Sample Category Title

Trade Idea: USD/CAD – Buy at 1.2395

USD/CAD - 1.2543

Trend: Down

Original strategy :

Buy at 1.2395, Target: 1.2595, Stop: 1.2335

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.2395, Target: 1.2595, Stop: 1.2335

Position: -

Target: -

Stop:-

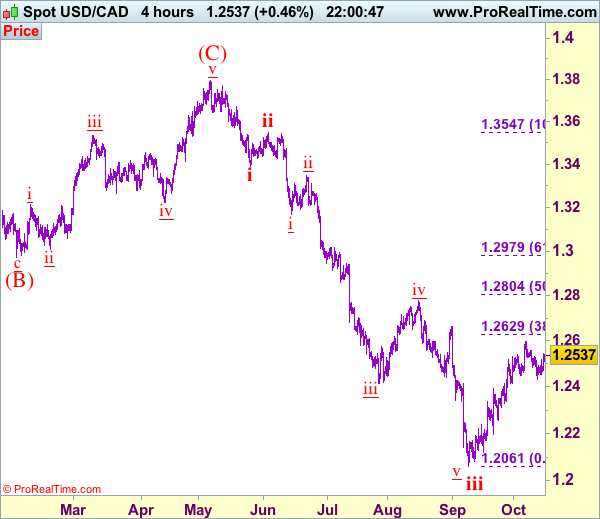

Although the greenback has rebounded again after finding support at 1.2433, reckon upside would be limited to 1.2555-60 and near term downside risk remains for another retreat, below 1.2460-65 would bring test of said support at 1.2433, break there would bring retracement of recent rise to 1.2395-00 where renewed buying interest should emerge, bring another rise, above 1.2555-60 would signal the pullback from 1.2599 has ended, bring retest of this level, break there would extend the rise from 1.2061 low (wave iii trough) towards previous resistance at 1.2663 but upside should be limited to 1.2700 and price should falter well below another previous resistance at 1.2778.

In view of this, would not chase this rise here and would be prudent to buy again on pullback as 1.2395-00 should limit downside. Below 1.2395-00 would bring correction back to 1.2350-55 but reckon indicated support at 1.2313 would hold. Only a drop below 1.2313 would abort and signal the aforesaid rise from 1.2061 has ended, bring further fall to 1.2254 support, however, reckon downside would be limited to another previous support at 1.2197, bring rebound later. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii ended at 1.2414, followed by wave iv correction ended at 1.2778, wave v has reached our indicated downside target at 1.2100 and may extend to 1.2000.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Dollar Going Nowhere. Euro Ignores Catalan Tensions

- European equities eke out small gains today (+0.2%) as the trading week slowly takes off. The Spanish IBEX 35 underperforms (-0.60%) as the standoff between Spain and Catalunya enters a crucial phase. US stock markets opened with gains of around 0.25%.

- The US empire manufacturing matched the highest level since 2009, unexpectedly rising from 24.4 to 30.2 in October (vs 20.4 expected).

- Italian President Mattarella may dissolve parliament the last days of the year, Corriere della Sera reports, without citing anyone. An electoral campaign may follow for 60 days, with election possibly falling on March 4 as one of the options being considered.

- The Spanish government has given Catalan leaders until Thursday to back away from claiming independence or face the possibility of direct rule from Madrid. Catalan president Puigdemont refused this morning to clarify whether he declared Catalonia independent from Spain last week. Mr Puigdemont instead called for dialogue.

- UK MP May travels to Brussels today for talks over dinner with EC Juncker after deadlock in Brexit appeared to dash her hopes a summit this week could launch negotiations on future trade ties. Sources say that Brexit negotiations are heading for a catastrophic breakdown unless the EU signals this week that it will allow talks to move on to trade

- China's central bank governor said the economy could grow 7% in the second half of this year, accelerating from the first six months and defying widespread expectations for a slowdown. The uncharacteristically explicit growth forecast by Zhou Xiaochuan came just days ahead of a twice-in-a-decade Communist Party Congress.

