Sample Category Title

Canadian Dollar Lower after a Batch of Disappointing Data, Sterling Rebounds on Positive Brexit News

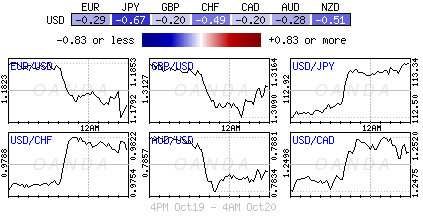

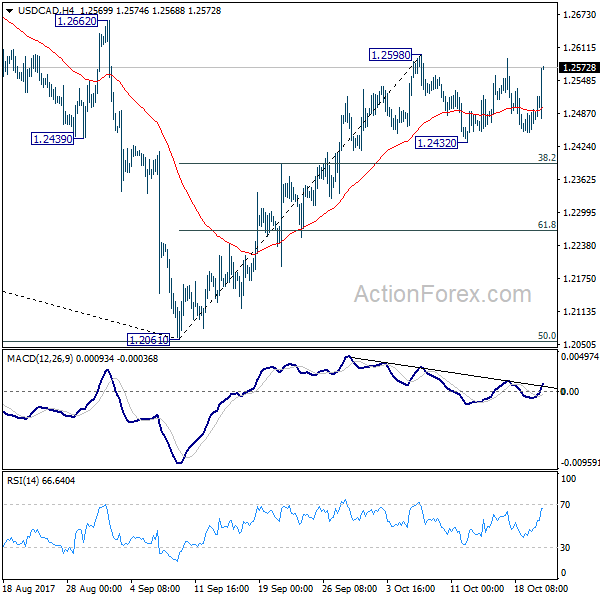

Canadian Dollar weakens notably in early US session after a batch of disappointing data. Headline CPI rose 0.2% mom, 1.6% yoy in September, up from August's 0.1% mom 1.4% yoy. But that's below expectation of 0.4% mom, 1.7% yoy. CPI core-common was unchanged at 1.5% yoy. CPI core - trim edged higher to 1.5% yoy. CPI core median also edged higher to 1.8% yoy. Meanwhile, headline retail sales dropped -0.3% mom in August, way below expectation of 0.4% growth. Ex-auto sales was even worse and dropped -0.7% mom, versus consensus of 0.3% mom. BoC will be meeting next week and there is practically no change for a rate hike from current 1.00%. USD/CAD is staying in range of 1.2432/2598 at the time of writing. Near term outlook remains bearish as rebound from 1.2061 should resume through 1.2598 sooner or later.

Sterling rebound on Brexit progress

Sterling rebounds strongly today on positive news out of Prime Minister Theresa May's appearance in the EU summit. May pledged to examine the Brexit bill line by line and UK could be willing to pay more than EUR 20B. And she doesn't dismiss the number of EUR 60b, which is believed to be what EU is asking for. Meanwhile, European Council President Donald Tusk said that the reports of the "deadlock" between EU and UK "have been exaggerated'. Tusk added that while progress was "not sufficient" to start trade talks, that "doesn't mean there is no progress at all".

Released from UK, public sector net borrowing rose to GBP 5.3B in September.

Euro firm as markets eyes next week's ECB

Euro has been very resilient this week in spite of the political uncertainties in Catalonia. The common currency could end as the second strongest major currency, after dollar. Markets are keenly awaiting next week's ECB monetary policy decision. ECB Governing Council Member Ewald Nowotny said today that the central bank will likely decide to cut down on its monthly asset purchase target next week. He noted that "the question will be whether the programme should be continued at the current intensity or whether hitting the brakes is called for". Though, he noted that "it would be dangerous to abruptly slam on the brake", but ECB "will slowly take its foot of the gas". It's speculated that ECB would cut the EUR 60B a month purchase by half to EUR 30B, or ever by two-thirds to EUR 20B.

Released from Eurozone, current account surplus widened to EUR 33.3B in August. Germany PPI rose 0.3% mom 3.1% yoy in September, above expectation of 0.1% mom 2.9% yoy.

