Sample Category Title

Market Update – Asian Session: Nikkei On Track For 11th Day Of Gains, NZ Inflation Comes In Hotter Than...

Asia Summary

Asian equity markets have opened generally higher, tracking the gains seen during the US session. These opening gains had put the Nikkei 225 on track for its 11th straight gain, while the Topix index was heading towards its 7th straight advance.

Markets in Japan have since pared gains. Shares of Softbank have underperformed and mixed trading in the Japanese banking sector.

At the same time, shares of Kobe Steel have traded higher, after the over 40% losses seen during the prior week amid the company’s data falsification issue. The company is said to have told analysts that it is not having any current funding issues and that it plans to release its corporate earnings, as scheduled, on Oct 30th, according to a Japanese Press report. Coupled with in the gains in Kobe Steel, the sector is moving broadly higher (Nippon Steel +1.5%, JFE +1.4%).

Australian energy companies are generally higher (Woodside Petroleum +0.7%, Santos +1%), following Mondays gain in oil prices. Rio Tinto’s shares have traded higher after its Q3 iron ore shipments beat estimates and it affirmed its full year shipment guidance. Fellow iron-ore miner, BHP, is due to release its quarterly production report on Oct 18th.

In South Korea, video game companies are moving higher. A Chinese official is said to have noted that the government will do its best to lift restrictions related to various types of Korean media.

In China, the small-cap ChiNext index has extended losses after the over 2% decline seen on Monday’s session, with the Oct 18th start of the Communist Party Congress in focus.

Thus far China’s 10-year bond yield has risen again on today’s session, after rising over 2bps on Monday’s session. An economist from the China State Information Center (think tank) said the government should tighten monetary policy, as the room for policy loosening is seen as limited in 2018.

There has been little initial reaction in the bond market following the release of the Reserve Bank of Australia’s Oct policy meeting minutes. Of note the October policy meeting was held on Oct 3rd, which was ahead of the weaker than expected Aug retail sales data which was released on Oct 5th (AUSTRALIA AUG RETAIL SALES M/M: -0.6% V +0.3%E). Looking ahead, the Australia Sept employment change data is due to be released on Thursday Oct 19th.

In New Zealand, the Kiwi initially gained following the above forecast Q3 CPI data. However, the currency has since pared gains. Inflation is still within the RBNZ’s 1-3% target range and a rate hike is not fully priced in until Nov of 2018. Besides this, the government formation talks in New Zealand continue to linger.

Looking ahead to the US session, corporate earnings are starting to pick up with results expected out of companies including Goldman Sachs, Morgan Stanley, Harley Davidson and J&J. UnitedHealth earlier reported better than expected Q3 earnings and in line revenues. Additionally, the company raised its FY17 EPS forecast.

Key economic data

(NZ) NEW ZEALAND Q3 CPI Q/Q: 0.5% V 0.4%E; Y/Y: 1.9% V 1.8%E

(SG) SINGAPORE SEPT NON-OIL DOMESTIC EXPORTS M/M: -11.0% V -2.2%E; Y/Y: -1.1% V 12.7%E;ELECTRONIC EXPORTS Y/Y: -7.9% V 15.0%E

(AU) Australia Sept New Motor Vehicle Sales m/m: -0.5% v 0.0% prior; y/y: -0.8% v 1.7% prior

(NZ) New Zealand RBNZ Q3 Sectoral Factor Model Inflation Index y/y: 1.4% v 1.4% prior

Speakers and Press

Japan

(JP) Japan and US reach agreement to boost cooperation on infrastructure development, financing, maintenance and transport technology - press

(JP) Japan Government Official: No discussion of FX at meetings between US and Japan officials

Korea

(KR) US North Korean envoy Joseph Yun reportedly to travel to Seoul this week – Axios

(KR) North Korea govt reportedly rejects any diplomacy with United States at this point - CNN

China

(CN) State Information Center Economist Zhu Baoliang: China should tighten monetary policy and strengthen property controls - Chinese press

