Sample Category Title

Forex: Iraqi Tensions Impact Oil Prices

On Monday, Iraqi forces moved to take control of the city of Kirkuk that had been under control of a Kurdish faction since 2014 and had recently voted for independence in a referendum with Baghdad objections. Kirkuk is home to over 10% of Iraq’s oil reserves and the “takeover” brought concerns to the markets regarding supply disruptions, which helped pushed WTI up to a 3-week high before retracing overnight.

The Reserve Bank of Australia released the minutes of their October 3rd meeting earlier today. The minutes reveal that the RBA appears to be in no hurry to hike interest rates, as many of its global peers are moving towards reducing monetary stimulus. The RBA noted that recent data pointed to reduced price pressures with a relatively strong labour market expected to support higher consumer spending that is restricted by slow growth in real wages and high levels of household debt. Whilst the Australian economy is improving, it is evident that the RBA is not thinking about raising interest rates anytime soon.

AUDUSD is little changed in the early Tuesday trading session at 0.7850.

On Monday, Spain’s deputy prime minister, Mrs. Soraya Sáenz de Santamaría, says that Catalonia’s leader didn’t give an adequate response in his letter about the region’s independence and has until Thursday to comply with the country’s laws. Catalonia Leader Puigdemont’s letter, issued two hours before a Monday deadline, didn’t clarify whether he in fact declared Catalonia’s independence from Spain. He called for talks with Spain’s government. Puigdemont now has until Thursday to give a response – the Spanish Government wants a simple “yes” or “no” – before Spain could activate Article 155 of the Constitution, which would allow the central government to take over parts of Catalonia’s self-governance.

EURUSD is 0.15% lower in early trading. Currently, EURUSD is trading around 1.1780.

USDJPY is little changed overnight, currently trading around 112.15.

GBPUSD is unchanged from Monday’s close to currently trade around 1.3255.

Gold is 0.2% lower overnight, currently trading around $1,292.50.

WTI gave back Monday’s gains to trade 0.3% lower in early Tuesday trading. WTI currently trades around $52.05.

Major data releases for today:

At 09:30 BST, UK National Statistics will release Consumer Price Index (YoY) for September. UK inflation is expected to climb to 3.0% from the previous release of 2.9%. A figure above 3.0% will put pressure on the Bank of England to raise UK interest rates sooner rather than later. Depending on the actual number the markets could experience increased volatility in GBP pairs.

At 11:00 BST, Eurostat will release Consumer Price Index & Core (YoY) for September for the Eurozone. The forecast is expected to come in unchanged at 1.5%, with Core CPI expected at 1.1%. Any deviation from the consensus is likely to cause EUR volatility.

At 11:15 BST, Bank of England Governor Mark Carney is scheduled to appear before members of the UK Parliament’s Treasury Select Committee, in which he will be questioned over recent policy decisions – and where he sees policy heading over coming months.

At 14:15 BST, the Board of Governors of the Federal Reserve will release Industrial Production (MoM) for September. The last release was greatly affected by the Hurricanes and came in at -0.9%. With the rebuilding process well underway and many factories back in operation, the release is expected to show a positive figure of 0.2% for September. A positive figure will be seen as inflationary and will help the Fed in justifying a rate hike before the end of the year.

Trade Idea : USD/JPY – Stand aside

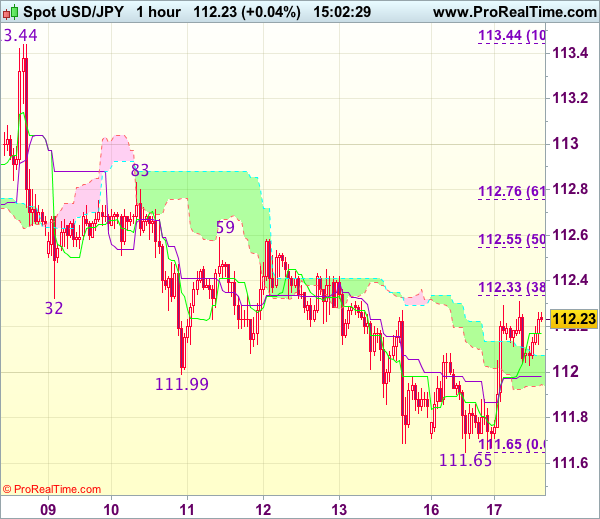

USD/JPY - 112.19

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 112.17

Kijun-Sen level : 111.98

Ichimoku cloud top : 112.07

Ichimoku cloud bottom : 111.95

Original strategy :

Sold at 112.25, stopped at 112.25

Position : - Short at 112.25

Target : -

Stop : - 112.25

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite falling to 111.65 yesterday, as dollar found good support there and has staged a strong rebound, suggesting a temporary low is possibly formed and consolidation with mild upside bias is seen for gain to 112.33-35 (38.2% Fibonacci retracement of 113.44-111.65), however, break of 112.55-59 (50% Fibonacci retracement and previous resistance) is needed to confirm and bring further subsequent gain to 112.76 (61.8% Fibonacci retracement) but reckon resistance at 112.83 would hold from here.