Dollar to end as the strongest one on tax hope

Dollar is set to ended the week as the strongest one, after a wild ride. The greenback was boosted by news that US President Donald Trump and Republicans have moved a big step forward on tax reforms. Republican-dominated Senate narrowly approved a budget blueprint for the next fiscal year, yesterday. Republicans could now pass legislation reform the tax plan without the need for help from Democrats. And more importantly, the voting some how showed unity among Republicans. Even Senator Bob Corker, who's in feud with President Donald Trump, voted the for the budget. Technically, dollar is mildly bullish against Swiss Franc and Yen. But it's sort of neutral against Euro and Sterling.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2458; (P) 1.2476; (R1) 1.2502; More....

USD/CAD rebound strongly in early US session. But it's still bounded in range below 1.2598. Intraday bias remains neutral first. On the upside, break of 1.2598 will extend the rebound from 1.2061 to 1.2777 resistance next. In case of another fall, downside should be contained by 38.2% retracement of 1.2061 to 1.2598 at 1.2393 to bring rally resumption.

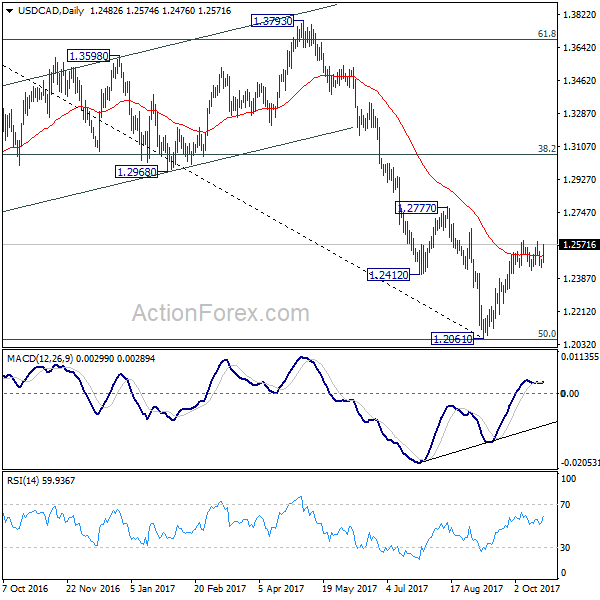

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. And in that case, USD/CAD should target 1.3793 resistance next. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | EUR | German PPI M/M Sep | 0.30% | 0.10% | 0.20% | |

| 06:00 | EUR | German PPI Y/Y Sep | 3.10% | 2.90% | 2.60% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Aug | 33.3B | 26.2B | 25.1B | 31.5B |

| 08:30 | GBP | Public Sector Net Borrowing (GBP) Sep | 5.3B | 5.7B | 5.1B | |

| 12:30 | CAD | CPI M/M Sep | 0.20% | 0.40% | 0.10% | |

| 12:30 | CAD | CPI Y/Y Sep | 1.60% | 1.70% | 1.40% | |

| 12:30 | CAD | CPI Core - Common Y/Y Sep | 1.50% | 1.50% | ||

| 12:30 | CAD | CPI Core - Trim Y/Y Sep | 1.50% | 1.40% | ||

| 12:30 | CAD | CPI Core - Median Y/Y Sep | 1.80% | 1.70% | ||

| 12:30 | CAD | Retail Sales M/M Aug | -0.30% | 0.40% | 0.40% | |

| 12:30 | CAD | Retail Sales Less Autos M/M Aug | -0.70% | 0.30% | 0.20% | |

| 14:00 | USD | Existing Home Sales Sep | 5.32M | 5.35M |

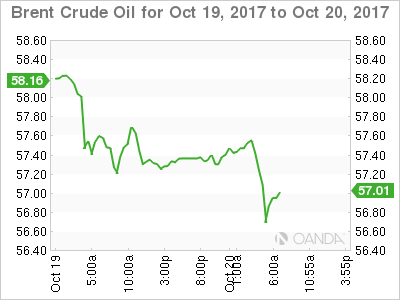

Brent Oil Another False Breakout

The Brent Oil dropped and resumed the yesterday's bearish candle and seems poised to reach fresh new lows in the upcoming days. Technically, it should start a larger drop after another false breakout and after the failure to reach the 59.50 previous high. Right now we still need a confirmation that we'll have another leg down because is still trapped above some important dynamic support levels.