(CN) S&P Comments: China is running unconventional monetary policy

Australia/New Zealand

(AU) RESERVE BANK OF AUSTRALIA (RBA) MEETING MINUTES OCT 3RD: Any rate changes would be dependent on domestic economy; Appreciation in A$ expected to contribute to subdued pricing pressures

(AU) RBA Assistant Gov Ellis (economic): Starting to see spillover effect from public infrastructure spending on non-mining private sector

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.2%, Hang Seng +0.1%; Shanghai Composite +0.1%; ASX200 +0.8%, Kospi +0.2%

Equity Futures: S&P500 -0.0%; Nasdaq100 +0.0%, Dax +0.1%; FTSE100 -0.0%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1797-1.1775; JPY 112.31-112.04; AUD 0.7857-0.7835;NZD 0.7198-0.7163

Dec Gold -0.6% at $1,295/oz; Nov Crude Oil -0.1% at $51.80/brl; Dec Copper -0.3% at $3.23/lb

(CN) China PBOC injects CNY190B in combined 7-day and 14-day reverse repos v CNY20B in 7-day prior

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.5883 V 6.5839 PRIOR

(JP) Japan MoF sells ¥800.1B in 0.6% (prior 0.6%) 2-yr JGBs; avg yield 0.5900% v 0.5600% prior; bid-to-cover 4.05x v 4.15x prior

(AU) Australia MoF sells A$2.1B in 3% 2047 bonds, yield 3.565%

Equities notable movers

Australia/New Zealand

RIO.AU Reports Q3 Pilbara iron ore production 85.0Mt (100% basis), 83.2Mt y/y; shipments 85.8Mt (100% basis) v 85.2Mte v 80.9Mt y/y; +1.4%

ANZ.AU IOOF to acquire One path pension business for A$975M cash; IOOF has also entered into a 20 year Strategic Alliance Agreement with ANZ

OSH.AU Reports Q3 Rev $380.8M v $332.5M q/q; production 7.91 MMBOE (record high) v 7.2 q/q; +0.8%

CIA.AU Completes series of previously announced financing arrangements raising C$300M; +15%

Japan

5406.JP Told investors that it is not having funding issues at the current time - Japanese Press; +6%

US/Canada

BBD.B.CA Airbus to acquire majority stake in the C Series Aircraft Limited Partnership; +1.3% after hours

UNH Reports Q3 $2.66 adj v $2.58e, Rev $50.3B v $50.3Be, Raises FY17 $10.00 adj v $9.88e (prior $9.75-9.90); +0.7%

Elliott Wave View: AUDUSD Short Term

AUDUSD Short term Elliott Wave analysis suggests decline to 0.7731 ended Primary wave ((W)) on 10/6 low. Bounce in Primary wave ((X)) is proposed to be unfolding as a double three Elliott Wave structure. Intermediate wave (W) of ((X)) ended at 0.7897 and Intermediate wave (X) of ((X)) pullback is in progress as a zigzag Elliott Wave structure. Down from 0.7897 high, Minor wave A is proposed complete at 0.7832. While Minor wave B bounce stays below 0.7897, pair should turn lower in Minor wave C of (X) to correct cycle from 10/6 low. Afterwards, as far as pivot at 10/6 low (0.7731) stays intact, expect pair to resume higher.

AUDUSD 1 Hour Elliott Wave Chart

Double three ( 7 swings) is the most important pattern in Elliott wave’s new theory. It is also probably the most common pattern in the market these days. Double three is also known as a 7-swing structure. It is a very reliable pattern that gives traders a good opportunity to trade with a well-defined level of risk and target areas. The image below shows what Elliott Wave Double Three looks like. It has labels (W), (X), (Y) and an internal structure of 3-3-3. This means that all 3 legs has corrective sequences. Each (W) and (Y) is formed by 3 wave oscillations and has a structure of A, B, C or W, X, Y of smaller degrees.

