Sample Category Title

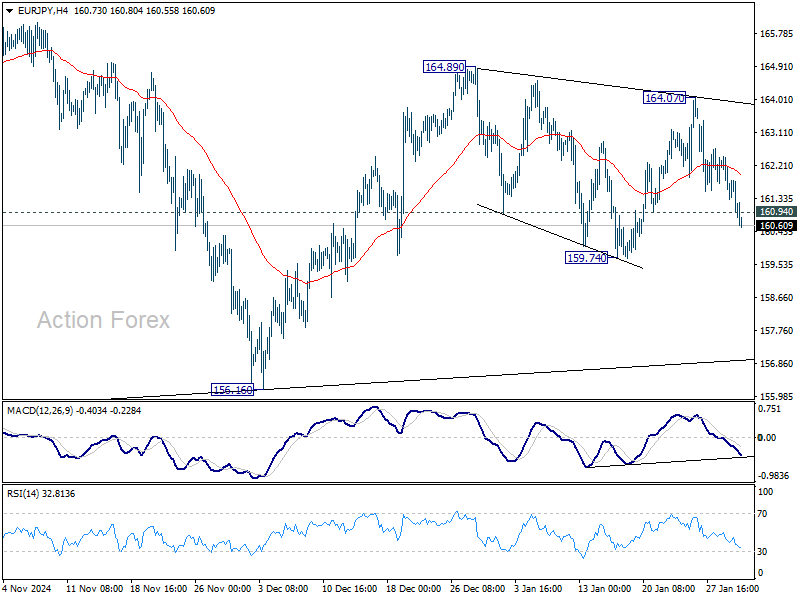

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.23; (P) 161.86; (R1) 162.41; More...

Intraday bias in EUR/JPY is back on the downside with break of 160.94 minor support. Deeper decline would be seen to 159.74 support and below. But overall, price actions from 154.40 are seen as a corrective pattern, which might still extend further.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8355; (P) 0.8378; (R1) 0.8393; More...

Intraday bias in EUR/GBP remains on the downside at this point. Sustained break of 55 D EMA (now at 0.8355) will argue that whole rebound from 0.8221 has completed at 0.8472 as a corrective move. Nevertheless, strong bounce from the 55 D EMA, followed by break of 0.8397 minor resistance, will argue that the pull back has completed and bring retest of 0.8472.

In the bigger picture, a medium term bottom should be in place at 0.8221, just ahead of 0.8201 key support (2022 low). Sustained trading above 55 W EMA (now at 0.8442) will pave the way to 0.8624 cluster zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621), even just as a correction to the down trend from 0.9267 (2022 high). But still, medium term outlook will be neutral at best as long as 0.8621/4 holds.

