Sample Category Title

Currencies: Will Draghi Prevent Further Euro Strength

Sunrise Market Commentary

- Rates: Position for hawkish outcome ECB

The Bond market reaction will be put against the consensus scenario of a 9-month extension of APP while slashing the pace of purchases to €30 bn/month from January. If consensus is right, the lifespan of the Bund rally will be limited. Our favourite scenario of a 6 month extension will put the Bund on the defensive with key yield resistance at 0.50% unable to stand. - Currencies: Will Draghi prevent further euro strength

The euro is resilient going into the ECB meeting . The dollar struggles as sentiment on risk turns less positive. Today, the ECB policy decision will decide the short-term fate of the euro. Given recent euro resilience, any perceived signs of hawkishness might support the single currency.

The Sunrise Headlines

- US stock markets corrected around 0.5% lower yesterday. Asian risk sentiment is mixed overnight with China outperforming.

- The ECB meeting today will decide on the future of APP. Consensus expects a 9-months extension to September 2018 while halving monthly purchases to €30 bn from January onwards. Risks are on the hawkish side of expectations. We favour only a 6-month extension until June 2018.

- South Korea’s economy kicked into gear in the third quarter (1.4% Q/Q) as renewed investment in construction and a return to growth for exports helped the country’s gross domestic product expand at the fastest pace in 7 years.

- The Bank of Canada held interest rates steady even as it said the economy was at or near full capacity, signalling it was willing to let the economy run a little bit hot amid uncertainty over NAFTA renegotiations. USD/CAD surged from 1.2650 to 1.28.

- “In my opinion, in order to make a fair deal with Nafta, you have to terminate the deal and you have to see where you’re going to come. And we’ll come out,” President Trump said.

- Today’s eco calendar contains EMU M3 money supply, US weekly claims and US trade balance. Swedish and Norwegian central banks meet as well. The US (7-yr Note) and Italy (I/L) tap the market

Currencies: Will Draghi Prevent Further Euro Strength

Will Draghi be dovish enough to avoid euro gains?

On Wednesday, trading showed its recent usual pattern. Core (EMU and US) yields extended their rise supported by strong eco data (German IFO and US durable orders). This rise in yields was fairly neutral for EUR/USD. Euro investors looked forward to the ECB meeting. USD/JPY and EUR/JPY outperformed and came close to MT highs. Later in the session, the rise in yields was aborted as equities fell prey to profit taking. This time, the dollar suffered most. EUR/USD returned north of 1.18 and closed at 1.1813. USD/JPY finished the session at 113.74.

Overnight, Asian equities are trading mixed with China outperforming. Asian investors are in wait-and-see modus ahead of the ECB policy decision and ahead of the results from major tech companies, expected later today. EUR/USD trades with a slightly positive bias in the low 1.18 area. Dollar is also losing a few ticks against the yen (EUR/USD at 113.45). AUD/USD struggles not to fall below the 0.77 handle.

Today, the US jobless claims, the advance trade balance and the pending home sales reports won’t be important, while halving monthly purchases to €30 bn from January 2018. We see risks for a shorter extension. Forward guidance on the end of APP will also be important. Even more important is the forward guidance on interest rate policy. Will the ECB repeat that rates will remain at the current levels for an extended period and well past the end of the APP programme? We think so as it is key to keep market expectations about the first rate hike at bay. Over the previous days, the euro traded strong across the board. The dollar failed to gain against the single currency even as interest rate differentials have risen sharply since early September. A prolongation of the APP by nine months and the ECB maintaining the forward guidance on interest rates should be negative for the euro. However, giving recent resilience of the single currency any hawkish deviations in the ECB assessment won’t go unnoticed in FX market

In that scenario, there are upside risks for the euro, especially short-term. Further down the road, issues like Spain, the replacement of Yellen and the US tax cuts come to support the dollar. For today, any ‘perceived hawkishness’ (or e.g. a positive tone on the economy) might already be enough to trigger a substantial up-tick in the single currency.

From a technical point of view, EUR/USD dropped below the 1.1823/ 1.2070 consolidation pattern, but there was no sustained follow-through price action, which was disappointing for EUR/USD bears. The pair needs to drop below 1.1670/62 to give comfort to EUR/USD bears. ON the topside, a break of the 1.1880 area might open the way for a retest of the 1.2092 correction top. The USD/JPY momentum was positive in September. The pair regained 110.67/95 resistance, a short-term positive. The 114.49 correction top is the next resistance. Sentiment improved further last week, but we still assume that a break beyond 114.49 will be difficult. This week’s failed return above 114 confirms our view.

