Sample Category Title

EUR/USD Mid-Day Outlook

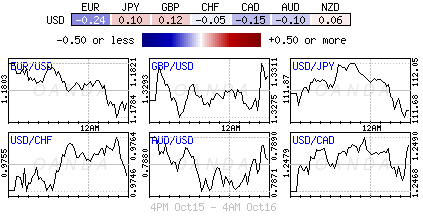

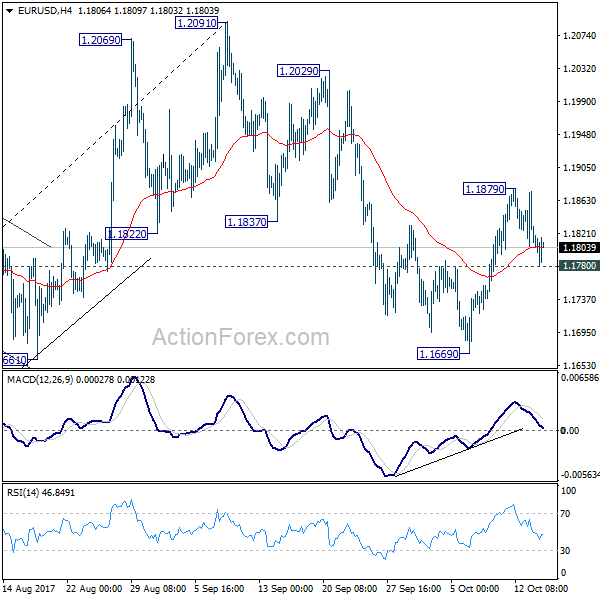

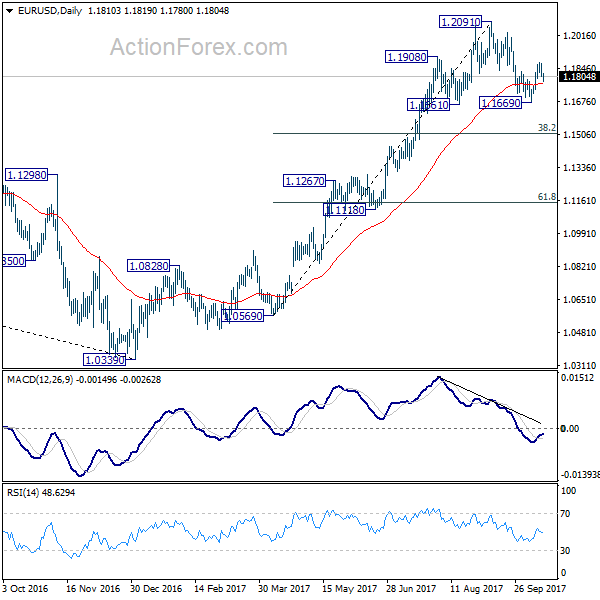

Daily Pivots: (S1) 1.1789; (P) 1.1832 (R1) 1.1860; More...

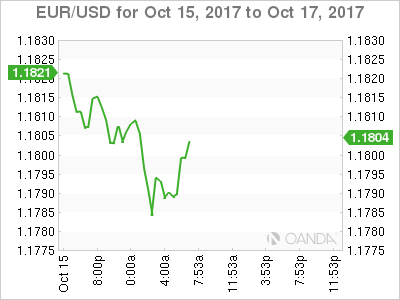

EUR/USD breaches 1.1787 minor support briefly but there is no follow through selling yet. Intraday bias stays neutral first. At this point, we're slightly favoring the case that pull back from 1.2091 has completed at 1.1669, ahead of 1.1661 support. Above 1.1879 will turn bias back to the upside for retesting 1.2091 high. However, break of 1.1780 will dampen this view. Intraday bias will be turned back to the downside through 1.1669 low. Correction from 1.2091 would then extend to 38.2% retracement of 1.0569 to 1.2091 at 1.1510 and completes there.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

