Sample Category Title

Market Morning Briefing: Dollar-Yen Looks Mixed/ Bullish

STOCKS

Overall global stock indices look bullish just now. While Dow could be poised for some more upmove in the coming sessions, Nikkei and Dax may possibly see a pause near current levels.

Dow (22956.96, +0.37%) is slowly rising and could move up towards 23000-23250 levels in the near term. Thereafter a small dip is possible towards current levels. Near term looks positive.

Dax (13003.70, +0.09%) has paused slightly just at the crucial resistance level and a sharp break above current levels is needed to initiate fresh bulls in the near to medium term. Else a corrective dip from here is possible, taking the index back towards 12800 levels.

Nikkei (21260.89, +0.03%) came off after testing 21400 on the upside. As mentioned yesterday, Nikkei looks overbought and a slight correction from here is preferred which could take the price down towards 21100 or lower. A failure to stop at 21400 (if seen) may take it higher to 21500/600 in the near term.

Shanghai (3372.73, -0.17%) has some scope of testing 3350/60 on the downside before re-attempting a rise towards 3410.

Nifty (10230.85, +0.62%) looks positive this week and could move up towards 10300/10 levels if the bulls continue to remain strong. Near term looks bullish.

COMMODITIES

Gold (1293.38) has come off as expected. While 1308 holds, the price could test 1280 before again rising back in the medium term.

Silver (17.20) is likely to test 17 before again bouncing back towards 17.35/40 again in the medium term. For now some sideways movement within 17.00-17.50 is preferred.

Brent (57.83) and WTI (51.81) are almost stable near levels seen yesterday. Both made an intra-day high yesterday to 58.47 and 52.37 respectively but came off to close at lower levels. There is some scope that the prices may move up in the near term towards 59 and 53 respectively.

Copper (3.2315) has moved up sharply to test immediate resistance levels seen on the line charts. A rejection from these levels looks possible in the next few sessions towards 3.15/10. Else a rise to 3.30/35 is likely before a sharp corrective fall is seen.

FOREX

Although we are bullish on the Euro (1.1780) in the longer term, with Support at 1.1730, we also notice possibilities of a Bear Shoulder-Head-Shoulder developing. A break/ close below 1.1700 could negate the bullish prospect.

We prefer bullishness on the Euro because the Dollar Index (93.35) may have Resistance between current levels and 93.50.

But, there are warning signs coming from Euro-Yen (132.05) which could be breaking its uptrend and from the German-US 10Yr Spread (-1.93%), which is trading below its earlier support trendline. Also, US yields have moved up (see Interest Rates below). So, we need to be careful about our current bullishness on the Euro.

Dollar-Yen (112.09) looks mixed/ bullish. The Pound (1.3258) has slipped a bit since yesterday and so has the Aussie (0.7850).

Dollar-Rupee (64.74/75) might start moving up soon, even though the NDF shows 64.70/74.

INTEREST RATES

Contrary to expectation, US Bond yields (5yr 1.96%, 10Yr 2.31% and 30Yr 2.82%) have moved up yesterday instead of coming down towards 1.81%, 2.21% and 2.72% respectively.

The US Yield Curve itself has flattened quite a bit, with a dramatic decline in the 10-5 Spread from 0.41% on 3rd Oct to 0.35% now. The 30-5 (0.87%) continues to be in a long-term downtrend that could potentially target 0.75%.

German Yields (5Yr -0.34% and 10Yr 0.37%) could have Supports here, but they seem to be rising slower than US yields.

In India too, we may see the Indo-US 10r Spread (4.4541%) come down.

EUR/JPY Taps Important Level Once Again

Remember the EUR/JPY retesting confluence of support setup that we were trading? Well we're back!

This is a prime example of what actually normally happens once a trend line breaks. We see sideways consolidation followed by price simply moving back in the direction of the original trend:

EUR/JPY Daily:

But it's the marked horizontal level that I really wanted to highlight this morning. By looking for confluence of support and backing up trend lines with solid horizontal levels, you're giving yourself that backstop. There is no subjectivity in a straight line and as you can see here, the level has been touched again basically to the pip.

So long as price is above the higher time frame zone that is also on that chart, these sorts of pullbacks should be looked at as possible buying opportunities.

Topsy Turvy Tuesday?

