Sample Category Title

Swiss ZEW Economic Expectations Index Advanced In October, UBS Consumption Indicator Rose In September

For the 24 hours to 23:00 GMT, the USD declined 0.16% against the CHF and closed at 0.9892.

On the macro front, Switzerland’s ZEW economic expectations index rose to a level of 32.0 in October. In the previous month, the index had registered a reading of 28.0. Further, the nation’s UBS consumption indicator registered a rise to 1.56 in September, after recording a revised reading of 1.50 in the prior month.

In the Asian session, at GMT0300, the pair is trading at 0.9890, with the USD trading marginally lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9859, and a fall through could take it to the next support level of 0.9829. The pair is expected to find its first resistance at 0.9930, and a rise through could take it to the next resistance level of 0.9971.

Amid no major macroeconomic releases in Switzerland today, investors will focus on global macroeconomic factors for further direction.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

BoC Holds Interest Rate Steady, Will Be Cautious In Making Future Adjustments To Rate

For the 24 hours to 23:00 GMT, the USD rose 1.03% against the CAD and closed at 1.2802.

The Canadian Dollar lost ground, after the Bank of Canada (BoC), at its latest monetary policy meeting, expressed caution on the prospects of future rate increases.

The BoC, as widely expected, opted to leave the benchmark interest rate unchanged at 1.00%, but suggested future increases are still likely, albeit at a more gradual pace. In its monetary policy statement, the central bank disclosed that it decided to hold interest rates as the recent strength of the Canadian dollar is expected to slow the pace of inflation. The central bank is now projecting inflation to rise to 2.0% a bit later in 2018 than previously expected and forecasted Canada’s economy to expand by 3.1% in 2017, 2.1% in 2018 and 1.5% in 2019.

In the Asian session, at GMT0300, the pair is trading at 1.2792, with the USD trading 0.08% lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.2682, and a fall through could take it to the next support level of 1.2573. The pair is expected to find its first resistance at 1.2859, and a rise through could take it to the next resistance level of 1.2927.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Elliott Wave View: FTSE Short-Term

FTSE Short-Term Elliott Wave view suggests that the Index ended Primary wave ((4)) with the decline to 7199.5. The rally from there is unfolding as an impulse Elliott Wave structure where Minor wave 1 ended at 7327.5 and Minor wave 2 ended at 7289.75. Minor wave 3 rally ended at 7494.34, and Minor wave 4 pullback ended at 7473.12. Minor wave 5 ended at 7565.11 and this also ended Intermediate wave (A) of a zigzag Elliott Wave structure from 9/15 low (7199.5).

Intermediate wave (B) is currently in progress as a double three Elliott Wave structure. Down from 7565.11 high, Minor wave W ended at 7485.42 and Minor wave X bounce ended at 7560.04. Near term, Intermediate wave (B) is expected to complete soon at 7432.25 – 7462.96 and Index should then resume the rally to new high or at least bounce in 3 waves. We don’t like selling the Index.

FTSE 1 Hour Elliott Wave Analysis

Zigzag is a 3 waves corrective pattern which is labelled as ABC. The subdivision of wave A is in 5 waves, either as impulse or diagonal. The subdivision of wave B can be any corrective structure. Finally, the subdivision of wave C is also in 5 waves, either as impulse or diagonal. Thus, zigzag has a 5-3-5 structure. Wave C typically ends at 100% – 123.6% of wave A.