EUR/USD: holding within established ranges going into ECB meeting

EUR/GBP

EUR/GBP holds near 0.89 as BoE rate hike is discounted

Yesterday, the focus for sterling trading turned from Brexit to the eco data. UK Q3 GDP growth printed slightly stronger than consensus. The ‘stronger’ Q3 GDP removed most market doubts on a BoE rate hike next week and kick-started a sterling rebound. EUR/GBP returned below 0.89 and closed the session at 0.8909. The rise in cable was even more impressive. The pair jumped from the 1.3120 area and closed the session at 1.3262. USD softness also play a role.

Today, the CBI retail data will be published. For October, a substantial setback is expected after a remarkable upswing in September. The correlation between the monthly CBI data and the ONS retail sales is very loose and the market reaction is thus modest at best. A one-off BoE rate hike is now ‘discounted’ after yesterday’s better than expected GDP data. We don’t expect the CBI data to amend it. Maybe there is room for a slightly bigger reaction in case of a weak than of a strong report. The euro reaction after the ECB will also be key for EUR/GBP.

EUR/GBP staged a strong uptrend from April till late August and set a top at 0.9307. Rising UK inflation and the BoE preparing markets for a November rate hike triggered a sterling rebound, but it has run its course. EUR/GBP supports at 0.8743 and 0.8652 proved too difficult to break. The recent rebound above 0.89 improved the ST technical picture of EUR/GBP, but for now there were no convincing follow-through gains. EUR/GBP 0.9026 is 50% retracement of the recent countermove.

EUR/GBP: holding tight ranges, but bottom looks well protected

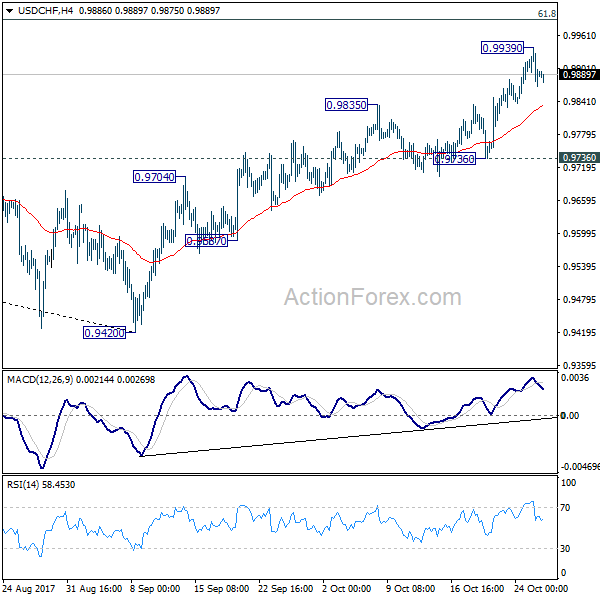

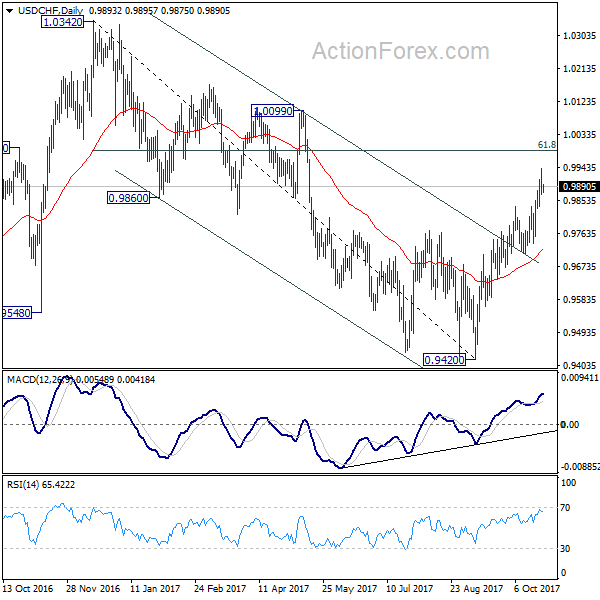

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9864; (P) 0.9901; (R1) 0.9934; More....

