Sample Category Title

Trade Idea Wrap-up: USD/JPY – Buy at 112.80

USD/JPY - 113.39

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.30

Kijun-Sen level : 112.93

Ichimoku cloud top : 112.73

Ichimoku cloud bottom : 112.64

Original strategy :

Buy at 112.80, Target: 113.80, Stop: 112.45

Position : -

Target : -

Stop : -

New strategy :

Buy at 112.80, Target: 113.80, Stop: 112.45

Position : -

Target : -

Stop : -

Although the greenback retreated to as low as 112.30 yesterday, dollar found renewed buying interest there and has rallied again, suggesting the rise from 111.65 is still in progress, hence bullishness remains for this move to extend further gain to 113.44 resistance, break of this recent high would provide confirmation and encourage for headway to 113.75-80 but reckon 114.00-10 would hold from here due to oversold condition.

In view of this, we are looking to buy dollar again on pullback as the Kijun-Sen (now at 112.93) should limit downside. Below the lower Kumo (now at 112.64) would defer and risk test of said support at 112.30 but break there is needed to signal top is formed instead, bring test of indicated strong support area at 112.03-13.

Dollar Hardly Profits from Senate Budget Vote

- European equities maintain only marginal gains as the US budget vote failed to trigger a protracted risk-on rally. US equities open with modest gains between 0.2% and 0.4%, the Nasdaq outperforming.

- UK prime minister Theresa May has left a two-day EU summit in Brussels facing demands that she must make a "firm and concrete commitment" to increase Britain's Brexit "divorce" payment before talks can move on to a future trade deal.

- The eurozone current account surplus with the rest of the world rose in August to its highest level since May last year (€33.3 bn). The increase was driven by a jump in the surplus for services from €2.6bn in July to €7.2bn in August, and a smaller deficit in secondary income, which fell to €12.4bn from €14.8bn the previous month.

- US President Trump signalled optimism for the passage of Republicans' sweeping tax cut plan, saying a key senator who rejected the party's budget blueprint a day earlier would back the proposed tax measure when it comes up for a vote.

- The Spanish government has secured opposition support to dissolve Catalonia's parliament and hold new elections there in January in an effort to defuse the regional government's push for independence.

- Jacob Zuma sacked the head of the Communist party from his cabinet in a reshuffle critics said was carried out to purge dissenters and consolidate his power weeks before the ruling African National Congress votes on his replacement.

- Canadian eco data disappointed. Inflation accelerated less than anticipated (1.6% Y/Y from 1.4% Y/Y) in September and August retail sales unexpectedly declined by 0.3% M/M. The loonie lost ground with USD/CAD rising above 1.2550 ahead of next week's BoC meeting.

Rates

US Senate revives reflationary spirits

Global core bonds lost ground today. The main move occurred overnight for the US Note future and in the European opening for the Bund. The US Senate adopted a fiscal budget for next year which is critical for implementing tax reforms. Reflationary spirits took control of trading and pushed yields higher. The sell-off slowed throughout the day, but core bonds held a slight downward bias. The eco/event calendar didn't impact trading. We expect volumes to decline from now on with investors eying next Thursday's ECB policy meeting. Draghi is expected to deliver clarity on the future of the central bank's asset purchase programme. Consensus has been building around a 9-month APP extension while lowering monthly purchases from the start of 2018 from €60 bn to €30 bn. We agree with the reduction in purchases, but think that underlying growth evelopments argue for a shorter, 6-month extension.

At the time of writing, US yields increase by 3.8 bps (2-yr) to 5.4 bps (5-yr). The German yield curve bear steepens with yields 1.3 bps (2-yr) to 5.9 bps (30-yr) higher. On intra-EMU bond markets, 10-yr yield spread changes versus Germany are nearly unchanged with the periphery outperforming (-3 bps to -5 bps).

