Sample Category Title

Trade Idea Update: USD/CHF – Buy at 0.9775

USD/CHF - 0.9827

Original strategy :

Buy at 0.9775, Target: 0.9875, Stop: 0.9740

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9775, Target: 0.9875, Stop: 0.9740

Position : -

Target : -

Stop : -

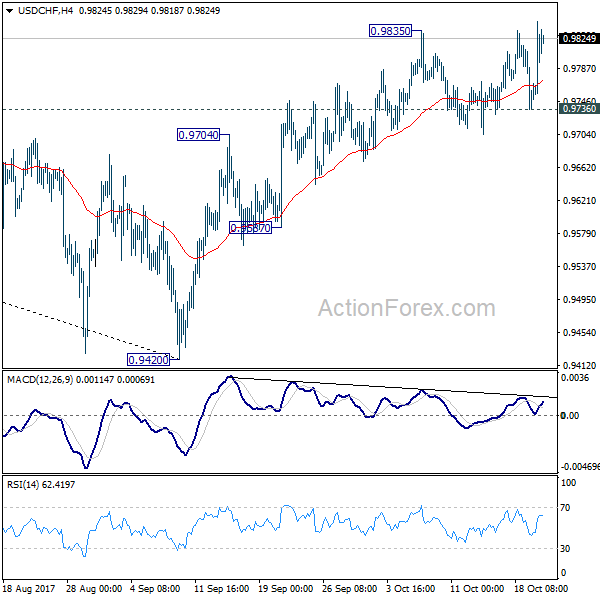

As the greenback found renewed buying interest at 0.9737 and has rallied again, price broke above recent high at 0.9837, signaling early upmove has resumed and although price has retreated from 0.9848, reckon downside would be limited to 0.9770-75 and bring another rise later, above said resistance at 0.9848 would confirms resumption of upmove from 0.9421 low for headway to 0.9870 and possibly towards 0.9900.

In view of this, we are looking to buy dollar again on pullback as 0.9770-75 should limit downside and bring another rise later. Only below support at 0.9730-37 would abort and signal top is formed instead, bring another corrective decline to previous support at 0.9705.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9725; (P) 0.9770; (R1) 0.9803; More....

Intraday bias in USD/CHF remains cautiously on the upside. Rise from 0.9420 is resuming and should target 61.8% retracement of 1.0342 to 0.9420 at 0.9990 next. As medium term fall form 1.0342 is possibly finished, sustained break of 0.9990 will pave the way to retest 1.0342 high. However, break of 0.9736 support will mixed up the near term outlook and turn bias back to the downside for 0.9587 support instead.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could develop into a medium term move and target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9587 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

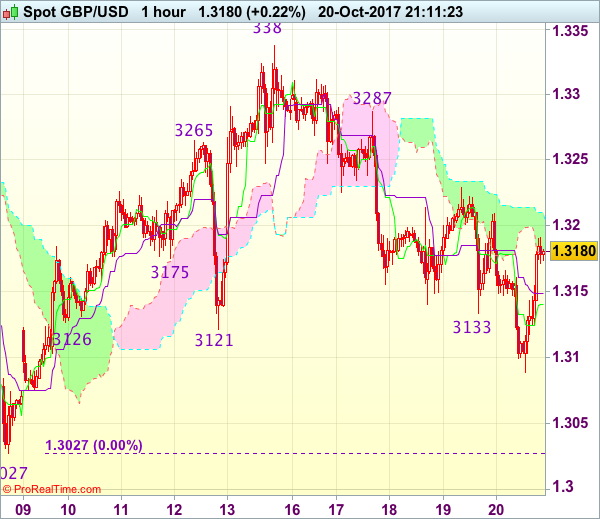

Trade Idea Update: GBP/USD – Sell at 1.3220

GBP/USD - 1.3171

Original strategy :

Sell at 1.3220, Target: 1.3100, Stop: 1.3255

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3220, Target: 1.3100, Stop: 1.3255

Position : -

Target : -

Stop : -

Although cable fell again to 1.3088, lack of follow through selling on break of previous support at 1.3121 suggests consolidation would be seen and another bounce to 1.3175-80 cannot be ruled out, however, reckon resistance at 1.3229 would limit upside and bring another decline later, below said support at 1.3088 would extend the fall from 1.3338 to 1.3050 but recent low at 1.3027 should remain intact due to oversold condition.

