Sample Category Title

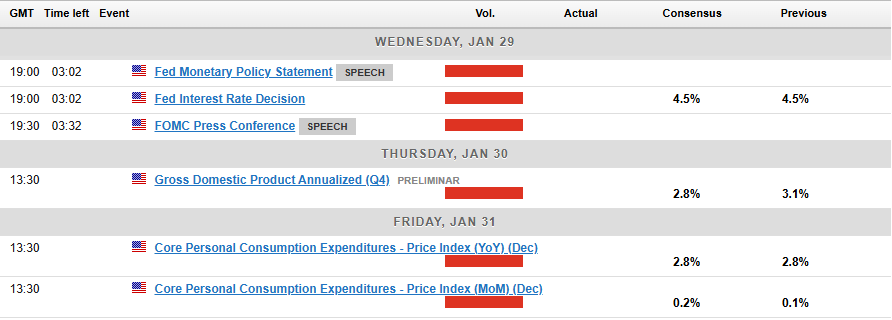

(FED) Federal Reserve Issues FOMC Statement

Recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate has stabilized at a low level in recent months, and labor market conditions remain solid. Inflation remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals are roughly in balance. The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Susan M. Collins; Lisa D. Cook; Austan D. Goolsbee; Philip N. Jefferson; Adriana D. Kugler; Alberto G. Musalem; Jeffrey R. Schmid; and Christopher J. Waller.

Mired in Uncertainty, Bank of Canada Cuts Again

The Bank of Canada cut its policy rate by 25 basis points as expected, but the focus of its commentary had less to do with its current assessment of the Canadian economy and much more on how to navigate an economy that potentially gets significantly knocked off course by U.S. tariffs.

The BoC had a good understanding (and confidence in) how the economy is currently travelling. With 200 bps of easing already in the pipeline, Canadian growth is low but slowly improving, the unemployment rate is near a peak, and inflation is now well within the BoC’s target range. We agree. Without any shocks, the central bank would likely continue to gradually ease towards, we think, 2% by year end, but in smaller magnitudes and at a slower pace than in 2024.

But, the BoC isn’t facing standard run-of-the-mill uncertainty in its outlook. Both the Monetary Policy Report and Governor Tiff Macklem’s communication took a very different tone this time around. If central banks use the idea that setting monetary policy in uncertain times is like walking around in a dark room and trying not to trip on furniture, the BoC could more appropriately be described as blindfolded with projectiles being thrown at it.

Indeed, the BoC is fighting two particular demons that make its base case forecasts and current assessment of the state of affairs far less useful than usual. Instead, the value of their communication is in the clues they drop about how they might navigate the shocks ahead. We think most signs continue to point to further declines in interest rates, the magnitude and speed of which will be determined by the details of a potential U.S.-Canada trade conflict.

1. The BoC is facing “more than unusual uncertainty.”

It mentions “uncertainty” 42 times in the report, and, even before launching into the MPR, the BoC states its economic outlook doesn’t include any specific U.S. tariff policies yet. Governor Macklem says that we are simply missing too many pieces of information to know exactly what a trade war means for Canada.

“There’s a lot of things we don’t know, when and for how long,” he says. “We don’t know what retaliatory measure… or fiscal measures will be taken in advance”.

As we highlighted in our A playbook for how to measure a tariff shock in Canada, those details can be very significant on the direction and size of the impact in Canada.

However, the forecasts recognize that tariff threats are already impacting financial markets and business decisions. We’ve also been highlighting that tariff threats creates a negative “uncertainty” shock that weighs on growth. Downward revisions to the BoC’s forecasts for growth in 2025 and 2026 to 1.8% reflects some of this.

Moreover, Governor Macklem noted tariff threats alone “weighed on our decision” and that the more the BoC could get the economy on “solid footing” ahead of the shock, the better. We think the mere possibility of tariffs will keep the BoC on a dovish bias as it tries to prepare Canada for a potential shock. Unlike a provincial or federal government, the BoC doesn’t have to keep any “powder dry” for what’s ahead. The central bank has the luxury of preparing the economy with this cut, and, we expect, future cuts as inflation is now comfortably below 2% for three of the past four months. Put differently, the risks of excess easing are quite low in Canada, especially relative to the U.S.

2. The BoC is challenged by the complexity of modelling a tariff shock on Canada and the central bank’s role in it.

Similarly to how RBC Economics described the transmission of a tariff shock in Canada, the BoC engages in an illustrative example that highlights the challenges of measuring how badly a tariff would hurt an economy and how many assumptions would need to go into the forecast. Policymakers appear to have avoided the idea that a single number can neatly summarize the risks ahead. Governor Macklem adds that the central bank is busy running scenarios and engaging in outreach with Canadians.