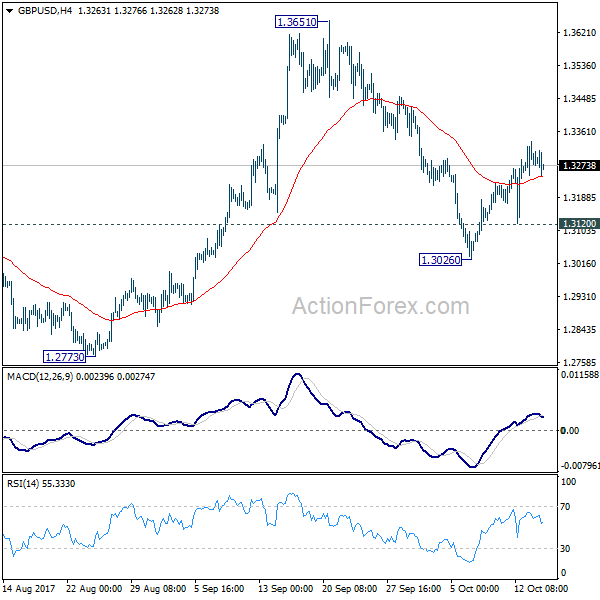

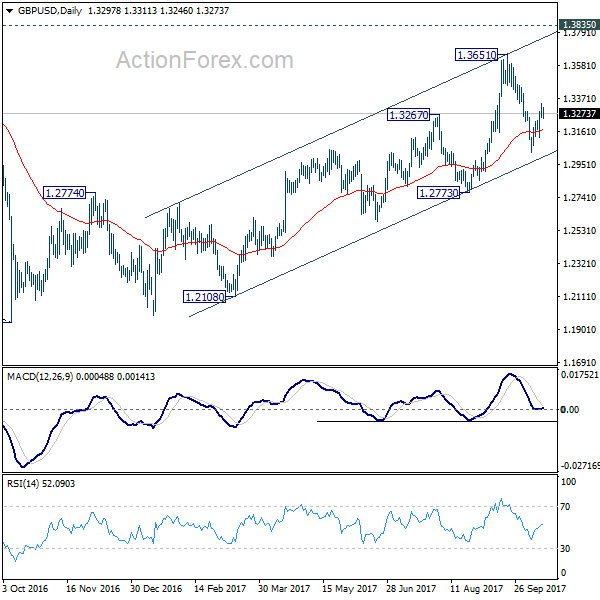

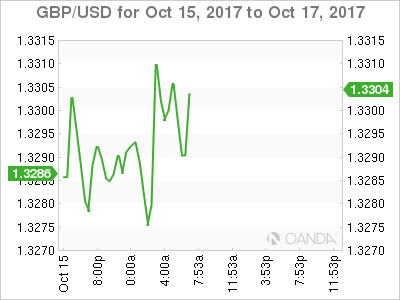

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3239; (P) 1.3288; (R1) 1.3331; More....

GBP/USD is losing some upside moment. But at this point, intraday bias stays mildly on the upside. Rebound from 1.3026 would target 1.3651 resistance. Break there will resume medium term rise from 1.1946 and target 1.3835 key resistance next. On the downside, below 1.3120 minor support will resume the fall from 1.3651 through 1.3026 instead.

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll turn neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