Topsy Turvy Tuesday?

Dealers have spent the last 24 hours digesting Friday's CPI fallout while keeping an eye on geopolitical risk amidst the deluge of Fed chair speculative headlines. As for the dollar, there was nothing earth-shattering within these idiosyncratic storylines usurping any broader USD trend. All in all, it made for a somewhat sleepy Monday in G-10

It's not wise getting too comfortable as tranquil Monday's tend to foreshadow a climatic tipping point and today's substantial economic diary could prove to be a real test of investor sentiment.

Also, it's worth keeping an eye on the expanding laundry list of geopolitical flashpoints. We're not only dealing with issues in the Korea Peninsula, but now an unpopular shooting war between Iraqi forces and the Peshmerga is full blown. With Turkey-US relations souring, and as the world is still trying to figure out what to do with ISIS, the Middle East looks like a powder keg waiting to explode.

Fed Chair debate

There's a growing buzz surrounding Stanford's Taylor who is suggested to be in Trump's good books, while the lack of impressive academic credential seems to be weighing negatively for former frontrunner Kevin Warsh. Also, Yellen is rumoured to be meeting with the president this week, and she is expected to be the last primary candidate interviewed for the job suggesting that decision time is near.

Euro

Traders continue to probe the EUR downside resolve after last weeks dovish Draghi comments and a slight rise in EU political risk in the wake of the surprising Austrian elections The EUR was primarily offered against the crosses with EURJPY looking suspectable to the bid tone on USDJPY.

Australian Dollar

The AUD was G-10 worst performer overnight despite the common signals suggesting otherwise. Metals ratcheted higher on very optimistic growth forecasts coming out of the Communist Party Summit. Also, yesterday's China Data supported regional risk, so the overnight AUD sell-off is a bit surprising. However, the reversals is likely more a case of traders taking profit ahead of the RBA Minutes based on their well-known dovish guidance

The British Pound

Brexit headlines continue to batter the Pound but with UK CPI report for September; and the testimonies of three key BoE members (Carney and for the first time, members Ramsden and Tenreyro) on tap, sterling traders will be buckling in for a bumpy ride. UK inflation is sitting just shy of the 3%, and if Septembers forecast to touch the elevated 3 % level, it will exert immense pressure on the BoE to begin the tightening cycle and should play positively for the Pound. Keep in mind; Carney has been extraordinarily Hawkish of late so his testimonies will also be a central focus for traders this afternoon.

Japanese Yen

The anticipated wave of dollar selling after last Friday's weak CPI failed to gain much traction below 111.75, and then USD bounced to 112.20 on Bloomberg headlines reiterating that Taylor is in Tumps good books. Thre remains an air of apprehension to sell dollar this week as traders are looking over their shoulder as hawkish Fed Chair headlines unfold.

Little to report ahead of the election this coming Sunday, where Abe continues to look strong. A substantial outcome for Abe should, in turn, mean a weaker JPY.

Chinese Yuan

Chinese data was robust but had a minor impact on currency markets. Unquestionably, the market is sitting tight while keeping eyes peeled and ears to the ground for any groundbreaking policy shift to come out of the Chinese Communist Pary Congress

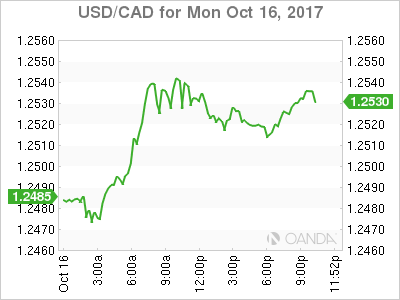

USD/CAD Canadian Dollar Lower As Growth Expectations Drop

The Canadian dollar depreciated on Monday after the release of the Bank of Canada (BoC) survey of managers. The Business Outlook Survey fell from 2.81 last quarter to 0.86. The anticipated slowdown in economic growth after it expanded at an accelerated growth was reflected in the reduced forecasts. The end result still points to a healthy economy, but not at the same pace that put the central bank into hiking rates twice.

The NAFTA negations have been anything but smooth sailing. The US trade delegation has been pushing for more America First clauses that have not been taken well by the Canada and Mexico delegations. The US tabled an idea a higher regional content for autos to be part of the free tariff access. Current North American content requirement is 62.5 percent and the US wants to increase that to 85 percent (with 50 percent of that being US content).

