Sample Category Title

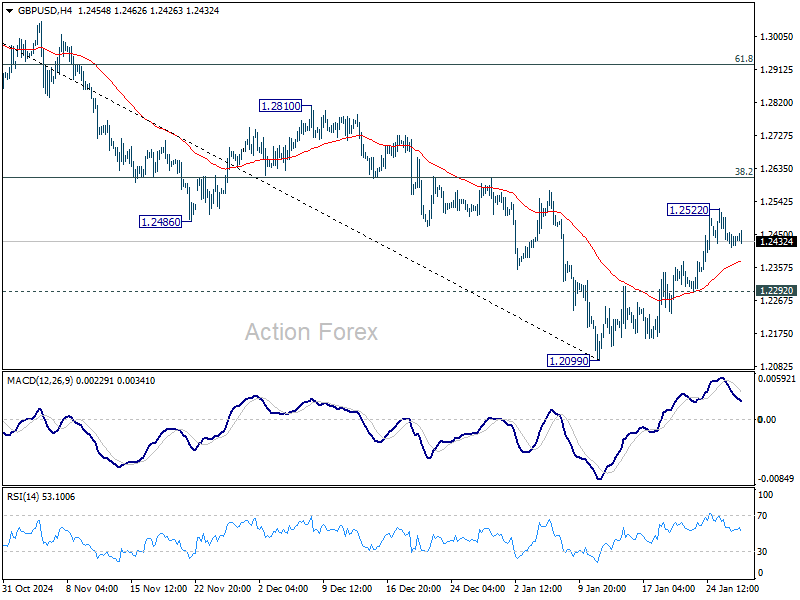

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2404; (P) 1.2453; (R1) 1.2491; More...

Intraday bias in GBP/USD stays neutral and outlook is unchanged. Rebound from 1.2099 is seen as a corrective move. While another rise cannot be ruled out, strong resistance could be seen 38.2% retracement of 1.3433 to 1.2099 at 1.2609 to limit upside. On the downside, below 1.2292 minor support will bring retest of 1.2099 low. However, sustained trading above 1.2609 will raise the chance of reversal and target 61.8% retracement at 1.2923.

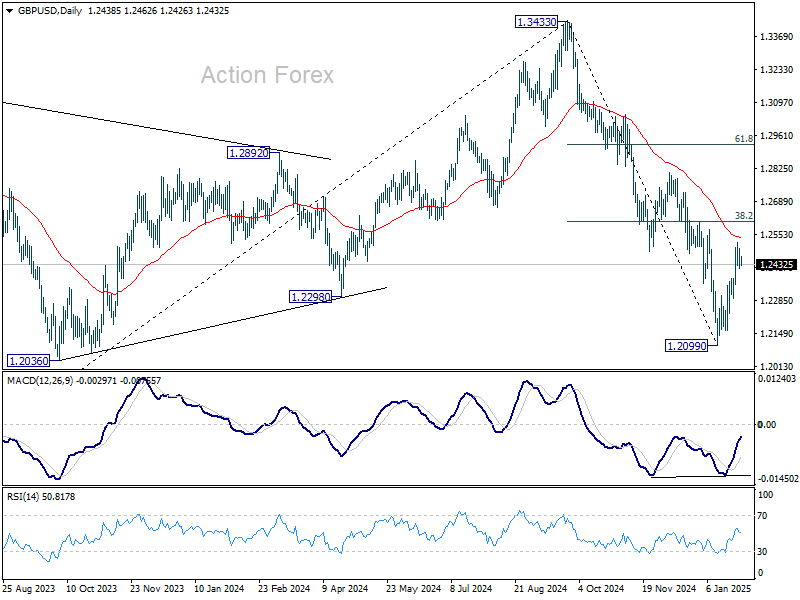

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

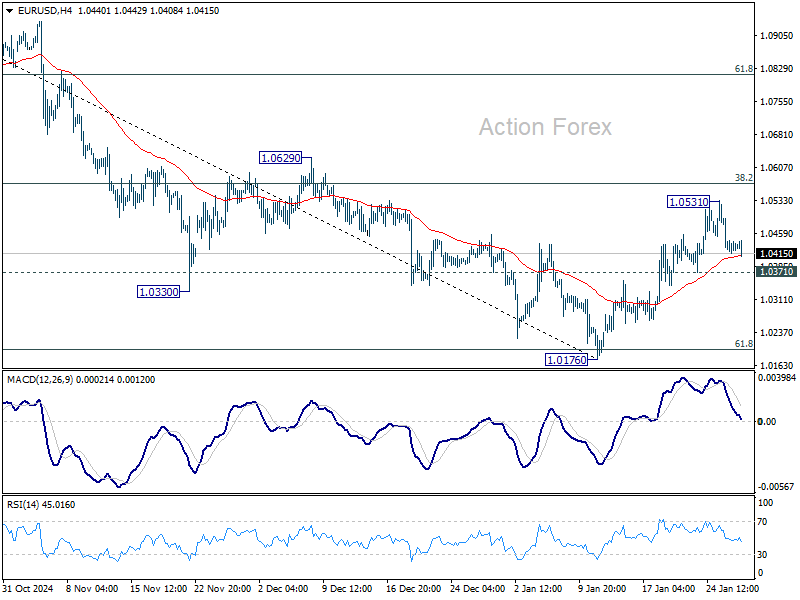

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0398; (P) 1.0447; (R1) 1.0480; More...

