Sample Category Title

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4932; (P) 1.4982; (R1) 1.5024; More....

EUR/AUD lost momentum after hitting 1.5031 and intraday bias is turned neutral again. Above 1.5031 will target 1.5173/5226 resistance zone first. Break will resume medium term rally from 1.3624. On the downside, below 1.4811 will turn bias to the downside and extend the fall from 1.5173 to retest 1.4421 support.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the price actions from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 support will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

XAUUSD Intraday Analysis

XAUUSD (1312.44): Gold prices were slightly bullish yesterday, but price action suggests cautious trading. The modest reversal off the lows near 1305.00 suggests a minor correction to the upside. Resistance is seen at 1320 - 1324 which will need to be breached in order for further gains to be logged. A breakout above this resistance will signal a move towards 1345.87. However, in the event that gold prices fail to break the resistance, the downside could see gold prices falling to 1300.00 support level.

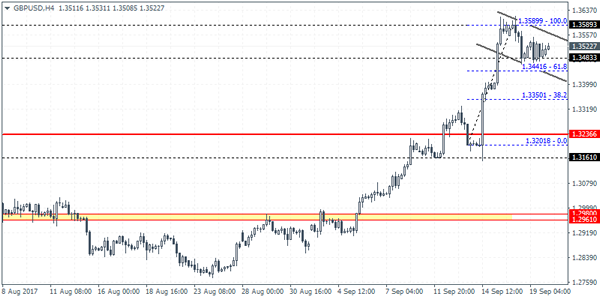

GBPUSD Intraday Analysis

GBPUSD (1.3522): GBPUSD has been seen consolidating after price touched highs of 1.3566. The consolidation in price action suggests a bullish flag pattern that has formed. A range has also been established with support at 1.3483 and 1.3589. A breakout from this level will suggest further direction in the currency pair. The bias is for an upside breakout. This will potentially suggest further gains to come with the price likely to target 1.3670 followed by 1.3830. In the event that the bullish flag fails, we can expect the downside to test 1.3236.

Trade Idea: EUR/JPY – Buy at 132.40

EUR/JPY - 133.72

Original strategy:

Buy at 132.00, Target: 134.00, Stop: 131.40

Position: -

Target: -

Stop: -

New strategy :

Buy at 132.40, Target: 134.40, Stop: 131.80

Position: -

Target: -

Stop:-

As the single currency has maintained a firm undertone after recent rally, adding credence to our view that recent upmove is still in progress and bullishness remains for further gain to 134.50-60, then towards 135.00-10, however, near term overbought condition should limit upside and reckon 135.55-60 would hold from here, risk from there is seen for a retreat to take place later.

In view of this, we are looking to reinstate long on pullback as 132.30-40 should limit downside and bring another rise. Below support at 132.27 would defer and risk test of previous resistance at 132.01 (should turn into support) but only break there would signal a temporary top is formed, bring correction to 131.40-50 first.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

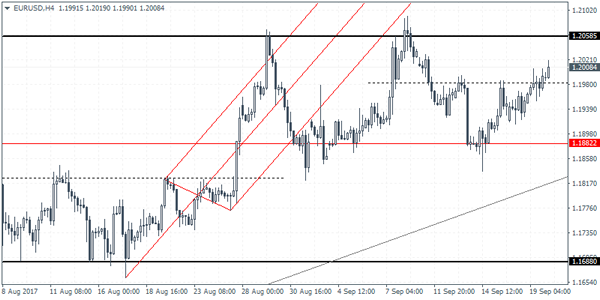

EURUSD Intraday Analysis

EURUSD (1.2008): The euro currency posted steady gains for the past five consecutive days with price action breaking above 1.1954. On the 4-hour chart, the inverse head and shoulders pattern that was formed has been validated and price action is likely to rally towards 1.2060 which marks the measured move. However, the rally to 1.2060 will be critical as it coincides with the resistance level that was previously tested. Failure to break out above this level could keep EURUSD trading in the range. To the downside, price action will need to push lower towards the 1.1882 support level. A break down below this support will push EURUSD to new lows and possibly the correction. To the upside, 1.2200 will be the next target on a successful breakout above 1.2060.