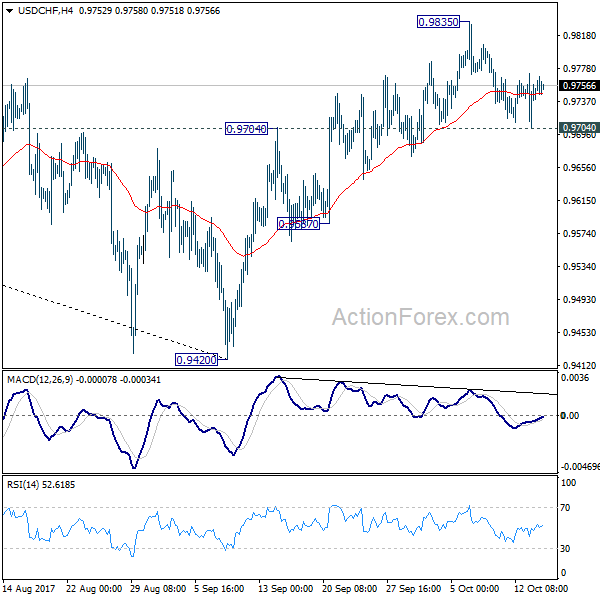

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9707; (P) 0.9739; (R1) 0.9774; More....

USD/CHF is still staying in range of 0.9704/9835 and intraday bias remains neutral first. As noted before, considering bearish divergence condition in 4 hour MACD, break of 0.9704 will argue that rebound from 0.9420 has completed. This will also mixed up the near term outlook and turn bias back to the downside for 0.9587 support. On the upside, break of 0.9835 will extend the rebound to 61.8% retracement of 1.0342 to 0.9420 at 0.9990.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could develop into a medium term move and target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9587 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

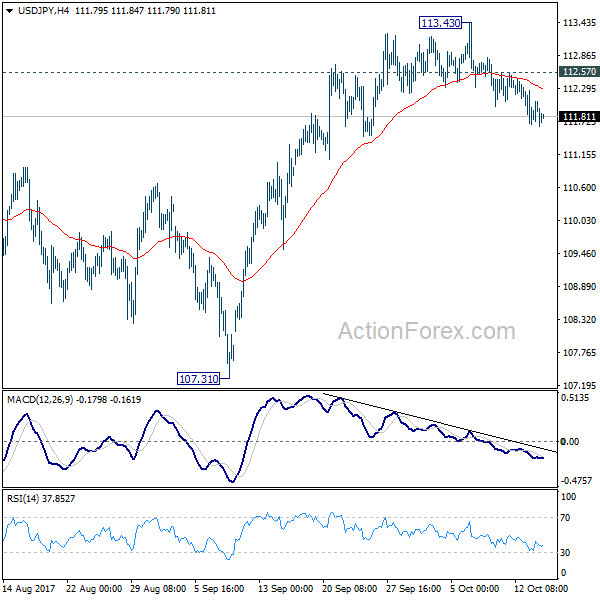

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.57; (P) 111.94; (R1) 112.19; More...

Intraday bias in USD/JPY stays on the downside at this point, as 112.57 minor resistance remains intact. 113.43 is seen as a short term top. Decline from there should target 55 day EMA (now at 111.37) first. As whole rebound from 107.31 is likely completed, sustained trading below 55 day EMA will target 107.31 low and below. In that case, we'd expect strong support from 61.8% retracement of 98.97 to 118.65 at 106.48 to contain downside and bring rebound. On the upside, above 112.57 minor resistance will turn intraday bias neutral first. But risk will stays on the downside as long as 113.43 resistance holds.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

Dollar Mixed Despite Upbeat Data and Fedspeaks

Dollar is trading mixed in spite of up beat US economic data and hawkish Fedspeaks. Empire state manufacturing index jumped to 30.2 in October, up from 24.4 and beat expectation of 20.7. That's also the highest level in three years. Boston Fed President Eric Rosengren sounded rather hawkish in an interview. He mentioned that Fed will need to hike interest rate December, and then three to four times "over the course of next year". He pointed out that unemployment rate, current at 4.2%, could drop below 4% when the economy is overheating. And in that case, Fed "might have to overshoot" interest rate to a level higher than expected in a healthy economy.

Over the weekend, Fed Chair Janet Yellen sounded quite upbeat on the economy. Yellen noted that "economic activity in the United States has been growing moderately so far this year, and the labor market has continued to strengthen." Impact of the hurricanes were "quite noticeable in the short term". But she emphasized that "history suggests that the longer-term effects will be modest and that aggregate economic activity will recover quickly."