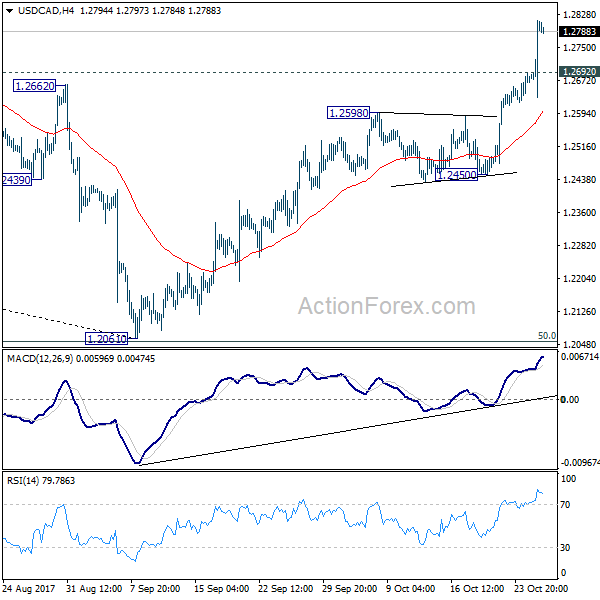

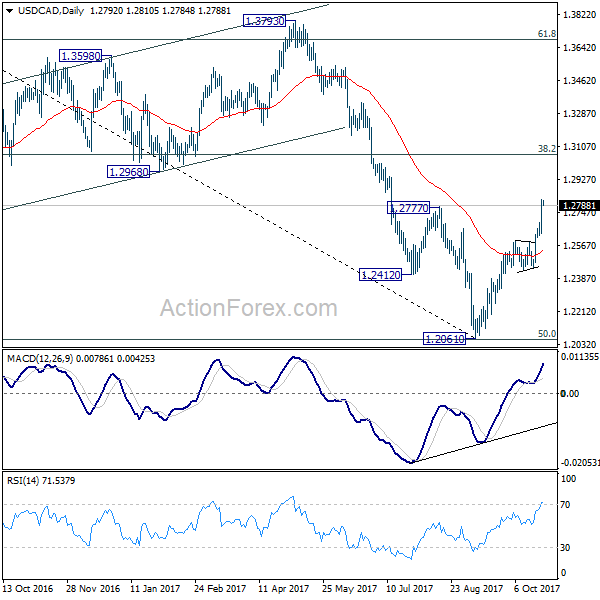

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2679; (P) 1.2748; (R1) 1.2864; More....

USD/CAD surges to as high as 1.2816 so far. The breach of 1.2777 resistance affirms our view of medium term reversal. Intraday bias remains on the upside. Sustained break of 1.2777 will pave the way to 38.2% retracement of 1.4689 to 1.2061 at 1.3065 next. On the downside, below 1.2692 minor support will turn intraday bias neutral and bring consolidations. But outlook will remain bullish as long as 1.2450 support holds.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. And in that case, USD/CAD should target 1.3793 key resistance next. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

Euro Firm as Markets Await ECB Recalibration, Loonies Weak after Dovish BoC

Euro recovers overnight against Dollar and remains generally firm this week. It's just overpowered by Sterling which was shot up by strong Q3 GDP data. ECB policy decision and press conference will be the main highlight for today. The central bank is widely expected to announce recalibration of its EUR 60B a month asset purchase program, after it expires by the end of this year. The general consensus is that ECB will half the program to EUR 30B per month, but give it a 9-month extension till end of September 2018.

One important thing to note is recent repeated comments of ECB chief economist Peter Praet. He noted that calmness in the markets makes it more appropriate for smaller monthly purchases with longer duration, because investors are more patient. This could be a yardstick in gauging how comfortable ECB policy makers are regarding economic and inflation outlook. That is:

- = EUR 30B, = 9 months - base case

- = EUR 30B, > 9 months - dovish

- = EUR 30B, < 9 months - hawkish

- > EUR 30B, = 9 months - dovish

- > EUR 30B, > 9 months - very dovish

- > EUR 30B, < 9 months - still dovish

- < EUR 30B, = 9 months - hawkish

- < EUR 30B, < 9 months - very hawkish

- < EUR 30B, > 9 months - cautiously hawkish

BoC turned cautious, Loonie dives

Canadian Dollar tumbles sharply overnight after BoC rate decision. Showing genuine concerns over the downside risks to inflation, BoC indicated it would be more 'cautious' over future rate hike decisions. In the concluding statement, policymakers stressed that 'while less monetary policy stimulus will likely be required over time, Governing Council will be cautious in making future adjustments to the policy rate'. The tone in this October appears more dovish than previous ones, likely resulting from recent developments of disappointing progress in NAFTA negotiations, household debt levels and appreciation of Canadian dollar. More in BOC Pledges Cautiousness In Future Rate Hike

Yen and Franc rebounded strongly

Yen and Swiss Franc staged strong rebound overnight. Pull back in equities is still as a contributing factor. DOW lost -0.48%, S&P 500 lost -0.47%, NASDAQ lost -0.52%. But the rally in 10 year yield indicates that it's likely just a temporary pull back after record runs. TNX indeed closed higher by 0.038, at 2.444, and is still on course for 2.621 high later this year. The more likely factor for yesterday's rebound in Yen and Franc is probably receding expectation for aggressive global rate hikes. That followed after disappointing Australia CPI and then dovish BoC statement. But it should still be noted that the trend of monetary stimulus exit is still there, probably just not as fast as prior BoC hikes implied.