Still, how the BoC would respond in a prolonged trade conflict isn’t clear. Governor Macklem said it would depend on what ended up dominating the economy once tariffs arrived—the downsides on growth or the upsides of inflation. However, there were some important takeaways about how the BoC may be thinking about its role:

- A tariff shock is a negative growth shock, but also increases inflation. It is, effectively, a “stagflationary” shock. The BoC noted it is “equally concerned about inflation rising above the 2% target or falling below it,” and there is both upside and downside risks surrounding the outlook. Our take is the BoC should focus on the downside risks around growth versus a supply-driven inflation shock (e.g. if the unemployment rate is rising, then even an inflation-targeting central bank would have to concede that rate hikes would do little to solve for inflation driven by tariffs except to create deflation in other areas of the economy). But, the BoC doesn’t appear to be determined on where it would land. That’s likely why it removed more explicit forward guidance from its statement (even as a dovish bias is clearly still in play).

- And yet, Governor Macklem emphasized that solving the damage to Canada’s economy couldn’t just be the bank’s job.

“Monetary policy cannot offset the economic consequences of a protracted trade conflict. The reality is the economy is going to work less efficiently, Canada’s going to produce less and going to earn less. Monetary policy cannot change that, it cannot offset it. It can help the economy adjust to that, a source of stability through that adjustment so that the adjustment is less unpleasant.”

(That reads like a call for fiscal policy to also help support the shock, though, of course, the BoC cannot opine directly on this topic). It also is another nod to the challenges of a stagflationary shock for a central bank, where the best course of action will remain murky even as details of a trade conflict materialize.

USDCAD: BoC Rate Cut and US Tariff Threats Weaken Loonie

Fundamental Analysis:

On January 29, 2025, the Bank of Canada (BoC) cut its interest rate by 25 basis points, bringing it to 3%. This decision, the sixth consecutive reduction, stems from a weak economy and persistently low inflation. Additionally, the BoC warned that the 25% tariffs the United States plans to impose on Canadian imports could cause significant economic harm. In response, the Canadian dollar weakened against the U.S. dollar, with the USD/CAD pair reaching levels near 1.4400.

Conversely, the U.S. Federal Reserve is expected to keep its interest rate unchanged in the 4.25%-4.50% range. Attention is focused on statements from Fed Chair Jerome Powell, especially regarding the impact of President Donald Trump's economic policies, such as the proposed tariffs, which could influence the future stance of monetary policy.

In summary, while the Bank of Canada continues with an expansionary monetary policy due to internal economic concerns and external threats like U.S. tariffs, the Federal Reserve maintains a more cautious stance, observing the development of trade policies and their impact on the economy. These divergences in monetary policies and trade tensions have contributed to the recent depreciation of the Canadian dollar against the U.S. dollar.

Technical Analysis

USDCAD, H2

Supply Zones (Sell): 1.45

Demand Zones (Buy): 1.4439, 1.4396, and 1.4330

The pair has been consolidating for just over a month after reaching March 2020 levels. However, it maintains a bullish bias, with the last validated intraday support at the 1.4369 level.

In this context, we observe a rebound in the initial sessions, breaking through supply zones at 1.4439 and 1.4465, confirming bullish dominance. Additionally, the rebound leaves a demand zone at the origin, very close to the daily opening around 1.4396, a zone that may be revisited in search of liquidity to continue purchases with targets in the average bullish range at 1.4484, 1.45, and 1.4516 in the short term.

However, a more aggressive decline below the demand zone around 1.4396 may signal bearish intent if it attempts to break the last validated intraday support at 1.4369.

Technical Summary

- Bullish Continuation Scenario: Consider buying at a price above 1.4420 and 1.44, with targets at 1.4484, 1.45 and 1.4516 in extension.

- Bearish Corrective Scenario: Sell below 1.45, with targets at 1.4470 and 1.4450, from where purchases could be considered.

- Bearish Reversal Scenario: Activated after the support at 1.4369 is broken, with the target at the demand zone of 1.4330.

Always wait for the formation and confirmation of an Exhaustion/Reversal Pattern (ERP) on the M5 timeframe, as taught here: https://t.me/spanishfbs/2258, before entering any trade in the key zones indicated.

Uncovered POC: POC = Point of Control: It is the level or zone where the highest concentration of volume occurred. If previously, a downward movement originated from it, it is considered a sell zone and forms a resistance area. Conversely, if an upward impulse originated from it, it is considered a buy zone, usually located at lows, forming support areas.

Oil Price Update – Brent Continues to Struggle as Technicals Offer Bulls Hope

- Oil prices are struggling due to uncertainty around tariffs and their impact on global demand.

- Libya supply fears were alleviated as exports returned to normal after discussions with protesters.