- The BoE confirmed its plans to take over the administration of an important interest rate benchmark in April 2018. April 20 of next year will be the last day that the Wholesale Market Brokers' Association will tabulate and publish the Sterling Overnight Index Average (Sonia), the BoE said.

- Support for billionaire Andrej Babis's ANO party dipped ahead of a Czech election on Oct. 20-21, but the party maintained a double-digit lead over its closest rival and remains favourite to lead the next government.

Rates

Bund outperforms US Note future in rather thin trading

German Bunds outperformed US Treasuries today. Fed chairwoman Yellen reiterated over the weekend confidence that inflation will move to target next year, warranting more gradual rate hikes. Her message slightly weighted on US Treasuries as did the only eco item on today's agenda. The US empire manufacturing for October beat consensus, matching the highest level since 2009. Some European election-related uncertainty might have been at play as well with the (expected) Austrian shift to the right, the (unexpected) outcome of German regional election (Lower Saxony) and the lasting political deadlock between Spain and Catalunya.

Catalan president Puigdemont refused to clarify whether he declared the region independent last week, missing a first Madrid deadline. Puigdemont called again for dialogue, but Madrid immediately answered that dialogue was only possible within the Spanish legal framework. The Catalan president now has three days to change his mind. Otherwise, the Spanish government will trigger article 155, stripping the Spanish region from its autonomy. The Spanish equity market underperformed, but the bond market didn't.

At the time of writing, the German yield curve bull flattens with yields 0.1 bp (2-yr) to 2 bps (30-yr) lower. US yields trade 1.6 bps (30-yr) to 2.2 bps (5-yr) higher. On intra-EMU bond markets, 10-yr yield spread changes versus Germany are nearly unchanged with Portugal (+3 bps) underperforming.

Currencies

Dollar going nowhere. Euro ignores Catalan tensions

There were few eco data in EMU and the US today. The dollar held up well despite Friday's 'soft' US CPI data. Catalan uncertainty weighed mostly on Spanish assets. The impact on other European markets was limited, but EUR/USD struggled not to fall below 1.18. USD/JPY held a tight range in the upper half of the 111 big figure. The dollar profited slightly from a very strong Empire manufacturing survey. EUR/USD trades close to 1.18. USD/JPY hovers just below 112.

The established equity rally continued in Asia. Major central bankers met in Washington this weekend. They saw a further improvement in the global economy. Yellen reiterated that she expects soft inflation readings not to persist. Also ECB top-policy makers expect inflation to pick up. The BoJ indicated to pursue ongoing aggressive monetary easing, but BoJ Kuroda warned that markets might be too complacent when pricing geopolitical risks. USD/JPY profited only modestly from CB signals of ongoing policy divergence between the US/EMU and Japan or from the risk rally. The pair hovered in the 112 area. EUR/USD traded in the low 1.18 area

Early in European dealings, the headlines of a letter of Catalan Leader Puigdemont to Spanish PM Rajoy hit the screens. He didn't answer Spain's question whether he has declared independence, but defended its mandate to do so. An institutional confrontation later this week is still on the cards. EMU/German yields declined slightly more than US ones. EUR/USD lost a few more ticks below the 1.18 handle, but the impact on global markets remained very subdued. Euro selling also evaporated. EUR/USD returned to the 1.18 pivot. Spain repeated that Catalonia has until Thursday to ' rectify' its independence call.

Early in US dealings, there were tentative signs that the dollar could feel some headwinds. However, the Empire manufacturing survey climbed from 24.4 to 30.2, a very strong level (matching the highest since 2009). The report blocked any potential USD losses. The dollar trades little changed in a daily perspective. Maybe this is slightly disappointing for USD bulls given the US data, the ongoing constructive risk sentiment and Catalan uncertainty.

