Sample Category Title

EUR/CHF Bearish Breakout

EUR/CHF has exited short-term bullish trend. Downside pressures are now likely to accelerate. Strong resistance lies at 1.1566 (12/10/2017 high). Support is given at 1.1388 (02/09/2017 low). Downside risk is very likely.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Bearish Pressures

EUR/GBP's weakness is only a consolidation. The pair is back below former resistance at 0.8899 (19/09/2017 low). The very short-term technical structure is clearly biased to the downside. Hourly support is given at a distance at 0.8746 (27/09/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

AUD/USD Consolidating Below 0.79

AUDUSD is consolidating lower. Hourly resistance is given at 0.7897 (13/10/2017 high). Support lies at at 0.7733 (06/10/2017 low). Expected to show continued consolidation.

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Middle Of Rising Channel

USD/CAD continues to bounce within uptrend channel. Strong support is located at a distance at 1.2062 (08/09/2017 low). Hourly support lies at 1.2331 (26/09/2017 high). Resistance is given at 1.2663 (31/08/2017 high). Expected to show continued short-term bullish pressures within uptrend channel.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head further lower.

USD/CHF Pushing Higher

USD/CHF is trading within uptrend channel, Hourly support stands at 0.9712 (12/10/2017 low). The technical structure suggests an improving short-term buying interest. Expected to show continued bullish pressures within uptrend channel.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

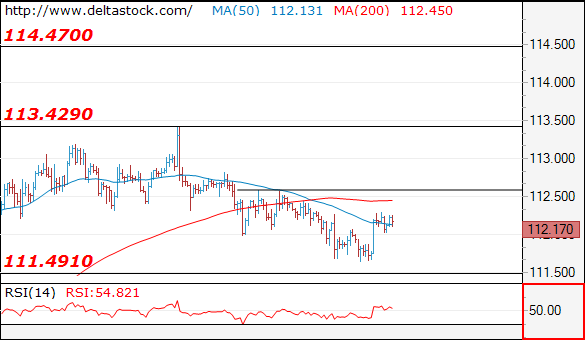

USD/JPY Bullish Breakout

USD/JPY has exited short-term decline. The pair is trading slightly above 112.00. Strong hourly resistance is given at 113.44 (06/10/2017 high). Support is located at 111.12 (20/09/2017 low). However downside risks are definitely rising as markets are now taking some short-term profit after the strong increase during September,

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

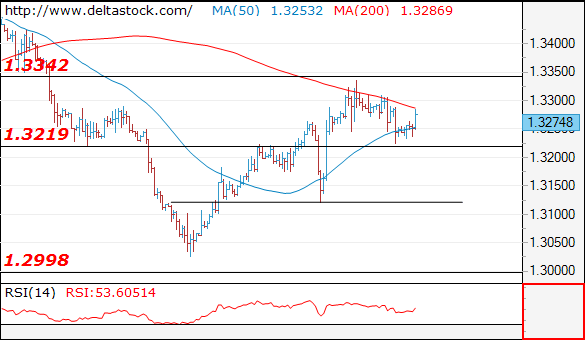

GBP/USD Ready For Another Leg Higher

GBP/USD continues to rise after the break of falling channel. A support can be found at 1.3122 12/10/2017 low). Hourly resistance stands at 1.3338 (13/10/2017 high).

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. Long-term support can be found at 1.1841 (07/10/2017 low). Long-term resistance given around 1.35 is at stake and indicates a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

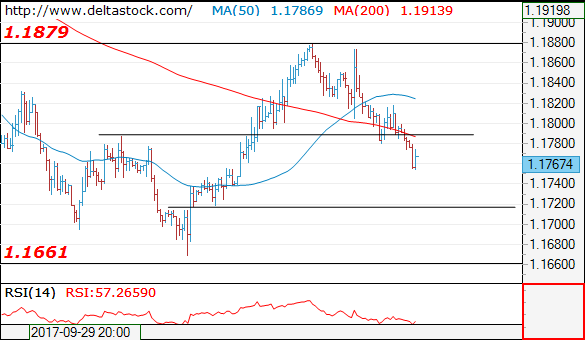

EUR/USD Increasing Selling Pressures

EUR/USD momentum is reversing since the pair has set up an hourly resistance at 1.1878 (12/10/2017 high). Strong support is given at a distance at 1.1662 (17/08/2017 low). Expected to show some short-term consolidation.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1790

My outlook remains bearish, for a slide towards 1.1720 area, en route to 1.1660 lows. Initial resistance lies at 1.1780.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1780 | 1.1940 | 1.1720 | 1.1660 |

| 1.1880 | 1.2030 | 1.1660 | 1.1480 |

USD/JPY

Current level - 112.17

After the recent reversal at 111.60 my outlook is already bullish, for a break through 112.60, towards 113.40.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 112.60 | 114.50 | 111.50 | 111.00 |

| 113.40 | 114.50 | 111.00 | 107.30 |

GBP/USD

Current level - 1.3274

Despite the intraday risk of one more short-lived spike to 1.3340, the overall bias is bearish, for a break through 1.3220, towards 1.3120, en route to 1.3000 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3340 | 1.3340 | 1.3220 | 1.2910 |

| 1.3460 | 1.3650 | 1.3120 | 1.2760 |

Technical Outlook: Spot Gold Eases Further As Safe-Haven Buying Fades

Spot Gold extends weakness on Tuesday to $1287, following Monday's upside rejection at $1305 and close in red.

Today's fresh bearish extension signal pullback, with slow stochastic reversed from overbought territory and showing a plenty of room at the downside.

The yellow metal was hit by stronger dollar and reduced safe-haven buying.

Gold price bears dented pivotal supports at $1288/87 zone (Fibo 38.2% of $1260/$1306 upleg / 20SMA) break of which would generate fresh bearish signal and risk extension towards supports at $1283 and $1277 (Fibo 50% and 61.8% retracement of $1260/$1306 respectively).

Broken 55SMA ($1296) marks solid resistance and caps today's action.

Res: 1296, 1300, 1305, 1309

Sup: 1287, 1283, 1277, 1275