Currencies

Dollar hardly profits from Senate budget vote

Overnight, the dollar profited form a budget vote in the US Senate that might also pave the way for a US tax reform. However, the USD rally slowed soon. There were no follow-through gains in Europe or in the US. The US currency didn't receive additional interest rate support. EUR/USD trades in the 1.18 area. USD/JYY is changing hands at around 113.25.

Overnight, the US Senate adopted a blueprint for the 2018 budget. The approval might also be a started point for US Republicans and the government to proceed with substantial tax reform. USD yields and the dollar rebounded after yesterday's decline. USD/JPY jumped north of 113. EUR/USD returned to the 1.18 area. The Kiwi dollar declined further below 0.70 after the formation of a government with Labour and the New Zealand first party.

European equity markets opened with modest gains supported by a rise in US futures after the overnight US budget vote. However, the hope on a US tax reform wasn't able to trigger sustained further USD gains. After some initial swings overnight, US/EMU interest rate differentials didn't widen as Bunds basically followed the price pattern of US Treasuries. In a broader perspective, global markets remained quite uncertain on what to expect from US tax reforms even after the overnight steps. European equities (and US equity futures) showed modest gains, but there was no euphoria. EUR/USD failed to sustain below 1.18 and settled in a tight range just north of the big figure. USD/JPY filled offers in the 113.45 area, but also ceded slightly ground as the session proceeded.

There were no important eco data in the US. Existing home sales will be published after finishing this report. The dollar still struggles to make further gains. EUR/USD trades around 1.18. USD/JPY is changing hands in the 113.25 area. Fed's Yellen gives a speech on monetary policy since the financial crisis after the close of the US markets this evening. Japanese parliamentary elections developments in Spain deserve attention this weekend.

Sterling rebounds as Brexit tensions ease (slightly)

Sterling remained in the defensive in Asia this morning, extending yesterday's decline as poor UK retail sales data questioned the room for the BoE to raise rates in the near future. However, sentiment on the UK currency improved from the start of trading in Europe. European investors apparently draw some comfort from reconciliatory remarks of German Chancellor Merkel after yesterday's EU summit. She saw no indications that the talks won't succeed. Later in the session, monthly UK public finance data were also better than expected. EUR/GBP drifted back below the 0.90 barrier. The pair trades currently in the 0.8960 area. Cable also rebound despite an, albeit cautious, overall USD rebound. GBP/USD trades in the 1.3180 area. Even so, sterling still trades modestly lower against the euro and the dollar as investors grow convinced that there is only room for one BoE rate hike in the coming months, at best.

Canadian Inflation Showed Little Direction in September

Highlights:

- The year-over-year increase in all items CPI rose to 1.6% in September from 1.4% in August.

- Much of the increase in headline inflation reflected higher energy prices as hurricane-related refinery shutdowns in the US put upward pressure on gasoline prices.

- Rising food prices were also a factor with that component continuing to rebound from multi-decade lows earlier this year.

- Year-over-year inflation excluding food and energy fell to 1.2%, its lowest reading since 2014, as clothing and footwear price deflation intensified.

- Just one of the Bank of Canada's three preferred core measures rose in September, with the average unchanged at 1.6% after rounding.

Our Take:

Today's inflation report was a mixed bag, with an energy-driven increase in the headline reading, little change in the Bank of Canada's core measures and a decline in ex food and energy inflation. Overall, there wasn't as much evidence this month that the economy's strong growth trend and limited economic slack are pushing inflation up toward the central bank's 2% target. Given their "particularly data dependent" stance, we think this gives the bank cover to be a bit more patient in removing accommodation following consecutive rate hikes in July and September. We don't see the bank raising their benchmark interest rate again next Wednesday.

With no move expected, our eye will be on the Bank of Canada's updated economic projections—particularly whether they see any remaining economic slack and if they think the economy's 'speed limit' has picked up amid stronger productivity growth. Any indication that the economy has more room to run without generating inflationary pressure will likely be seen as a dovish development. But on balance, we think the combination of an economy near capacity and still-accommodative monetary policy calls for further, gradual rate increases. We expect the next hike will come in December but we'll likely need confirmation that above-trend growth continued into the second half of the year for that to happen.