Yesterday's sharp fall in AUD/JPY now puts 87.24 near term support in focus. Firm break there will be an early sign of medium term topping, on bearish divergence condition in daily MACD. Further break of 85.44 support will bring deeper fall to 81.48 cluster (50% retracement of 72.39 to 90.29 at 81.34) before drawing enough support for sustainable rebound.

On the data front

New Zealand trade deficit narrowed slightly to NZD 1143M in September. Australia import price index dropped -1.6% qoq in Q3. Japan corporate service price index rose 0.9% yoy in September. German Gfk consumer sentiment, Eurozone M3 and UK CBI reported sales will be released in European session. US will release jobless claims, wholesale inventories, trade balance and pending home sales.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2679; (P) 1.2748; (R1) 1.2864; More....

USD/CAD surges to as high as 1.2816 so far. The breach of 1.2777 resistance affirms our view of medium term reversal. Intraday bias remains on the upside. Sustained break of 1.2777 will pave the way to 38.2% retracement of 1.4689 to 1.2061 at 1.3065 next. On the downside, below 1.2692 minor support will turn intraday bias neutral and bring consolidations. But outlook will remain bullish as long as 1.2450 support holds.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. And in that case, USD/CAD should target 1.3793 key resistance next. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Sep | -1143M | -900M | -1235M | -1179M |

| 23:50 | JPY | Corporate Service Price Y/Y Sep | 0.90% | 0.80% | 0.80% | |

| 0:30 | AUD | Import Price Index Q/Q Q3 | -1.60% | -1.50% | -0.10% | |

| 6:00 | EUR | German GfK Consumer Confidence Nov | 10.8 | 10.8 | ||

| 8:00 | EUR | Eurozone M3 Y/Y Sep | 5.00% | 5.00% | ||

| 10:00 | GBP | CBI Realized Sales Oct | 14 | 42 | ||

| 11:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | ||

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | USD | Wholesale Inventories Sep P | 0.90% | |||

| 12:30 | USD | Initial Jobless Claims (OCT 21) | 236K | 222K | ||

| 12:30 | USD | Advance Goods Trade Balance (USD) Sep | -63.8B | -62.9B | ||

| 12:30 | USD | Retail Inventories M/M Sep | 1.00% | 0.90% | ||

| 14:00 | USD | Pending Home Sales M/M Sep | 0.60% | -2.60% | ||

| 14:30 | USD | Natural Gas Storage | 51B |

Market Morning Briefing: Surprised By The Sharp Rise In The Pound

STOCKS

Overall major stock indices are in a rally and may soon reach their exhaustion point from where a sharp correction is possible in the medium to long term.

The 2-month long rally in Dow (23329.46, -0.48%) from levels near 21750 could possibly be reaching its exhaustion levels in the near term. We need to remain cautious as the index may be vulnerable to a sharp correction in the medium term. Immediate upside target is 24000 from where a correction is possible.

No major movement expected in Dax (12953.41, -0.46%) while it trades between 12900-13065 levels. Only a break on either side of this range would give us some clarity on further direction.

Nikkei (21738.39, +0.14%) has broken above the initial target of 21600 and is headed towards the next crucial levels at 22666 while the index sustains the current rise above 21600. A rally in the coming sessions is expected with some interim corrections followed by a long term fall which could start soon. Look for an initial turn-around in Dollar Yen for cues.

Shanghai (3409.47, +0.37%) is trading above 3400 just now and could target 3420-3425 in the coming sessions before facing a rejection back towards 3400 or lower. 3425 is a decent resistance which could hold in the near term. For the week, Shanghai looks bullish.