- US inventories rose, but total US oil demand also increased, offsetting downward pressure on oil prices.

- From a technical analysis standpoint, Brent has tapped into a key area of support and formed a double bottom pattern.

Oil prices continue to struggle to gain any sort of bullish traction as uncertainties around tariffs and the impact it will have on Global Demand continue to weigh on the minds of market participants. Meanwhile, comments earlier this week by US President Trump have put OPEC in a corner with the President saying he will speak to the group about lowering prices.

Libya Supply Fears Alleviated

Oil prices received a bit of a boost yesterday with news that protesters in Libya threatened to block Crude Oil exports via two terminals.

These fears were alleviated as the State Oil company reportedly talked to protesters and exports returned to normal.

The National Oil Corporation released a statement on Tuesday per Reuters, stating that operations are proceeding without interruption across all fields and ports, subsequent to discussions held with protesters who conducted a demonstration this morning at the ports of (Es Sider) and Ras Lanuf.

Tariff Threats Continue to Offer Support to Crude Oil Prices. A Double Edged Sword of Sorts?

Tariff threats continue to ramp up with markets expecting US President Donald Trump to slap a 25% tariff on all goods from Canada and Mexico.

The President has said this will come into effect on February 1st, with many market participants and analysts of the view that this will make Brent Crude more expensive.

For context, In 2023, Canada sent 3.9 million barrels of oil per day to the U.S., making up about half of all U.S. oil imports. Mexico supplied 733,000 barrels per day, according to the Energy Information Administration. Tariffs may also impact refined products such as gasoline, while an increase in transport costs may also factor in.

At the moment there does appear to be some back and forth between President Trump and Treasury Secretary Scott Bessent on the tariff issue. According to reports, Bessent would like to introduce tariffs gradually,starting at 5%. However, yesterday President Trump pushed back against this idea suggesting tariffs on individual products and items.

Such uncertainty will do little to ease the concerns of market participants who are already adopting a cautious approach as they weigh up the potential impact of tariffs. Much like with Gold, this is a double edged sword as market participants are concerned about the impact on global growth, while on the other hand we have the idea that tariffs will lead to an increase in Oil and refined products.

US Inventories on the Rise

Earlier we had data from the EIA regarding US crude inventories which rose by 3.5 million barrels to 415.1 million barrels in the week ended Jan. 24. This could have added further strain to Oil prices but the data also showed total U.S. oil demand rose last week.

This could have offset any downward pressure on Oil prices as demand continues to thrive.

Looking ahead, we do have a significant amount of US Dollar news to end the week. However, I do not expect many surprises with the tariff picture and geopolitical risks remaining the biggest factors to pay attention to.

Technical Analysis – Brent Crude

This is a follow-up analysis of my prior report “Oil Prices Slide – Brent Crude Taps 200-day MA. Can it Snap 4-day Losing Streak?” published on 13 January 2025.

From a technical analysis standpoint, Brent has tapped into a key area of support where the previous impulsive move to the upside began following a period of consolidation.

The key level serving as support is 76.35 with crude oil hovering above for the past three days. A sign of bearish exhaustion?

Brent Crude Oil Daily Chart, January 29, 2025

Source: TradingView (click to enlarge)

Dropping down to a four-hour chart and as you can see price has formed a double bottom pattern at the key support level of 76.35.

The 200-day MA adds another layer of support as it rests at 76.65 and currently supports prices.

In order for the double bottom pattern to play out, oil prices need to record a four-hour candle close above the previous swing high resting at 77.57 which could embolden bulls and see prices make a swift return toward the psychological 80.00 a barrel mark.

Oil is another prime example of the conundrum facing market participants at the moment where the fundamental and technical outlooks appear to be diverging. This makes it hard for market participants and may not get any easier until a clear path forward on tariffs is established.

Brent Crude Oil Four-Hour (H4) Chart, January 29, 2025

Source: TradingView (click to enlarge)

Support

- 76.35

- 75.00 (psychological level)

- 72.38

Resistance

- 78.97

- 80.00 (psychological level)

- 81.58

Australian Dollar Extends Losses on Soft Aussie CPI

The Australian dollar is down for a third straight trading day and has declined 1.3% this week. In the North American session, AUD/USD is trading at 0.6228, down 0.37% on the day.

Australian CPI falls to 2.4%

Australia’s annual inflation rate dropped to 2.4% in the fourth quarter of 2024 from 2.8% in Q3. This was below the market estimate of 2.5% and was the lowest reading since Q1 2023. Electricity prices were sharply lower due to an energy bill rebate and services inflation dropped to 4.3% from 4.6%, its lowest level in three quarters. On a quarterly basis, CPI remained unchanged at 0.2% in Q4, below the market estimate of 0.3%.

