Sample Category Title

Gold Prices Climb as Oil Takes a Hit

Gold price rallied further and traded above the $2,750 resistance. Crude oil is showing bearish signs and might decline below $72.20.

Important Takeaways for Gold and Oil Prices Analysis Today

- Gold price started a steady increase from the $2,715 zone against the US Dollar.

- It cleared a connecting bearish trend line with resistance at $2,750 on the hourly chart of gold at FXOpen.

- Crude oil prices failed to clear the $80.00 region and started a fresh decline.

- There is a key bearish trend line forming with resistance at $73.85 on the hourly chart of XTI/USD at FXOpen.

Gold Price Technical Analysis

On the hourly chart of Gold at FXOpen, the price found support near the $2,715 zone. The price remained in a bullish zone and started a strong increase above $2,730.

There was a decent move above the 50-hour simple moving average and $2,750. The bulls pushed the price above the $2,765 and $2,770 resistance levels. Finally, the price climbed as high as $2,785 before there was a pullback.

The price tested the $2,730 zone and is currently rising. There was a move above the 50% Fib retracement level of the downside correction from the $2,785 swing high to the $2,730 low, and the RSI is stable above 60.

Immediate resistance is near the $2,765 level and the 61.8% Fib retracement level of the downside correction from the $2,785 swing high to the $2,730 low.

The next major resistance is near the $2,772 level. An upside break above the $2,772 resistance could send Gold price toward $2,785. Any more gains may perhaps set the pace for an increase toward the $2,800 level.

Initial support on the downside is near $2,750 and the 50-hour simple moving average. The first major support is near the $2,742 zone. If there is a downside break below the $2,742 support, the price might decline further.

In the stated case, the price might drop toward the $2,730 zone. Any more losses might push the price toward the $2,715 level.

Oil Price Technical Analysis

On the hourly chart of WTI Crude Oil at FXOpen, the price struggled to clear the $80.00 resistance zone against the US Dollar. The price started a fresh decline below the $76.35 support.

The price even dipped below the $75.00 level and the 50-hour simple moving average. The bulls are now active near the $72.20 level. A low was formed at $72.16, and the price is now consolidating losses. If there is a fresh increase, it could face resistance near the 23.6% Fib retracement level of the downward move from the $79.44 swing high to the $72.16 low at $73.85.

There is also a key bearish trend line forming with resistance at $73.85. The first major resistance is near the $75.80 level or the 50% Fib retracement level of the downward move from the $79.44 swing high to the $72.16 low.

Any more gains might send the price toward the $76.35 level. Any more gains might call for a test of $79.45. Conversely, the price might continue to move down and revisit the $72.20 support. The next major support on the WTI crude oil chart is $70.00.

If there is a downside break, the price might decline toward $70.00. Any more losses may perhaps open the doors for a move toward the $68.50 support zone.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

FTSE In Process Of 5 Waves Advance With Pullback Expectation

Short Term Elliott Wave View in FTSE index shows that the Index breaks to new all-time highs confirming the right side of the market remains bullish. The rally from 12.20.2024 low looks to be extending higher in an impulsive structure within wave 1. While pullback to 8002.28 low ended wave (4) as a triangle consolidation & made new highs supports more strength to continue. Up from wave (4), wave (i) ended at 8152.01 high and wave (ii) pullback ended at 8094.88 low.

The Index resumed higher in wave (iii) which ended at 8270.60 high. Pullback in wave (iv) ended at 8189.50 low. The final leg wave (v) ended at 8326.32 low which also completed wave ((i)) in higher degree. Index then pullback in wave ((ii)) which ended at 8192.31 low. Index has resumed higher again in wave ((iii)). Up from wave ((ii)) low, lesser degree wave (i) ended at 8244.31 high. Pullback in wave (ii) ended at 8193.54 low. Wave (iii) higher ended at 8584.73 high and pullback in wave (iv) ended at 8527.92 low. Then final push higher towards 8586.68 high ended wave (v) thus completed wave ((iii)). Down from there, wave ((iv)) pullback ended at 8462.18 low. Near-term, as far as dips remain above 8462.18 low the index is in process of 3 waves advance with 1 more push higher. Minimum towards 8616.11- 8663.95 area higher to end wave ((v)) of 1. Afterwards, a pullback in wave 2 is expected to take place in 3, 7 or 11 swings before more upside resumes.