Negotiations have been tense after the US also proposed a five year term for the updated NAFTA, to which both Canada and Mexico had already objected. US and Mexican governments wanted to wrap up trade negotiations before the end of the year, but with the current pace of progress make this very unlikely.

The USD/CAD rose 0.47 percent since the Asian open. The currency pair is trading at 1.2528 as the US Empire State Manufacturing index posted a higher than expected figure. The survey of NY manufacturers was 30.2 on a 20.3 forecast. The combination of a softer BoC Business Outlook Survey in Canada and a stronger manufacturing indicator in the US further tipped the scales in favour of the US dollar.

NAFTA uncertainty has put the Bank of Canada (BoC) on alert as the loonie could lose up to 10 percent of its value if the Trump administration ends the agreement with no renegotiation. The central bank will meet next week, with 20 percent probability of a rate hike, but since the September rate hike and with a softer pace of growth a third rate hike in 2017 is still a long shot. Inflation and retail sales data later in the week will be more telling on what the BoC could do before the end of the year.

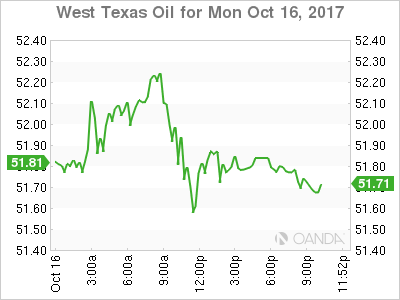

West Texas Intermediate prices have been volatile due to geopolitical events but seem to be attracted to the 51.80 level. The disruption of oil production from Kirkuk in Northen Iraq after the army seized the territory from Kurdish fighters drove prices to the $52.30. The situation is still ongoing, but for now prices remain stable below $52.

The comments from US President Donald Trump threatening to end the Iran nuclear had a positive effect on prices as lower output from oil pushed prices higher. The US congress has a 60 day period to decide if it reinstates the economic sanction to Iran.

Market events to watch this week:

Monday, October 16

5:45pm NZD CPI q/q

8:30pm AUD Monetary Policy Meeting Minutes

Tuesday, October 17

Tentative GBP BOE Gov Carney Speaks

4:30am GBP CPI y/y

Wednesday, October 18

4:30am GBP Average Earnings Index 3m/y

8:30am USD Building Permits

10:30am USD Crude Oil Inventories

8:30pm AUD Employment Change

10:00pm CNY GDP q/y

10:00pm CNY Industrial Production y/y

Thursday, October 19

4:30am GBP Retail Sales m/m

8:30am USD Unemployment Claims

Friday, October 20

8:30am CAD CPI m/m

8:30am CAD Core Retail Sales m/m

7:15pm USD Fed Chair Yellen Speaks

$1300 Gold Pauses After Strong Week

Gold prices are unchanged in the Monday session. Currently, the spot price for an ounce of gold is $1303.94, up 0.04% on the day. On the release front, there are no major releases out of the US. The Empire State Manufacturing Index soared to 30.2 points, easily beating the estimate of 20.3 points. This was the indicator's highest level since 2009.

Gold prices climbed 2.2 percent last week, as the metal closed on Friday above the symbolic $1300 level. The gold rally continued on Friday, as investors were disappointed that September CPI and Core CPI both missed their estimates. Low inflation levels continue to frustrate Fed policymakers, many who have predicted that a strong US economy and red-hot labor market will boost inflation levels. With inflation an important consideration in future rate decisions by the Federal Reserve, investors will be anxiously monitoring how Fed policymakers respond to September's soft inflation numbers. So far, the soft inflation numbers have not affected the odds of a December rate hike, as fed futures have currently priced a December hike at 91 percent.

The crisis over Catalan independence is at a deadlock, in if the situation escalates, nervous investors could dump euros in favor of safe assets such as gold. Last week, the Spanish government set a Monday deadline for Catalan President Carles Puigdemont to expressly state whether he had declared independence, and if so, Puigemont was given three more days to retract his proclamation. However, the Catalan President shirked away from a clear answer and let the first deadline pass, calling for more dialogue with Madrid. Prime Minister Mariano Rajoy has threatened to suspend the Catalan parliament and impose direct rule from Madrid, which could trigger a violent response. The crisis has led 500 companies to start leaving Catalonia, and the Standard and Poor's rating agency has said that the region could face a recession if the crisis continues.