The Reserved Bank of Australia’s trimmed mean CPI, a key indicator of underlying inflation, slowed to 0.5% q/q in Q4, lower than 0.8% in Q3 and below the market estimate of 0.6%. Annually, trimmed mean CPI fell to 3.2%, compared to a revised 3.6% in Q3 and below the market estimate of 3.3%.

The soft inflation report has raised expectations that the RBA will lower rates at the Feb. 18 meeting, with the market pricing in a quarter-point cut at 80%. That would bring the cash rate to 4.10%, its lowest since Oct. 2023. Today’s inflation report has added significance as it is the final tier-1 event prior to next month’s rate meeting.

Investors are awaiting the Federal Reserve’s rate announcement later today, although it would be a massive surprise if the Fed did not maintain the current benchmark interest rate of 4.25%-4.5%. The Fed has cut rate three consecutive times, including a jumb0 half-point chop in September 2024, but the resilient US economy has stalled plans to aggressively lower rates further and currently the Fed is projected to cut rates only once or twice in 2025.

AUD/USD Technical

- AUD/USD is testing support at 0.6228. Below, there is support at 0.6204

- 0.6262 and 0.6286 are the next resistance lines

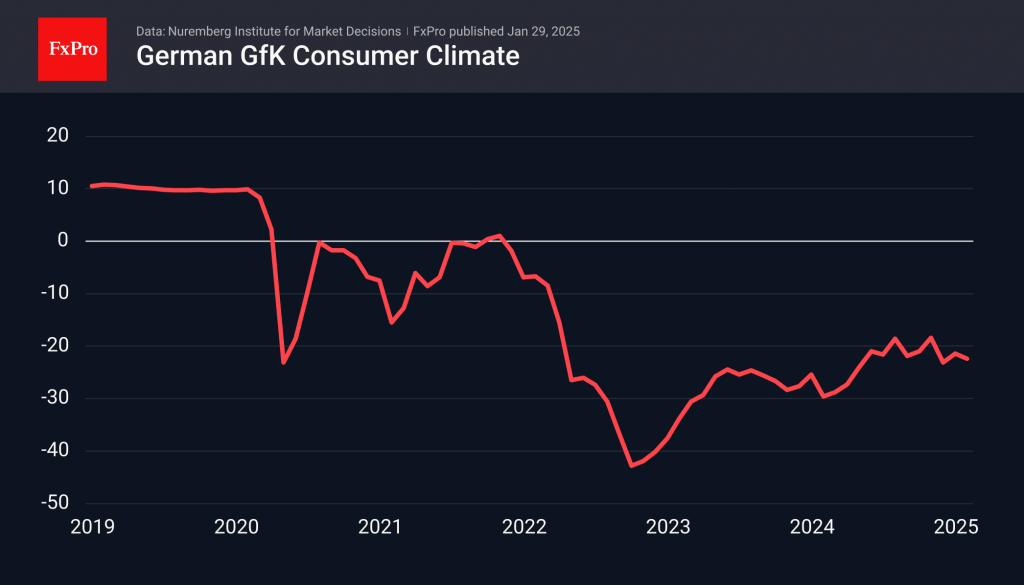

Euro Pressured by German Pessimism

The German Consumer Climate Index declined in January, impacting the eurozone’s largest economy and applying pressure on the single currency. The index fell by 1 point to -22.4 by February, having remained deeply negative since late 2021 without showing an upward trend since mid-last year. The report highlights a decrease in income expectations and purchase intentions, potentially linked to an increase in inflation.

Furthermore, the German Ministry of Economic Affairs adjusted its GDP growth forecast for 2025 from 1.1% to 0.3%, following contractions of 0.3% and 0.2% in 2023 and 2024, respectively. This economic situation underscores the need for continued monetary policy easing by the ECB despite indications of rising inflation.