RBA Shrugged Off Global Normalization Trend, Maintaining Neutral Stance

The RBA minutes for the October meeting reaffirmed the market that the central bank is in no hurry to increase interest rates. Policymakers stressed that rate hikes, or other kinds of monetary policy normalization, in other major economies do not necessarily imply that the RBA would follow suit anytime soon. The RBA remained upbeat in the domestic economic outlook, staying confident in the employment market conditions. Yet, it was still weary of subdued inflation. As usual, the central bank continued to warn of the strength in Australian dollar.

Notwithstanding rate hikes by other major central banks, including the Fed, BOC and BOE (likely in November), the RBA affirmed that its monetary policy would not be affected by others. As suggested in the minutes, the RBA acknowledged that 'a number of major central banks had either started to reduce the degree of monetary stimulus or were considering doing so' and 'that moves towards higher interest rates in other economies were a welcome development'. However, it emphasized that those moves 'did not have mechanical implications for the setting of policy in Australia, where the timing of any changes in interest rates would be dependent, as always, on developments in domestic economic conditions'.

The members were confident over the employment market situation, noting that 'both full-time and part-time employment had recorded solid growth in August'. Such growth had been 'well above that required to absorb increases in the labour force owing to population growth'. They expected the strength in employment growth to support household spending in the period ahead, although wage growth remained subdue.

Policymakers remained concerned about the inflation outlook as 'recent data had pointed to subdued price pressures across the economy in the June quarter'. Going forward, they projected retail electricity prices 'to increase significantly in the September quarter' while 'liaison with businesses had suggested that a number of firms, particularly in the retail and manufacturing sectors, were largely absorbing increases in energy costs into margins rather than passing them through to final prices'. Aussie’s pullback during the intermeeting period has made the members less concerned about currency appreciation. Yet, they still mildly warned that 'a material further appreciation of the exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast'.

Besides weak inflation, the less severe increase in property prices has also diminished the urgency of a rate hike. The minutes suggested that 'established housing market conditions had continued to ease in Sydney and Melbourne, but had been broadly unchanged in other cities. This pattern was evident in revised housing price data released by CoreLogic in September, as well as in auction clearance rates. Housing prices had continued to decline gradually in Perth. Nationwide measures of housing prices had increased by around +9% over the year to September'. The RBA likely believes that low interest rates have been less stimulative to properties prices with the help of macro-prudential measures. Should the economic growth continues to evolve as the central bank expected, the policy rate would probably stay unchanged at least until 2H18.