Intraday bias in EUR/USD stays neutral and outlook is unchanged. On the downside, break of 1.0371 support will indicate rejection by 38.2% retracement of 1.1213 to 1.0176 at 1.0572 and retain near term bearishness. Retest of 1.0176 low should be seen next. On the upside, though, decisive break of 1.0572 will raise the chance of bullish reversal, and target 61.8% retracement at 1.0817.

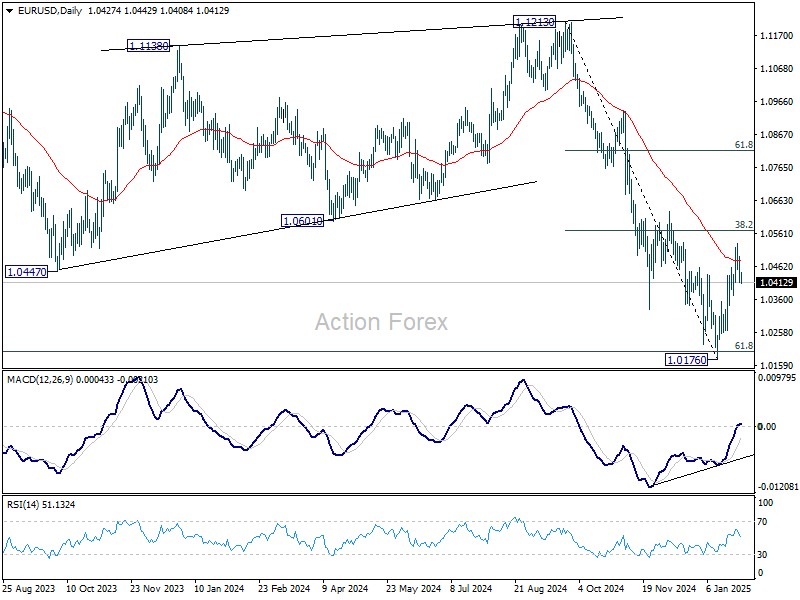

In the bigger picture, outlook is mixed as fall from 1.1274 (2023 high) could either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. Strong support from 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will favor the former case, and sustained break of 55 W EMA (now at 1.0722) will argue that the third leg might have started. However, sustained trading below 1.0199 will favor the latter case and bring retest of 0.9534 low.

Cautious Trading Continues as RBA Cut Expectation Rise, BoC and Fed in Spotlights

Forex markets are trading with a mild risk-off tone in a relatively quiet day so far, with many Asian markets closed for Lunar New Year holiday. Safe-haven currencies, including Yen, Swiss Franc, and Dollar, are holding firm, while commodity-linked currencies are on the weaker side. However, there is little follow-through momentum, with traders hesitant to make significant moves for now. The AI-driven tech rout that dominated sentiment earlier in the week appears to have faded from traders’ focus, with attention squarely on Fed and BoC policy updates.

In Asia Pacific, expectations for an RBA rate cut in February have strengthened following weaker-than-expected Q4 CPI data. Westpac’s Chief Economist Luci Ellis emphasized that trimmed mean inflation data suggests disinflation is advancing more quickly than anticipated, which should give RBA confidence to start cutting rates. CBA’s Head of Australian Economics, Gareth Aird, echoed this view, calling the latest figures a "green light" for policy normalization. While Australian Dollar weakened in response to the data, there has been no sharp acceleration in selling pressure, indicating that markets had already priced in the likelihood of the dovish shift.

BoC is widely expected to cut rates by 25bps today, lowering the policy rate to 3.00%. As rates enter deeper into the estimated neutral range of 2.25–3.25%, policymakers will likely take a more cautious approach moving forward. Adding to the uncertainty is the risks of trade conflict with the US, which could complicate BoC’s policy outlook. Traders will pay close attention to Governor Tiff Macklem’s assessment of economic risks, particularly how the central bank plans to balance easing monetary policy with external uncertainties.

Meanwhile, FOMC is expected to hold rates steady at 4.25–4.50%. The main focus will be on whether Fed signals an extended pause in its rate-cutting cycle, either in its statement or through Chair Jerome Powell’s press conference. Market pricing currently assigns a 67.6% probability of a hold in March and a 49.3% chance in May, with expectations for the next rate cut rising to 75% in June. Powell’s tone will be critical in either reinforcing or reshaping these expectations, with any hawkish signals likely to support the Dollar, while a dovish stance could provide room for further risk-on sentiment.