A temporary top in place at 0.9939 and intraday bias is turned neutral first. Near term outlook remains bullish as long as 0.9736 support holds. Above 0.9939 will target 61.8% retracement of 1.0342 to 0.9420 at 0.9990. Sustained break there will pave the way to retest 1.0342 high. However, firm break of 0.9736 support will dampen our bullish view and suggest that rebound from 0.9420 is completed.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could develop into a medium term move and target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9587 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

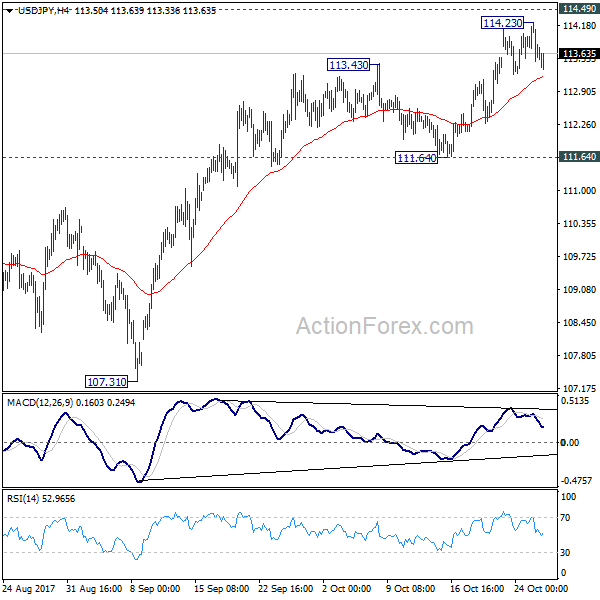

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.39; (P) 113.81; (R1) 114.16; More...

A temporary top is formed again at 114.23, ahead of 114.49 key resistance. Intraday bias is turned neutral first. More consolidation would likely be seen in near term. but after all, outlook stays bullish as long as 111.64 support holds. Decisive break of 114.49 resistance will confirm that correction pattern from 118.65 has completed at 107.31 already. And USD/JPY should then target a test on 118.65. However, break of 111.64 will dampen this bullish view and suggests that rebound from 107.31 has completed.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completed. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming.

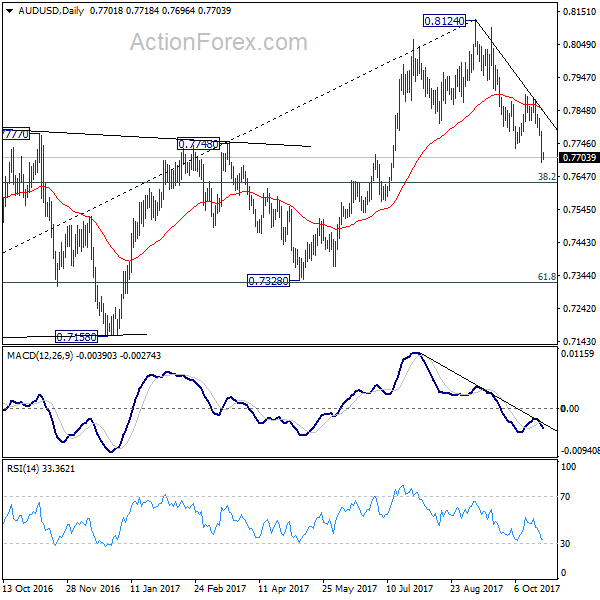

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7667; (P) 0.7725; (R1) 0.7760; More...

Intraday bias in AUD/USD remains on the downside as fall from 0.8124 is still in progress. Deeper decline would be seen to medium term fibonacci level at 0.7628 first. Current development affirms the case of medium term reversal. Firm break of 0.7628 will pave the way to 0.7328 key support next. On the upside, above 0.7769 minor resistance will turn intraday bias neutral first. But outlook will remain cautiously bearish as long as 0.7896 resistance holds.

In the bigger picture, rise from 0.6826 medium term bottom is seen as corrective pattern. Current development suggests that it might be completed with three waves up to 0.8124 already. Break of 38.2% retracement of 0.6826 to 0.8124 at 0.7628 will affirm this bearish case. And, decisive break of 0.7328 key cluster support (61.8% retracement at 0.7322) will confirm and bring retest of 0.6826 low. In case rise from 0.6826 resumes and extends, strong resistance should be seen at 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside.

Market Update – Asian Session: South Korea Q3 GDP Surprises To The Upside

Asia Summary

Asian equity markets have opened the session mostly lower following the negative leads out of the US and ahead of the later today ECB decision.