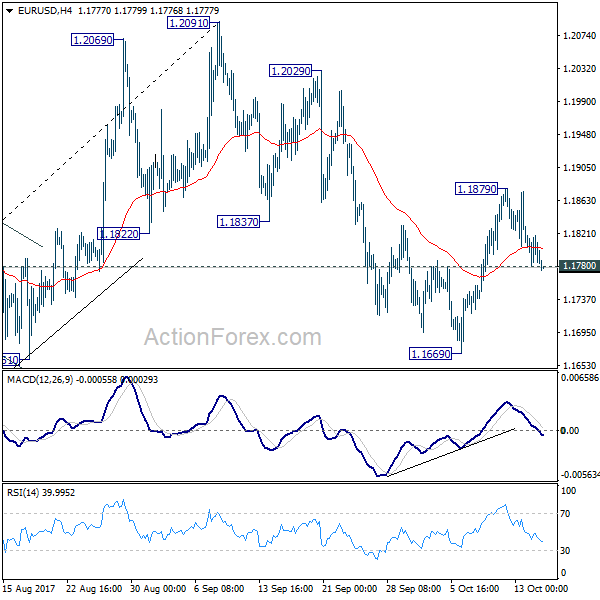

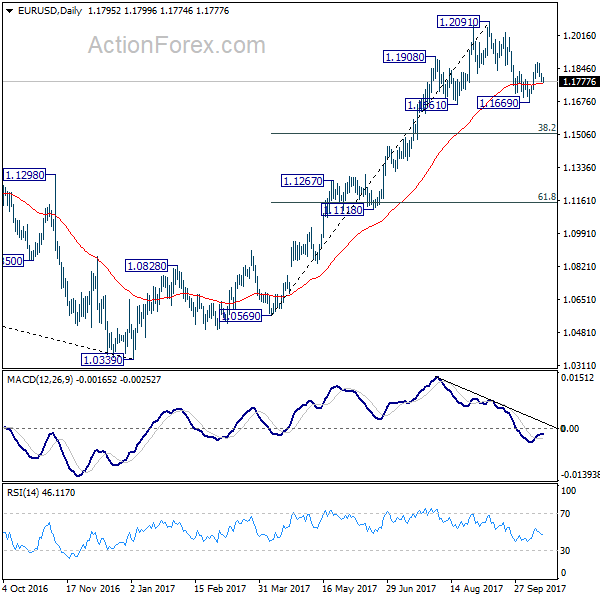

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1777; (P) 1.1799 (R1) 1.1817; More...

The break of 1.1780 minor support argues that rebound from 1.1669 is completed. Also, correction from 1.2091 is still in progress. Intraday bias is turned back tot he downside for 1.1669 first. Break will target 38.2% retracement of 1.0569 to 1.2091 at 1.1510. Strong support is expected there to complete the correction. On the upside, above 1.1879 will turn bias back to the upside for retesting 1.2091 high.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

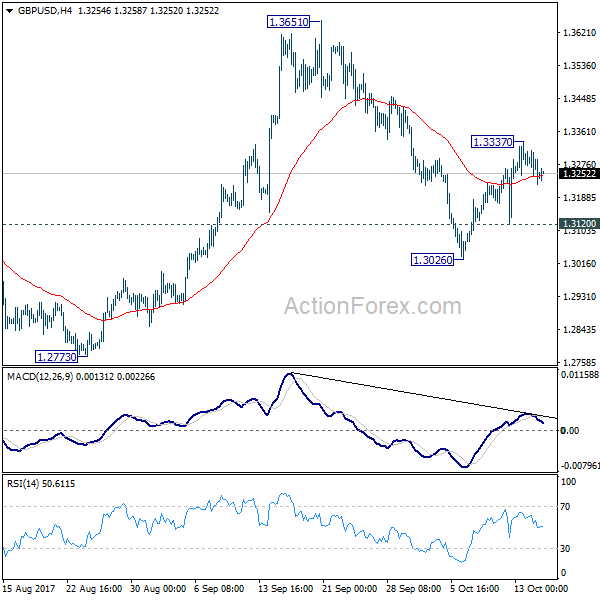

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3212; (P) 1.3261; (R1) 1.3299; More....

A temporary top is in place at 1.3337 in GBP/USD and intraday bias is turned neutral first. Another rise is mildly in favor as long as 1.3120 minor support holds. Above 1.3337 will target a test on 1.3651 high. Break there will resume medium term rise from 1.1946 and target 1.3835 key resistance next. On the downside, below 1.3120 minor support will resume the fall from 1.3651 through 1.3026 instead.

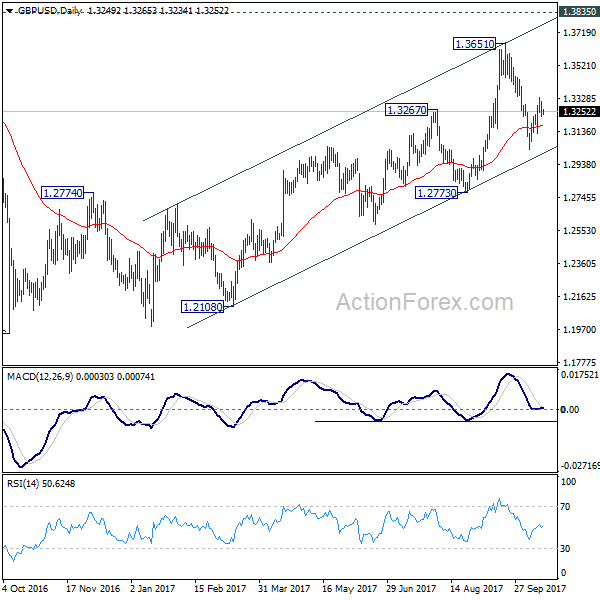

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we'll turn neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9732; (P) 0.9751; (R1) 0.9772; More....