Canadian Retail Spending Falters in August

Highlights:

- August retail sales unexpectedly dropped 0.3% in the month following an unrevised 0.4% gain in July.

- The decline was led by lower sales at food stores and housing-related retailers such as furniture stores.

- E-commerce sales (not all of which are included in the retail sales totals) were up 41.9% over the past year ending in August though their share of retail trade is just 2.3%.

Our Take:

Retail sales unexpectedly dropped 0.3% in August following a 0.4% gain in July. The decline in the more recent month was relatively broadly based led by a 2.5% plummet in sales at food stores that almost fully reversed cumulative gains over the previous four months. StatsCan commented on the weakness evident in housing-related sales components with building materials down 1.9% and furniture store sales off 2.4%. Eliminating the impact of overall price changes the volume of retail sales dropped a disappointing 0.7% following the 0.1% decline in July. This represents a sharp shift from the average monthly increase through Q2 of 0.5%. Though the earlier strength will still allow the Q3 consumer spending growth rate to increase, the pace seems likely to drop to 1 1/2% from the 4.7% average gain achieved over the first two quarters of this year. With the Canadian economy likely close to capacity, a slowing in spending from the outsized gains over the first half of the year is likely desirable. The weakening in consumer spending is expected to be mirrored in overall GDP growth moderating to a still above-potential rate of 2.0% though this would be down sharply from the Q2 gain of 4.5%.

Today's retail sales report, along with the September inflation numbers also released this morning coming in lower than expected, are consistent with the Bank of Canada likely remaining on the sidelines coming out of next week's policy meeting leaving the overnight rate unchanged at 1.00%. Our forecast assumes that the central bank will eventually return to a modest pace of tightening though such will await signs of inflation moving closer to target and growth being sustained at or slightly above potential.

Trade Idea: EUR/GBP – Stand aside

EUR/GBP - 0.8957

Original strategy :

Sold at 0.8975, stopped at 0.9015

Position : - Short at 0.8975

Target : -

Stop : - 0.9015

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although euro’s rebound from 0.8856 turned out to be stronger than expected, as the single currency has retreated after faltering below resistance at 0.9033, suggesting further choppy trading would be seen and pullback to 0.8930-35, then 0.8900 cannot be ruled out, however, price should stay well above said support at 0.8856 and bring further consolidation.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Above 0.9000 would bring another test of resistance at 0.9033 but break there is needed to the rebound from 0.8856 is still in progress for further gain to 0.9060 and later towards 0.9090-00.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

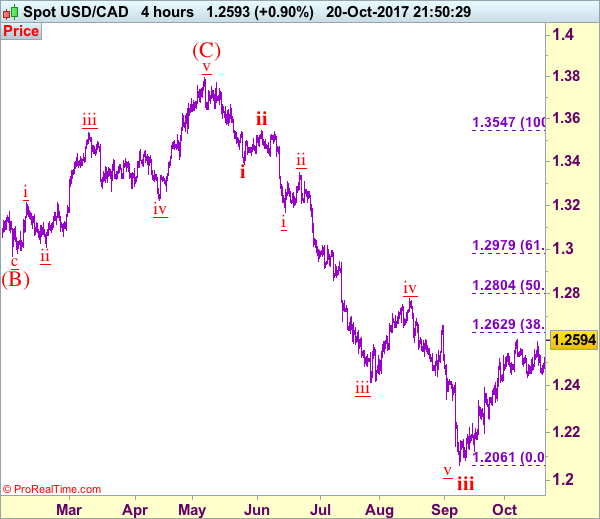

Trade Idea: USD/CAD – Stand aside

USD/CAD - 1.2591

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Current rebound suggests a retest of recent high at 1.2599 would be seen, however, break there is needed to confirm recent upmove from 1.2061 low (wave iii trough) has resumed for further gain towards previous resistance at 1.2663, then 1.2700 but price should falter well below another previous resistance at 1.2778. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii ended at 1.2414, followed by wave iv correction ended at 1.2778, wave v has reached our indicated downside target at 1.2100 and may extend to 1.2000.