Euro softer on some political risks

Euro is trading generally softer, except against Aussie and Canadian. Catalan leader Carles Puigdemont didn't clarify his position regarding independence as requested by Spanish Prime Minister Mariano Rajoy. Instead, Puigdemont requested two months of communications over the status. Puigdemont emphasized that "the suspension on our side of the results that come out of the vote on 1 Oct, shows our firm commitment to find a solution, and avoid confrontation." However, Spain's Deputy Prime Minister Soraya Sáenz de Santamaría criticized that Puigdemont haven't made his position clear. And he offered Puigdemont an ultimatum to give a formal confirmation on independence or not by Thursday morning.

In Germany, Social Democrats defeated Chancellor Angela Merkel's Christian Democrats in an election in the northern state of Lower Saxony on Sunday. That is seen as a blow to Merkel as she's in preparation for coalition talks this week. The task is known to be difficult as her coalition partner of Afd and Greens are standing on different side of the spectrum. While Merkel acknowledged it, she tried to sound optimistic and said that "unusual combinations can of course bring the opportunity to find some solutions to things that had seemed unsolvable until now."

Released from Eurozone, trade surplus widened to EUR 21.6b in August. German WPI rose 0.6% mom in September.

Sterling firm as May meets Juncker

Sterling continues to trade as the strongest one for the week. Markets are keenly await inflation, employment and retail sales data. UK Prime Minster Theresa May will have a dinner with EU leaders in Brussels today, trying to rescue the Brexit negotiations. That include EU Commission President Jean-Claude Juncker and chief Brexit negotiator Michel Barnier. It came days after EU officials said the talks were deadlocked, as conclusion to the fifth round. It's believed that May would try to persuade the EU counter parts to start the talks on post-Brexit trade agreements. But so far, nothing is know about what May could offer in return. And it's clear that the EU side sees there isn't "sufficient progress" to move on, with key issues like the divorce bill unresolved.

Released from UK, Rightmove house prices rose 1.1%% mom in October.

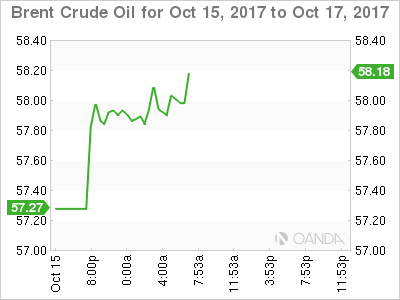

Oil surged on Iran concerns, But CAD lags

Oil price surged today as geopolitical tensions have heightened concerns over Middle East exports. The Iraqi government has sent forces to the northeastern Kurdish region, trying to take control of the oil fields there. It is estimated that the conflict would cut the exports in the area by -75% to 0.15M bpd. Meanwhile, US President Donald Trump refused to certify the Iran has been complying with the nuclear deal. His plan to impose new sanctions against Iran is doomed to affect oil output there.

However, French President Emmanuel Macron has criticized Trump's threat to of tearing up the Iranian deal, while the EU has indicated that the US has no right to terminate the deal. China has also expressed the hope of keeping the deal in place. If the US were the only country that imposes new sanctions against Iran, the actual impacts on the oil market would be limited. Indeed, the major destinations of Iran's oil are European countries, China and India.

Canadian dollar, however, shows no reaction to oil price and trades broadly lower. Released from Canada, international securities transactions dropped to CAD 9.85b in August.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.57; (P) 111.94; (R1) 112.19; More...