FTSE 1-Hour Elliott Wave Chart From 1.29.2025

FTSE Elliott Wave Video

https://www.youtube.com/watch?v=Q2_NEDxzkAc

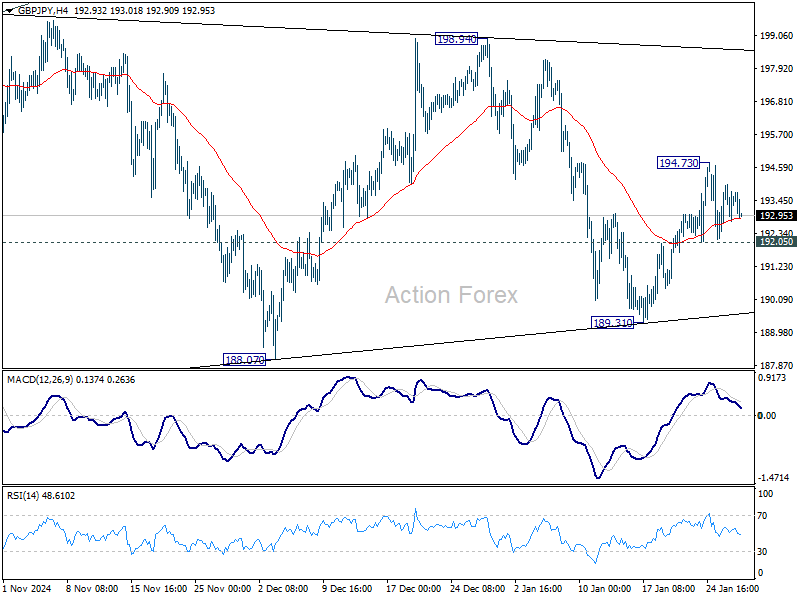

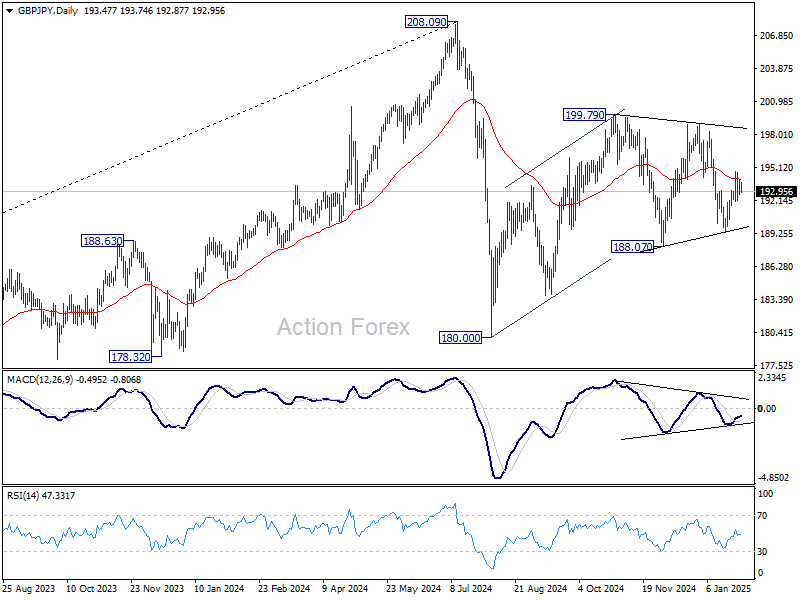

GBP/JPY Daily Outlook

Daily Pivots: (S1) 192.82; (P) 193.43; (R1) 194.13; More...