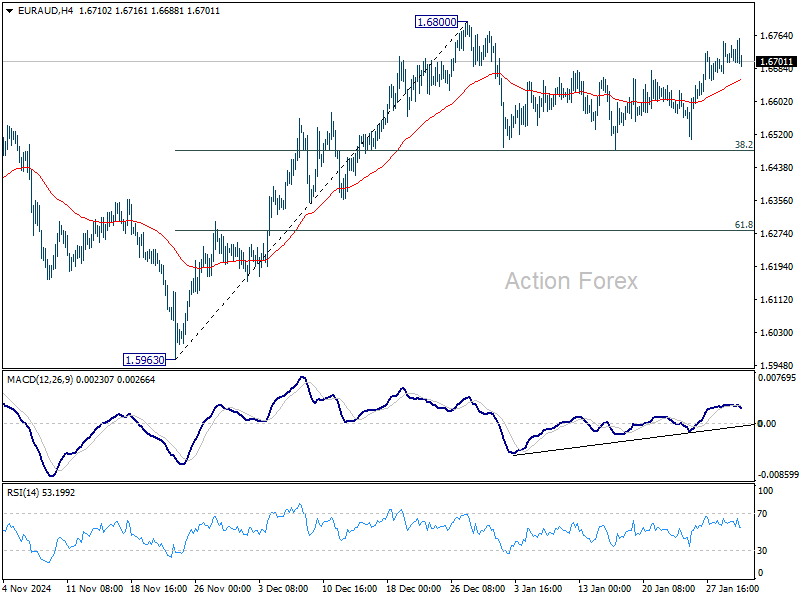

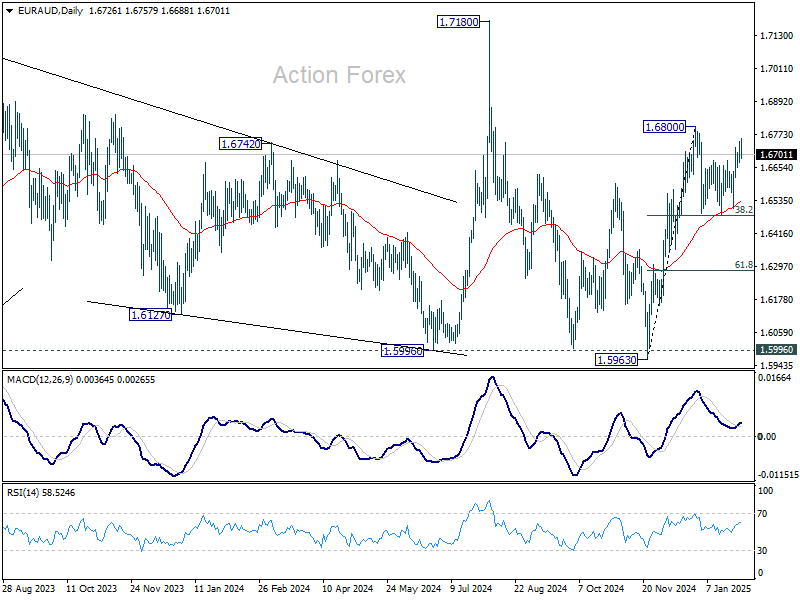

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6679; (P) 1.6715; (R1) 1.6756; More...

Range trading continues in EUR/AUD below 1.6800 and intraday bias remains neutral. In case of another dip, strong support is expected from 38.2% retracement of 1.5963 to 1.6800 at 1.6480 to contain downside. On the upside, firm break of 1.6800 will resume the rally from 1.5963. However, sustained break of 1.6480 will bring deeper correction 61.8% retracement at 1.6283 instead.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support (2024 low) despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

