Sample Category Title

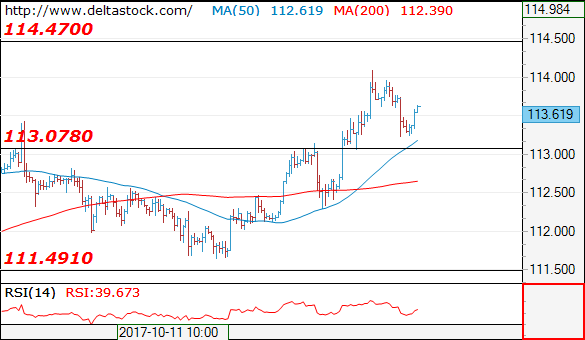

USDJPY Analysis: Retreats As Expected

After reaching the high level above the 114.00 mark on Monday in the aftermath of the Japanese election the USD/JPY currency pair retreated back down to the support zone near the 113.20 mark. At that level the rate rebounded and offered a chance to adjust the drawing of the medium scale ascending channel pattern.

In general the rate faced no resistance levels up to the mentioned 114.00 mark, as it was being driven higher by the support of the 55-hour SMA. Moreover, the SMA was supported by the ascending lower trend line of the dominant medium scale channel up pattern.

Due to that reason it is assumed that the 114.00 mark will be reached once more.

Gold Analysis: Rebound Results In Jump

On Tuesday morning initially it looked like the yellow metal has broken the dominant ascending channel. However, the situation is quite different. After examining the chart more one can discover that the ascending channel needs to be adjusted. Meanwhile, the bullish long term outlook still persists.

In regards to the short term outlook, the bullion's price had approached the support of the proven 61.80% Fibonacci retracement level at the 1,279.05 level, where it seemed to have made a rebound.

Although, the metal still faced the 55 and 100-hour SMAs, which needed to be passed until the price surges back higher.

USD/CAD: Canadian Wholesale Sales

The USD/CAD exchange rate was little changed on the Canadian wholesale sales report, failing to spoil Friday gains. The Greenback lost 0.03% against the Canadian Dollar to remain in the 1.2640 area.

Statistics Canada revealed that the country's wholesale sales grew at a weaker-than-expected pace of 0.5% in August, following an upwardly revised 1.7% gain in the prior month. The main contributors were higher sales of household and private goods, as well as in the motor vehicle subsector. Though, the weak reading provided further signs that the Canadian economy entered the stage of slowdown. In this regard, the Bank of Canada is widely expected to kept interest rates unchanged on its Wednesday meeting, which could cause some volatility in the pair.

Technical Outlook: AUDUSD – Bears Extend To New Two-Week Low, Eye Key Support At 0.7732

The Aussie dollar accelerated further down on Tuesday and broke below pivotal support at 0.7795 (Fibo 61.8% of 0.7732/0.7897 upleg).

Last Friday’s long red daily candle continues to weigh strongly for bearish extension towards 0.7732 (06 Oct low), to mark full retracement of 0.7732/0.7897 upleg.

Bearish daily techs are supportive, with formation of 20/100SMA bear-cross, additionally weighing on near-term action.

Close below 0.7795 will be bearish signal for further easing through 0.7771 (Fibo 76.4%) towards 0.7732 target.

Meanwhile, bears may take a breather ahead of 0.7732 as strongly oversold slow stochastic warns of correction.

Initial resistance lies at 0.7824 (20/100 bear-cross / session high) while daily cloud base (0.7848) is expected to cap extended upticks.

Res: 0.7824, 0.7848, 0.7883, 0.7897

Sup: 0.7771, 0.7732, 0.7712, 0.7670

Technical Outlook: USDJPY – Hourly Cloud Top Is Key For Fresh Probe Above 114.00

The pair is in recovery mode in early Tuesday's trading after Monday's post-election rally failed to clearly break above 114.00 barrier at first attempt and pulled back to113.24.

Today's recovery is attacking key near-term barrier at 113.72 (top of thickening hourly cloud), break of which is needed for fresh bullish signal for renewed probe through 114.00 barrier and attack at key resistances at 114.33 (Fibo 61.8% of 118.66/107.31 descend) and 114.36/49 (11 May / 11 July former tops).