USD/CHF is still staying in range of 0.9704/9835 and intraday bias remains neutral first. As noted before, considering bearish divergence condition in 4 hour MACD, break of 0.9704 will argue that rebound from 0.9420 has completed. This will also mixed up the near term outlook and turn bias back to the downside for 0.9587 support. On the upside, break of 0.9835 will extend the rebound to 61.8% retracement of 1.0342 to 0.9420 at 0.9990.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could develop into a medium term move and target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9587 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

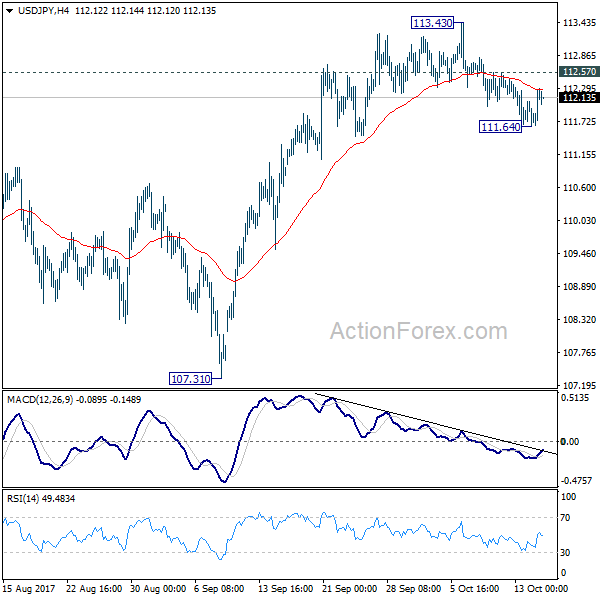

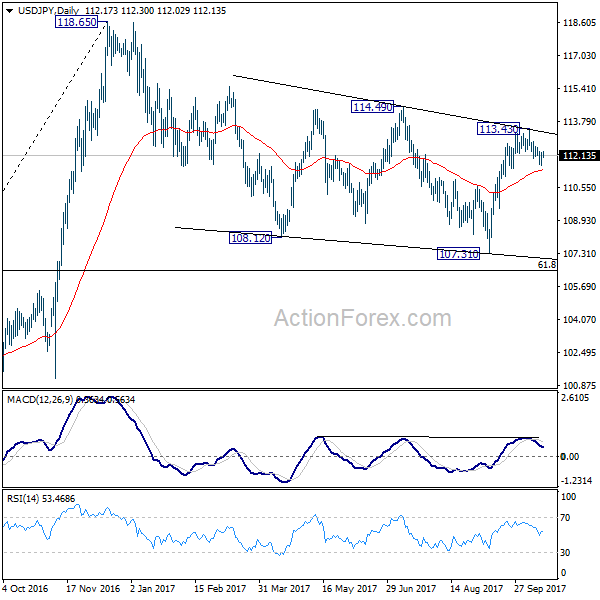

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.79; (P) 112.04; (R1) 112.42; More...