Intraday bias in GBP/JPY remains neutral at this point. Overall outlook is unchanged that corrective pattern from 180.00 might extend. On the upside above 194.73 will target 198.94/197.79 resistance zone. On the downside, however, break of 192.05 minor support will turn bias back to the downside for 189.31 support instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

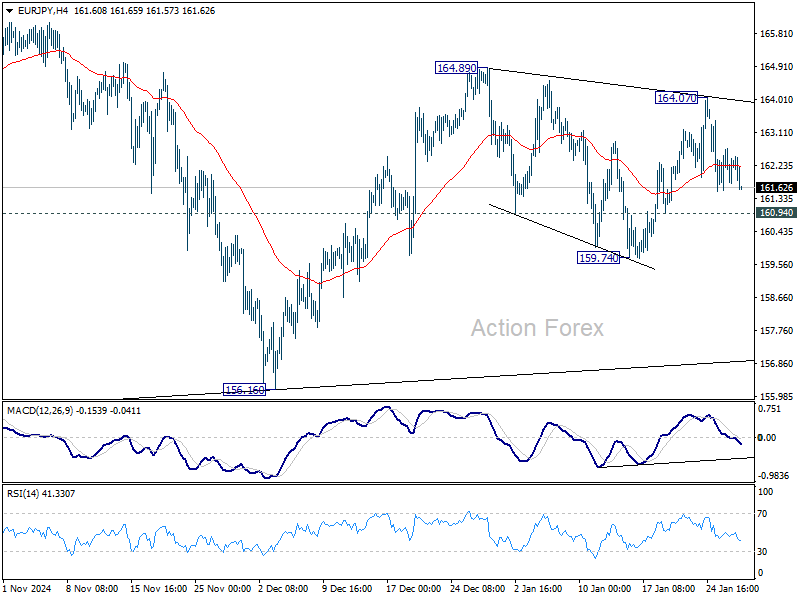

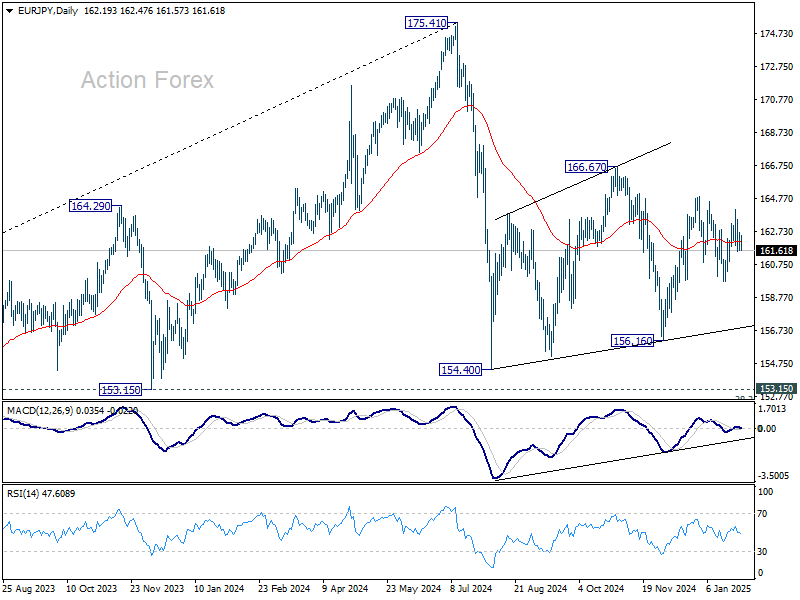

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.64; (P) 162.17; (R1) 162.77; More...

Outlook in EUR/JPY is unchanged and intraday bias stays neutral. Corrective pattern from 154.40 could extend. On the upside, break of 164.07 will target 164.89 and above. On the downside, break of 160.94 minor support will bring deeper fall through 159.74 support.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