In view of this, wee are looking to sell cable on subsequent recovery as resistance at 1.3229 should limit upside and bring another decline later. Above 1.3250-55 would defer and risk test of indicated resistance at 1.3287 but only a firm break above this level would abort and signal low is formed instead, bring rebound to 1.3300 and possibly test of resistance at 1.3312.

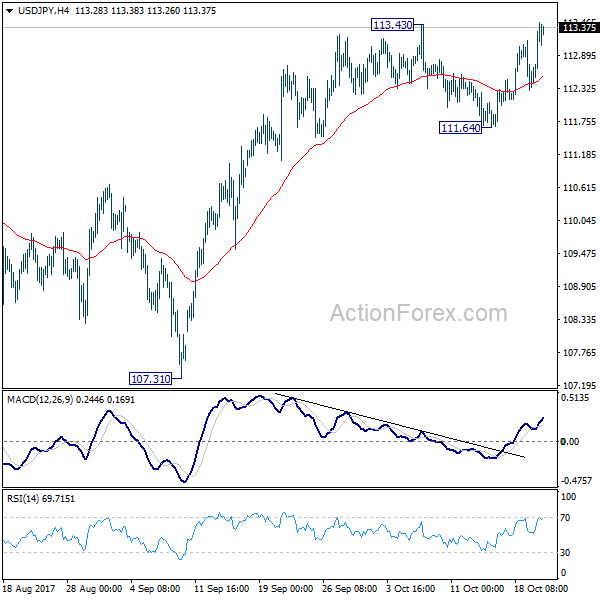

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.17; (P) 112.66; (R1) 113.02; More...

Focus in USD/JPY remains on 113.43 resistance. Firm break there will resume the rise from 107.31 and target 114.49 resistance. More importantly current development revives the case that correction from 118.65 has completed at 107.31. Decisive break of 114.49 will pave the way to retest 118.65 high. However, break of 111.64 will mixed up the outlook again and turn bias back to the downside for deeper fall.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

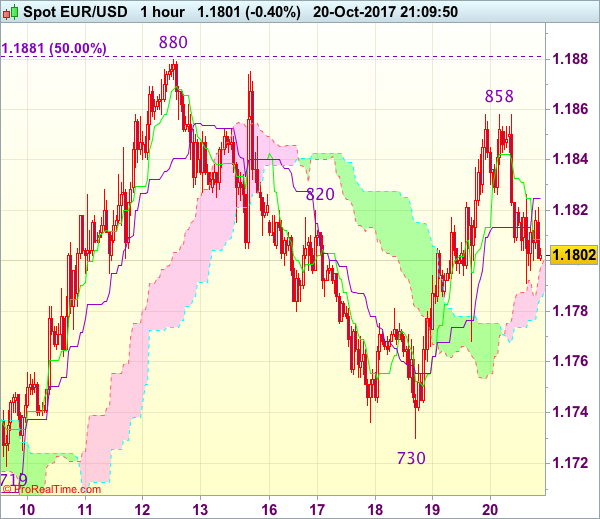

Trade Idea Update: EUR/USD – Stand aside

EUR/USD - 1.1799

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The single currency continued meeting resistance at 1.1858 (like several times) and has retreated today, suggesting consolidation below this level would be seen and pullback to 1.1785-90 cannot be ruled out, however, break of support at 1.1768 is needed to signal the rebound from 1.1730 has ended at 1.1858, bring another fall towards this level later. A drop below this support would prolong consolidation below 1.1880, bring weakness to 1.1700 first.

On the upside, above said resistance at 1.1858 would suggest the correction from 1.1880 has ended, bring retest of this level, break there would signal another leg of erratic upmove from 1.1669 low is underway for gain to 1.1900-10, then towards 1.1940-50 later. As near term outlook is mixed, would be prudent to stand aside for now.

Higher Gasoline Prices Push Up Canadian Inflation in September

Consumer price inflation rose to 1.6% year-on-year in September (from 1.4% in August), a hair under the consensus expectation for 1.7%. Month-on-month seasonally-adjusted prices rose 0.2%.

Gasoline prices were the main factor driving up the headline index. Gas prices have risen substantially over the past two months as a result of disruptions related to Hurricane Harvey and are up 14.1% year-on-year.

Food prices rose modestly month-on-month in September (+0.07%), but accelerated to 1.4% year-on-year, as past declines fell out of the 12-month average.

Core prices were little moved on the month. CPI-median ticked up to 1.5% (y/y) from 1.4% previously, but both CPI-trim and CPI-common were unchanged at 1.8% and 1.5% respectively.