Nifty (10295.35, +0.86%) opened with a gap-up at 10333 as expected but eventually came down to test 10250 before closing at higher levels. 10350-10400 is an immediate resistance on the upside which is likely to keep the index down for a few sessions at least. A sharp correction in Nifty is on the cards for the medium term. We need to be cautious near current levels.

COMMODITIES

Gold (1279.39) is trading narrow since the last couple of sessions. While above 1275, there is still some scope for the price to rise towards 1290/95 again; else a fall below 1275 if seen and sustains could bring in fresh weakness in Gold. For now the support on the daily candle chart holds and remains intact.

Brent (58.37) is trying to attempt towards 59 and could eventually move up to test 60-61 levels in the next couple of weeks. Near term looks bullish with some small interim corrective dips.

WTI (52.09) looks stable just now. There could be some chances of testing 53 from where a slight rejection is possible. Resistance on the weekly candles is likely to push WTI prices to lower levels in the near term.

Copper (3.1875) could be ranged sideways within 3.25-3.10 region in the near term. Thereafter a corrective fall towards 3.00 or lower is possible in the longer run.

FOREX

Further strength in the Euro (1.1827) overnight as the market shies away from going in Short into today's important ECB meeting where Draghi is expected to unveil the ECB's plan on "recaliberating" the ongoing QE. Intra-day range would be 1.1740-1850. A break above 1.1850 sets the Euro on course to test 1.20 in a couple of weeks.

The Euro-Yen (134.27) moves up further, this time on Euro strength, continues to target 135+ in the coming days. This is despite the dip in Dollar-Yen (113.55) from yesterday's high of 114.25, such dip possibly increasing the strength of the long-term Resistance at 114.50. "Outside" Resistance seen at 115.00.

There are chances that the dip in the Dollar Index (93.55) from the Resistance at 94.00 can help keep Dollar-Yen below 114.50-115.00.

Surprised by the sharp rise in the Pound (1.3268), which has rallied strongly on a strong UK GDP data, which has brought back chances of a rate hike in next week's BOE meeting on 2nd Nov. This possibly changes the near-term direction of the market from 1.30 on the downside towards 1.34+ on the upside.

The Aussie (0.7713) dipped to 0.7690 (200-day MA) yesterday and is trading just above that today. The earlier resemblence with the Euro has been broken and unless a strong bounce is seen from here, the Aussie might be vulnerable to some more dip towards 0.7655.

Dollar-Yuan (6.6335) came close to testing 6.65 yesterday, a level that can still be seen in the coming days. Dollar-Rupee (64.89/90) fell sharply in late trade yesterday and may trade quiet today.

INTEREST RATES

Higher bond yields all around it seems.

Important ECB meeting today, where Draghi is expected to unveil plans for recabilerating the ongoing QE. Market views range from (a) QE will be cut from 60 bln p.m. down to 40-10 bln p.m. while (b) duration of the programme will be extended by 6-12 months, or may even be made open-ended. There does not seem to be a consensus within the above possibility range.

German 10 Yr (0.47%) has written 1bp more yesterday while the US 10Yr (2.44%) has risen even more, past the resistance at 2.40% mentioned yesterday. This has pushed the German-US 10Yr Spread (-1.96%) just below the earlier mentioned Support at -1.95%. This could be a cause for concern for the Euro unless there is a strong bounce after the ECB meeting.

The UK 10yr (1.41%) has also risen past earlier resistance near 1.38%. The Japan 10Yr (0.07%) is also testing its long-term down-trendline at current levels. Need to see if that also rises ahead of the BOJ meeting next week (Tuesday).

Keep an eye out for whether the FED will surprise with a rate hike at its next meeting on 1st Nov, next Wednesday.

BOC Pledges Cautiousness In Future Rate Hike

Showing genuine concerns over the downside risks to inflation, BOC indicated it would be more 'cautious' over future rate hike decisions. In the concluding statement, policymakers stressed that 'while less monetary policy stimulus will likely be required over time, Governing Council will be cautious in making future adjustments to the policy rate'. The tone in this October appears more dovish than previous ones, likely resulting from recent developments of disappointing progress in NAFTA negotiations, household debt levels and appreciation of Canadian dollar. USDCAD jumped about +1% after the announcement.