Elliott Wave Trade Ideas Performance Update

4 positions were entered last week with total loss of 100 points and the positions are listed below.

9 Oct : EUR/GBP - Short at 0.8930, exited at 0.8970 (- 40 points)

10 Oct : EUR/JPY - Short at 132.40, exited at 133.00 (- 60 points)

13 Oct : GBP/USD - Short at 1.3315,

16 Oct : AUD/USD - Short at 0.7875,

| AUD EUR/JPY EUR/GBP CAD GBP GBPJPY

Jan - 15 -275 - 35 -120

Feb + 140 -17 - 40 +11

Mar - 20 +115 +132 - 19

Apr + 30 - 40 +120 + 45

May - 55 +100 - 6 -65 -60

Jun + 81 +150 - 10 +185 -120 +205

Jul - 40 - 60

Aug +155 +200 + 100 + 195 -45 - 50

Sep -50 + 165 + 5

Oct - 60 - 40 +200

Nov

Dec

Y-T-D + 371 + 8 +127 +823 -230 +285

Candlesticks and Ichimoku Trade Ideas Performance Update

4 positions were entered among all 4 currency pairs with total loss of 25 points and the positions are listed below:

10 Oct : GBP/USD - Short at 1.3170, exited at 1.3195 (- 25 points)

12 Oct : USD/CHF - Short at 0.9755,

13 Oct : USD/JPY - Short at 112.25,

13 Oct : GBP/USD - Long at 1.3250,

| JPY EUR CHF GBP

Jan + 167 - 85 - 10 + 50

Feb + 200 +150 +93 - 59

Mar -23 -70 -23 - 35

Apr + 65 + 93 + 50 - 40

May - 65 - 35 + 100 -175

Jun -100 -10 - 10 +175

Jul + 85 - 35 - 8

Aug + 35 +210 + 35 +65

Sep +129 +210 +200 - 70

Oct - 35 - 25

Nov

Dec

Y-T-D + 492 +423 +392 -104

Pound Steady ahead of May’s Brussels Meeting; Euro Posts Moderate Losses after Puigdemont Misses Deadline

With Fed chair Janet Yellen being confident that inflation measures will move towards the Fed's 2% target in the upcoming months and business conditions improving the most in three years in October according to a survey conducted by the New York Fed, the dollar index managed to gain 0.12% on the day, climbing to a 5-day high of 93.36. Dollar/yen stood flat around 111.81.

Meanwhile, in the fiscal policy front, a tax analysis released by the Trump administration on Monday tried to counter criticism that tax proposals are largely benefitting the rich, showing that middle-class earnings would increase by $4,000 under the new tax reforms.

The Catalan leader, Carles Puigdemont, missed the deadline set by the Spanish government, choosing instead to reply to the Spanish Prime Minister, Mariano Rajoy, with a letter, in which he insisted for both sides to start a dialogue over the next two months. As a response, Rajoy expressed through a written statement that Puigdemont would be "solely responsible" if the Spanish government takes control of the region, while Spain's Deputy Prime Minister, Soraya Sáenz de Santamaría warned that Madrid would take the "next step" unless Catalonia changes its stance by Thursday.

In terms of data released today out of the Eurozone, August's trade surplus narrowed to 16.1 billion euros as the growth in imports offset the rise in exports due to a stronger currency. Expectations were for trade surplus to increase by 0.1 billion euros to 23.3 billion.

The news above, however, had a moderate impact on the euro at a time when political concerns in other Eurozone countries (besides Spain) are on the rise, as traders were more confident that ECB policymakers will announce the tapering of the central bank's asset-buying program on October 26. Particularly, political risks involved the rising support for Euroskeptic parties in Sunday's national elections in Austria and in Germany the previous month, which gave the chance to far-right parties to enter the government after a long time of absence. The euro managed to recoup part of its losses against the dollar during the session, climbing to $1.1809 after earlier touching a one-week low of $1. 1779.Still, the pair remained 0.13% down on the day.