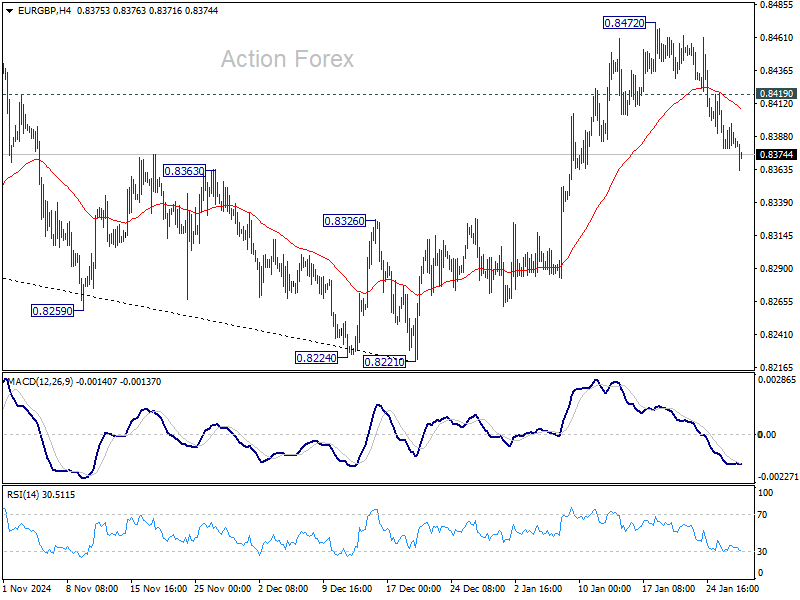

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8371; (P) 0.8392; (R1) 0.8405; More...

Intraday bias in EUR/GBP remains on the downside as fall from 0.8472 short term top is in progress. Sustained break of 55 D EMA (now at 0.8354) will argue that whole rebound from 0.8221 has completed as a corrective move. Nevertheless, strong bounce from the 55 D EMA, followed by break of 0.8419 minor resistance, will argue that the pull back has completed and bring retest of 0.8472.

In the bigger picture, a medium term bottom should be in place at 0.8221, just ahead of 0.8201 key support (2022 low). Sustained trading above 55 W EMA (now at 0.8442) will pave the way to 0.8624 cluster zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621), even just as a correction to the down trend from 0.9267 (2022 high). But still, medium term outlook will be neutral at best as long as 0.8621/4 holds.