Sterling in a limbo as UK PM May and EU's Juncker meet

There were few eco data in the UK today. Key data including tomorrow's UK price data will be important input for the BoE as it debates the need for a rate hike in the coming months. In the meantime, the focus remained on Brexit. UK PM May went to Brussels today and will meet EU commission president Juncker and EU Chief Brexit negotiator Barnier at CET 18.30. Sterling initially gained a few tics on the announcement of May's Brussels' trip, hoping on a positive outcome. However, this hope was torpedoed by comments from 'sources close to the UK government'. According to these rumours, Brexit negotiations are heading for a catastrophic breakdown unless the EU signals this week it will allow to move to talks on trade and the transition period. EUR/GBP returned to the 0.89 area. Cable traded in the 1.33 area before the Brexit headlines, but returned south again, currently trading in the 1.3265/70 area. (FX) markets look out for the outcome of the next phase in the political poker game between the UK and the EU.

USDCAD – Fresh Bulls Look for Break above Daily Cloud Top

The US dollar rallied against its Canadian counterpart on Monday and broke above daily Tenkan-sen which capped Friday's action and was acting as initial resistance at 1.2515.

The pair is establishing in fresh direction after recovery from last week's low at 1.2432 stalled on Friday, when the action showed strong indecision, ending in long-legged Doji.

Monday's rally cracked barrier at 1.2534 (Fibo 61.8% of 1.2597/1.2432 pullback) and is approaching another pivotal barrier at 1.2552, provided by top of falling thick daily cloud.

Bulls need close above cloud to confirm an end of corrective phase from 1.2597 (06 Oct high) and open way for full retracement of 1.2597/1.2432 correction.

Daily techs in bullish setup are supportive for further advance, with broken Tenkan-sen (1.2515) and 10 SMA (1.2503) marking solid supports which should keep the downside protected and guard lower pivot at 1.2465 (55SMA/Monday's low).

Res: 1.2544; 1.2552; 1.2597; 1.2636

Sup: 1.2515; 1.2503; 1.2465; 1.2446

Trade Idea Update: USD/CHF – Hold short entered at 0.9755

USD/CHF - 0.9759

Original strategy :

Sold at 0.9755, Target: 0.9655, Stop: 0.9775

Position : - Short at 0.9755

Target : - 0.9655

Stop : - 0.9775

New strategy :

Hold short entered at 0.9755, Target: 0.9655, Stop: 0.9775

Position : - Short at 0.9755

Target : - 0.9655

Stop : - 0.9775

Although the greenback fell briefly to 0.9705 late last week, lack of follow through selling on break of previous support at 0.9710-12 and the subsequent strong rebound suggest consolidation above said support would be seen, however, as long as resistance at 0.9772 (Friday’s high) holds, bearishness remains for recent decline to resume after consolidation, below said support at 0.9705 would signal the decline from 0.9837 top has resumed and extend weakness to 0.9669-70 (61.8% Fibonacci retracement of 0.9565-0.9837 and previous support) but previous support at 0.9642 should remain intact.

In view of this, we are holding on to our short position entered at 0.9755. Above said resistance at 0.9772 would defer but only break of resistance at 0.9808 would signal low is formed and indicate the pullback from 0.9837 has ended, bring retest of this level later.

Trade Idea Update: GBP/USD – Hold long entered at 1.3250

GBP/USD - 1.3287

Original strategy :

Bought at 1.3250, Target: 1.3350, Stop: 1.3245

Position : - Long at 1.3250

Target : - 1.3350

Stop : - 1.3245

New strategy :

Hold long entered at 1.3250, Target: 1.3350, Stop: 1.3245

Position : - Long at 1.3250

Target : - 1.3350

Stop : - 1.3245

As the British pound has eased after Friday’s brief rise to 1.3338, suggesting minor consolidation below this level would be seen, however, as long as 1.3245-50 holds, bullishness remains for the rise from 1.3027 low to bring a stronger retracement of recent decline, hence gain to 1.3345-50 and then 1.3375-80 (61.8% Fibonacci retracement of 1.3596-1.3027), however, overbought condition should limit upside to 1.3400-10, bring another retreat later.

In view of this, we are holding on to our long position entered at 1.3250. Below 1.3245 would defer and risk test of the Kijun-Sen (now at 1.3223), break there would defer and suggest top is formed, bring weakness to 1.3200, then towards 1.3175 but said support at 1.3121 should remain intact.