Earnings reports out of Asia have been in focus on today’s session. Japanese industrial company Fanuc has traded higher by over 2%, as it raised its FY18 outlook.

In the tech sector, Japan’s Line Corp has gained over 13% as its Q3 earnings beat expectations. At the same time, chip equipment company Advantest has declined by over 3% after the company reduced its FY net profit forecast. South Korea’s Hynix has traded marginally lower after reporting in line profits and better than expected revenues.

The Shanghai Composite Consumer index has gained over 1.8%, as liquor producer Kweichow Moutai has risen by over 6% following its earnings report

In the financial sector, Daiwa Securities has gained over 4%, as the board announced an up to 3.1% share buyback with the H1 financial results. Singapore-based OCBC has traded flat after reporting in line Q3 results. In Australia, ANZ Bank has declined by over 1% on weaker than expected FY17 profits.

Chinese insurance companies are generally higher, as China’s 10-year bond yield has continued to trade at multi-year highs. The rise in bond yields follows Wednesday’s increase in US Treasury yields. China is also marketing its first US dollar denominated bonds since 2004. According to initial reports, orders for the 2 tranche issuance are said to exceed $10B.

South Korea’s 3-year bond yield has risen on the session, as the country’s prelim Q3 GDP data showed the fastest q/q growth rate in over 7-years.

Looking ahead, traders are expected to focus on the later today ECB decision. Japanese companies due to report earnings later today include Fuji Electric, Fujitsu, Hitachi, Koito Mfg Co, Kyowa Hakko Kirin, Mitsubishi Motors, NTT Docomo, Nomura Real Estate, Oki Electric, Osaka Gas, SBI Holdings, Seiko Epson and Tohoku Electric Power.

Companies out of China and Hong Kong expected to report results include Aluminum Corp of China, BYD, Bank of Communications, China Coal Energy, China Eastern Airlines, China Grand Auto, China Merchants Bank, China Pacific Insurance, China Railway, China Shenhua Energy, China Unicom, China Vanke, Everbright Securities, Great Wall Motor, Inner Mongolia Bao Tou Steel, Jiangxi Copper, New China Life Insurance, Ping An Insurance, Poly Real Estate, Sinopec Shanghai, Sinopharm Group and Xinjiang Goldwind.

US companies due to report results on Thursday include, Alphabet, Altria, Amazon, American Airlines, Baidu, Boston Beer, Charter Communications, ConocoPhilips, First Solar, Ford, Intel, Microsoft, Potash , UPS, Valero, Western Digital and Xerox.

Key economic data

(NZ) NEW ZEALAND SEPT TRADE BALANCE (NZ$): -1.14B V 0.9BE; YTD -2.91B V -2.71BE

(KR) SOUTH KOREA Q3 PRELIM GDP Q/Q: 1.4% V 0.9%E; Y/Y: 3.6% V 3.0%E

(JP) JAPAN SEPT SERVICES PPI Y/Y: 0.9% V 0.8%E

(AU) AUSTRALIA Q3 EXPORT PRICE INDEX Q/Q: -3.0% V -4.0%E; IMPORT PRICE INDEX Q/Q: -1.6% V -1.5%E

Speakers and Press

Japan

(JP) Japan PM Abe Adviser Hamada: Abe's new approach for sales tax revenue is good

Korea

(KR) South Korea Finance Min Official: Q4 q/q GDP to be just over 0% as growth was focused on Q3

(KR) South Korea and China said to seek to resolve tensions related to Thaad - South Korean Press

(KR) North Korea official warns that hydrogen bomb threat should be taken literally - financial press

China/Hong Kong

(CN) China said to set initial pricing talk for planned 5 and 10-year US dollar denominated bonds (first USD issuance since 2004)

(CN) China Communist Party Sr Official: Will not set target to double GDP from 2021

(CN) China Official: China has shifted gears to medium-high growth rate

Australia/New Zealand

(NZ) New Zealand PM Designate Ardern to disclose 100-day plan early next week; taking advice on whether to have 'mini-budget'

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.3%, Hang Seng -0.2%; Shanghai Composite +0.5%; ASX200 -0.0%, Kospi -0.1%

Equity Futures: S&P500 +0.0%; Nasdaq100 +0.0%, Dax -0.1%; FTSE100 -0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1833-1.1813; JPY 113.71-113.37; AUD 0.7717-0.7697;NZD 0.6897-0.6872