Price drops also because the Cable has lost some ground versus the greenback, remains to see what will happen in the upcoming hours as the Canadian data should bring some action. The figures should shake the USD/CAD and most likely will have an impact on the Brent as well. Personally, I believe that only the fundamental factors could force the rate to turn to the upside again.

Price plunged since yesterday and erases the latest gains, signaling that the bulls are too exhausted and that we have an overbought situation. I've said in the yesterday's daily report that a larger drop will come if the rate will close below the median line (ML) of the major ascending pitchfork and if will retest this level. Brent dropped without a retest, actually has tried to come back above the ML in the morning, but failed to stay there.

It is trading above the 57.00 psychological level because has squeezed a little in the last hours, the next downside target will be at the 250% Fibonacci line (descending dotted line). Price could retest the upper median line (uml) of the minor descending pitchfork before will drop towards the next downside targets.

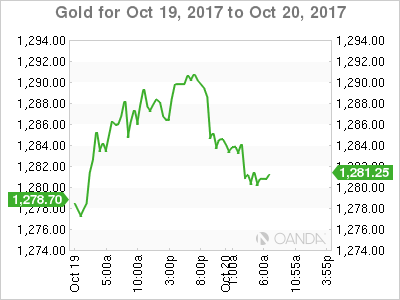

Gold Retested The Broken Support

Price dropped after the retest of the first warning line (WL1) of the major ascending pitchfork. The downside was paused by the strong support area near the 50% Fibonacci retracement. Only a valid brekdown below the 50% level will announce a further drop. A USDX's breakout above the 93.81 static resistance will send it towards the $1248 per ounce.

AUD/USD Losing Momentum

Price dropped today as the USD has taken the lead again on the short term. AUD/USD erased the yesterday's gains, but failed to reach the 38.2% retracement level. I've said in the last reports that technically, is expected to climb towards the upper median line (uml) of the minor blue descending pitchfork. I've drawn a minor red ascending pitchfork hoping that I'll catch an upside movement, price could come to retest the lower median line (lml). A valid breakout from the ascending pitchfork's body will signal a further drop on the daily chart.

Dollar Elevated by Trump Tax Hopes, While Gold Dips

Global equity bulls were missing in action on Thursday, after weaker corporate earnings, soft economic data from China and heightened political drama in Spain encouraged investors to head to the sidelines.

Interestingly, Asian shares concluded higher on Friday amid confidence over the global economy, while European stocks found support in the form of the US Senate passing a budget proposal – a big step for tax reforms. With the renewed sense of optimism over Donald Trump's tax reforms stimulating investor appetite for riskier assets, Wall Street could receive a boost this afternoon.

Dollar rallies on tax reform optimism

The dollar was king today, following reports of the US Senate passing a budget blueprint, which was an important step for Republicans to push ahead with tax reforms.

With the Senate voting 51-49 late on Thursday to the pass the bill, it appears that Trump's hopes of moving forward with the planned $1.5 trillion tax-cut package, are gaining traction.

While Dollar bulls may benefit from the renewed sense of optimism over Trump's tax reforms, some headwinds could come in the form of uncertainty over who the next chair of the Federal Reserve will be. With markets speculating that Trump may appoint Jerome Powell, who is seen as a dove, to become the next Fed head, bears could make an unwelcome appearance. It should be kept in mind that a dovish Fed Chair has the ability to weigh on the prospects of higher US interest rates in 2018, consequently pressuring the dollar.

Sterling punished by a BoE dove

Sterling extended losses against the Dollar on Friday morning, after dovish comments from Bank of England Deputy Governor Jon Cunliffe, prompted investors to reassess the likelihood of a rate hike in November.

After Cunliffe stated on Thursday that there was no clear case for a rate hike in the near future, speculation is now mounting that two of the central bank's nine policy makers will not be voting for a rate hike in November. The fact that Sterling sharply depreciated following Cunliffe's comments, continues to highlight how the currency has become increasingly sensitive to monetary policy speculation.