A temporary low is in place at 111.64 in USD/JPY and intraday bias is turned neutral first. Another decline is expected as long as 112.57 minor resistance holds. Below 111.64 will target 55 day EMA (now at 111.40) first. Sustained break there will target 107.31 and possibly below. Nonetheless, above 112.57 will bring retest of 113.43. Break there will resume whole rise from 107.31 for 114.49 key resistance.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

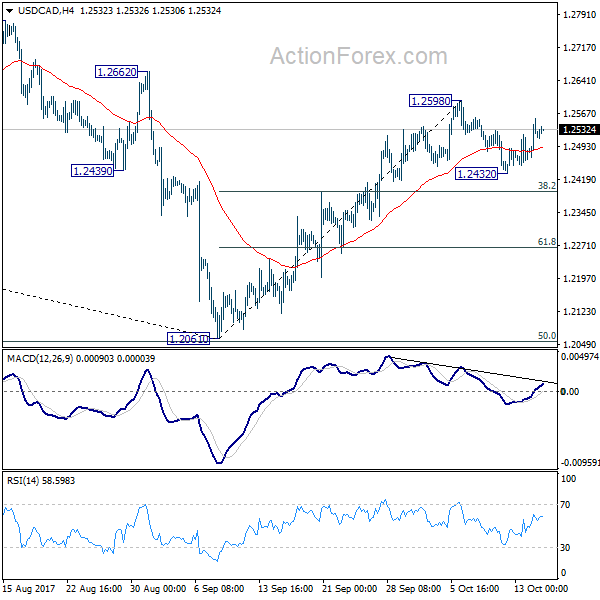

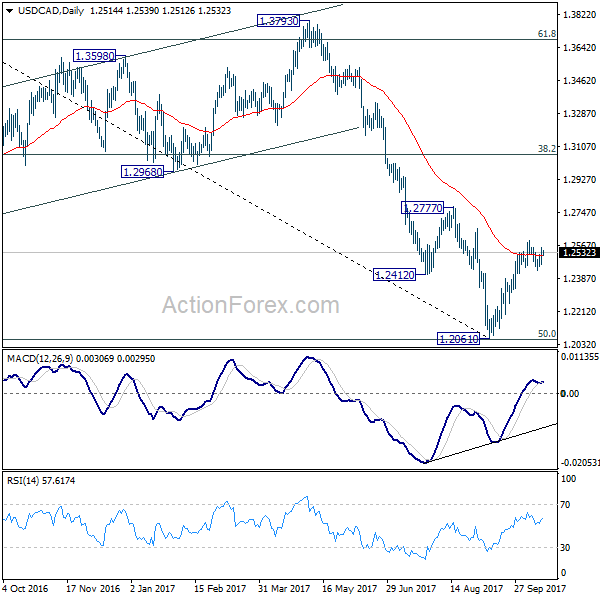

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2467; (P) 1.2512; (R1) 1.2563; More....

USD/CAD's recovery suggests that pull back from 1.2598 has completed at 1.2432 already. Intraday bias is turned back to retest 1.2598 first. Break will extend the rebound from 1.2061 to 1.2777 resistance next. In case the consolidation from 1.2598 extends with another fall, downside should be contained by 38.2% retracement of 1.2061 to 1.2598 at 1.2393 to bring rally resumption.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. And in that case, USD/CAD should target 1.3793 resistance next. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

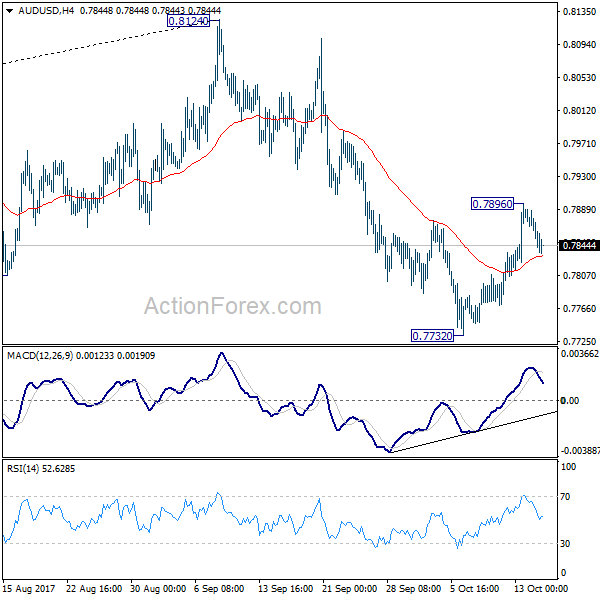

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7833; (P) 0.7861; (R1) 0.7879; More...