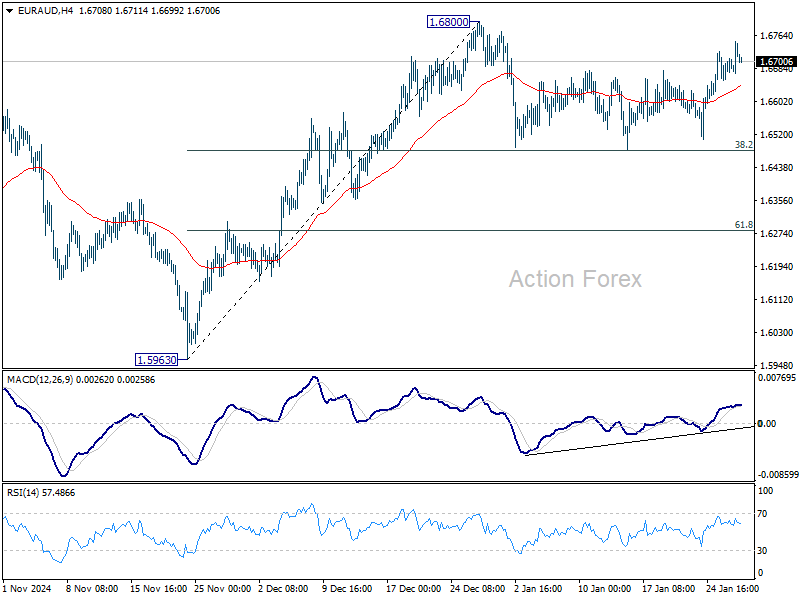

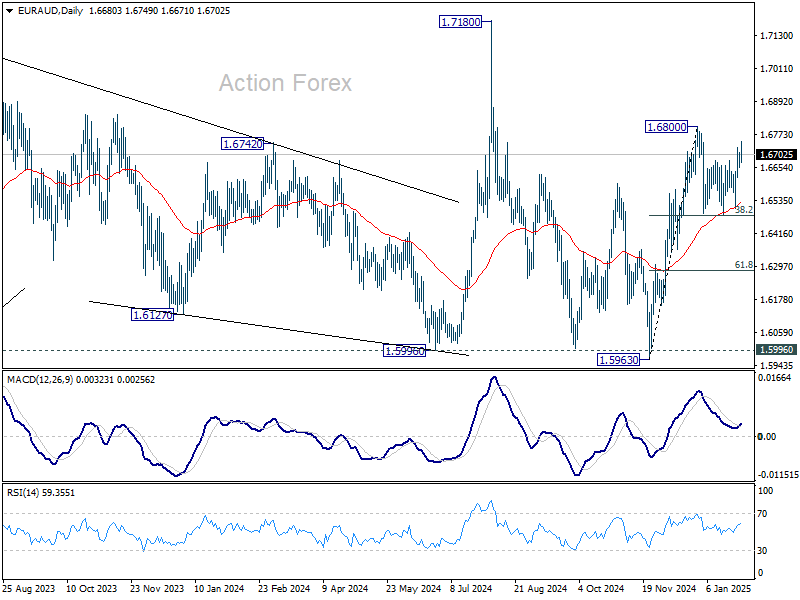

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6656; (P) 1.6684; (R1) 1.6711; More...

Intraday bias in EUR/AUD remains neutral as consolidation continues below 1.6800. In case of another dip, strong support is expected from 38.2% retracement of 1.5963 to 1.6800 at 1.6480 to contain downside. On the upside, firm break of 1.6800 will resume the rally from 1.5963. However, sustained break of 1.6480 will bring deeper correction 61.8% retracement at 1.6283 instead.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support (2024 low) despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

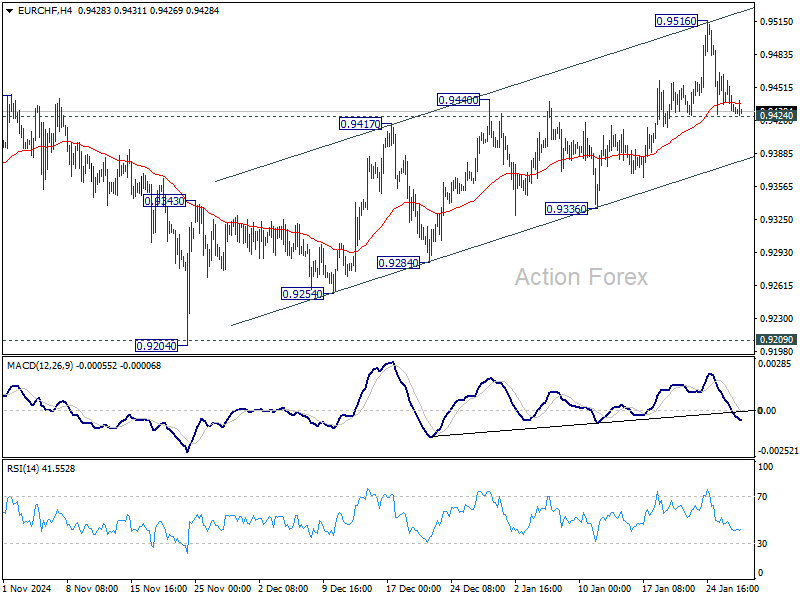

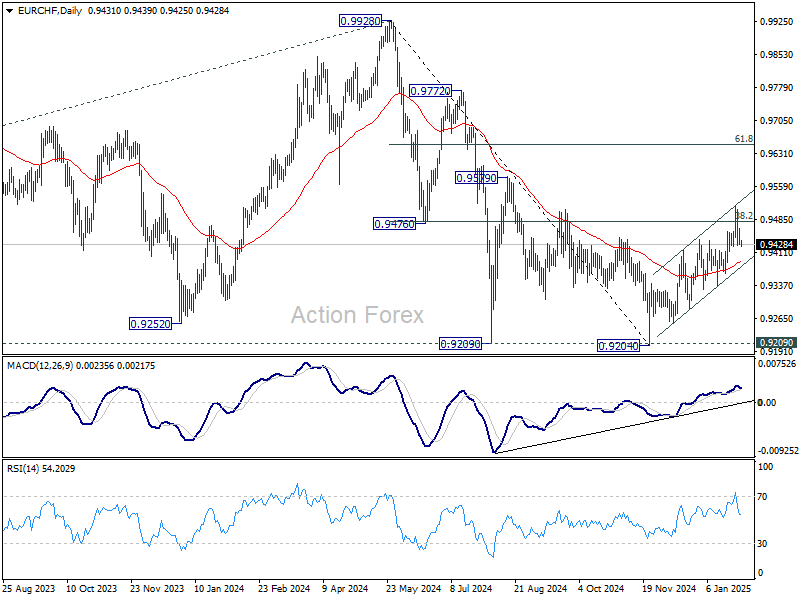

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9418; (P) 0.9442; (R1) 0.9455; More....