Theresa May has admitted for the first time that Brexit talks have been in "difficulty", which is likely to punish Sterling further. With political risk at home, weak economic fundamentals and Brexit uncertainty all weighing heavily on Sterling, further downside is on the cards. Even if the Bank of England raises interest rates in November as is widely expected, in an effort to limit inflation, this may not be enough to heal the bruised buying sentiment towards Sterling.

From a technical standpoint, the GBPUSD has broken below the 1.3150 which may encourage a decline towards 1.3050.

Commodity spotlight – Gold

This has certainly been another interesting week for Gold, which has tumbled more than 1.7% after closing above the $1300 level last week. The metal has steadily depreciated in recent days, despite geopolitical tensions and political uncertainty supporting the flight to safety. There is a suspicion that the culprit behind Gold's selloff may be renewed optimism over Donald Trump's tax reforms. With the US Senate voting for new budget measures on Thursday, the possibility that proposed tax reforms will be passed has increased. This will likely boost the dollar, consequently pressuring Gold. From a technical standpoint, the yellow metal remains pressured below the $1300 level. Sustained weakness under $1280 may open a path towards $1267.

Let's not forget about Bitcoin…

Could everybody's favorite cryptocurrency be gearing up for another incredible appreciation, that pushes it above $6000?

With politicians, central banks and leading investment banks all showing a keen interest in Bitcoin, bulls are supported and can make another move at any moment. Taking a look at the technical picture, Bitcoin experienced a sharp decline on Wednesday, with prices almost hitting $5100 before losses were aggressively clawed back. This cryptocurrency continues to display its resilience on repeated occasions, with a solid breakout above the $5850 level paving a path towards $6000.

GBPUSD Backs Off Lower Prices, Eyes Further Recovery

GBPUSD: The With a temporary bottom seen, we may see further recovery higher. Support lies at the 1.3150 level where a break will turn attention to the 1.3100 level. Further down, support lies at the 1.3050 level. Below here will set the stage for more weakness towards the 1.3000 level. Conversely, resistance stands at the 1.3200 levels with a turn above here allowing more strength to build up towards the 1.3250 level. Further out, resistance resides at the 1.3300 level followed by the 1.3350 level. On the whole, GBPUSD continues to face further downside pressure but with caution of a recovery.

USDJPY Buying Likely to Accelerate Above 113.47

The U.S dollar has moved to its highest trading level against the Japanese Yen in over three-months, hitting 113.47 during the European trading session, as the U.S dollar index continues to push higher. The USDJPY pair is currently trading around the 111.38 level, as traders await U.S economic data and the latest opinion polls from this weekend's snap Japanese election.

Intraday buying interest in the USDJPY pair is likely to accelerate above the 113.47 level, with price-action likely to test towards the key 113.57 and 113.90 technical resistance levels.

If sellers push price-action below the key 113.20 level, the USDJPY pair is likely to see a further decline back towards the 112.89 region. Extended intraday technical support is located at 112.58 and 111.89.

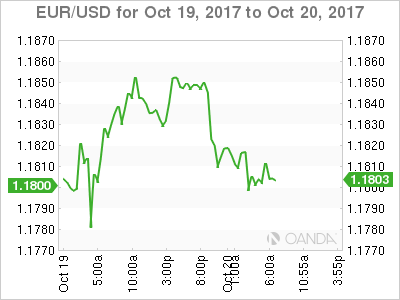

EURUSD Bullish Above 1.1800

The euro currency has pulled back towards the 1.1800 level against the U.S dollar, after earlier trading as high as 1.1857. A move lower in European stocks and a stronger U.S dollar index have contributed to the EURUSD shedding intraday gains. Price-action currently trades around the 1.1809 level, as traders await key housing data from the U.S economy.

The EURUSD pair retains a bullish intraday trading bias while holding price above the key 1.1800 level. Further upside towards 1.1816 and 1.1833 can be expected while the bullish tone continues. Extended resistance is found at 1.1857 and 1.1875.