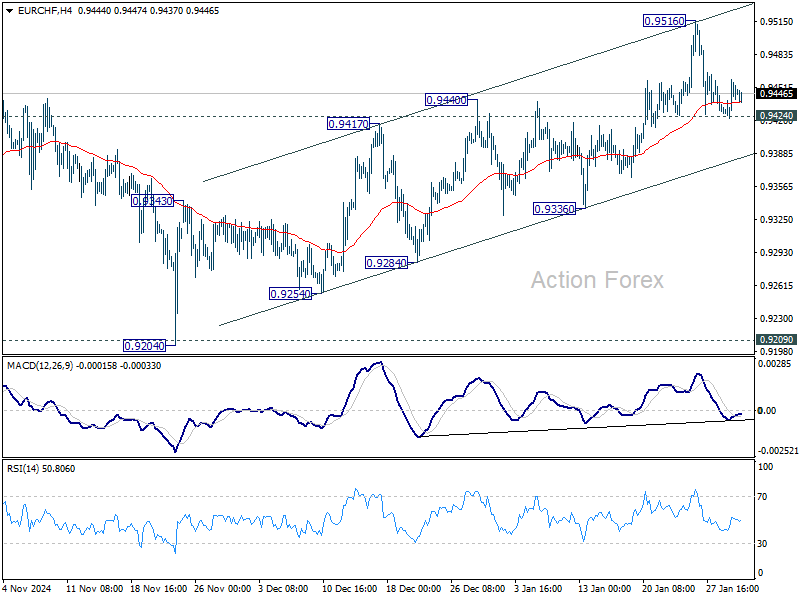

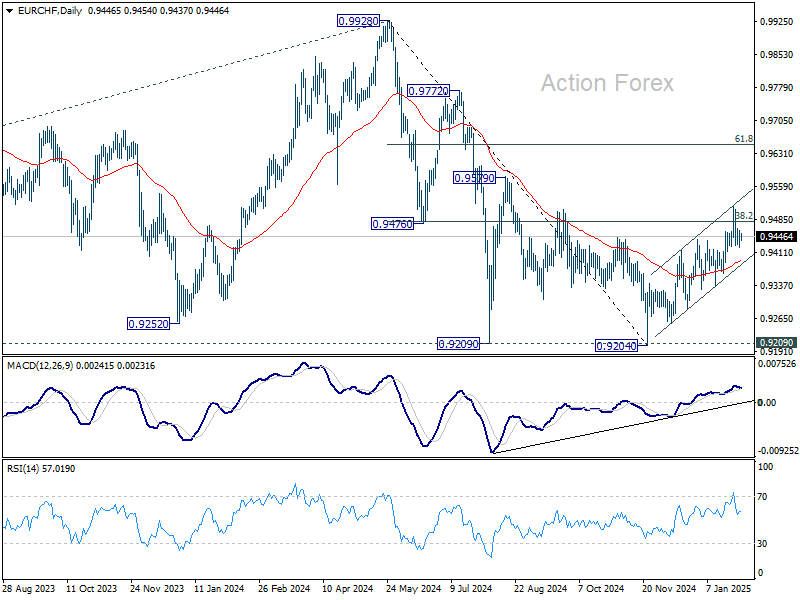

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9428; (P) 0.9444; (R1) 0.9466; More....

EUR/CHF is still bounded in range of 0.9424/9516 and intraday bias remains neutral. On the downside, firm break of 0.9424 support will indicate rejection by 38.2% retracement of 0.9928 to 0.9204 at 0.9481. Deeper fall would then be seen back to channel support (now at 0.9377). However, strong rebound from current level will keep the choppy rally from 0.9204 intact.

In the bigger picture, fall from 0.9928 should have completed at 0.9204 with the current strong rebound, after failing to sustain below 0.9252 (2023 low). It's still early to confirm long term bullish reversal. But even as a corrective move, current rebound could extend to 61.8% retracement of 0.9928 to 0.9204 at 0.9651. On the downside, firm break of 55 D EMA (now at 0.9390) will maintain medium term bearishness and bring retest of 0.9204 low.

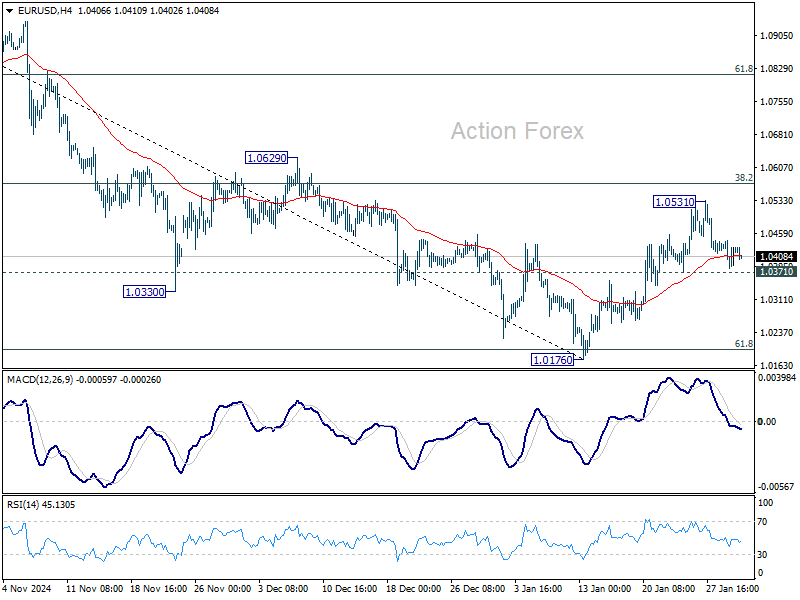

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0387; (P) 1.0415; (R1) 1.0449; More...