Intraday bias in EUR/CHF remains neutral and outlook is unchanged. On the downside, firm break of 0.9242 support will indicate rejection by 38.2% retracement of 0.9928 to 0.9204 at 0.9481. Deeper fall would then be seen back to channel support (now at 0.9377). However, strong rebound from current level will keep the choppy rally from 0.9204 intact.

In the bigger picture, fall from 0.9928 should have completed at 0.9204 with the current strong rebound, after failing to sustain below 0.9252 (2023 low). It's still early to confirm long term bullish reversal. But even as a corrective move, current rebound could extend to 61.8% retracement of 0.9928 to 0.9204 at 0.9651. On the downside, firm break of 55 D EMA (now at 0.9390) will maintain medium term bearishness and bring retest of 0.9204 low.

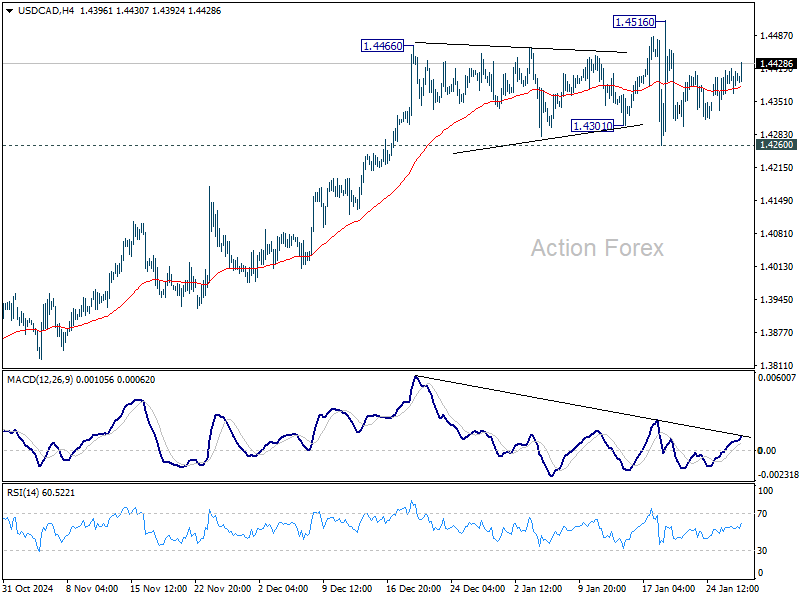

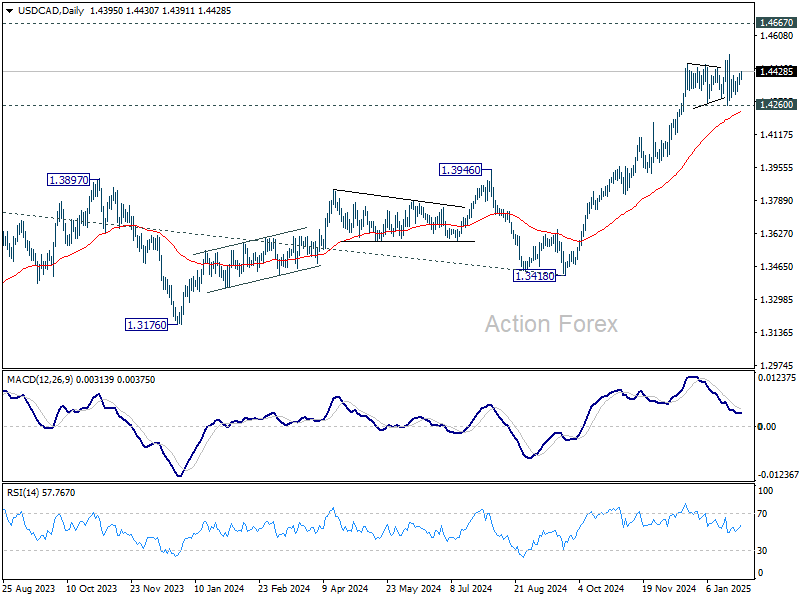

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4367; (P) 1.4394; (R1) 1.4428; More...