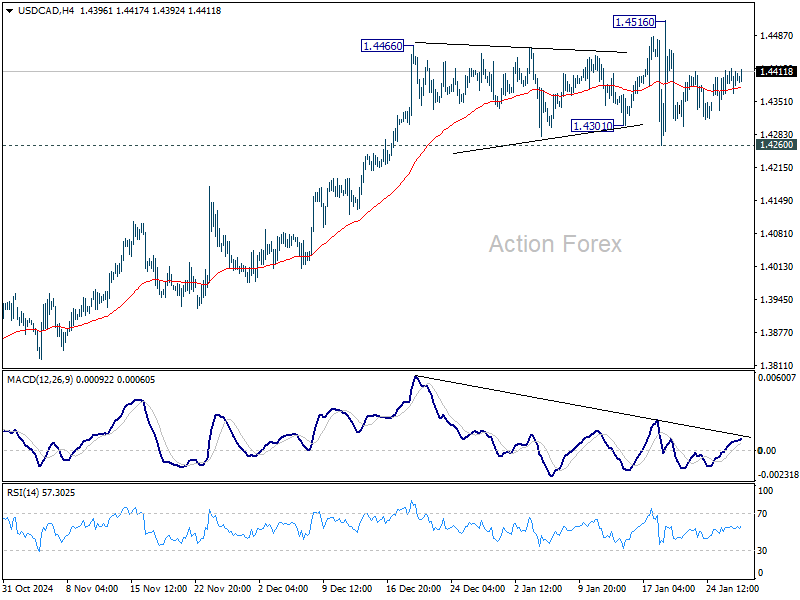

Technically, USD/CAD remains within range between 1.4260 and 1.4516. While the broader outlook remains bullish as long as 1.4260 holds as support, an immediate breakout appears unlikely unless today’s policy announcements deliver a significant surprise. A clearer directional move may only emerge once the tariff situation between the US and Canada is clarified, which remains a key source of uncertainty for the pair.

For the week so far, risk aversion continues to dominate, though without significant intensification. Yen remains the strongest performer, followed by Swiss Franc and Dollar. Aussie continues to struggle at the bottom, followed by Kiwi and then Euro. Sterling and Loonie are positioning in the middle.

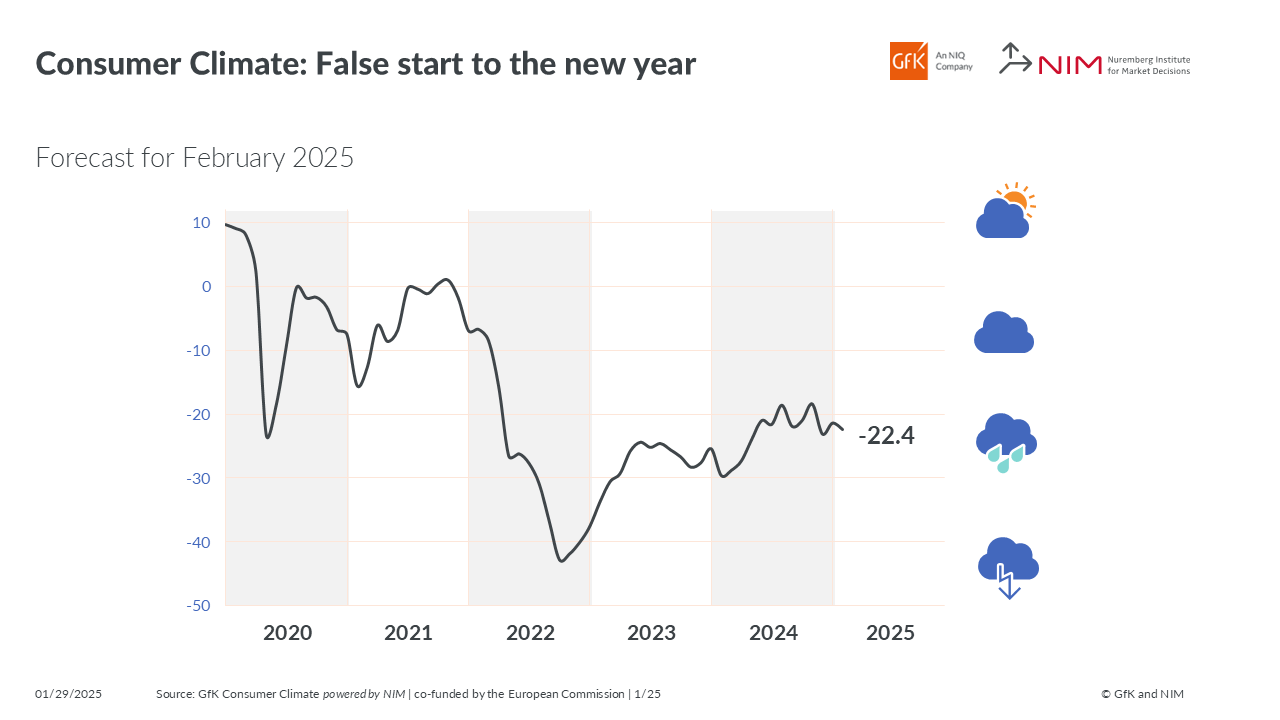

German Gfk consumer sentiment falls to -22.4, recovery hopes fade

Germany’s GfK Consumer Sentiment Index for February fell to -22.4, down from -21.4 and missing expectations of -20.5.