AUD/USD lost momentum after hitting 0.7896 and retreated. A temporary top was formed and intraday bias is turned neutral first. Another rise is mildly in favor for the moment. Break of 0.7896 will target a test on 0.8124 high. But we'd be cautious on strong resistance from there to limit upside and bring another fall to extend the corrective pattern. On the downside, break of 0.7732 will resume the decline from 0.8124 and target medium term fibonacci level at 0.7628 first.

In the bigger picture, rise from 0.6826 medium term bottom is seen as corrective pattern. Current development suggests that it might be completed with three waves up to 0.8124 already. Break of 38.2% retracement of 0.6826 to 0.8124 at 0.7628 will firm this bearish case. And, decisive break of 0.7328 key cluster support (61.8% retracement at 0.7322) will confirm and bring retest of 0.6826 low. In case rise from 0.6826 resumes and extends, strong resistance should be seen at 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside.

Australia Dollar Mildly Lower after RBA Minutes, British Pound Firm ahead of CPI

Dollar trades mildly higher this week even though momentum is relatively week. US equities extended the record runs, with DOW, S&P 500 and NASDAQ closing at new records overnight. Treasury yields also recovered mildly. But there is little support to the greenback yet. The forex markets are generally mixed in consolidative mode, except that some extra weakness is seen in Euro, due to political jitters. Meanwhile, Australia Dollar is trading a touch softer after RBA minutes. Sterling, on the other hand, is firm as markets await inflation data from UK.

RBA minutes give no sign of tightening soon

The minutes of RBA's October meeting showed that "the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time." The central bank acknowledged that "strengthening in global economic conditions had reduced some near-term risks to financial stability arising from rare or extreme events." But, it warned that "low interest rates and low financial market volatility had promoted financial risk-taking." Overall, there is practically no sign from RBA that indicates a rate hike soon. And considering sluggish wage growth that suggests plenty of spare capacity, RBA is no where near tightening. There are talks that RBA could stand pat throughout 2018.

NZ CPI beat expectations, but no change to RBNZ's stance

New Zealand CPI rose 0.5% qoq 1.9% yoy in Q3, up from prior 0.0% qoq 1.7% yoy, and beat expectation of 0.4% qoq 1.8% yoy. It's also well above RBNZ's own projection of 1.6% yoy. Still, it's believed that RBNZ won't change it's neutral stance on monetary policy. So far, there is little signs of overheating in the economy that points to higher inflation ahead. Instead, the economy could be entering a slowing phase.

Former EM Takenaka: Abe win will push the tide towards Kuroda

In Japan, former Economy Minister Heizo Takenaka hailed that BoJ Governor Haruhiko Kuroda has done an "excellent job" and "should continue" after his term expires next year. He pointed out that after Kuroda's massive stimulus policy, prices have stopped falling, and the economy is in better shape. And, according to Takenaka, a win for Prime Minister Shinzo Abe in the October 22 election will "of course push the tide" towards another term for Kuroda. He noted that "there is a sufficient amount of trust between the government and the BoJ for that to happen". Also, renewing Kuroda's term will raise expectations for appropriate policies but "a shift in personnel can change expectations at once".

May and Juncker agreed to accelerate Brexit negotiation

UK Prime Minister Theresa May and European Commission President Jean-Claude Juncker had a "constructive and friendly" dinner in Brussels yesterday. Coming out of the meeting, they said there was a "broad, constructive exchange on current European and global challenges". And in a joint statement regarding Brexit, they "reviewed the progress made in the Article 50 negotiations so far and agreed that these efforts should accelerate over the months to come." Separately, it's reported that despite brief objections by France and Germany, a revised draft circulated by European Council President Donald Tusk retains the option open for Brexit negotiations to move on to trade as soon as after December EU summit.