Intraday bias in EUR/USD remains neutral for the moment. On the downside, break of 1.0371 support will indicate rejection by 38.2% retracement of 1.1213 to 1.0176 at 1.0572 and retain near term bearishness. Retest of 1.0176 low should be seen next. On the upside, though, decisive break of 1.0572 will raise the chance of bullish reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, outlook is mixed as fall from 1.1274 (2023 high) could either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. Strong support from 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will favor the former case, and sustained break of 55 W EMA (now at 1.0722) will argue that the third leg might have started. However, sustained trading below 1.0199 will favor the latter case and bring retest of 0.9534 low.

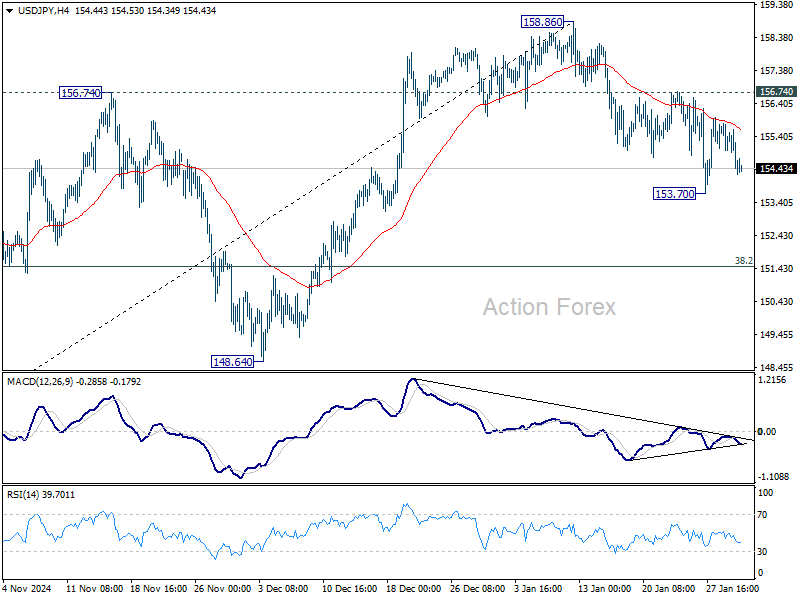

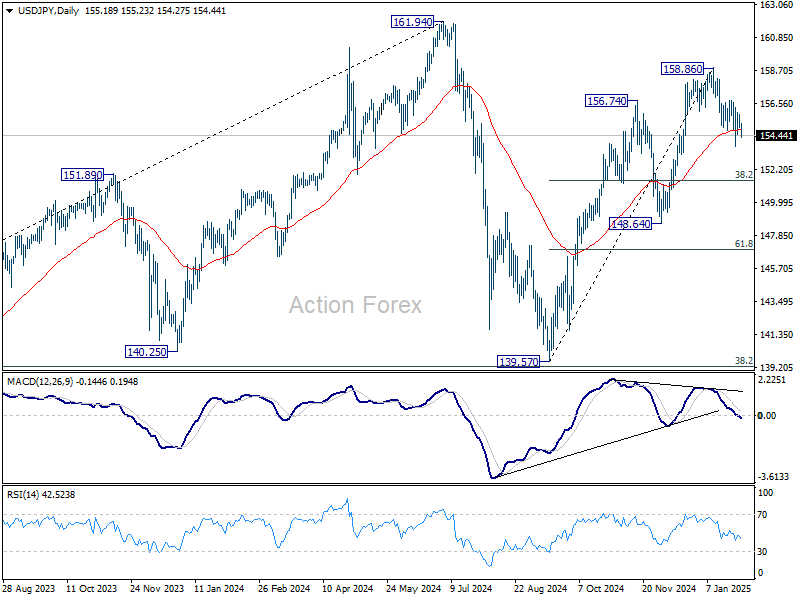

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.86; (P) 155.33; (R1) 155.71; More...