On the downside, whilst pullback to 1.2540-50 cannot be ruled out, reckon 1.2520 (previous minor resistance) would hold and bring another rise later. Only below 1.2475-80 would abort and bring test of 1.2450 but break of support at 1.2433 is needed to signal top has been formed, bring retracement of recent rise to 1.2400, then towards 1.2350-55 but support at 1.2313 should remain intact.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Canadian Dollar Fell Sharply after Downbeat Canadian Data

Inflation in September missed forecast at 0.3% m/m on 0.2% rise while annualized figure came along with expectations at 1.6%.

Canada's retail sales disappointed in August, falling by 0.3% against forecast for 0.5% and 0.4% in the previous month.

Core retail sales fell by 0.7%, strongly undershooting forecast for 0.3% rise and increase by 0.2% in July.

USDCAD spiked to three-day high at 1.2567 and emerged above daily cloud, where the price was stuck in past one week.

Break above cloud top is bullish signal which requires confirmation on close above it for confirmation and could trigger acceleration towards next targets at 1.2590/1.2610.

Firm break here would signal an end of 1.2597/1.2432 congestion and resumption of larger uptrend from 1.2061 (08 Sep low).

Res: 1.2567; 1.2590; 1.2610; 1.2662

Sup: 1.2515; 1.2502; 1.2465; 1.2458

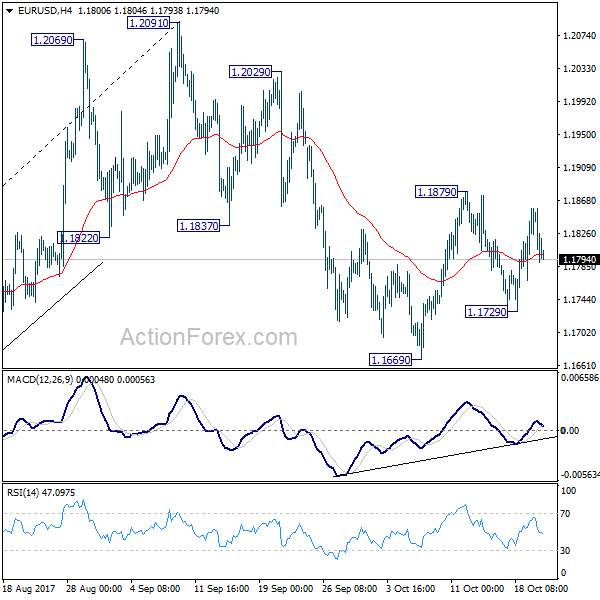

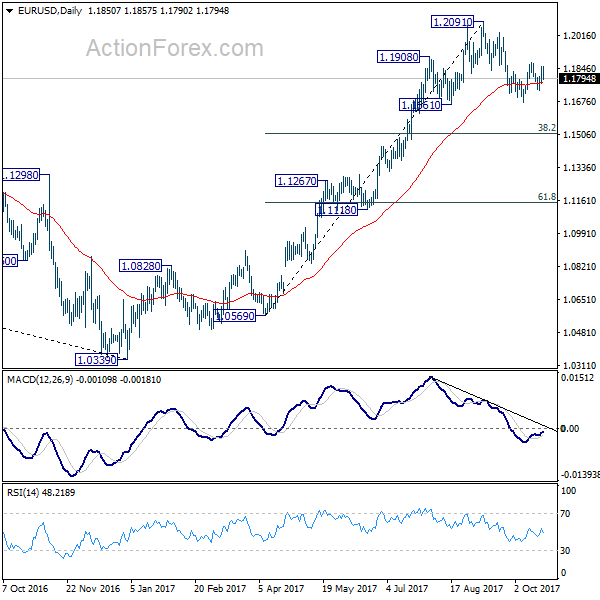

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1792; (P) 1.1825 (R1) 1.1883; More...