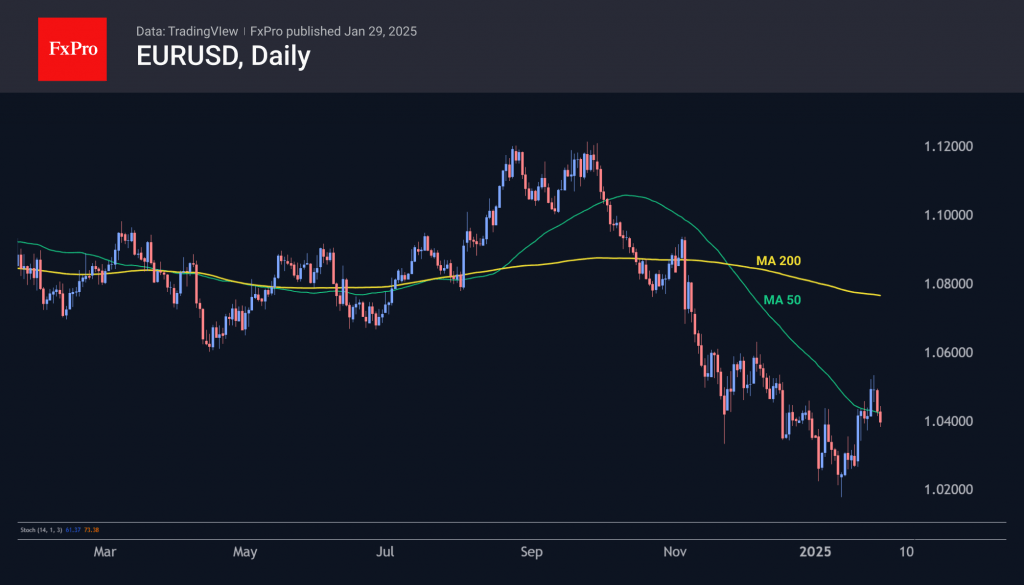

Market participants are anticipating further rate cuts from the ECB, with expectations of a quarter-point reduction this coming Thursday and additional cuts later this year. In contrast, about two cuts are expected from the Fed and the Bank of England, with the possibility of fewer reductions in the US.

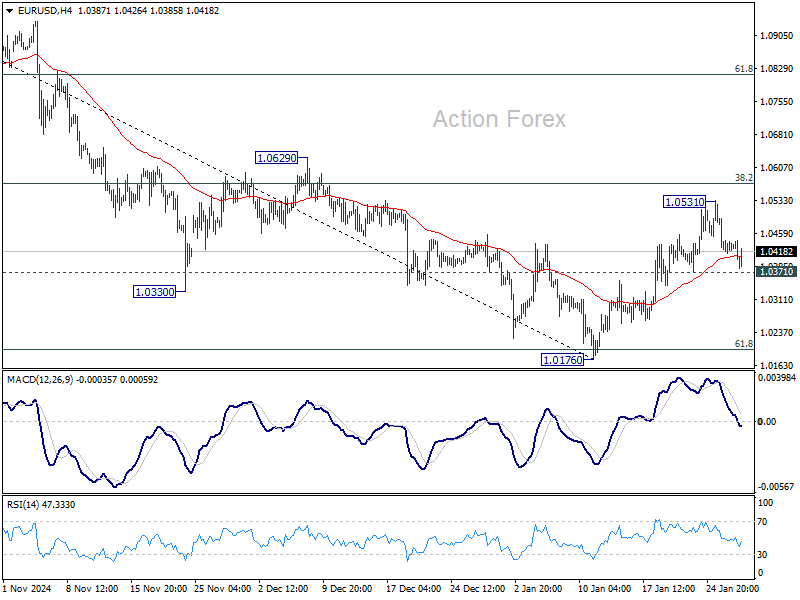

These market expectations suggest a potential decline in the euro against the dollar and pound, influenced by technical factors. The EURUSD rally from 13 to 27 January appears to be a technical rebound following the decline since October. The recovery lost momentum after surpassing the 50-day moving average and the 1.05 level. EURUSD is likely to consolidate below the 1.05 level, which could lead to declines below parity.