No change in USD/CAD's outlook as range trading continues. Intraday bias stays neutral for the moment. Further rally is expected as long as 1.4260 support holds. On the upside, firm break of 1.4516 will resume larger up trend to 1.4667/89 key resistance zone. Nevertheless, firm break of 1.4260 will turn bias to the downside for deeper pullback to 55 D EMA (now at 1.4235) and below.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Decisive break there will confirm long term up trend resumption. Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

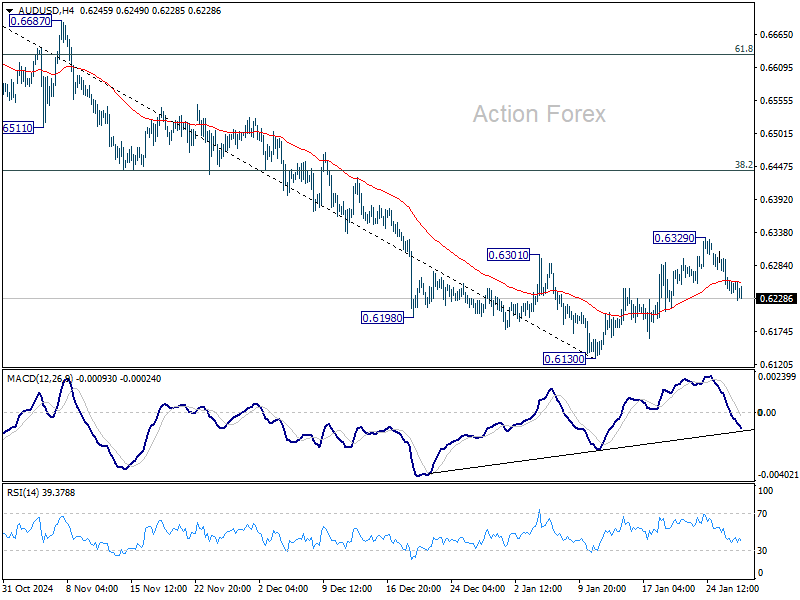

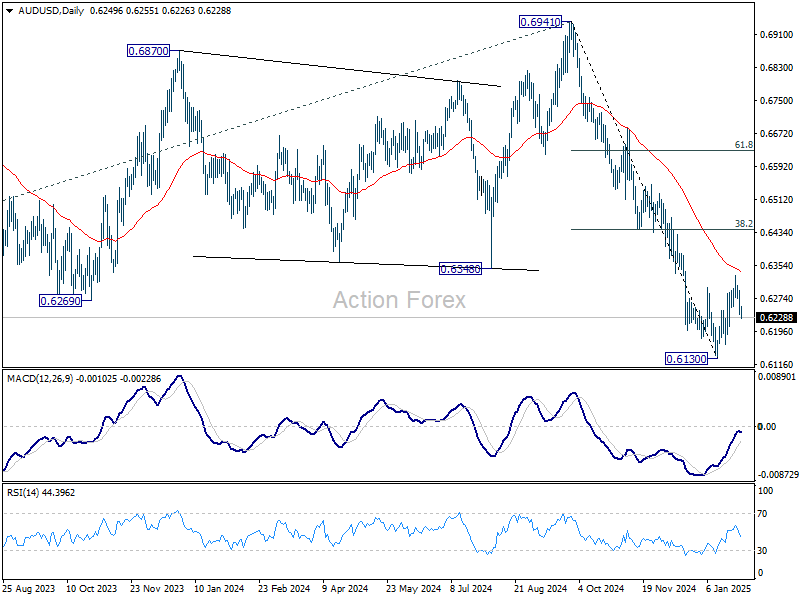

AUD/USD Daily Report

Daily Pivots: (S1) 0.6228; (P) 0.6262; (R1) 0.6286; More...