In January, economic expectations dropped by 1.9 points to -1.6, while income expectations declined by 2.5 points to -1.1. The most concerning development came from willingness to buy, which fell 3 points to -8.4, its lowest level since August 2024,.

Rolf Bürkl, consumer expert at NIM, noted that “the Consumer Climate has suffered another setback and starts gloomy into the new year.”

The moderate optimism seen in late 2024 has faded, with Bürkl adding that the trend since mid-2024 has been stagnation at best. A key concern is inflation, which has recently picked up again, limiting prospects for a meaningful rebound in consumer demand.

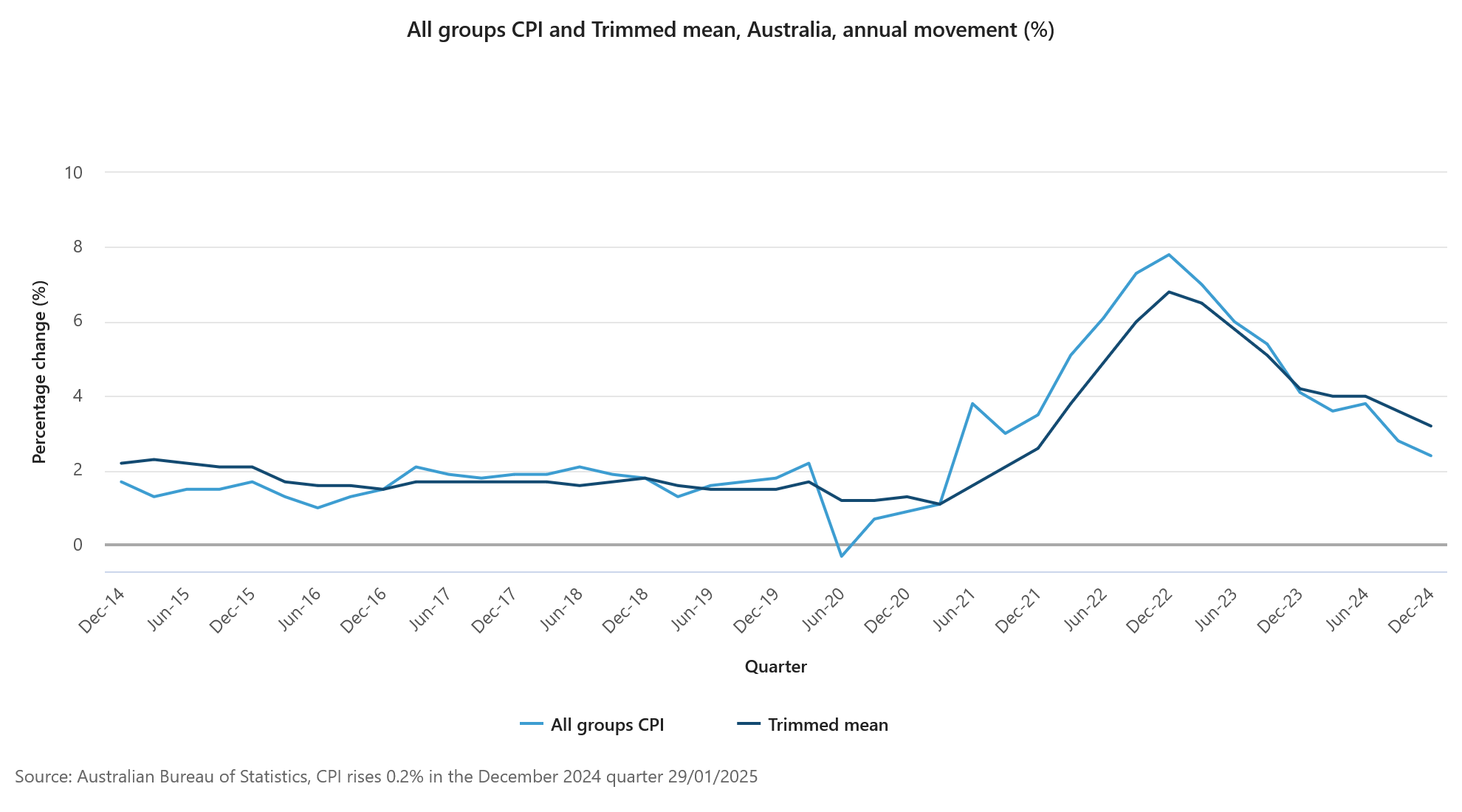

Australia's CPI slows to 2.4% in Q4, trimmed mean CPI down to 3.2%

Australia’s Q4 CPI rose just 0.2% qoq, same as the prior quarter, falling short of expectations of 0.4% yoy. Trimmed mean CPI also undershot forecasts, rising 0.5% qoq versus the expected 0.6% qoq.