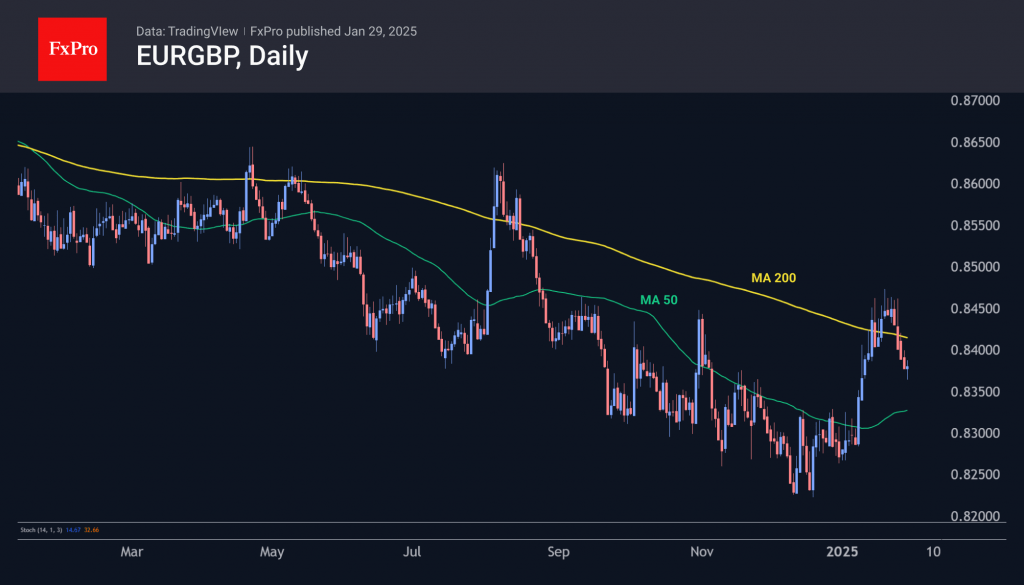

Regarding macroeconomic factors, especially consumer demand, the euro also seems weaker compared to the pound. The EURGBP pair declined for the fifth consecutive trading session, completing its technical rebound. Bearish sentiment resumed after reaching the 200-day moving average level. The euro has been depreciating against the pound since October 2023. The pair is approximately 1.75% above cyclical lows at 0.8250 but may retest these levels in the coming weeks. Consolidation below this mark could result in a fundamental reassessment of attitudes towards the euro, similar to the period in 2014-2015 when EURGBP fell below 0.7000.

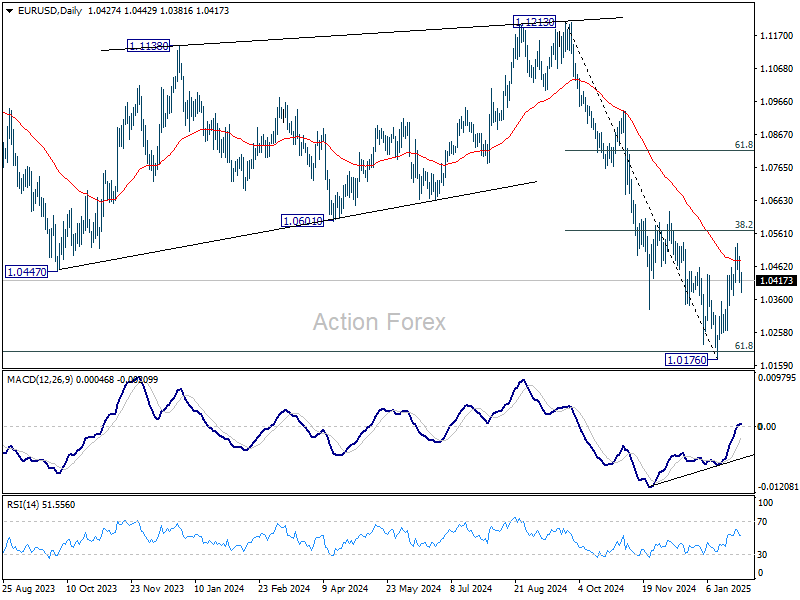

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0398; (P) 1.0447; (R1) 1.0480; More...

Outlook in EUR/USD is unchanged and intraday bias remains neutral. On the downside, break of 1.0371 support will indicate rejection by 38.2% retracement of 1.1213 to 1.0176 at 1.0572 and retain near term bearishness. Retest of 1.0176 low should be seen next. On the upside, though, decisive break of 1.0572 will raise the chance of bullish reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, outlook is mixed as fall from 1.1274 (2023 high) could either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. Strong support from 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will favor the former case, and sustained break of 55 W EMA (now at 1.0722) will argue that the third leg might have started. However, sustained trading below 1.0199 will favor the latter case and bring retest of 0.9534 low.