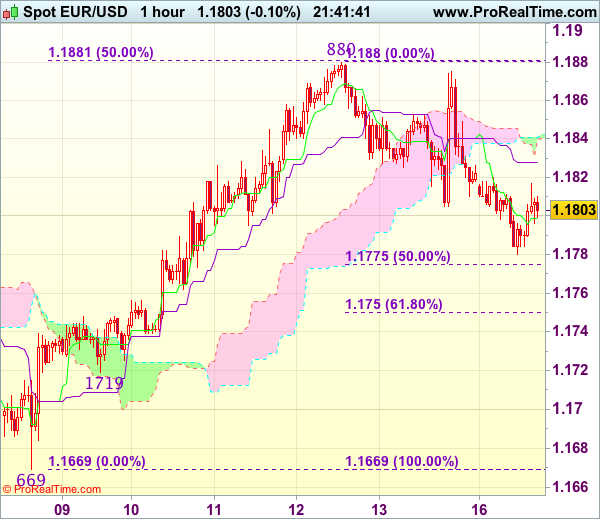

Trade Idea Update: EUR/USD – Stand aside

EUR/USD - 1.1803

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite Friday’s rebound to 1.1875, as the single currency has retreated after faltering below resistance at 1.1880, suggesting further consolidation below this last week’s high would be seen and pullback to 1.1775 (50% Fibonacci retracement of 1.1669-1.1880) cannot be rued out, however, reckon 1.1745-50 (61.8% Fibonacci retracement) would limit downside and bring rebound later.

On the upside, expect recovery to be limited to 1.1820-25 and 1.1850 should hold, bring another retreat later. Above 1.1850 would suggest the pullback from 1.1880 has ended and revive bullishness for retest of 1.1880, break there would confirm recent upmove from 1.1669 low has resumed for headway to 1.1895-00 (61.8% Fibonacci retracement of 1.2035-1.1669) first. As near term outlook is mixed, would be prudent to stand aside in the meantime.

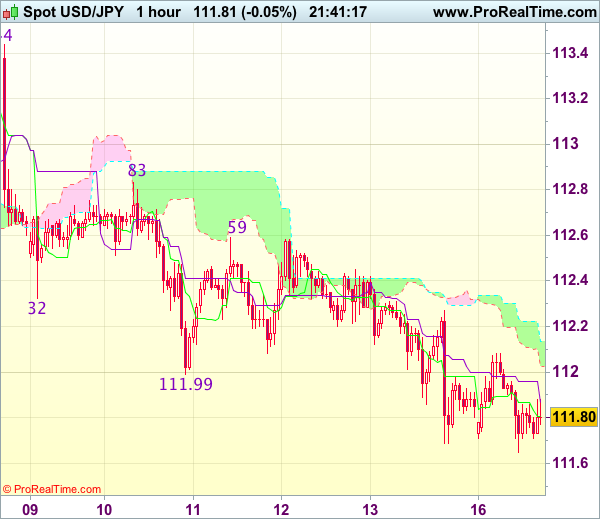

Trade Idea Update: USD/JPY – Hold short entered at 112.25

USD/JPY - 111.80

Original strategy :

Sold at 112.25, Target: 111.25, Stop: 112.25

Position : - Short at 112.25

Target : - 111.25

Stop : - 112.25

New strategy :

Hold short entered at 112.25, Target: 111.25, Stop: 112.25

Position : - Short at 112.25

Target : - 111.25

Stop : - 112.25

As dollar has remained under pressure after breaking below last week’s low at 111.99, adding credence to our bearishness and signaling the fall from 113.44 top is still in progress, hence downside bias remains for this move to extend weakness to 111.70 (100% projection of 113.44-112.32 measuring from 112.83), below there would bring subsequent decline to 111.47 support but oversold condition would limit downside and reckon 111.11 support would remain intact.

In view of this, we are holding on to our short position entered at 112.25. Only above resistance at 112.59 would abort and signal low is formed instead, risk a stronger rebound to indicated resistance level at 112.83.

Euro Pressured by Political Jitters

The Euro found itself vulnerable to losses on Monday morning, thanks to heightened political drama in Spain.