On an annual basis, headline CPI slowed from 2.8% yoy to 2.4% yoy, slightly below 2.5% yoy consensus. Trimmed mean CPI fell from 3.6% yoy to 3.2% yoy, missing 3.3% yoy estimate.

These weaker inflation prints reinforce expectations that RBA may begin easing policy as early as its February 17-18 meeting.

The decline in annual inflation was largely driven by steep drops in electricity prices (-25.2%) and automotive fuel (-7.9%). Goods inflation slowed sharply to 0.8% yoy, down from 1.4% yoy in Q3. Meanwhile, services inflation remained elevated at 4.3% yoy, though slightly lower than the 4.6% yoy in the previous quarter.

In December, monthly CPI rebounded from 2.3% yoy to 2.5% yoy, matched expectations.

RBNZ's Conway sees cautious OCR path to neutral

RBNZ Chief Economist Paul Conway stated in a speech today that Official Cash Rate at 4.25% remains "north of neutral". The central bank estimates the neutral rate between 2.5% and 3.5%.

"Easing domestic pricing intentions and the recent drop in inflation expectations help open the way for some further easing," Conway added.

However, Conway emphasized a cautious approach, noting that policymakers will "feel our way" as rates approach neutral. RBNZ will continuously reassess its neutral rate estimate, adjusting based on economic conditions.

If neutral is underestimated, stronger-than-expected activity and inflation would signal a less restrictive policy than intended, prompting recalibration, he added.

The central bank expects potential output growth to range between 1.5% and 2% annually over the next three years, reflecting a lower economic "speed limit." This weaker outlook stems from sluggish productivity and reduced net immigration, limiting long-term economic capacity.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0398; (P) 1.0447; (R1) 1.0480; More...

Intraday bias in EUR/USD stays neutral and outlook is unchanged. On the downside, break of 1.0371 support will indicate rejection by 38.2% retracement of 1.1213 to 1.0176 at 1.0572 and retain near term bearishness. Retest of 1.0176 low should be seen next. On the upside, though, decisive break of 1.0572 will raise the chance of bullish reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, outlook is mixed as fall from 1.1274 (2023 high) could either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. Strong support from 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will favor the former case, and sustained break of 55 W EMA (now at 1.0722) will argue that the third leg might have started. However, sustained trading below 1.0199 will favor the latter case and bring retest of 0.9534 low.

German Gfk consumer sentiment falls to -22.4, recovery hopes fade

Germany’s GfK Consumer Sentiment Index for February fell to -22.4, down from -21.4 and missing expectations of -20.5.

In January, economic expectations dropped by 1.9 points to -1.6, while income expectations declined by 2.5 points to -1.1. The most concerning development came from willingness to buy, which fell 3 points to -8.4, its lowest level since August 2024.

Rolf Bürkl, consumer expert at NIM, noted that “the Consumer Climate has suffered another setback and starts gloomy into the new year.”

The moderate optimism seen in late 2024 has faded, with Bürkl adding that the trend since mid-2024 has been stagnation at best. A key concern is inflation, which has recently picked up again, limiting prospects for a meaningful rebound in consumer demand.

Australia’s CPI slows to 2.4% in Q4, trimmed mean CPI down to 3.2%

Australia’s Q4 CPI rose just 0.2% qoq, same as the prior quarter, falling short of expectations of 0.4% yoy. Trimmed mean CPI also undershot forecasts, rising 0.5% qoq versus the expected 0.6% qoq.

On an annual basis, headline CPI slowed from 2.8% yoy to 2.4% yoy, slightly below 2.5% yoy consensus. Trimmed mean CPI fell from 3.6% yoy to 3.2% yoy, missing 3.3% yoy estimate.

These weaker inflation prints reinforce expectations that RBA may begin easing policy as early as its February 17-18 meeting.

The decline in annual inflation was largely driven by steep drops in electricity prices (-25.2%) and automotive fuel (-7.9%). Goods inflation slowed sharply to 0.8% yoy, down from 1.4% yoy in Q3. Meanwhile, services inflation remained elevated at 4.3% yoy, though slightly lower than the 4.6% yoy in the previous quarter.

In December, monthly CPI rebounded from 2.3% yoy to 2.5% yoy, matched expectations.