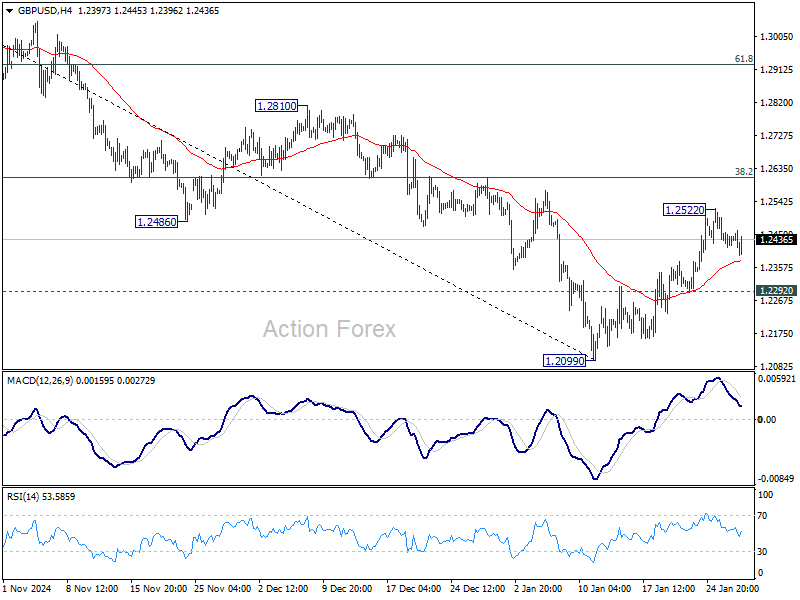

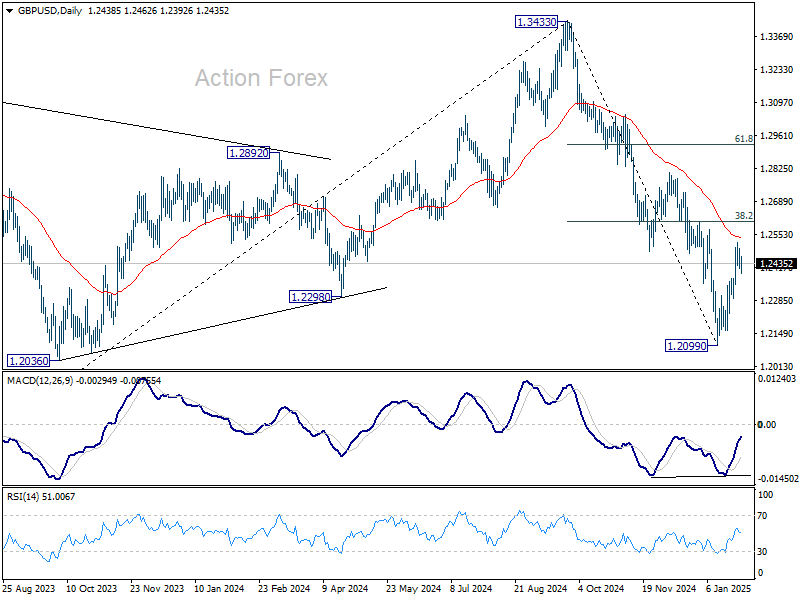

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2404; (P) 1.2453; (R1) 1.2491; More...

Outlook in GBP/USD is unchanged and intraday bias stays neutral first. Rebound from 1.2099 is seen as a corrective move. While another rise cannot be ruled out, strong resistance could be seen 38.2% retracement of 1.3433 to 1.2099 at 1.2609 to limit upside. On the downside, below 1.2292 minor support will bring retest of 1.2099 low. However, sustained trading above 1.2609 will raise the chance of reversal and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

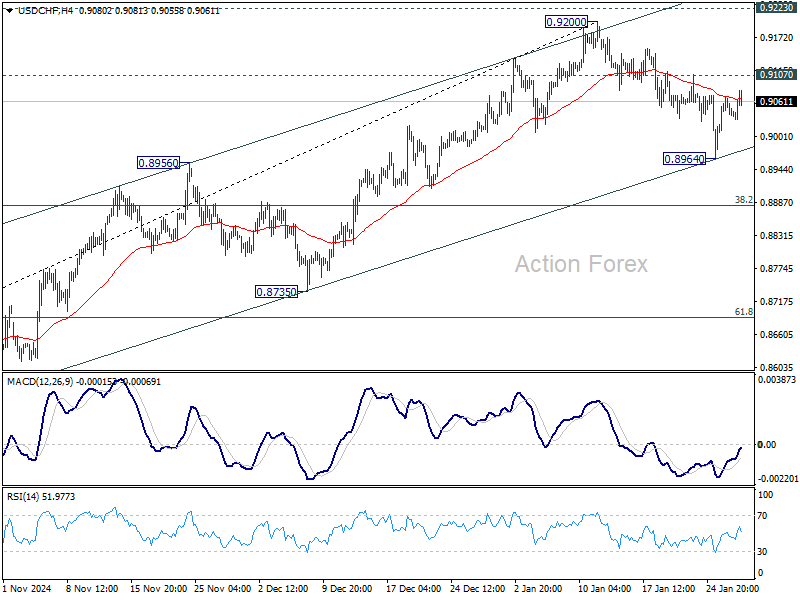

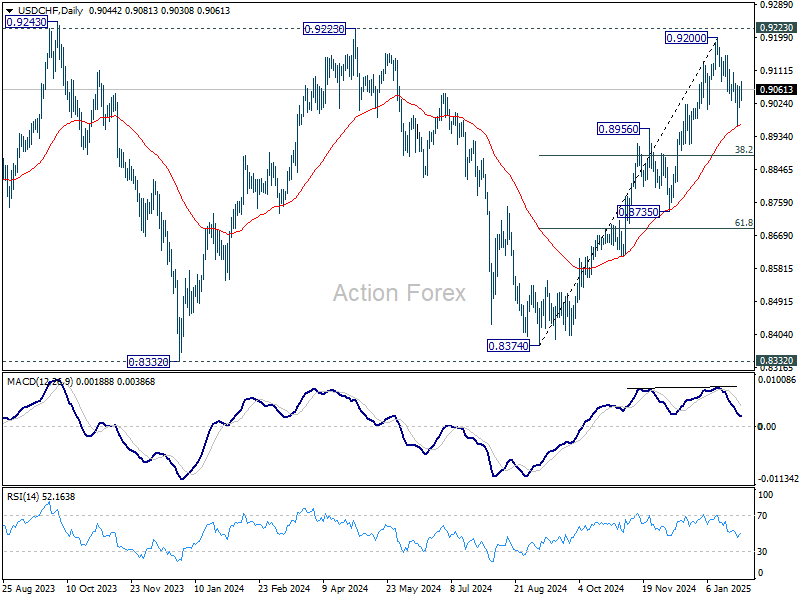

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9012; (P) 0.9041; (R1) 0.9071; More…