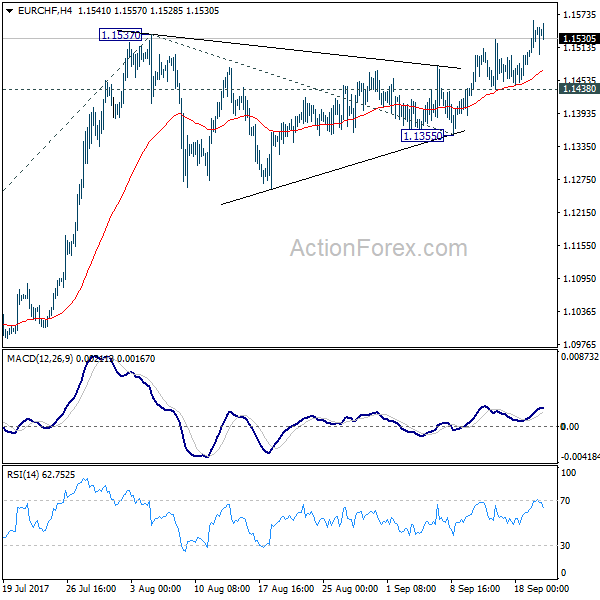

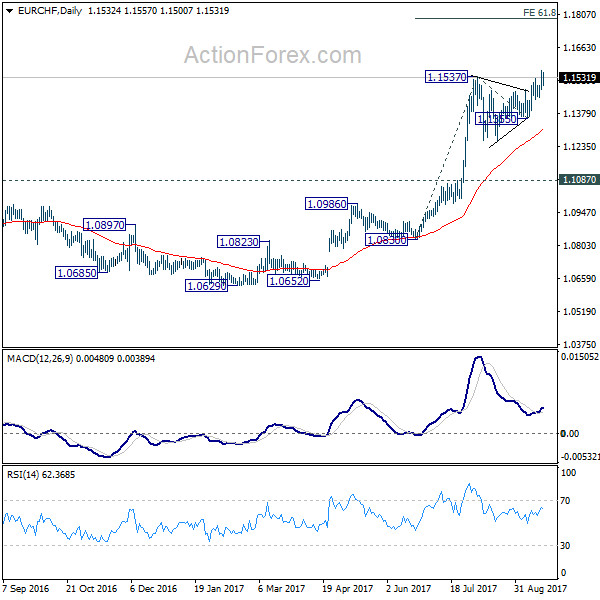

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1498; (P) 1.1531; (R1) 1.1576; More... .

Intraday bias in EUR/CHF remains on the upside for the moment. Prior break of 1.1537 resistance indicates resumption of medium term rise. Further rally should be seen to the upside for 61.8% projection of 1.0830 to 1.1537 from 1.1355 at 1.1792 next. However, considering weak upside momentum so far, break of 1.1438 will turn focus back to 1.1355 support instead.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

Markets Await FOMC Meeting Today

The markets were trading fairly subdued although the US dollar was seen easing back. Economic data over the day included the German ZEW economic sentiment rising to 17.0, beating estimates of 12.3. The Eurozone ZEW economic sentiment was however soft, rising just 31.7 falling below estimates of 32.4. Data from the US saw the building permits which increased 1.30 million, but housing starts remained sluggish at 1.18 million.

Looking ahead, the main event for the day will be the FOMC meeting. The Fed is expected to announce it balance sheet normalization at today's meeting while keeping interest rates steady. The Fed will also be releasing its dot plot giving fresh forecasts on GDP, inflation and interest rates. Later in the day, New Zealand GDP is expected to show a quarterly GDP growth rate of 0.8%.

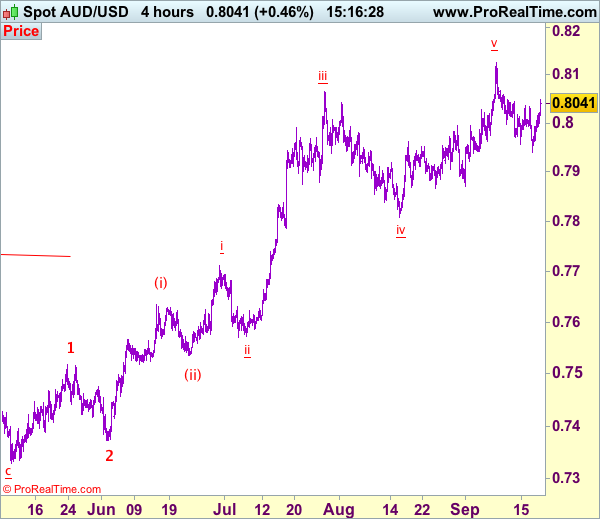

Trade Idea: AUD/USD – Stand aside

AUD/USD – 0.8040

Original strategy:

Sell at 0.8080, Target: 0.7900, Stop: 0.8140

Position: -

Target: -

Stop:-

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Despite falling to 0.7940, as aussie found good support there and has staged a strong rebound, suggesting near term upside risk remains for gain to 0.8080-90, however, reckon upside would be limited and resistance at 0.8125 (this month’s high) would hold, bring further consolidation. Only break of this level would revive bullishness and extend recent upmove to 0.8150-60, then towards 0.8190-00 later this week.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below 0.7985-90 would bring another test of said support at 0.7940 but only break there would signal top has been formed at 0.8125, bring retracement of recent rise to 0.7920-25 and later 0.7890-00 but support at 0.7867-71 should remain intact.

On the 4-hour chart, recent upmove from 0.7329 is unfolding as an impulsive rise with wave 3 as well as smaller degree wave (iii) extending, only minor wave v of (iii) has ended at 0.8125, hence bullishness remains for this move to extend headway to 0.8200, then towards 0.8300, however, reckon upside would be limited to 0.8400 and the final wave 5 should falter below 0.8500, bring correction probably next week.

North Korean Rocket Man Didn’t Have Any Strong Risk-Off Sentiment To Currency Markets, Traders Await FOMC Decision

Dollar Edged Up Ahead of Federal Reserve's Meeting. The dollar index added 0.1 percent to 91.855, holding well above its more than 2-1/2 year low of 91.011 plumbed on Sept. 8. Analysts expect U.S. central bank policymakers to announce at the end of their two-day meeting later on Wednesday that they will trim its $4.2 trillion in bond holdings starting in October, and also leave the door open for an interest rate hike at their Dec. 12-13 meeting.

Strong Euro Driving a Rift Between ECB Policymakers. European Central Bank policymakers disagree on whether to set a definitive end-date for their money-printing program when they meet in October, raising the chance that they will keep open at least the option of prolonging it again. The euro was steady on the day, at $1.1990.

Yen Unmoved by Trump's Fiery North Korea Rhetoric at the U.N. The yen tends to benefit during times of economic and political uncertainty, but it had a muted reaction to U.S. President Donald Trump's speech to the U.N. General Assembly on Tuesday. This week the main factor for the yen is Japanese Prime Minister Shinzo Abe, who is considering calling an election for as early as next month. The U.S. currency was steady on the day against its Japanese counterpart at 111.56 yen, moving back toward an eight-week peak of 111.88 yen scaled overnight.

Precious Metals Retained Their Lead. Gold and silver remained supported as several market watchers are still wary of geopolitical risks stemming from Trump's latest batch of threats on North Korea. In his speech to the UN General Assembly, the U.S. President declared: “The United States has great strength and patience, but if it is forced to defend itself or its allies, we will have no choice but to totally destroy North Korea.”

Crude Oil Rises on Possible OPEC Cut Extension. Oil prices rose on Wednesday after Iraq's oil minister said OPEC and other crude producers were considering extending or even deepening a supply cut to curb a global glut, while a report showed a smaller-than-expected increase in U.S. inventories. US West Texas Intermediate (WTI) crude futures were up 34 cents at USD 49.82, Brent crude futures were 24 cents higher at USD 55.38. OPEC and producers including Russia have agreed to reduce output by about 1.8 million barrels per day until March 2018, when the agreement expires, in a bid to reduce global oil inventories and support prices.

Watch Out Today For:

08:00 am GMT: EUR Non-monetary policy's ECB meeting

19:00 pm GMT: USD Fed Interest Rate Decision

19:30 pm GMT: USD FOMC Press conference

Gold Testing The Sellers

Gold has come back to retest the broken uptrend line and the first warning line (WL1) of the major red descending pitchfork. Is traded above the $1312 per ounce and could climb much higher if the USD will drop further after the FOMC. A minor consolidation above the WL2 and above the $1303 per ounce will signal another rally towards the 250% Fibonacci line, despite the breakdown below the uptrend line.