RBNZ’s Conway sees cautious OCR path to neutral

RBNZ Chief Economist Paul Conway stated in a speech today that Official Cash Rate at 4.25% remains "north of neutral". The central bank estimates the neutral rate between 2.5% and 3.5%.

"Easing domestic pricing intentions and the recent drop in inflation expectations help open the way for some further easing," Conway added.

However, Conway emphasized a cautious approach, noting that policymakers will "feel our way" as rates approach neutral. RBNZ will continuously reassess its neutral rate estimate, adjusting based on economic conditions.

If neutral is underestimated, stronger-than-expected activity and inflation would signal a less restrictive policy than intended, prompting recalibration, he added.

The central bank expects potential output growth to range between 1.5% and 2% annually over the next three years, reflecting a lower economic "speed limit." This weaker outlook stems from sluggish productivity and reduced net immigration, limiting long-term economic capacity.

S&P 500 Rebounds After Monday’s Drop

The S&P 500 index (US SPX 500 mini on FXOpen) has recovered following Monday’s sharp decline, which was triggered by the success of Chinese startup DeepSeek and its AI model. As of this morning, the index is trading above the week’s early high.

This resilience suggests that the stock market has stabilised ahead of the Federal Reserve’s decision, scheduled for today at 22:00 GMT+3. Interest rates are expected to remain unchanged, but the key question is what stance Fed Chair Jerome Powell will take now that Donald Trump has officially assumed the U.S. presidency. Trump has already stated at the Davos forum that interest rates should be lowered. Powell’s press conference is set for 22:30 GMT+3.

Technical analysis of the S&P 500 index (US SPX 500 mini on FXOpen) shows that the price is approaching the 6,100 level for the third time. The first two attempts to break above this level (marked with red arrows) were unsuccessful.

From a bullish perspective:

→ The long-term trend remains upward, as indicated by the moving average.

→ A successful breakout above 6,100 could turn this level into strong support, similar to how 5,660 acted previously.

However, it is also possible that:

→ Powell’s remarks today will be more hawkish than expected.

→ The market may react negatively.

→ The price could make a bearish move, reinforcing the relevance of the downward channel (marked in red).

Prepare for heightened market volatility this evening.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

RBA Rate Call: 0.2 Beats 0.3, It’s on for February

It’s on: the better-than-expected inflation data tips the balance back to the February move we had previously expected. RBA’s view of the economy will need to pivot further.

Normally it should not come down to one number. This round, however, the CPI has been the deciding factor because the message from other available data has been so mixed. With trimmed mean inflation at 0.5% in the quarter (3.2%yr), we have just enough evidence to conclude that disinflation has proceeded faster than the RBA expected, so the Board will have the required confidence to start the rate-cutting phase in February.

When we changed our call back in November to a start date of May 2025, we nonetheless assessed that a February move could not be ruled out. It was a matter of what was the most likely outcome, not what the only possible outcome was. The better-than-expected inflation data tilts the balance of probabilities back in February’s favour.

In addition to the trimmed mean outcome (Westpac had a ‘skinny’ 0.6%, while the actual outcome was 0.5%), we see encouraging signs in housing-related inflation suggesting that the momentum in domestic price pressures is fading a bit faster than the RBA feared. Both rents and home-building costs have decelerated noticeably in recent months, and not just because of government cost-of-living support.

As noted, the rest of the data flow had not provided a clear steer either way. Domestic demand growth has disappointed, with consumers spending less of the Stage 3 tax cuts than had been widely assumed. Wages growth and other measures of labour costs have also undershot the RBA’s forecasts for late-2024 outcomes (though not our own).

Against that, the labour market has been more resilient than we or the RBA expected. At 4%, the unemployment rate in the December quarter was 0.3ppts below the RBA’s November forecast. Other indicators such as job vacancies and business surveys implied that the labour market had not eased at all in second half of 2024. Average hours worked painted a somewhat softer picture, but this was matched by an unwind in hours offered as cost-of-living pressures eased. The number of people reporting being underemployed therefore fell. The RBA already viewed the labour market as being tighter than full employment, and the recent wages data would not have induced enough of a downward revision to its assessment of the unemployment rate consistent with full employment to bridge the gap.

While we do not regard recent exchange rate movements as particularly consequential for the RBA decision, the prospect of more volatility here and in financial markets more broadly could have been a reason to delay and wait for more information.

In the end though, the good news on inflation beats the stronger news on the labour market. Recall that the RBA’s November forecasts had trimmed mean inflation at 3.4% and an unemployment rate of 4.3% for the December quarter of 2024. The 0.2ppt downside surprise on trimmed mean inflation outweighs the 0.3%pt surprise on the unemployment rate.