Jitters over the Catalan developments were felt across the board, after Prime Minister Mariano Rajoy gave Carles Puigdemont until 08:00 GMT to clarify Catalonia's independence status. Puigdemont simply ignored Madrid's ultimatum, submitting a letter that failed to provide a clear indication on his response to the independence declaration last week. The Spanish government has given Catalan leaders until Thursday to officially declare independence, or back down.

Should Puigdemont officially declare independence, he may prompt Madrid to invoke Article 155 of the Spanish Constitution. Such a development is likely to intensify the political drama in Spain, and spark concerns over political instability in Europe that may ultimately punish the Euro.

Taking a look at the technical outlook, the EURUSD remains in a wide range on the daily charts, with 1.1850 acting as a level of interest. A decisive breakout above 1.1850 may encourage a further incline towards 1.1920. In an alternative scenario, weakness below 1.1850 may open a path back towards 1.1730.

Commodity spotlight – Gold

Gold extended gains during Monday's trading session, with prices venturing towards $1305 despite the Dollar stabilizing.

The yellow metal received a boost last Friday, after soft inflation figures from the United States in September clouded prospects of higher US interest rates in 2018. With political risk in Spain, and geopolitical tensions concerning Iran and North Korea still supporting some flight to safety, the yellow metal could find support in the short term. From a technical standpoint, Gold has broken above the $1300 psychological level, which may encourage a further incline towards $1315 and $1320, respectively. If prices fail to stay above $1300, this should encourage a decline back towards $1280.

GBPUSD Hesitates Below Key Resistance Zone

GBP/USD: The pair continues to see price hesitation below its key resistance at 1.3337 level. However, while that resistance remains unbroken, we could see the pair weaken. Support lies at the 1.3250 level where a break will turn attention to the 1.3200 level. Further down, support lies at the 1.3100 level. Below here will set the stage for more weakness towards the 1.3050 level. Conversely, resistance stands at the 1.3250 levels with a turn above here allowing more strength to build up towards the 1.3300 level. Further out, resistance resides at the 1.3350 level followed by the 1.3400 level. On the whole, GBPUSD continues to face further upside pressure but with caution.

Inflation Secular Stagnation

Friday's weak US CPI was a powerful reminder that central bankers have been wrong about inflation for a decade, and not just in the US. The pound was the top performer last week while the Canadian dollar lagged. CFTC positioning showed more specs selling the yen. A big week for GBP traders lies ahead. Friday's GBP Premium trade is already in the green.

On Friday, US September CPI rose 2.2% y/y compared to 2.3% expected, stripping out food and energy left prices up 1.7% compared to the 1.8% consensus. It was one of many inflation misses this year, expecially compounded by real average weekly earnings rising a paltry 0.6% compared to 1.0% expected.

IMF leaders were glowing last week about upbeat potential for global growth and central bankers everywhere believe it's only a matter of time until prices rise. If they don't, it will mean a complete re-think of how central banks operate.

The case against inflation is what many emerging markets are experiencing now. inflation is low virtually everywhere. Few emerging markets are generating runaway inflation.

China's economy continues to grow at a nearly 7% pace annually, but inflation is just 1.8% and has been below 3% for four years. Rare pockets of inflation like Russia have been due to currency shocks and have flattened shortly afterwards.

Looking ahead, the Party Congress in China is the main event in the week ahead, starting Wednesday. In an early hint of what people will be talking about, PBOC Gov Zhou warned that Chinese companies have taken on too much debt.

CFTC Commitments of Traders

Speculative net futures trader positions as of the close on Tuesday. Net short denoted by - long by +.

- EUR +91K vs +91K prior

- GBP +15K vs +20K prior

- JPY -101K vs -85K prior

- CHF –4.3K vs -3.2K prior

- CAD +76K vs +75K prior

- AUD +69K vs 72K prior

- NZD +6K vs +8K prior

The pound longs who hung in there after the beating over the past few weeks were rewarded with a big bounce last week. Overall the moves aren't large but if US 10-year yields can break above 2.40%, then expect an extreme short. A big week for GBP traders lies ahead. Further analysis on UK data and events follows after this IMT.