Intraday bias in USD/JPY stays on the downside at this point, as 112.57 minor resistance remains intact. 113.43 is seen as a short term top. Decline from there should target 55 day EMA (now at 111.37) first. As whole rebound from 107.31 is likely completed, sustained trading below 55 day EMA will target 107.31 low and below. In that case, we'd expect strong support from 61.8% retracement of 98.97 to 118.65 at 106.48 to contain downside and bring rebound. On the upside, above 112.57 minor resistance will turn intraday bias neutral first. But risk will stays on the downside as long as 113.43 resistance holds.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | Rightmove House Prices M/M Oct | 1.10% | -1.20% | ||

| 01:30 | CNY | CPI Y/Y Sep | 1.60% | 1.60% | 1.80% | |

| 01:30 | CNY | PPI Y/Y Sep | 6.90% | 6.40% | 6.30% | |

| 04:30 | JPY | Industrial Production M/M Aug F | 2.00% | 2.10% | 2.10% | |

| 06:00 | EUR | German WPI M/M Sep | 0.60% | 0.40% | 0.30% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Aug | 21.6B | 20.2B | 18.6B | 17.9B |

| 12:30 | CAD | International Securities Transactions (CAD) Aug | 9.85B | 20.05B | 23.95B | |

| 12:30 | USD | Empire State Manufacturing Index Oct | 30.2 | 20.7 | 24.4 | |

| 14:30 | CAD | BOC Business Outlook Survey |

DAX Ticks Higher as German Inflation Report Beats Estimate

The DAX has posted small gains in the Monday session. Currently, the index is at 13,013.50, up 0.17% on the day. On the release front, eurozone data was positive. German Wholesale Price Index gained 0.6%, above the forecast of 0.4%. The eurozone trade surplus jumped to EUR 21.6 billion, above the estimate of EUR 20.3 billion. On Tuesday, Germany releases ZEW Economic Sentiment and the eurozone will publish Final CPI.

Last week, ECB President Mario Draghi appeared to pour cold water on hopes that the ECB would raise interest rates in the near future. Draghi stated that he plans to maintain ultra-low rates "well past" the end of its bond-buying program in December. The ECB has been under pressure to tighten monetary policy, primarily from Germany, where the central bank has called for tighter policy, given the stronger eurozone economy. The ECB is expected to taper its monthly bond purchases of 60 billion euros at the October policy meeting, but Draghi has sent out a clear message that rate hikes will have to wait until 2018. With inflation levels will below the ECB target of around 2 percent, Draghi has been reluctant to raise interest rates until inflation shows clear signs of moving upwards.

The crisis in Catalonia continues this week, with no resolution in sight. Last week, the Spanish government set a Monday deadline for Catalan President Carles Puigdemont to expressly state whether he had declared independence, and if so, Puigemont was given three more days to retract his proclamation. However, the Catalan President shirked away from a clear answer and let the first deadline pass, calling for more dialogue with Madrid. Prime Minister Mariano Rajoy has threatened to suspend the Catalan parliament and impose direct rule from Madrid, which could trigger a violent response. The crisis has led 500 companies to start leaving Catalonia, and the Standard and Poor's rating agency has said that the region could face a recession if the crisis continues.

USDJPY Tests 200 Week MA

The U.S dollar has fallen below key support against the Japanese Yen, hitting 111.66, as technical selling intensifies after the USDJPY pair broke below the lower-end of its recent trading range.

Intraday trading sentiment surrounding the USDJPY pair is currently bearish, with further declines likely whilst price-action continues to trade below the 111.98 level.

On Friday, the USDJPY declined after softer than expected U.S CPI figures, with price reaching 111.68. Price-action continues to suggest further losses, as the pair prints bearish lower daily time-frame candles.

Going forward, traders will look for multiple daily price-closes beneath the pairs 200-week moving average, at 111.79, and the pairs 200-day moving average, located at the 111.40 level.

Key technical support for USDJPY pair is located at 111.79 and 111.66. Further support is found at 111.40, and the pairs monthly pivot point, at 111.03.

To the upside, key intraday resistance is found at 111.98 and the pairs weekly pivot point, at 112.12. Further technical resistance is found at the pairs weekly pivot point, at 112.31, and the former swing high, at 112.57.