Finally, there is the question of timing and tactics. Contrary to the speculation seen occasionally, the RBA Board has historically set policy according to the demands of its mandate and its assessment of the economy without political considerations. Elections or other political events do not generally influence the timing of rate moves. This time, though, the forthcoming change of the make-up of the Board could create some awkward optics around timing. If the current Board held rates steady in February and then the revamped Board cut rates in April, it would look like the government ‘stacked’ the Board to get the desired result. This is one of the reasons why we focused on February and May in our assessments. So there is an argument that the current Board will opt to get on with it rather than get caught up in the politics of the situation.

We are also mindful that moving now would represent a further pivot in the RBA’s view of the economy, following the pivot at the December meeting. We therefore cannot completely rule out that the Board (and the staff) dig in on their assessment that the demand is still outstripping supply, and keep rates on hold. The run of inflation data of late makes such an assessment even harder to justify, though.

Looking beyond the next meeting, we see the RBA as remaining data-dependent from here and not in a hurry to move further. Conditional on further declines in inflation and some softening in the labour market, we see cuts in May, August and November, taking the terminal rate to 3.35%. This is in effect a reversion to our earlier call, now that it has become clearer that the economy is evolving broadly in line with our forecasts, and not the more hawkish view of domestic cost growth that would have led to further delays.

Fed Will Hold Rates Steady Against Backdrop of Healthy Economy and Still-Above Target Inflation

Markets

US tech stocks rebounded sharply with the likes of Nvidia surging 9% after losing market capitalization +/- the size of Belgium’s economy. The Nasdaq’s 2% gain almost wiped out Monday’s 3% drop. US Treasuries marginally outperformed Bunds with rates closing slightly lower in the former and about 2-3 bps higher in the latter. The risk-on nor UST outperformance hindered a USD comeback. Trump’s hawkish trade comments that downplayed the gradual tariff approached favoured by UST Secretary Bessent jolted the greenback against all G10 peers. EUR/USD retreated to 1.043 while USD/JPY and the DXY reclaimed the 155 and attacked the 108 respectively.

Yesterday’s moves were more of a (technical) countermove than they were inspired by major news. Today, though, there’s a lot more in store for markets, Bloomberg’s article this morning covering an interview with the European Commissioner for financial services Albuquerque to name just one. She’s open to the idea of a coalition of the willing to move forward with a capital markets union in an attempt to break the long-running deadlock at the EU-wide level. Draghi’s report of last September appears to have put something in motion. Trump’s return to the White House has expedited things further. The EU faces a massive financing gap to fund defense spending as well as the green transition. The Financial Times end last year reported a similar coalition of the willing initiative for the former. Regarding the latter, EC president von der Leyen is expected to announce major legislative changes today to cut red tape (mostly ESG reporting rules) dramatically. The eco calendar is really heating up today with policy meetings in Sweden, Canada end the US. The Fed will hold rates steady against the backdrop of a healthy economy and still-above target inflation. Economic data since the Fed’s and chair Powell’s hawkish pivot in December has been outright strong and offered no reason to scale down the rhetoric. That should place a bottom below US yields and the dollar. Trump is a wildcard. Powell will probably keep his cards close to his chest in terms of what the central bank expects of his (yet-to-be-announced) policies going forward. Given the state of the economy the Fed has and will use the time at the sidelines. But POTUS will surely have a say on the Fed’s decision not to cut rates after doing so three times straight, triggering perhaps more market volatility than the decision itself. US tech remains at the center stage as well with Microsoft, Tesla and Meta all reporting, be it after-market. Belgium and Spain are among the first to report Q4 GDP numbers ahead of the euro area figure tomorrow.

News & Views

In an interview with the Financial Times (FT) this morning, Ales Michl, head of the Czech National Bank (CNB) said that he will present to the Bank board on Thursday a plan to invest in Bitcoin as a way of asset diversification. If approved, it could lead the bank to hold 5% of its reserves (approx. €140 bln) in Bitcoin. Michl acknowledges the extreme volatility and limited record of the Bitcoin but also pointed at growing investor interest since the launch of several ETFs. He also refers to US president Trump’s pledges on deregulation with respect to Bitcoin and growing influence of cryptocurrency executives in the US administration. Michl ‘defends’ his different approach compared to peers, who are more reluctant towards crypto, as he takes more of an approach similar to running an investment fund. The CNB’s €140 bln currency reserves are equivalent to about 45 % of GDP. Some 22% is already invested in equities. Michl also aims the raise the part of US stocks to about 50% from 30% currently in a three year horizon. On monetary policy, he indicated that its very likely the CNB will cut rates by 25 bps at the February meeting.

Australian inflation in the final quarter of last year slowed to 0.2% Q/Q and 2.4% Y/Y. The 0.2% quarterly rise matched the September quarter, which was the lowest since June 2020. The Y/Y measure declined from 2.8% in Q3. The underlying trimmed mean (ex. volatile components such as electricity) also slowed to 0.5% M/M to 3.2% (from 3.6%). Electricity prices fell by 9.9% in the December 2024 quarter, following a fall of 17.3% 2024Q3. Without the rebates, electricity prices would have risen 0.2% this quarter, the Australian Bureau of Statistics indicated. Annual goods inflation was 0.8%, down from 1.4% in Q3. Annual services inflation was 4.3% down from 4.6%. The slowdown of inflation dynamics in the second half of last year is seen opening the door for the Reserve Bank of Australia staring its easing cycle as soon as the February 18 meeting (policy rate currently 4.35%). The Aussie dollar this morning is ceding modest ground to trade near AUD/USD 0.625.