Bullish daily studies are supportive for further advance but bulls may hesitate again as slow stochastic is entering overbought territory.

Prolonged consolidation could be expected while the price holds within hourly cloud (spanned between 113.19 and 113.72).

Stronger bearish signal could be expected on sustained break below hourly cloud, which would trigger deeper pullback towards 112.70 (converged 10/20 SMA's).

Res: 113.72, 114.09, 114.33, 114.50

Sup: 113.60, 113.48, 113.19, 112.70

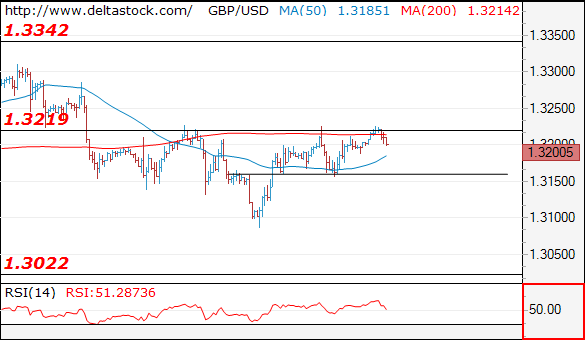

Technical Outlook: GBPUSD – Downside Remains Vulnerable After Triple Upside Failure

Repeated failure to clearly break into daily cloud limited by 10SMA/Tenkan-sen and left triple-top at 1.3228, keeping the downside at risk.

Mixed setup of daily studies (indicators are in negative territory/slow stochastic continues to head north) sees no clear n/t direction while the price is holding between 1.3151 (55SMA) and 1.3214 (10SMA).

Also, daily cloud is thickening and weighs.

UK GDP data on Wednesday are in focus for stronger direction signal. First downside trigger lies at 1.3181 (session low), followed by 55SMA (1.3151) and sustained break here would generate fresh bearish signal for extension towards last Friday's low at 1.3087 and 100SMA at 1.3051.

Conversely lift above triggers at 1.3214/28 (10SMA/upside rejections) would spark fresh upside for probes above 1.3257 pivot (daily cloud top), break of which will be bullish.

Res: 1.3214, 1.3228, 1.3257, 1.3286

Sup: 1.3181, 1.3151, 1.3087, 1.3051

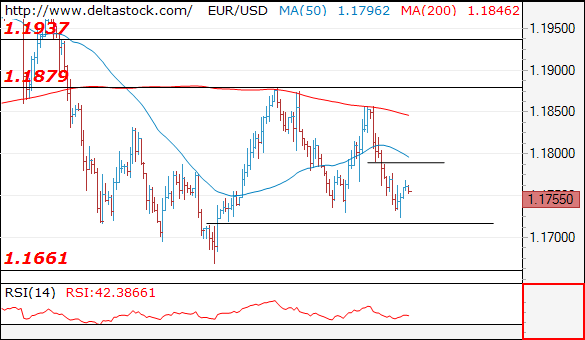

Technical Outlook: EURUSD Looks For Break Below Daily Cloud Base, 20SMA Caps

The Euro moved higher on Tuesday after bears stalled ahead of daily cloud base on Monday, but overall picture remains bearish.

Today's bounce is seen as consolidation ahead fresh attack at cloud base, as barriers at 1.1777 (20SMA) and 1.1802 (Tenkan-sen) weigh on near-term action and expected to cap recovery attempts.

Sustained break below daily cloud base (1.1731) would expose next pivotal points at 1.1671/69 (neckline of daily H&S pattern and 16 Oct low), break of which would generate stronger bearish signal. Bearish daily studies support the notion.

PMI data from Germany / EU are in focus today with forecasts being slightly below previous releases, which could further soften the tone on release at/below forecasts.

Traders are eyeing Thursday's ECB meeting for further signals

Res: 1.1777, 1.1802, 1.1839, 1.1851

Sup: 1.1731, 1.1725, 1.1669, 1.1612

Daily Wave Analysis: US Dollar Builds Corrective Patterns And Offers Breakout Setups

Currency pair EUR/USD

The EUR/USD is testing the support zone at 1.17 again. A break below this zone (blue) will probably indicate a larger correction within wave 4 (light purple). A break above resistance would confirm a bullish breakout within wave C of wave X (pink).