EURUSD Selling Limited Below 1.1790

The euro has fallen against the U.S dollar during today's European session, reaching an intraday low of 1.1780, as tensions between Spanish authorities and the Catalan government intensify.

Moving into the U.S session, the trading sentiment surrounding the EURUSD pair is mixed. Despite political woes in Spain, intraday sellers failed to close the last H4 candle below the key 1.1790 support level. Euro buyers are now starting to push price-action back above the 1.1800 handle.

Moving into the U.S session, we see the release of the New York manufacturing index, which is expected to come in worse than the previous month, and may affect the U.S dollar index.

Daily price closes below the 1.1790 level will be considered bearish, whilst any daily price closes above the 1.1845 level will be taken as bullish.

Key intraday EURUSD technical resistance is currently found at 1.1790 and 1.1770. A further decline below the 1.1770 level should lead to a deeper sell-off towards 1.1740 and 1.1710.

To the upside, key resistance is found at 1.1800, and the weekly pivot point, at 1.1807. Above the 1.1807 level, further resistance is found at 1.1825, 1.1845 and 1.1879.

Elliott Wave Analysis: Potential Triangle On GBPNZD Points Higher

GBPNZD is trading in a potential complex correction as part of wave iv). We see a possible contracting triangle correction in the making, with four sub-waves already unfolded. Current intra-day move can now be final sub-wave e of iv), that can search for a base near the lower triangle line and later make a new five-wave recovery higher, into wave v)

GBPNZD, 4H

Politics Pressures The EUR

Monday October 16: Five things the markets are talking about

The EUR has slipped in early Monday trading after posting its biggest weekly gain in four-weeks as political uncertainty in the form of an approaching deadline over Catalonia's bid for independence and Austria's Sunday election outcome has convinced many to book some profits.

Later this morning, Catalan leader Carles Puigdemont is expected to clarify whether he is calling for the region's independence from Spain, with Madrid threatening a return to direct rule if his stance remains ambiguous.

In Austria, the young conservative leader Sebastian Kurz is on track to become the country's next leader after Sunday's election – He will likely seek a coalition with the resurgent far right as his party is well short of a majority.

However, the euro's losses have been somewhat limited due to a muted U.S dollar as subdued inflation data again raises market expectations that the Fed may not convey a ‘hawkish' tone at next weeks policy meeting. Friday's U.S inflation data suggested that the U.S's underlying inflation remains muted.

There are no central bank meetings this week, but the Fed will publish its Beige book Thursday (Oct 18).

In the U.K, it is a big data week with both the consumer and producer price indexes (Oct 17), retail sales and labor market data (Oct 19) due to be released.

This week is also a big one for China with the release of last nights September consumer and producer prices along with its Q3 GDP report (Oct 19) and last month's industrial production and retail sales data (Oct 18).

Note: China's 19th party congress begins on Wednesday Oct. 18 in China. Next Sunday (Oct. 22), Japan will hold an election for the lower house of the Diet.

1. Stocks are give the green light

In Japan, equities continue to find no reason to fall, with the Nikkei (+0.5%) printing its first ten-session win streak in over two years overnight. The prospects of an Abe election win later this month continues to attract buyers. The broader Topix gained +0.9%.

In Hong Kong, stocks rallied to a ten-year high overnight, joining a regional stock rally, which have been boosted by a surprisingly rosy growth forecast for China. The Hang Seng index rose +0.8%, while the China Enterprises Index gained +0.7%.

In contrast, Chinas share indexes fell as a surprisingly strong People's Bank of China (PBoC) economic growth projection failed to support the market. Governor Zhou indicated that China was expected to grow +7%in Q2 and defy widespread expectations for a slowdown. The blue-chip CSI300 index fell -0.2%, while the Shanghai Composite Index lost -0.4%.

In Europe, regional bourses are trading mostly higher with the exception of the Spanish IBEX, which continues to be weighed down on uncertainty over Catalonia independence.

U.S stocks are set to open unchanged.