If intraday EURUSD sellers push price-action below the key 1.1800 level, further declines towards 1.1790 and 1.1770 should be expected. Extended intraday support is found at 1.1755 and 1.1730.

Canadian Dollar Quiet Ahead of Canadian CPI, Retail Sales

The Canadian dollar is almost unchanged in the Friday session, as USD/CAD stays close to the 1.25 line. In European trade, the pair is trading at 1.2488, up 0.03% on the day. On the release front, Canada releases key consumer spending and inflation data. CPI is expected to accelerate to 0.3%. The markets are also expecting an improvement in retail sales reports, with Core Retail Sales and Retail Sales expected at 0.5% and 0.3%, respectively. In the US, Existing Home Sales is expected to slow to 5.30 million, and Federal Reserve Chair Janet Yellen will deliver remarks at an event in Washington.

It's been a quiet week for the Canadian dollar, which hasn't veered far from the 1.25 level. The lack of movement could change in Friday's North American session, as Canada releases CPI and retail sales. If these indicators beat expectations, the Canadian currency could move higher. As well, the odds of the Bank of Canada raising rates before the end of 2107 would likely improve. There was positive news from the manufacturing sector earlier this week, as Manufacturing Sales jumped 1.6% in August, ending a streak of two declines. The excellent reading was the highest gain this year, and points to a manufacturing sector which has benefited from strong demand for Canadian-made motor vehicles. The robust manufacturing sector and increase in oil prices has led to a surge in exports, which are expected to jump 8.0% in 2017. Still, there are some sore spots in the export sector, such as softwood lumber, due to a dispute over tariffs with the US.

There has been plenty of speculation about whether Janet Yellen will be replaced as chair of the Federal Reserve when her term expires in February 2018. Yellen may be interested in serving a second term, but President Trump is looking at other options. Trump has not been complimentary towards Yellen, although it's hard to argue that Yellen has not done an admirable job. Yellen has ended quantitative easing, raised interest rates and started to unwind the Fed's balance sheet. Trump's shortlist includes Jerome Powell, Kevin Warsh and John Taylor. Trump may lean towards Taylor, an economist who is considered more hawkish on policy than Yellen. Under Taylor, interest rates would likely move substantially higher than the current 1.25%, and a rate hike early in 2018 could strengthen the US dollar.

U.S Budget Resolution Provides Dollar Temporary Relief

Friday October 20: five things the markets are talking about

There are three themes that are dominating current position taking.

First, political developments in Spain, second, the decision on the next Fed chair that may influence the course of U.S interest rates and third, Brexit negotiations.

Overnight, the 'mighty' U.S dollar has climbed against all its G10 peers after the U.S Senate adopted a budget resolution, giving some momentum to President Trump's planned tax cuts.

Elsewhere, the EUR is underperforming as investors try to anticipate the next move in Spain's Catalan crisis, while the yen comes under renewed pressure ahead of this weekend's Japanese election.

Note: Japan goes to the polls on Sunday with a win tipped for PM Abe.

Gold and U.S Treasury prices are both under pressure as safe haven trading has lost some of its lustre for now with investors.

1. Stocks get the green light

In Japan, the Nikkei (+0.4%) has posted its longest winning streak since 1961 on a weaker yen and PM Abe hopes. The index rallied for the 14th consecutive session overnight. For the week, it has gained +1.4%, its sixth straight weekly gain and the longest such winning streak in a year. The broader Topix traded flat.

Down-under, Australia's S&P/ASX 200 Index rose +0.2% and South Korea's Kospi index gained +0.7%. In New Zealand, the S&P/NZX 50 Index ended little changed after losing as much as -1.2% in the previous session on the news that Labor party will form a coalition.

In Hong Kong, stock prices rebounded sharply overnight, as investors scrambled for bargains, which was triggered by the People's Bank of China (PBoC) reference to a 'Minsky moment.' the Hang Seng Index rose +1.2%, recovering much of the previous sessions -1.9% decline, and ending the week roughly flat. The Hong Kong China Enterprises Index jumped +1.8%, up +0.3% for the week.