Looking ahead

UK inflation data will be the main focus of the day. CPI is expected to finally hit 3% mark in September, solidifying the case for a BoE rate hike in November. But it should be noted that, that rate hike would only bring interest rate back to pre-Brexit referendum level. And based on the current uncertainty around Brexit negotiations, there is little chance for BoE to start a tightening cycle. RPI and PPI will also be released from UK.

Elsewhere, German ZEW economy sentiment and Eurozone CPI final will be featured in European session. US will release import price index, industrial production and NAHB housing index later in the day.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7833; (P) 0.7861; (R1) 0.7879; More...

AUD/USD lost momentum after hitting 0.7896 and retreated. A temporary top was formed and intraday bias is turned neutral first. Another rise is mildly in favor for the moment. Break of 0.7896 will target a test on 0.8124 high. But we'd be cautious on strong resistance from there to limit upside and bring another fall to extend the corrective pattern. On the downside, break of 0.7732 will resume the decline from 0.8124 and target medium term fibonacci level at 0.7628 first.

In the bigger picture, rise from 0.6826 medium term bottom is seen as corrective pattern. Current development suggests that it might be completed with three waves up to 0.8124 already. Break of 38.2% retracement of 0.6826 to 0.8124 at 0.7628 will firm this bearish case. And, decisive break of 0.7328 key cluster support (61.8% retracement at 0.7322) will confirm and bring retest of 0.6826 low. In case rise from 0.6826 resumes and extends, strong resistance should be seen at 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q3 | 0.50% | 0.40% | 0.00% | |

| 0:30 | AUD | RBA Meeting Minutes Oct | ||||

| 8:30 | GBP | CPI M/M Sep | 0.30% | 0.60% | ||

| 8:30 | GBP | CPI Y/Y Sep | 3.00% | 2.90% | ||

| 8:30 | GBP | Core CPI Y/Y Sep | 2.70% | 2.70% | ||

| 8:30 | GBP | RPI M/M Sep | 0.30% | 0.70% | ||

| 8:30 | GBP | RPI Y/Y Sep | 4.00% | 3.90% | ||

| 8:30 | GBP | PPI Input M/M Sep | 1.20% | 1.60% | ||

| 8:30 | GBP | PPI Input Y/Y Sep | 8.20% | 7.60% | ||

| 8:30 | GBP | PPI Output M/M Sep | 0.20% | 0.40% | ||

| 8:30 | GBP | PPI Output Y/Y Sep | 3.30% | 3.40% | ||

| 8:30 | GBP | PPI Output Core M/M Sep | 0.10% | 0.20% | ||

| 8:30 | GBP | PPI Output Core Y/Y Sep | 2.60% | 2.50% | ||

| 8:30 | GBP | House Price Index Y/Y Aug | 5.40% | 5.10% | ||

| 9:00 | EUR | Eurozone CPI M/M Sep | 0.40% | 0.30% | ||

| 9:00 | EUR | Eurozone CPI Y/Y Sep F | 1.50% | 1.50% | ||

| 9:00 | EUR | Eurozone CPI - Core Y/Y Sep F | 1.10% | 1.10% | ||

| 9:00 | EUR | German ZEW (Economic Sentiment) Oct | 20 | 17 | ||

| 9:00 | EUR | German ZEW (Current Situation) Oct | 88.5 | 87.9 | ||

| 9:00 | EUR | Eurozone ZEW (Economic Sentiment) Oct | 34.2 | 31.7 | ||

| 12:30 | USD | Import Price Index M/M Sep | 0.60% | 0.60% | ||

| 13:15 | USD | Industrial Production Sep | 0.20% | -0.90% | ||

| 13:15 | USD | Capacity Utilization Sep | 76.20% | 76.10% | ||

| 14:00 | USD | NAHB Housing Market Index Oct | 64 | 64 | ||

| 20:00 | USD | Net Long-term TIC Flows (USD) Aug | 14.3B | 1.3B |