On the downside, expect pullback to be limited to 111.90-95 and said support at 111.65 (yesterday’s low) should hold, bring another rebound later. A drop below 111.65 would revive bearishness for the fall from 113.44 top to extend weakness to 111.47 support and later towards another previous support at 111.11 which is expected to remain intact. As near term outlook has turned mixed, would be prudent to stand aside for now.

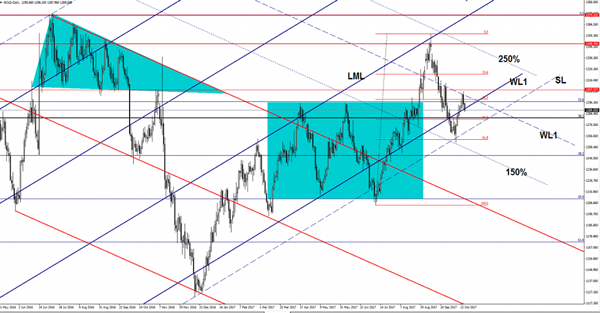

Gold Very Heavy

The yellow metal was rejected by the first warning line (WL1) of the major descending pitchfork and now could ignore the support from the warning line (WL1) of the ascending pitchfork. Gold has made a false breakout above the 38.2% retracement level and now is expected to reach the 50% level again. Only a valid breakdown below the SL will confirm a broader drop.

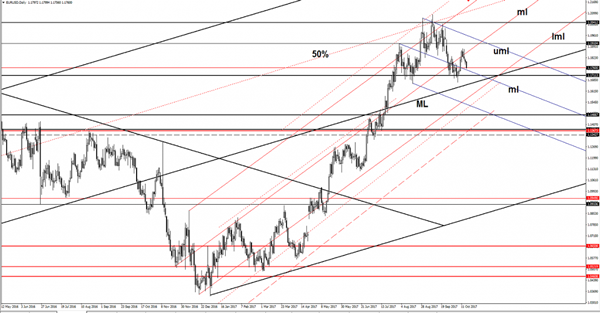

EUR/USD On The Way Down

Price dropped and is almost to reach the median line (ml) of the descending pitchfork, where he may find temporary support. The current drop is natural after the false breakout above the median line (ml) of the minor ascending pitchfork. However, only a valid breakdown below the median line (ML) of the major ascending pitchfork will confirm a larger drop.

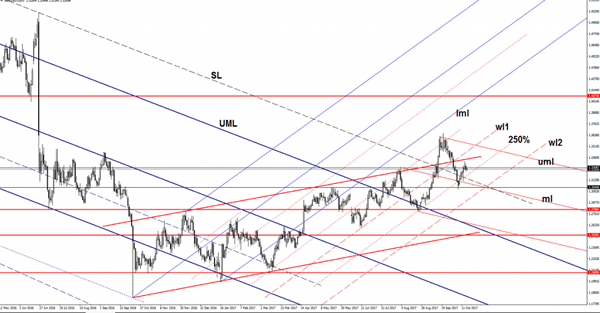

GBP/USD Is The Rebound Completed?

The GBP/USD decreased a little today, but looks undecided as the USDX is facing a tough resistance. Will be better to stay away right now because we don’t have any trading opportunity. Price is trading near crucial support and resistance level, so I hope that we’ll have a clear direction very soon.

You should be careful later as the Fundamental factors will take the lead and will drive the price, remains to see the direction. The US and the United Kingdom are to release high impact data, which will bring life on the currency market.

The Cable could receive a helping hand from the UK’s inflation data, the CPI is expected to increase by 3.0% in the previous month, while the Core CPI may increase by 2.7%, matching the 2.7% growth in the former reading period. You should keep an eye on the economic calendar today because is filled with significant data.

The GBP/USD failed to reach and retest the upside line of the up channel and failed to stay above the 1.3268 as well and now should hit the 250% Fibonacci line again. The perspective remains bullish as long as the rate stays above this line. Price has shown some exhaustion signs on the short term as the USDX has pushed the USD higher. Is very important to see what will really happen on the USDX because a further increase will send the rate tumbling.

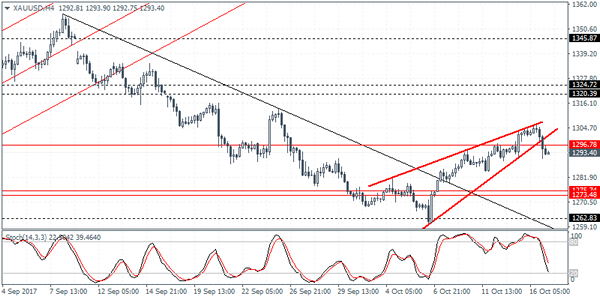

XAUUSD Intraday Analysis

XAUUSD (1293.40): Gold prices turned bearish, and eventually price action was seen slipping to the downside from the rising wedge pattern. With the minor support level at 1296.00 being cleared, the bias remains to the downside as a result. Support is seen at 1275 - 1274 which could be the next downside target. However, in the event of a breakout above 1296.00 level, gold prices could be seen pushing higher. The next target area comes in at 1320.00 resistance level. The current breakdown comes with price action posting an outside bar on the daily session.