Intraday bias in USD/JPY remains neutral at this point. On the upside, break of 156.74 resistance will indicate that fall from 158.86 has completed as a correction. Intraday bias will be back on the upside for 158.86 and above to resume the whole rally from 138.57. On the downside, below 153.70 will resume the fall from 158.86 to 38.2% retracement of 139.57 to 158.86 at 151.49.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

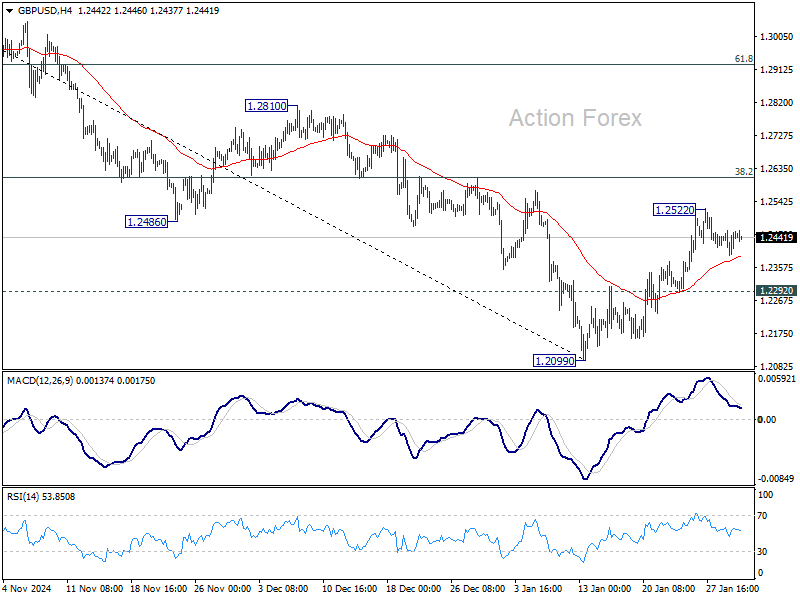

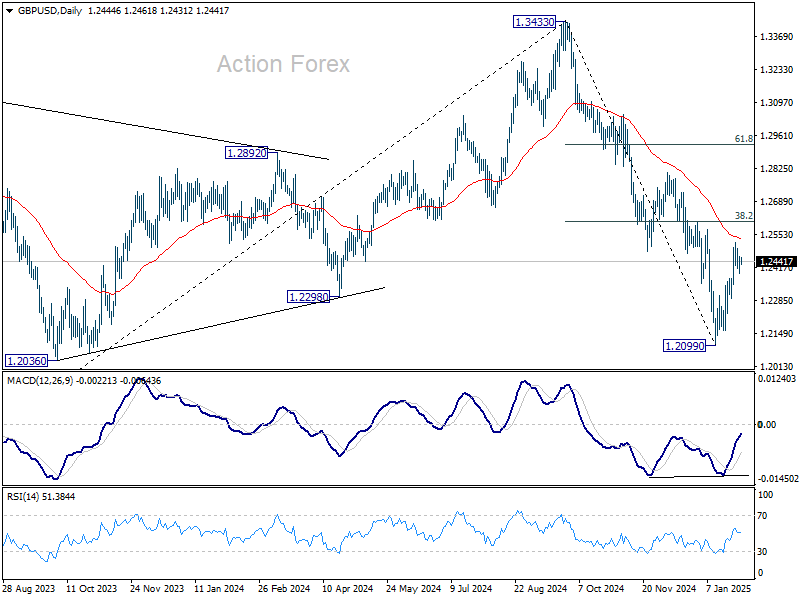

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2409; (P) 1.2436; (R1) 1.2480; More...

Intraday bias in GBP/USD remains neutral for the moment. Rebound from 1.2099 is seen as a corrective move. While another rise cannot be ruled out, strong resistance could be seen 38.2% retracement of 1.3433 to 1.2099 at 1.2609 to limit upside. On the downside, below 1.2292 minor support will bring retest of 1.2099 low. However, sustained trading above 1.2609 will raise the chance of reversal and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