Note: 'Minsky Moment' is a sudden collapse of asset prices that follows a long period of growth, sparked by debt or currency pressures.

In China, stocks eked out modest gains overnight, but ended the week lower; amid concerns China's economy is losing momentum after official data showed growth slowing in Q3 and property sales softening. The Shanghai Composite Index added +0.3% while the blue-chip CSI300 index fell -0.1%. For the week, CSI300 was up +0.2%, while SSEC lost -0.4%.

In Europe, regional bourses have opened higher and are maintaining that trend. The risk sentiment is supported by political developments in U.S. The outlier continues to be Spain due to Catalonia uncertainty heading into weekend.

U.S stocks are expected to open a tad higher (+0.1%).

Indices: Stoxx50 +0.2% at 3,607, FTSE +0.1% at 7,532, DAX +0.2% at 13,020, CAC-40 +0.1% at 5,372, IBEX-35 -0.1% at 10,190, FTSE MIB +0.5% at 22,239, SMI flat at 9,237, S&P 500 Futures+0.1%

2. Oil rises on tighter fundamentals, gold lower

Oil prices have rallied ahead of the U.S open, supported by signs of tightening supply and demand fundamentals, but a warning about excessive China economic optimism continues to provide regional resistance.

Brent crude futures are at +$57.45, up +22c, or +0.4% from Thursday's close. U.S West Texas Intermediate (WTI) crude futures are at +$51.54 per barrel, up +25c, or +0.5%.

Data this week from the EIA showed that U.S commercial crude oil stocks have dropped -15% from their March records to +456.5m barrels, well below levels seen last year.

Gold prices have turned lower ahead of the U.S open as the dollar gains traction after the U.S Senate approved a budget plan for the 2018 fiscal year. Spot gold has declined -0.4% to +$1,284.06 an ounce. The yellow metal is down -1.6% for the week.

3. Sovereign yields back up

Thus far, the market consensus believe it's unlikely that we will get an official announcement next week on whether the ECB's QE tapering will be asymmetric, but there may be hints. The European Central Bank (ECB) meets Oct 26.

Consensus expects the ECB to cut its bond purchase total to €30B from the current €60B per month and continue at that volume for nine months, starting in January. Officials are expected to leave it opened ended, to extend after September, and hint that this decision will be taken in a data-dependent fashion as per usual.

The yield on U.S 10's has backed up +5 bps to +2.36%, the highest in more than four months. In Germany, the 10-year Bund yield has climbed +4 bps to +0.44%, the largest increase in three-weeks, while in the U.K 10-year Gilt yield has advanced +3 bps to +1.276%.

4. Dollar advances vs. G10

The USD has found traction, supported by the U.S Senate adopting a fiscal 2018 budget resolution that has raised the markets hopes that Presidents Trumps tax plan could actually pass.

Higher U.S Treasury yields are also providing support for the world's reserve currency of choice. It's believed that Trump's advisors appear to be steering him towards choosing either Taylor or Powell as the next Fed chair, which is being considered as a 'hawkish' move.

Sterling (£1.3129) continues to trade on the back foot, today's initial softness being attributed to BoE's Cunliffe comments that he is committed to the process of slowly raising interest rates, but called the timing an 'open question.' However, the currency continues to be guided by Brexit rhetoric.

Elsewhere, USD/JPY is trading at four-month high at ¥113.40 aided by interest rate differentials and by the markets expectation that this weekend's Japanese election will give PM Abe's ruling coalition a solid win, with as many as 300 of the 465 seats in the Lower House.

5. U.K. borrowing declines

Data from the Office for National Statistics (ONS) this morning shows that the U.K Government borrowing in Britain declined in the first six months of the financial year compared with the same period a year earlier, buoyed by strong tax receipts.

The public sector borrowed +£32.5B in the six months-through September to plug the gap between spending and taxes, compared with +£35B in Q1 of last year.

The figures suggest that Treasury chief Philip Hammond is on track to meet forecasts for borrowing of +£58.3B for the financial year as a whole.

Note: The outlook for U.K public finances has worsened in recent months, however, as weakening consumer spending and uncertainty over the country's future ties to the European Union weigh on growth.