Intraday bias in EUR/USD remains neutral at this point. On the upside, break of 1.1879 will revive the case that corrective fall from 1.2091 has completed at 1.1669, ahead of 1.1661 support. EUR/USD should target a test on 1.2091 high then. Meanwhile, break of 1.1729 will bring retest of 1.1669 instead.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

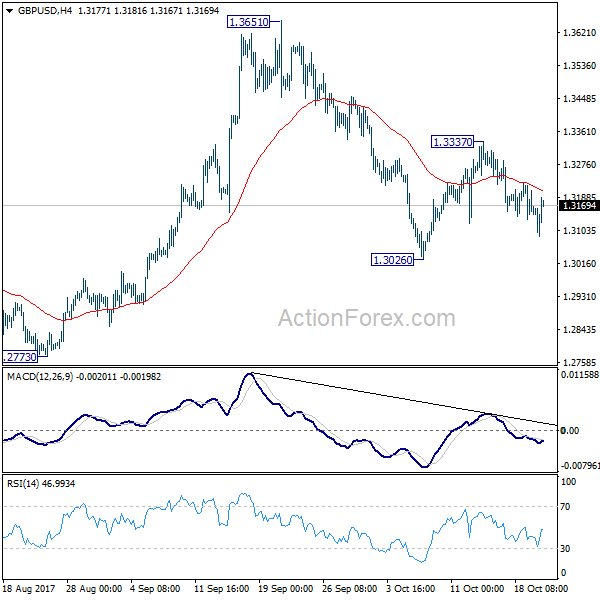

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3109; (P) 1.3169; (R1) 1.3217; More....

GBP/USD recovers again after hitting 1.3087 and intraday bias remains neutral again. On the downside, break of 1.3026 will resume whole decline from 1.3651 and target 1.2773 key support next. That will also revive the case that medium term rise from 1.1946 has completed at 1.3651. Meanwhile, above 1.3337 will bring retest of 1.3651 high instead.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll turn neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

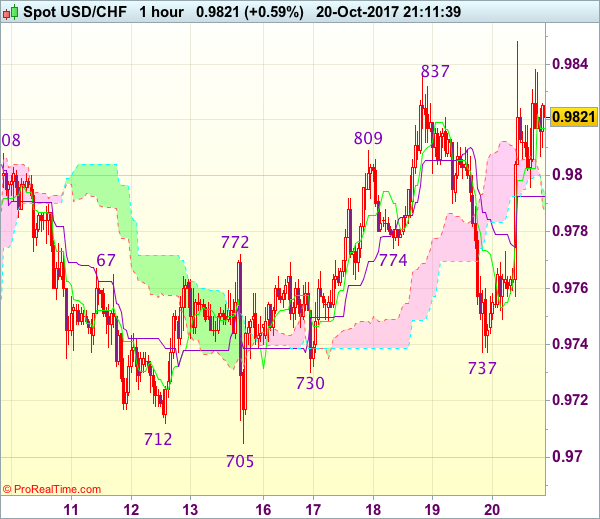

Trade Idea Update: USD/CHF – Buy at 0.9775

USD/CHF - 0.9827

Original strategy :

Buy at 0.9775, Target: 0.9875, Stop: 0.9740

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9775, Target: 0.9875, Stop: 0.9740

Position : -

Target : -

Stop : -

As the greenback found renewed buying interest at 0.9737 and has rallied again, price broke above recent high at 0.9837, signaling early upmove has resumed and although price has retreated from 0.9848, reckon downside would be limited to 0.9770-75 and bring another rise later, above said resistance at 0.9848 would confirms resumption of upmove from 0.9421 low for headway to 0.9870 and possibly towards 0.9900.

In view of this, we are looking to buy dollar again on pullback as 0.9770-75 should limit downside and bring another rise later. Only below support at 0.9730-37 would abort and signal top is formed instead, bring another corrective decline to previous support at 0.9705.