The EUR/USD could be building a wave 1-2 (green) if price stays above the 100% Fibonacci level of wave 2 vs 1.

Currency pair GBP/USD

The GBP/USD needs to break above resistance (red) before a larger wave C (orange) can take place. A break below support (blue) indicates a potential bearish breakout.

The GBP/USD could be in a wave 1-2 (brown) if price stays above the 100% Fibonacci level.

Currency pair USD/JPY

The USD/JPY bullish momentum could take it higher towards 114.50-115.

The USD/JPY retraced within a wave 4 (green) towards the 50% Fibonacci level which provided support. A break above resistance (red) could confirm the wave 5 (green) breakout.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1755

Yesterday's low at 1.1723 signals a reversal of the slide from 1.1860, so my outlook is bullish, for a break through 1.1790, towards 1.1880 area. Initial support lies at 1.1720.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1790 | 1.1940 | 1.1715 | 1.1660 |

| 1.1880 | 1.2030 | 1.1660 | 1.1480 |

USD/JPY

Current level - 113.61

The minor reversal at 114.10 shall seek support at 113.05 static level and the latter should provide a reliable base for another upswing towards 114.50 hurdle.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 114.50 | 114.50 | 113.10 | 111.00 |

| 115.50 | 115.50 | 112.30 | 107.30 |

GBP/USD

Current level - 1.3200

My outlook here is bullish, for a break through 1.3220, towards 1.3340 area. Intraday allow a brief slide to 1.3160, before breaking through 1.3220.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3220 | 1.3340 | 1.3160 | 1.2910 |

| 1.3340 | 1.3650 | 1.3020 | 1.2760 |

China: Xi Gets Name In Constitution – Wang Qishan Steps Down

The Chinese leader Xi Jinping has had his name added to the Party Constitution with his ‘Xi Jinping Thoughts on Socialism with Chinese Characteristics in a new Era'.

It puts Xi alongside Mao and Deng Xiaoping whereas China's two previous leaders Hu Jintao and Jiang Zemin did not get their names in the Constitution. It underlines that Xi is the strongest Chinese President since Deng Xiaopeng and some believe since Mao.

The list of the new Central Committee of 205 members is also released and reveals that Wang Qishan is stepping down as he is not on the list. Wang Qishan has been the leader of the corruption campaign and generally believed to be the no. 2 in the Party after Xi Jinping. Wang Qishan is 69 and thus due to retire according to the informal rule of ‘7 up, 8 down' that says a member of the Standing Committee must retire if he is above 67. However, it had been speculated that Xi Jinping would keep him on and thus break the informal rule. However, it turns out Xi Jinping has decided to respect the line of the Party – a positive sign that despite being more powerful, he still respects the Party line.

The Central Committee will now have its first plenum and vote on the members of the Standing Committee. The members will be presented tomorrow. The SCMP revealed a list of likely members of the new Committee on Sunday. It suggests that it will continue to consist of seven members and that there will be representatives from different factions of the Party. This would be another sign that Xi Jinping is striking a balance in exercising his power. With his name in the constitution, it is clear he is a strong leader. At the same time, he would signal openness for cooperation across the factions of the Party by not just putting his ‘own people' in the Standing Committee. It is of course still not official who the members are and we will need to see this confirmed tomorrow. Below is the list named in the article.

What will be in focus tomorrow is also if a successor for Xi Jinping is designated when he is supposed to step down in 2022. If the list from the South China Morning Post holds true, none of the members will be young enough to be a successor and thus be able to serve one five-year term in the Standing Committee and then two five-year terms as President if the informal rule of ‘7 up, 8 down' is respected. This would require an age of 57 or younger when entering the Standing Committee. However, it is only an informal rule, so it is possible to deviate without the need for changes of any formal rules. If confirmed, however, it may increase speculation that Xi Jinping will aim to stay on after his second term expires in 2022. The two possible members young enough to be successors and that have been in the run-up are Chen Min'er (54) and Hu Chunhua (57). However, if the latest list of members is true, neither of them will make it to the Standing Committee.