quarter, above expectations of 0.3% which also coincided with Q2's growth figure. Year-on-year, growth stood at 1.5%, above forecasts of 1.4% and at the same pace as Q2's annual expansion. The stronger-than-anticipated figures pushed sterling higher as expectations that the BoE will hike interest rates upon completion of its meeting on monetary policy on Thursday were on the rise. Pound/dollar was last up 0.8% on the day, having hit an eight-day high of 1.3270 at its peak, with euro/pound being down by 0.4%, recording an eight-day low of 0.8877 earlier in the day.

The Canadian dollar hit a three-month low as dollar/loonie rose to as high as 1.2788 after the Bank of Canada decided to maintain rates at 1.00% upon completion of its policy meeting today. The decision was expected but the central bank's policymakers pushed forward to the second half of 2018 their expectations for inflation to reach the bank's 2% target. Dollar/loonie was last 0.9% up, trading close to the aforementioned high.

Euro/dollar last traded 0.5% up on the day and above the 1.18 handle. The ECB's decision tomorrow on how it will adjust its asset purchase program starting next year is eagerly awaited by market participants. Economists expect a 20-billion-euros-per-month reduction (to 40 billion euros per month). Uncertainty over the program's duration will also clear out tomorrow with reports saying policymakers are split over whether it should last for six or nine months.

The aussie remained significantly down on the day relative to its US counterpart after today's third quarter inflation figures surprised to the downside, scaling back expectations for an interest rate rise to be delivered anytime soon by the RBA. Aussie/dollar was last down 0.9%, having earlier fallen to 0.7696, its lowest since July 13.

Kiwi/dollar remained on a downward path on uncertainty over the economic policies of the new Labour-led government. The pair was 0.3% down, trading near its daily low of 0.6865 which is the lowest the pair has experienced since May 16.

In commodities, gold was 0.05% lower, trading just below $1,275 an ounce. WTI was 0.25% lower at $52.34 per barrel and Brent crude traded 0.4% higher at $58.58. The Energy Information Administration's (EIA) weekly report showed US crude stocks rising by 0.86 million barrels during the previous week. Expectations were for a fall by 2.58 million barrels.

Yen Edges Higher Despite Sharp US Durable Goods Reports

USD/JPY has recorded small losses in the Wednesday session. In North American trade, USD/JPY is trading at 113.78, down 0.18% on the day. On the release front, US data was sharp, as durable goods orders and housing reports beat the forecasts. Core Durable Goods Orders gained 0.7%, above the estimate of 0.5%. Durable Goods Orders soared 2.2%, crushing the estimate of 1.0%. As well, New Home Sales jumped to 667 thousand, well above the forecast of 555 thousand. Later in the day, Japan releases Services Producer Price Index, which is expected to remain unchanged at 0.8%. On Thursday, the US releases unemployment claims and Pending Home Sales, and Japan will publish Tokyo Core CPI.

Japanese Prime Minister Shinzo Abe cruised to victory in the Japanese election on Sunday, and this means 'more of the same' for Japan's ultra-accommodative monetary policy. The Bank of Japan holds a policy meeting next week, and policymakers are expected to maintain its inflation forecasts. At the September meeting, the BoJ stated that it did not expect inflation to reach the Bank's 2.0% target until fiscal year 2020. BoJ Governor Haruhiko Kuroda has long insisted that the bank will not taper its stimulus program until inflation moves higher. Kuroda's 5-year term as governor expires in April 2018, although he remains the top contender for the position.

The guessing game at the Federal Reserve continues, as investors await the next choice for Federal Reserve chair. Janet Yellen's 3-year term expires in February, and President Trump has said he will nominate a new Fed head in the coming days. The front runners are economist John Taylor and Federal Reserve Governor Jerome Powell. Taylor advocates a rule in which rates which be as high as 3 percent, given current economic conditions. Powell is more closely aligned to Fed Chair Janet Yellen's monetary stance which advocates an incremental increase in rates. With the two candidates representing sharply differing views on interest rate levels, Trump's choice for the new Fed chair could have an effect on monetary policy and the strength of the US dollar. Still, most economists are of the view that monetary policy will be largely driven by the performance of the US economy. Inflation levels remain weak and may not reach Fed's target of 2 percent before 2020, but that has not dampened expectations of a December rate hike. According to CME FedWatch, the odds of a raise in December stand at 96 percent.

Trade Idea Wrap-up: USD/CHF – Buy at 0.9840

USD/CHF - 0.9890

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 0.9913

Kijun-Sen level : 0.9907

Ichimoku cloud top : 0.9862

Ichimoku cloud bottom : 0.9846

Original strategy :

Buy at 0.9840, Target: 0.9940, Stop: 0.9805

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9840, Target: 0.9940, Stop: 0.9805

Position : -

Target : -

Stop : -

As the greenback has retreated after rising to 0.9940, suggesting consolidation below this level would be seen and pullback to 0.9880, then test of the upper Kumo (now at 0.9862) cannot be ruled out, however, reckon support at 0.9838 would limit downside and bring another rise later, above said resistance at 0.9940 would extend recent rise from 0.9421 low to 0.9970, having said that, overbought condition should limit upside and price should falter well below psychological resistance at 1.0000, bring retreat later.

In view of this, we are looking to buy dollar again on further pullback as said support at 0.9838 should limit downside and bring another rise. A firm break below 0.9830 would defer and risk test of support at 0.9796 but only break of latter level would signal top is formed instead, risk retracement of recent rise to 0.9775-80, however, support at 0.973037 should remain intact.

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.3247

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.3189

Kijun-Sen level : 1.3189

Ichimoku cloud top : 1.3193

Ichimoku cloud bottom : 1.3158

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite falling marginally to 1.3110, as cable found decent demand there and has rallied in London session, the subsequent breach of previous resistance at 1.3228 has shifted risk to the upside as this move signals the fall from 1.3338 has ended at 1.3088, hence further gain to resistance at 1.3287 cannot be ruled out, however, break there is needed to provide confirmation, bring a stronger rebound towards 1.3338 resistance.

On the downside, whilst pullback to 1.3228 (previous resistance turned support) cannot be ruled out, recon 1.3190-00 would limit downside and 1.3150 should hold, bring another rebound later. As near term outlook has turned mixed, would not chase this rise here and would be prudent to stand aside for now.