Outlook in USD/CHF is unchanged and intraday bias remains neutral. Rise from 0.9374 remains intact so far with strong support seen from near term rising channel. On the upside, break of 0.9107 will target 0.9200 and 0.9223 key resistance. On the downside, however, break of 0.8964 will resume the fall from 0.9200 to 38.2% retracement of 0.8374 to 0.9200 at 0.8884 next.

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.

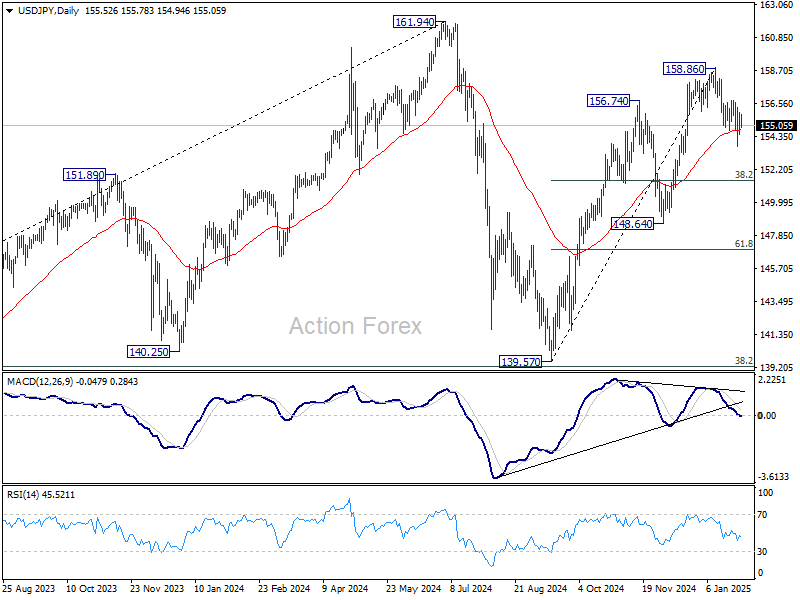

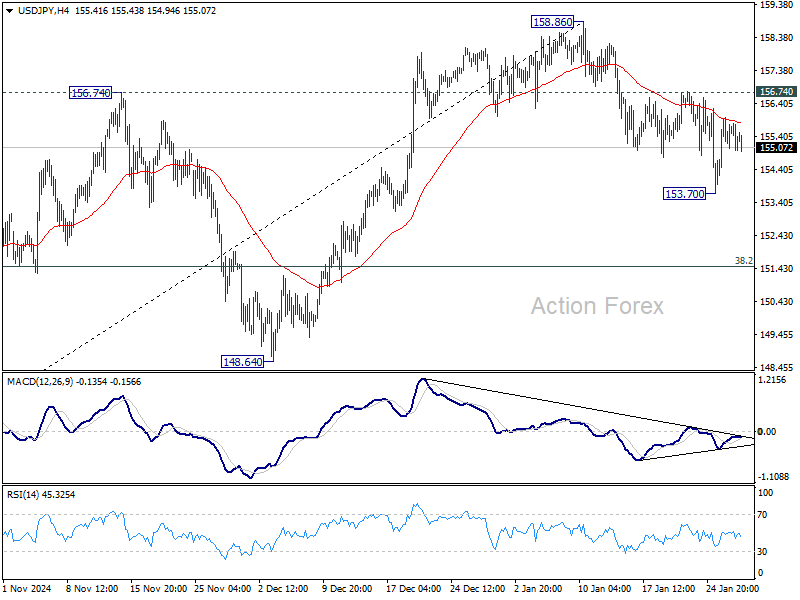

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.61; (P) 155.30; (R1) 156.21; More...

Outlook in USD/JPY remains unchanged and intraday bias stays neutral. On the upside, break of 156.74 resistance will indicate that fall from 158.86 has completed as a correction. Intraday bias will be back on the upside for 158.86 and above to resume the whole rally from 138.57. On the downside, below 153.70 will resume the fall from 158.86 to 38.2% retracement of 139.57 to 158.86 at 151.49.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.