Stuck Between a Rock and Trump

I was clearly not alone thinking that Monday’s AI selloff triggered by DeepSeek news was overdone. Investors rushed back to the market to buy Nvidia shares at a discount – there was strong dip buying below the $120 per share, and the stock price closed the session 9% up. The afterhours was calm. The Magnificent 7 stocks rebounded 3%, Nasdaq jumped 1.60%, Apple – which was among rare tech stocks that was cheering the cheaper AI news – rallied more than 3% on Monday and on Tuesday, while the Global X Uranium ETF recovered 1.77%.

The DeepSeek shock is probably behind without further damage until investors and the Big Tech leaders get more clarity on if and how DeepSeek managed to create a model *this* cheap. But no matter if DeepSeek’s claims are true or not, Monday’s tech rout will taint the earnings season, and investors will be peakier about the AI spending announcements. Together, Amazon, Meta, Alphabet and Microsoft are expected to spend up to $300bn in AI this year, while the earnings growth is expected to slow to less than 20% in 2025.

Zooming into the Q4, the Magnificent 7 are expected to print a 20% earnings growth last quarter. That’s down from nearly 60% printed the same time last year. And the combination of robust spending and slowing earnings doesn’t bode well with investors. The narrative this earnings season is shifting from how much the big Tech should spend to get to the place they want to be to how little they could spend to get there.

This being said, I still strongly believe that compromising quality for lower cost is not the best way to remain a leader in such a fast evolving tech environment, but investors will say the last word.

Speaking of earnings, ASML—another victim of the DeepSeek-triggered tech rally this week—couldn’t rebound as successfully as its US peers on Tuesday. But the company just printed a set of better-than-expected Q4 results before the bell in Europe, which should help shrug off some of the DeepSeek dust.

Today, after the bell, Tesla, Meta and Microsoft will reveal their own Q4 results. Hopefully, they will come with encouraging news regarding the return on their AI investment to help soothing investors’ nerves about further, massive AI spending announcements... Strong results could help improving appetite after a difficult start to the week, while any misstep will likely be hardly punished. Expect volatility.

Rate decisions

US yields remained under pressure yesterday as capital continued to flow into the safer US treasuries as many investors preferred to stay on the safe side of the game. The US dollar, however, gained on the back of Donald Trump’s renewed tariff threats. The Tariff Man reacted to Treasury Secretary Bessent’s proposal of imposing a 2.5% universal tariff by saying that the tariffs should be ‘much bigger than that’.

But of course, the higher the tariffs, the higher the price pressures will be. And it’s up to Federal Reserve to deal with the consequences. So yes, the Fed members have been scratching their heads since yesterday and will announce their latest policy verdict later today. The Fed is broadly and highly expected to maintain rates unchanged at today’s announcement. The US job market remains healthy, US growth robust, earnings encouraging, consumer spending strong and inflation is giving signs of heating up. US headline inflation hit the 2.9% in the latest reading, up from 2.4% printed earlier in fall, while core inflation has slightly come down but proves to be very sticky above the 3% mark. But, the latest consumer survey showed that Americans are losing confidence in the economy, they say that the jobs are harder to get, that the income is expected to improve less and that business conditions don’t look as encouraging as they did a few months ago. Therefore, the Fed is stuck between a rock and Donald Trump. What Powell will say matters more than what the Fed announces today. Before the Fed announcement, investors bet that the Fed won’t announce the next rate cut before May. A dovish tone from the Fed should further ease the US yields, while a cautious tone could revive the bond sell off. The US dollar could give back a part of Trump-led gains with a supportive Fed statement, but the fundamentals compared to the other major economies will likely remain supportive of the US dollar. And the Trump tariff risks remain tilted to the upside.

Speaking of other countries, the Bank of Canada (BoC) is expected to announce a 25bp cut to its policy rate today and the European Central Bank (ECB) will likely do the same when it meets tomorrow. The USDCAD is consolidating a few pips below the 1.44 mark this morning. While the divergence between the BoC and the Fed is already priced in, any dovish comments from the BoC could revive the selling pressure in the Loonie and support a further advance in USDCAD toward the 1.45 mark. In Europe, the euro appetite is losing strength after the failure to pursue gains above the 1.05 psychological mark. Technically, there is an evening star formation that hints that the weakness could extend into the next few sessions. The eurozone’s growth outlook is less than ideal and the ECB has solid reason to sound supportive and act.