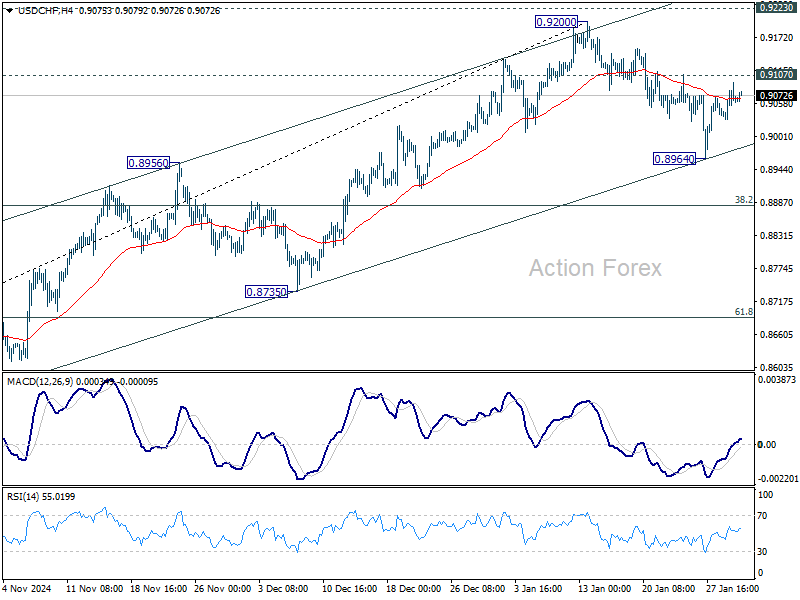

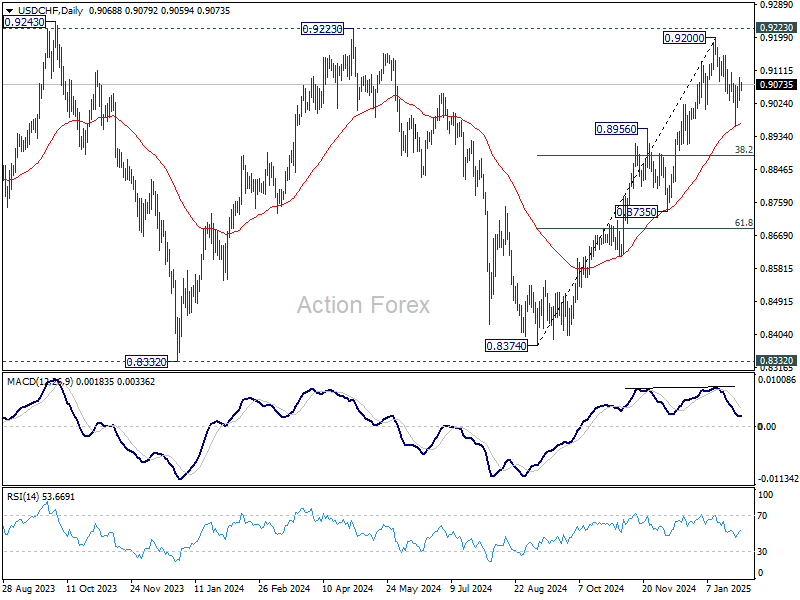

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9036; (P) 0.9065; (R1) 0.9099; More…

Intraday bias in USD/CHF remains neutral for the moment. Rise from 0.9374 stays intact with strong support seen from near term rising channel. On the upside, break of 0.9107 will target 0.9200 and 0.9223 key resistance. On the downside, however, break of 0.8964 will resume the fall from 0.9200 to 38.2% retracement of 0.8374 to 0.9200 at 0.8884 next.

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.