Dec Gold +0.2% at $1,281/oz; Dec Crude Oil -0.2% at $52.09/brl; Dec Copper +0.1% at $3.18/lb

(NZ) New Zealand sells NZ$150M in 3.5% 2033 bonds; avg yield 3.3655%; bid-to-cover 2.86x

(CN) PBoC OMO: Injects CNY120B in 7 and 14-day reverse repos v CNY160B injected prior; injects net CNY20B v CNY0B prior

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT 6.6288 V 6.6322 PRIOR

(JP) Japan MoF sells ¥2.199T in 0.1% (prior 0.1%) 2-yr JGBs; avg yield -0.1430% v -0.1490% prior; bid-to-cover 5.93x v 4.97x prior

(JP) Japan MoF sells ¥4.439T in 3-month bills; avg yield -0.1961%

Equities notable movers

Australia/New Zealand

ANZ.AU Reports FY17 (A$) Net 6.41B v 6.7Be; Cash profit 6.94B v 7.0Be; Op 20.3B v 20.7Be; -1.7%

RFX.AU Gives business update regarding Thailand operations; +10%

ISD.AU Guides FY18 (A$) EBITDA 32-36M; Rev 133-138M; To exit King Content business; Reaches settlement with Meltwater; -37%

Japan

3938.JP Reports 9-month Net profit ¥12.1B v 5.3B y/y, Op ¥24.5B v ¥18.3B y/y, Rev ¥121.2B v ¥103.2B y/y; +15%

6755.JP Reports H1 Net ¥5.8B v ¥5.7B y/y; Op ¥7.8B v ¥12.6B y/y; Rev ¥123.1B v ¥122.5B y/y; -6.7%

China/Hong Kong

3606.HK Reports 9M Net 2.14 v 2.18B y/y, Rev 13.4B v 11.6B y/y; +5.5%

Korea

000660.KR Reports Q3 (KRW) Net 3.05T v 3.0Te; Op 3.7T v 3.8Te; Rev 8.10T v 7.9Te

Race For Fed Chair Is Narrowing

Market movers today

The big event of the day is the ECB meeting. The QE extension details are set to be released at 13:45 CEST in the ‘monetary policy decision' press release, while ot her technicalities will first be announced in the press conference at 14:30 CET. We expect the ECB to announce a QE extension by nine months at a pace of EUR30bn. Apart from a scaling down of QE purchases, we do not expect the ECB to make any changes to its forward guidance at the upcoming meeting.

However, we also have central bank action in the Nordic region with both the Riksbank and Norges Bank decisions at 9:30 and 10:00 CEST, respectively. In terms of the Riksbank, our view is that the will Riksbank end QE (but continue to reinvest coupons) by year -end but that the announcement will wait until the December policy meeting. Also, we do not expect changes to the Swedish repo rate forecast when the Riksbank meets. In Norway, we expect Norges Bank to stay on hold, as it is one of the intermediate meetings without a Monetary Policy Report and a press conference. Please see page two for further details.

Selected market news

Race for fed chair is narrowing. According to Bloomberg sources (link), President Trump is now ruling out National Economic Council Director Gary Cohn becoming the next leader of the Federal Reserve. The field thus seems to have been narrowed to Fed Governor Jerome Powell, who appears to be the front runner, followed by incumbent Fed Chair Janet Yellen and Stanford University economist John Taylor.

Strong US data out yesterday. Durable goods orders rose 1.3% in September (0.3% expected, 1.3% in August revised higher from 1.1%) indicators that business capex spending remained on a solid footing in Q3, which should cushion the negative impact on GDP from the hurricanes. Separately, new home sales surprised to the upside, surging 18.9% in September to the highest level in 10 years.

Bank of Canada puts hiking cycle on hold for now. At yest erday's BoC meeting, rates were kept steady as expected following two consecutive hikes in July and September. Moreover, the statement indicated that policy makers are now on hold; in addit ion to highlighting the negative impact of the strong currency on inflation and exports, for the first time growing risks stemming from a renegotiation of NAFTA were also noted. As a result , the Canadian dollar weakened in the wake of the announcement as expectat ions for further hikes were priced out .

US stocks lower, while rates increased. The S&P index fell 0.49% yesterday as earnings reports from several companies including AMD, AT&T, Boeing and Chipot le disappointed. Furthermore, a story in the Wall Street Report suggest ing that Republicans are still considering limits on 401(k) retirement savings plans, which could dampen flows into investment plans, also weighed on sentiment . However, bond yields rose, supported by the strong economic data, causing 10-year yields to hit a seven-month high of 2.475%.