Indices: Stoxx600 +0.20% at 392.2, FTSE +0.2% at 7546, DAX +0.20% at 13018, CAC-40 +0.3% at 5366, IBEX-35 -0.5% at 10203, FTSE MIB +0.1% at 22436, SMI -0.1% at 9305, S&P 500 Futures flat

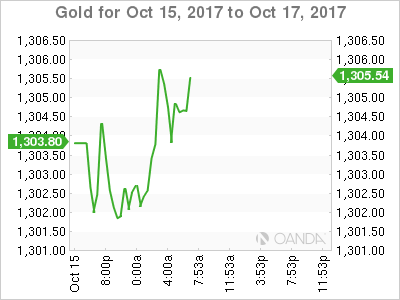

2. Oil rises as fighting escalates in Iraq, gold higher

Oil markets are well supported this morning as Iraqi forces entered the oil city of Kirkuk, taking territory from Kurdish fighters and raising concerns over exports from OPEC's second-largest producer.

Iraq launched the operation in the region yesterday as the crisis between Baghdad and the Kurdish Regional Government (KRG) escalated. Tensions have been building since the KRG voted for independence in late September.

Brent crude futures are at +$57.75 per barrel, up +58c from Friday's close, while U.S. WTI crude is at +$51.95 per barrel, up +50c.

Note: Kirkuk accounts for +200k bpd of the some +600k bpd of oil produced in the KRG region.

Prices are also being supported by market worries over renewed U.S sanctions against Iran.

Gold is trading atop of the psychological +$1,307 an ounce, buoyed by worries geopolitical risks, including the ongoing tensions over Iran and North Korea. Friday's weaker-than-expected U.S. inflation print helped push U.S Treasury yields lower, giving a boost to gold to trade above +$1,300.

3. Yields tug of war

Fixed income traders are stuck between Fed rhetoric and global growth on one hand and the ECB's expected action and subdued inflation on the other. Growth and the Fed point to higher yields, while inflation and the ECB should at least keep yields at current levels.

The Fed is expected to raise rates in December (Fed funds are pricing in odds of +90%), while ECB members contemplate a softer-than-expected reduction in asset purchases. The latest estimate is to reduce monthly bond purchases to+€40B per month and carry that out for six-months, to maintain maximum flexibility. The possibility of a longer-than-expected extension of +12-months for the ECB's QE program caused yields to tumble Friday. German 10-year Bund yields are trading at +0.4% – their lowest level since late September.

The bond market is growing to the idea that the ECB will start withdrawing asset purchases, most likely in January and expect the ECB to announce some details next week (Oct 26).

Elsewhere, the yield on 10-year Treasuries gained +2 bps to +2.29%, while the U.K's 10-year gilt increased +1 bps to +0.41%.

4. Dollar finds a foothold

Ahead of the U.S open, the EUR (€1.1788) trades under pressure after yesterday's Austrian elections, which are likely to result in a coalition led by the People's Party, which wants tougher rules on immigration, and the far-right Freedom Party. EUR/GBP has fallen -0.3% to €0.8866. There are also concerns about Catalonia after President Puigdemont has yet to clarify whether he declared the region independent, raising the prospect of reprisals from Madrid. Market focus will also be looking ahead to next week ECB decision see if Euro policy makers will announce the bulk of its decisions on QE tapering.

Sterling (£1.3297) is a tad higher on reports that PM May is planning to meet with E.U officials in Brussels in the hope of ending the Brexit stalemate. EUR/GBP is at €0.8867.

5. Euro-area exports jump

Data this morning showed that Eurozone exports rose +2.5% in August from July, leading to a widening of the seasonally adjusted trade surplus to+€21.6B vs. +€17.9B.

This strong print is go some ways to reassure ECB policy makers that the EUR's appreciation this year has not been capable to pressure the region's economic recovery, which should provide further ammunition to decide to scale back their bond purchases at next week's ECB meeting (Oct. 26).