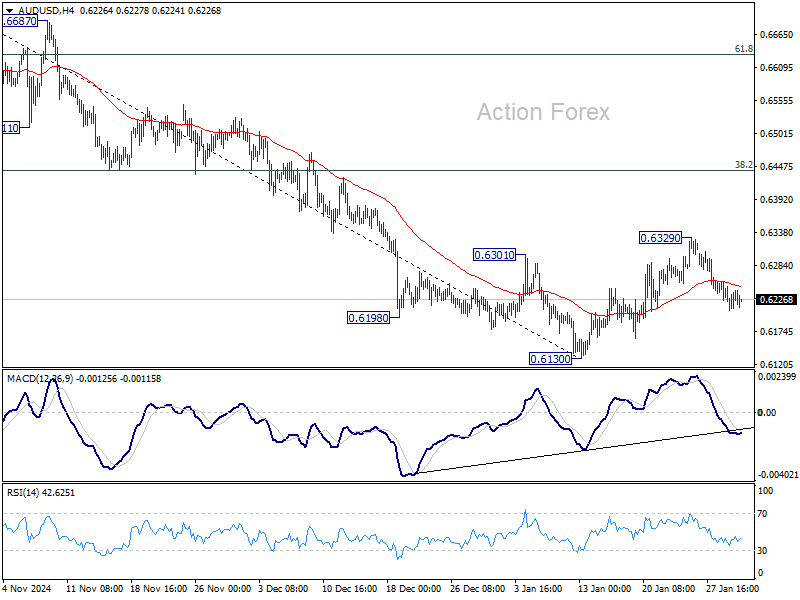

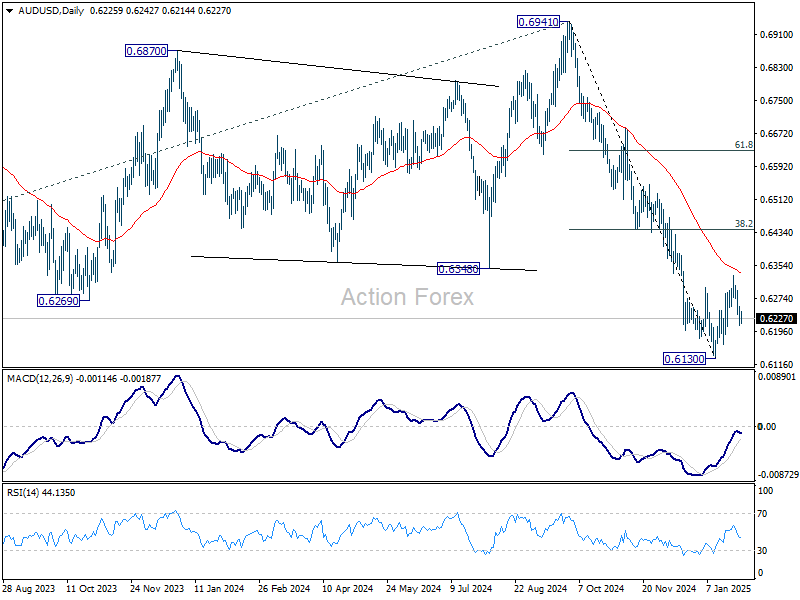

AUD/USD Daily Report

Daily Pivots: (S1) 0.6208; (P) 0.6234; (R1) 0.6257; More...

No change in AUD/USD's outlook for now, and intraday bias stays mildly on the downside. Corrective rebound from 0.6130 could have completed at 0.6329. Deeper fall would be seen to retest 0.6130 low. On the upside, above 0.6329 will resume the rebound. But still, strong resistance is expected from 38.2% retracement of 0.6941 to 0.6130 at 0.6440 to limit upside to complete this corrective rebound.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6545) holds.

USD/CAD Chart Analysis Following Bank of Canada’s Rate Cut

Unlike the Federal Reserve, which opted to leave its monetary policy unchanged, the Bank of Canada cut its interest rate yesterday. According to Forex Factory, as expected by analysts, the Overnight Rate was lowered by 25 basis points from 3.25% to 3.00%.

According to Reuters:

→ The Bank of Canada reduced interest rates to support the economy ahead of anticipated US trade tariffs.

→ This weakened the Canadian dollar, as the gap between Canadian and US bond yields widened.

→ Market participants estimate a 41% probability that the Bank of Canada will cut rates again in March.

→ The depreciation of the Canadian dollar is also influenced by oil prices (one of Canada’s key export commodities), which have fallen by over 8% since their mid-January peak.

Technical analysis of the USD/CAD chart indicates that the Canadian dollar’s exchange rate against the US dollar is forming a “Megaphone” pattern, with price action demonstrating the presence of selling pressure. On 21 January, sellers sharply pushed the price down from the psychological level of 1.4500, and yesterday, the price made a bearish reversal from 1.4450.

There is a possibility that seller activity could drive USD/CAD lower towards a key trendline (marked in grey) that has been forming since the second half of 2024.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.