After unexpectedly taking the policy rate higher, by +25 bps, to 1% in September, the BOC kept its powder dry this month. During the period, incoming data have sent a mixed note. GDP growth in July was flat from June, ending the 8-month uptrend. Retail sales surprisingly contracted -0.3% m/m in August, following a +0.4% growth in July. Excluding sales at gas stations and auto dealers, retail sales was down -1.3% for the month. On inflation, headline CPI accelerated to +1.6% in September, from +1.4% a month ago. However, if gasoline prices were excluded, inflation climbed +1.1%. Concerning BOC’s preferred measures, trimmed CPI rose to +1.5%, while both median and common CPI stayed unchanged at +1.8% and +1.5% respectively. Canada’s unemployment rate stayed at 9-year low of 6.25 in September while wage growth remained limited.

Against this backdrop, BOC retained the view that domestic economy has operated 'close to its potential'. However, it remained concerned over the slack in the labour market, given the limited wage growth. The officials upgraded the GDP growth forecasts from 2017 to 2019. The economy is expected to expand +3.1% (previous: +2.8%) this year, before easing to +2.1% (previous: +2%) in 2018 and to +1.5% (previous: +1.6%) in 2019. Inflation forecast for 2018 is adjusted slightly lower to +1.7%, from +1.8% previously, while that for 2019 stayed unchanged at +2.1%. The central bank anticipates inflation to reach the +2% target by the second half of next year.

At the press conference, governor Poloz dismissed concerns over overshooting of inflation. Rather he suggested that 'given our recent history with inflation running below target, we continue to be more preoccupied with the downside risks to inflation'. The accompanying statement also reminded that the remaining slack in labour markets suggested that there is 'room for more economic growth than the Bank is projecting without inflation rising materially above target'.

Notwithstanding the fact that the loonie has dropped about -6% against US dollar from its high made on September 8, BOC warned of the strength in the exchange rate. This indicates the central bank’s worry over the currency’s impact on inflation and exports growth. Indeed, it noted the reason for it to push backward the time for inflation to reach the +2% target is 'recent strength in the Canadian dollar'. Meanwhile, it also warned that 'projected export growth is slightly slower than before, in part because of a stronger Canadian dollar than assumed in July'.

In the concluding statement, BOC pledged to stay 'cautious' in making future monetary decision, reinforcing that it would be 'guided by incoming data to assess the sensitivity of the economy to interest rates, the evolution of economic capacity, and the dynamics of both wage growth and inflation'.

Bank of Canada Holds Steady But Has a Bias to Tighten amid Limited Slack

Highlights:

- Nominal The overnight rate was left unchanged at 1% after rate hikes in both July and September.

- The bank thinks the economy is operating close to its potential but noted some evidence of remaining labour market slack that could give the economy more room to run without generating inflation.

- Uncertainty around NAFTA renegotiation was cited as the main international risk to the economic outlook. A breakdown of talks would likely lead to a more cautious approach from the Bank of Canada.

- The bank expressed a tightening bias, noting less monetary policy stimulus is likely over time, but indicated they will proceed cautiously and will be guided by incoming data.

- The bank discussed whether some structural factors might be weighing on inflation but they remain of the view that the degree of slack in the economy is the main determinant of inflation.

Our Take:

As expected, the Bank of Canada took a pass on raising interest rates today after consecutive 25 basis point hikes at each of their last two meetings. While maintaining an explicit tightening bias, the policy statement sounded a bit more cautious and kept a good deal of flexibility on the pace at which stimulus will be withdrawn. The bank remains constructive on the economic outlook, noting broadly-based growth though still predicting a more modest pace of activity going forward as housing and consumer spending shift down a gear. With the economy's speed limit picking up amid productivity-enhancing business investment, they see the economy remaining fairly close to full capacity, or possibly modestly above, over the next year. Monetary policy remains data dependent and how growth shakes out relative to potential in the coming quarters will be an important factor in the pace of future rate increases.

Our current forecast is for the overnight rate to be raised to 2% by the end of next year. That assumes a rate hike in December, although such a move looks a bit less likely given the bank's more cautious tone today. There is a risk that the Bank of Canada holds off on resuming tightening until early 2018.