Aussie Dollar Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the AUD declined 0.96% against the USD and closed at 0.7702.

LME Copper prices declined 1.5% or $103.0/MT to $6970.0/MT. Aluminium prices rose 0.3% or $5.5/MT to $2149.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7713, with the AUD trading 0.14% higher against the USD from yesterday’s close.

The pair is expected to find support at 0.7691, and a fall through could take it to the next support level of 0.7670. The pair is expected to find its first resistance at 0.7733, and a rise through could take it to the next resistance level of 0.7754.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

German Business Confidence Soared Unexpectedly To A Record High In October

For the 24 hours to 23:00 GMT, the EUR rose 0.43% against the USD and closed at 1.1816, after an unexpected rise in German Ifo data suggested that business confidence remains buoyant as the nation’s economic fundaments remain strong.

Germany’s Ifo business climate index unexpectedly advanced to a record high level of 116.7 in October, confounding market expectations for a drop to a level of 115.1 and following a revised reading of 115.3 in the prior month. Further, the nation’s Ifo business expectations index surprised to the upside, climbing to a level of 109.1 in October. Market participants had envisaged for a fall to a level of 107.3, compared to a revised reading of 107.5 in the previous month. Additionally, the nation’s Ifo current assessment index recorded an unexpected rise to a level of 124.8 in October, against market consensus for a drop to a level of 123.5. In the previous month, the index had registered a revised reading of 123.7.

Macroeconomic data indicated that the preliminary durable goods orders in the US jumped to a three-month high in September, after it increased more-than-expected by 2.2%, amid robust demand for transportation equipment, suggesting that business spending remained robust in the third quarter. Markets had anticipations for a rise of 1.0%, following a rise of 2.0% in the previous month. Further, the nation’s new home sales unexpectedly climbed 18.9% on a monthly basis to a level of 667.0K in September, surging to a ten-year high level and providing fresh hints that the housing market was regaining momentum after appearing to stall in recent months. New home sales had registered a revised reading of 561.0K in the previous month, while markets were anticipating for a drop to a level of 554.0K.

Other data revealed that the US mortgage applications dropped 4.6% in the week ended 20 October 2017. In the previous week, mortgage applications had climbed 3.6%.

In the Asian session, at GMT0300, the pair is trading at 1.1825, with the EUR trading 0.08% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.1775, and a fall through could take it to the next support level of 1.1725. The pair is expected to find its first resistance at 1.1854, and a rise through could take it to the next resistance level of 1.1883.

Moving ahead, all eyes will be on the European Central Bank’s (ECB) interest rate decision, due later in the day, wherein the central bank is expected to shed more light on the tapering of its quantitative easing programme. Moreover, the US initial jobless claims followed by advance goods trade balance and pending home sales data, both for September, all slated to release later in the day, will garner significant amount of market attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

British Economy Grew Faster-Than-Expected In 3Q 2017

For the 24 hours to 23:00 GMT, the GBP rose 1.03% against the USD and closed at 1.3268, triggered by better-than-expected UK's GDP report.

Data showed that Britain's preliminary GDP climbed more-than-expected by 0.4% on a quarterly basis in the third quarter of 2017, driven by strong performance in services and manufacturing sector, thus raising the odds of that the Bank of England will likely raise interest rate next month. Market had expected GDP to rise by 0.3%, after recording an expansion of 0.3% in the previous quarter.

In the Asian session, at GMT0300, the pair is trading at 1.3268, with the GBP trading flat against the USD from yesterday's close.

The pair is expected to find support at 1.3159, and a fall through could take it to the next support level of 1.3050. The pair is expected to find its first resistance at 1.3328, and a rise through could take it to the next resistance level of 1.3388.

In absence of macroeconomic releases in the UK today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Extends Its Gains In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.27% against the JPY and closed at 113.63.

In the Asian session, at GMT0300, the pair is trading at 113.54, with the USD trading 0.08% lower against the JPY from yesterday’s close.

The pair is expected to find support at 113.19, and a fall through could take it to the next support level of 112.85. The pair is expected to find its first resistance at 114.06, and a rise through could take it to the next resistance level of 114.59.

Going forward, traders would eye the release of Japan’s national consumer price index for September, due to release overnight.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.