Key Implications

Outside of energy prices, inflation made little progress in September. Moreover, the recent appreciation in the Canadian dollar, which was up 6.7% year-on-year in September, appears to be weighing on goods prices with higher import content. Core goods prices decelerated to -0.3% (y/y) in the month, with clothing and footwear prices leading the way (down 2.3% y/y).

Risks around future Bank of Canada rate hikes are becoming skewed to the downside. Recent B-20 guidelines from OSFI are likely to add to the string of regulatory changes impacting the housing market, and are likely to slow the pace of housing activity and home prices. This will present a headwind to economic growth over the next year, helping to slow growth from its breakneck pace over the past year.

With inflation still showing some signs of softness, there is little need for urgency on the monetary policy front. Governor Poloz has noted that the central bank is in "intense data dependent mode." With that, we look forward to the Bank of Canada's updated assessment of economic developments in its upcoming policy announcement and Monetary Policy Report to be released on Wednesday of next week.

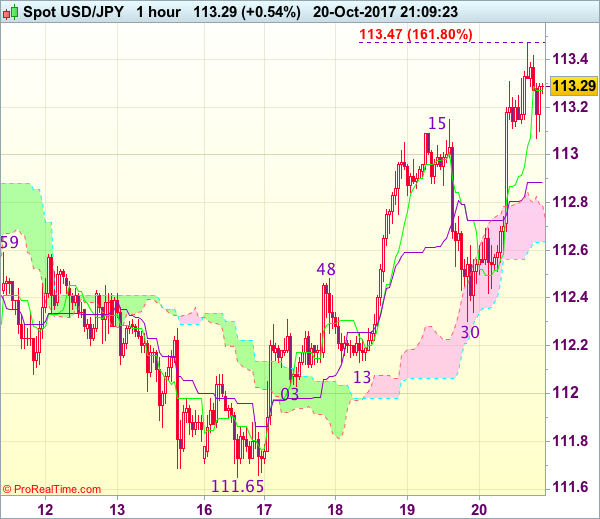

Trade Idea Update: USD/JPY – Buy at 112.80

USD/JPY - 113.30

Original strategy :

Buy at 112.80, Target: 113.80, Stop: 112.45

Position : -

Target : -

Stop : -

New strategy :

Buy at 112.80, Target: 113.80, Stop: 112.45

Position : -

Target : -

Stop : -

Although the greenback retreated to as low as 112.30 yesterday, dollar found renewed buying interest there and has rallied again, suggesting the rise from 111.65 is still in progress, hence bullishness remains for this move to extend further gain to 113.44 resistance, break of this recent high would provide confirmation and encourage for headway to 113.75-80 but reckon 114.00-10 would hold from here due to oversold condition.

In view of this, we are looking to buy dollar again on pullback as 112.81 (current level of the Kijun-Sen and upper Kumo) should limit downside. Below the lower Kumo (now at 112.56) would defer and risk test of said support at 112.30 but break there is needed to signal top is formed instead, bring test of indicated strong support area at 112.03-13.

Canada: Retail Sales Pull Back a Tick in August

Canadian retail sales fell slightly in August, down 0.3% month-on-month. With the effect of prices removed, the performance was softer, as volumes fell 0.7%.

Despite solid sales growth among motor vehicle and parts dealers (+0.7%), a 2.5% drop in sales at food and beverage stores more than offset the gain. Across the remaining categories, Statistics Canada noted weakness at stores traditionally associated with housing: furniture and home furnishings (-2.4%), electronics/appliances (-0.2%), and building material and garden equipment stores (-1.9%).

Sales fell across most provinces, with the largest decline by value recorded in Quebec (-1.2%). However, Ontario recorded a modest gain (+0.3%), as did P.E.I., Nova Scotia, and New Brunswick.

Key Implications

Two months is hardly a trend, but after six straight months of growing retail sales volumes, Canadians appear to be taking a summer breather as volumes fell for a second month in August. As to whether this marks the beginning of a trend, that is likely to hinge on the evolution of housing markets - absent the pullback in housing-associated sales categories, sales would have been roughly flat on the month. After a summer adjustment period, Canadian housing markets have recovered somewhat, suggesting that the Canadian consumer may not be done just yet.

For the Bank of Canada, the link to housing in today's data may result in a slight discounting, both for the reasons discussed above, and that the data pre-dates their September interest rate increase - indeed, there is still only limited data with which they can assess the full impact of the two hikes already implemented this year.