Kiwi Momentum Halted At Support. For Now

Just a quick post today to highlight the price action in NZD/USD. The Kiwi is a pair we’ve been following from a while now and one that has had a HUGE momentum move:

NZD/USD Daily:

As you can see, even during a large momentum drop like what you see in the above chart, technical levels are always at least respected.

Respected doesn’t necessarily mean held, but you can see the effect that they have on halting momentum at least at the first touch here.

The US Dollars Dual Personalities

The US Dollars dual personalities

The US dollars dual personalities were in full view overnight as an endless stream of headline surprises weighed on investors sentiment while some localised circumstances played in its favour. Indeed the numerous idiosyncratic storylines had currency markets rocking in every pocket of the globe, however, in general, the USD dollar lost some momentum overnight as concerns resurfaced over the pace of Fed normalisation, and a case of the willies gripped investors ahead of The House Vote on the budget resolution.

Not surprisingly, Republican infighting once again threatens to derail the vote as clouds gather over state and local income tax provision.

Uncertainty over the next Fed Chair has traders double and even triple guessing their best-educated guess. Indeed, the agonising wait is taking its toll on positioning as the longer the process gets drawn out, the more nervous the market becomes and then starts to wonder if the what appeared to be the unlikely scenario of a status quo wins out.

Australian Dollar

There’s entirely no way to sugar coat yesterday’s domestic CPI miss, and the broadcast of a re-weighing of the CPI basket for the January print only adds to the misery.

If there was any doubt about RBA policy, the CPI print suggests they will be parked in neutral for some time as the lack of any wage inflation to mollify the household debt burden will continue to weigh dovish on RBA policy. Indeed all eyes will be focused on the RBA’s inflation spin in the Statement of Monetary Policy next month where any sliding revision to the CPI forecast could spell doom for the Aussie dollar.

Japanese Yen

Market chatter elevated after coming within a hair’s breadth of breaking the critical 114.25, and the burning question remains can we push through this level which has been the markets undoing for the better part of 2017.

Technical hoodoo aside, breaching the 10 Y UST 2.4% inflexion point and the surging Nikkei suggests yes.But with the US tax reform getting more priced into the risk equation, a significant near-term move towards 115 will need some help from a hawkish shift at the Fed helm for the dollar bulls to have their cake and eat it also.

The Euro

Expectations have been tempered by ECB speak and the dearth of leaks. But of course, when it comes down to crunch time the concern is that the market has written today’s meeting off as a non-event more or less expecting currency neutrality and continuation of well-travelled ranges between 1.1675 -1.1875

While the market is not expecting anything earth-shattering from Draghi dealers will none the less trade the ECB policy lean, but the risk of a hawkish surprise is real and we could see a further extension of recent EUR gains as investors hedge for that possibility

Canadian Dollar

What was thought to be the beginning of a Bank of Canada interest rate hike cycle is being discounted as nothing more than a removal of emergency accommodation. Governor Poloz is back roosting with doves. With interest rate differential likely to favor the long USD position going forward after the BoC expressed concerns about downside inflation risk, the Canadian dollar could remain on its back foot heading into 2018

FX Asia

Risk sentiment rand out of gas yesterday as local equity markets moved into consolidation mode with US tax reform narrative and the Fed Chair search still the key themes.

Indian Rupee

The Rupee is back on investor radar on the bank recapitalization headlines underpinning local equity markets. USDINR moved lower aggressively as investors refocus medium and longer-term outlooks based on these extremely positive developments in the banking sector that have been weighted down by substantial loan loss provisions. In early trade, the USDINR is trading just below 64.90 level, but further short-term gains could be challenged by the shifting USD sentiment around the Fed Chair announcement.

The Malaysian Ringgit

The Ringgit is trading gingerly ahead of the budget.

Indeed, all Forex roads lead to the Fed Chair nomination and US tax reform. But on the domestic from all eyes are on Budget day where its expected Prime Minister Najib Razak will walk the fine line between reducing the fiscal deficit while providing enough tax incentives in what is being perceived as an election budget.

However, what happens on the deficit front will likely shape the Ringgit’s medium-term outlook as the balanced budget would greatly appeal to foreign investors.