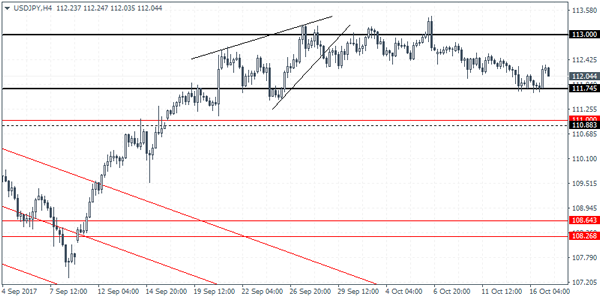

USDJPY Intraday Analysis

USDJPY (112.04): The USDJPY closed on a bullish note yesterday recovering from Friday's declines. Price action remains in a consolidation mode. On the 4-hour chart, the bounce off the minor support at 111.74 saw prices briefly pushing higher, although current price action is seen giving up some of the gains. With the range strongly established at 113.00 and 111.74, USDJPY could be looking at a volatile breakout soon. While the gains to the downside are limited towards the next support at 111.00, to the upside, clearing the resistance at 113.00 could signal further gains in price.

EURUSD Intraday Analysis

EURUSD (1.1780): The EURUSD was seen trading lower on Monday although price action was modest. Following the breakdown below the resistance and support level of 1.1843 - 1.1822, EURUSD could be seen pushing lower. The next support at 1.1720 will be the next big target for the common currency. Overall, price action is likely to remain range bound, but the bias for a downside decline is increasing. On the daily chart, the EURUSD is attempting to carve out a head and shoulders pattern with the neckline support seen at 1.1704. A breakdown below this level will see EURUSD posting further declines for a minimum target of 1.1440.

New Zealand CPI Rises 0.5% On The Quarter

The quarterly inflation data from New Zealand saw consumer prices rising 0.5% in the quarter ending September. It was higher than the median estimates of 0.4% and also beat the 0.2% forecast given by the Reserve Bank of New Zealand. The third quarter increase in inflation puts it in line with the RBNZ's target although the central bank is likely to wait for more evidence that inflation was firming.

Elsewhere, the German wholesale price index data showed a 0.6% increase on the month, beating estimates of 0.4% and doubling from the 0.3% increase in the previous month. The US dollar was seen maintaining its gains on Monday.

Looking ahead, the UK's consumer price index data is due for release today. Economists expect consumer prices in the UK to hit 3% in September, accelerating slightly from the 2.9% increase the month before. The BOE Governor Carney is expected to speak later in the day. From the Eurozone, the final inflation figures for September will be released today. Headline CPI is expected to rise 1.5% while core CPI is expected to rise 1.1% on a yearly basis.

UK Inflation Data Key As BoE Ponders Rate Hike

- Will UK inflation data alleviate policy makers concerns?

- Three BoE policy makers appear before Treasury Select Committee;

- Eurozone inflation data eyed as ECB prepares QE reduction.

European equity markets are expected to open relatively flat on Tuesday, as we await some important inflation data from the UK and the eurozone, as well as appearances from Bank of England policy makers.

It could be an important week for the UK as we get three economic reports that could strongly influence whether or not the BoE follows through with plans to raise interest rates for the first time since the global financial crisis. Policy makers have shown a desire to do so in recent months despite the outlook for the economy being far from encouraging.

The MPC is apparently growing increasingly concerned about persistent above target inflation, despite the fact that the one-off post-referendum currency devaluation has likely played a considerable role in this. If this is the case then we would expect annual measures of inflation to naturally correct themselves, which suggests policy makers are of the belief that the numbers go beyond these transitory factors.

Should the September CPI data remain elevated – as is expected – it’s unlikely to ease policy makers concerns, making a rate hike this year all the more likely. If the data falls short of expectations then those policy makers that remain on the fence – which appears to include Governor Mark Carney – may be inclined to await more data before committing to a rate hike, which could weigh on sterling and boost the FTSE.

Carney is due to appear before the Treasury Select Committee this morning so we could get his view on interest rates then. His new colleagues Sir David Ramsden and Silvana Tenreyro will also make an appearance earlier in the morning, which could provide important insight as none of the three have so far voted in favour of raising interest rates.

The BoE is not the only central bank looking to tighten monetary policy before the year is out. The ECB is believed to be preparing plans to end its quantitative easing program, possibly starting with a 50% reduction and nine month extension from January, bringing purchases down to €30 billion until September next year.

The improved economic outlook has coincided with improvements in inflation in the eurozone and as long as this continues to point in the right direction, policy makers are likely to continue towards policy normalisation. We’re expecting no revisions to the September CPI data today, with overall inflation seen remaining at 1.5% and core at 1.1%