Intraday bias in AUD/USD remains mildly on the downside. Corrective rebound from 0.6130 could have completed at 0.6329. Deeper fall would be seen to retest 0.6130 low. On the upside, above 0.6329 will resume the rebound. But still, strong resistance is expected from 38.2% retracement of 0.6941 to 0.6130 at 0.6440 to limit upside to complete this corrective rebound.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6545) holds.

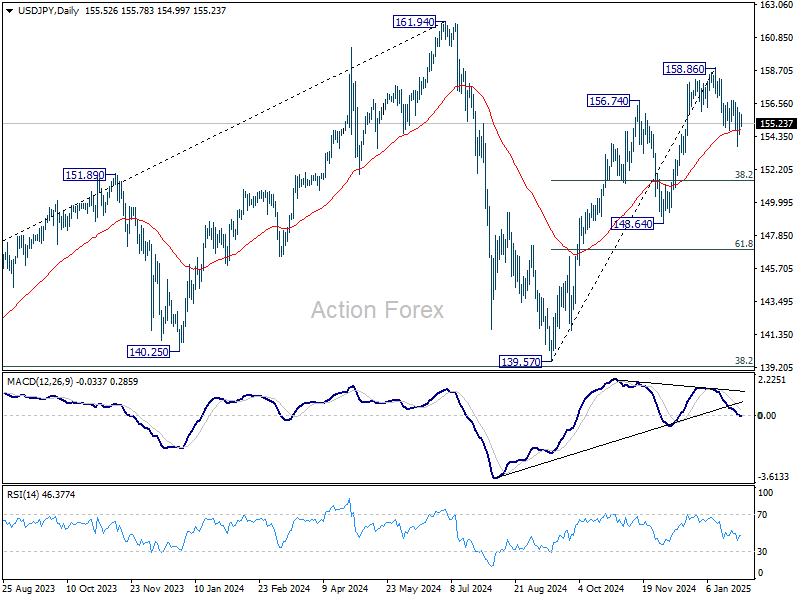

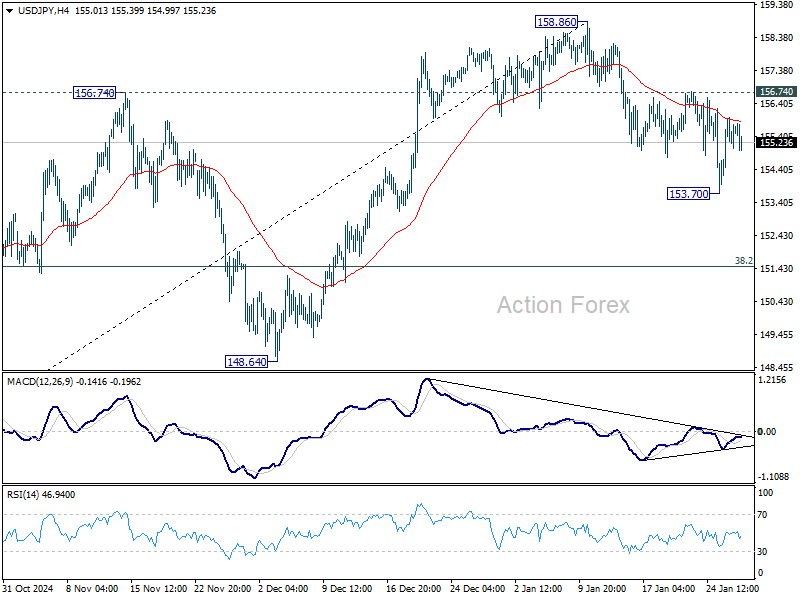

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.61; (P) 155.30; (R1) 156.21; More...

Intraday bias in USD/JPY stays neutral at this point. On the upside, break of 156.74 resistance will indicate that fall from 158.86 has completed as a correction. Intraday bias will be back on the upside for 158.86 and above to resume the whole rally from 138.57. On the downside, below 153.70 will resume the fall from 158.86 to 38.2% retracement of 139.57 to 158.86 at 151.49.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.