This Wednesday's interest rate decision and Monetary Policy Report will be closely watched given recent economic developments. With the Bank of Canada in 'intense data dependent mode', the interpretation of recent softness in the data, as well as the impact of this week's 'B-20' guidelines for mortgage underwriting will be crucial in assessing the likely path forward for interest rates.

Canadian Dollar Plummets on Poor Retail Sales

Canadian retail sales unexpectedly fell in August due to the biggest month-over-month drop in purchases of food and beverages in three-years.

Headline retail sales fell -0.3%. Market expectations were looking for a strong +0.5% gain. On a year-over-year basis, retail sales rose +6.9%.

Ex-autos, retail fell by a steep -0.7%.

The 'loonie' has taken it on the chin, as the 'big' dollar rallied immediately from just below the C$1.25 handle to touch C$1.2573, the first real resistance point for the dollar.

Stronger headline numbers would have improved the odds of the Bank of Canada (BoC) raising rates before the end of 2017. Today's print should take the BoC out of the rate hike equation for the time being. The BoC meet next Wednesday, Oct 25.

Canada inflation

Canada's annual inflation rate accelerated higher in September for a third consecutive month, supported by a surge in gas prices due to the impact of Hurricane Harvey stateside.

The headline CPI rose +1.6% y/y, following a +1.4% advance in the previous month. Market expectations were looking for a +1.7% advance. On a month-over-month basis, CPI rose +0.2%.

Note: Core inflation, edged upward to +1.6%, or an eight-month high.

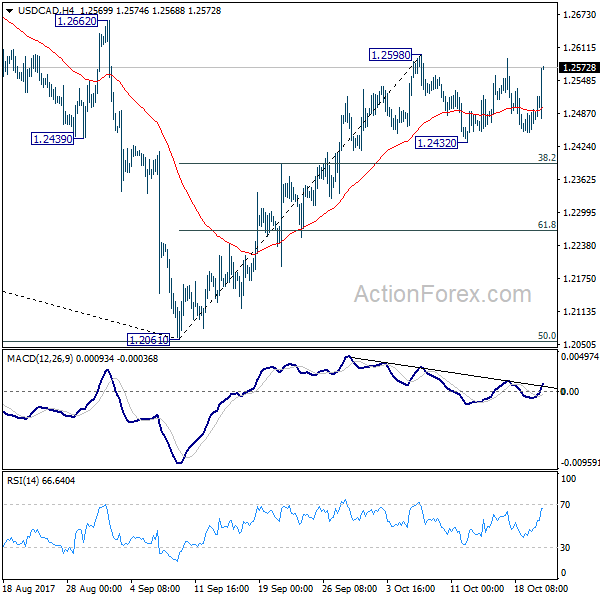

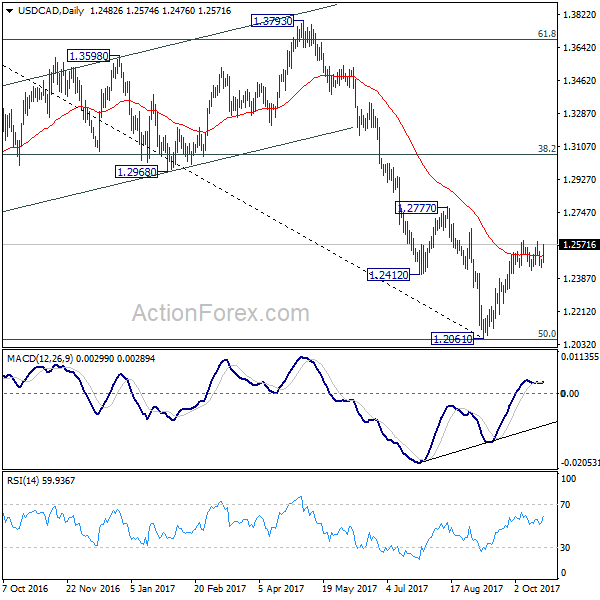

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2458; (P) 1.2476; (R1) 1.2502; More....

USD/CAD rebound strongly in early US session. But it's still bounded in range below 1.2598. Intraday bias remains neutral first. On the upside, break of 1.2598 will extend the rebound from 1.2061 to 1.2777 resistance next. In case of another fall, downside should be contained by 38.2% retracement of 1.2061 to 1.2598 at 1.2393 to bring rally resumption.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. And in that case, USD/CAD should target 1.3793 resistance next. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.