The pound was trading steadily around $1.3281 as the UK Prime Minister, Theresa May, was preparing for her meeting with the head of the European Commission, Jean Claude Junker, and the EU's Chief Brexit negotiator, Michel Barnier, in Brussels at 1630GMT. May's spokesman said on Monday that the British Prime Minister is expecting a "constructive" discussion that would contribute to her efforts for a smoother Brexit. CPI readings out of the UK will be also in focus on Wednesday with analysts forecasting headline inflation to rise slightly by 0.1 percentage points to 3.0% y/y in September.

The loonie was the worst performing major currency, tumbling to a one-week low as the time is ticking for NAFTA negotiations. The treaty was not successfully updated so far. Negotiators are seeking to extend the remaining rounds (three out of seven) to meet a deadline at the end of December after tough proposals by the Trump administration complicated the talks. Dollar/loonie gained 0.58%, last trading at 1.2538.

In energy markets, oil prices surged on the news that Iraq's Kurds disrupted oil production amounting to 350,000 bpd as tensions heightened with the Iraqi government. WTI crude jumped by 1.11% to $51.85 per barrel, while Brent drifted higher by 1.47% to $58.01.

Pound Quiet at Start of Week, British CPI Next

The British pound is almost unchanged in the Monday session. In the North American session, GBP/USD is trading at 1.3279, down 0.01% since the Friday close. On the release front, there are no major events in the UK or the US. British Rightmove HPI rebounded in October with a gain of 1.2%, marking a 5-month high. In the US, the Empire State Manufacturing Index soared to 30.2 points, easily beating the estimate of 20.3 points. This was the indicator's highest level since 2009. On Tuesday, the UK releases a host of inflation indicators, led by CPI. The markets are expecting inflation to hit 3.0% in September, up from 2.9% a month earlier.

The Brexit talks are in trouble, as the sides have made little progress after several rounds of negotiations. Prime Minister Theresa May is hopeful of generating some positive momentum, as she meets on Monday with EU Commission President Jean-Claude Juncker and EU chief negotiator Michel Barnier. The Europeans have insisted that there must be progress on a number of issues, such as Britain's divorce payment, before they will discuss a trade deal. The EU holds a summit on Thursday, and could announce that they won't talk trade until next year. Both sides have been talking about the possibility of a 'hard Brexit' in which Britain would leave with no deal being reached, but British businesses are dead set against such a scenario, and are pushing for a 2-year interim period to soften the blow of leaving the EU.

Although the US economy has been performing well and the labor market remains red-hot, inflation numbers remain soft. There was some disappointment in the markets as September CPI and Core CPI narrowly missed their estimates. On the release front, CPI gained 0.5%, short of the estimate of 0.6%. Core CPI posted a small gain of 0.1%, shy of the forecast of 0.2%. With inflation an important consideration in future rate decisions by the Federal Reserve, investors will be anxiously monitoring how Fed policymakers respond to September's soft inflation numbers. Also on Friday, US retail sales data was a mix. Core Retail Sales gained 1.0%, above the estimate of 0.9%. However, retail sales were up 1.6%, short of the forecast of 1.7%.

EUR/JPY – Turned To The Downside

The EUR/JPY dropped and touched fresh new lows today, even if the Nikkei stock index has increased further. The Yen increase also versus the Cable today, not only against the Euro. The JP225 has resumed the upside movement, has managed to reach the 21350 level and maintains a bullish perspective on the daily chart.

The Nikkei has increased sharply in the last weeks and seems poised to hit fresh new highs in the upcoming period, only a minor drop will force the Yen to accelerate the appreciation versus its rivals. The USD/JPY decreased in the last hours as the Nikkie stock index has slipped lower and erased some of the morning gains.

The Yen increased even if the Japanese Revised Industrial Production increased only by 2.0%, less versus the 2.1% estimate and versus the 2.1% growth in the former reading period. On the other hand, the Euro-zone Trade Balance and the German WPI have come in better than expected, but the Euro wasn't impressed.

The EUR/JPY opened with a gap down today, signaling that the bears are very strong on the short term. Price has come back to close the morning gap, but failed to stay above the 132.13 Friday's high. The next downside target will be at the upper median line (UML) of the major ascending pitchfork. Remains to see if we'll have a retest of the broken chart pattern, or will continue to drop. I've said in the previous weeks that only a valid breakdown below the UML will confirm a larger drop.