Sample Category Title

USD Bears Return

USD bears returned to the market as the tensions between North Korea and the US have greatly 'cooled' this week. North Korean media reported that North Korea Leader Kim had delayed his decision to fire missiles towards Guam while he waited to see what the US did next. On Wednesday, President Trump praised North Korean leader Kim Jong Un for a 'wise' decision. Minutes, released on Wednesday, from the Fed’s July meeting showed the central bank growing warier about recent weak inflation data, with some policymakers wanting proof of inflation moving towards the Fed’s 2% rate before deciding on the next rate hike. In addition, the minutes also revealed that the uncertainty surrounding the fiscal, healthcare, and trade policies was holding back business investments – which will hamper domestic growth. The CME FedWatch tool is indicating that the markets are pricing a 46.8% probability of a 0.25% rate hike in December. GBP gained following data that revealed UK wages rose faster than expected in the three months to June, and the unemployment rate fell to 4.4% – its lowest since 1975.

EURUSD rose overnight to a high of 1.17896 following data that revealed Eurozone Q2 was revised to 2.2% (prev. 2.1%). EURUSD is currently trading around 1.1770

USDJPY declined 0.4% overnight hitting a low of 109.664. USDJPY is currently trading around 109.95

GBPUSD trades in a relatively narrow range of less than 30 pips in early trading. Currently GBPUSD is trading around 1.2890

Gold climbed 0.4% to $1,289.35 adding to Wednesday’s 0.9% increase. Gold is currently trading around $1,288

WTI edged higher but remains close to a near 4 week low touched earlier this week as US output hit a 2-year high offset by the 7th weekly drawdown in stockpiles. WTI is currently trading around $46.95pb

At 09:30 BST UK National Statistics will release Retail Sales for July. Forecasts are for a lower reading than previous across all time frames – notably Month-on-month expected at 0.2% (prev. 0.6%) and Year-on-year expected 1.4% (prev. 2.9%)

At 10:00 BST Eurostat will release CPI for Eurozone in July. CPI (YoY) & Core (YoY) is expected to be unchanged at 1.3% & 1.2% respectively. Any major deviation will impact ECB monetary policy with regards to future interest rate hikes.

At 12:30 BST the ECB Monetary Policy Meeting Accounts will be released. Markets will be looking at the rationale behind monetary policy decisions and economic growth prospects.

At 14:15 BST the Board of Governors of the Federal Reserve release US Industrial Production for July. Consensus calls for a decline to 0.3% from the previous reading of 0.4%.

At 17:30 BST Federal Reserve Bank of Dallas President Robert Kaplan participates in a moderated question-and-answer session at the 'Dialogue with the Dallas Fed' event hosted by the Lubbock, Texas, Chamber of Commerce.

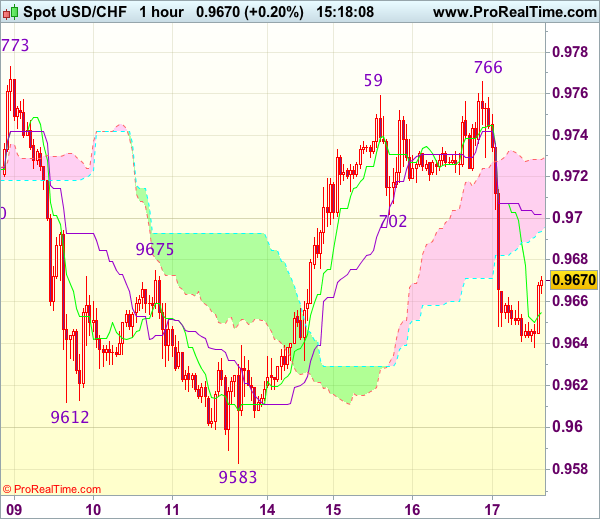

Trade Idea : USD/CHF – Stand aside

USD/CHF - 0.9662

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9656

Kijun-Sen level : 0.9702

Ichimoku cloud top : 0.9728

Ichimoku cloud bottom : 0.9694

Original strategy :

Bought at 0.9680, stopped at 0.9645

Position : - Long at 0.9680

Target : -

Stop : - 0.9645

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s brief rise to 0.9766, the subsequent sharp retreat after faltering below resistance at 0.9773 dampened our bullishness and further choppy consolidation below said resistance would be seen, hence weakness to 0.9630-35 cannot be ruled out, however, reckon downside would be limited to 0.9600-05 and support at 0.9583 should remain intact, bring another rebound later.

On the upside, whilst recovery to the Kijun-Sen (now at 0.9702) cannot be ruled out, reckon upside would be limited to the upper Kumo (now at 0.9728) and price should falter well below resistance at 0.9766, bring another retreat later. As near term outlook is mixed, would be prudent to stand aside in the meantime.

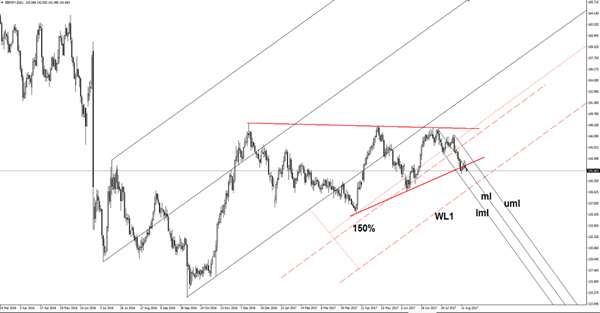

GBP/JPY Drops As Expected

Price is expected to drop further on the Daily chart after the retest of the broken red uptrend line, the next downside target will be at the first warning line (WL1) of the major ascending pitchfork. Could be attracted by the confluence area formed at the intersection between the lower median line (lml) with the WL1.

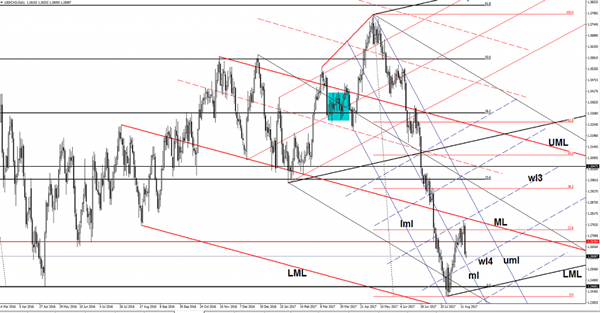

USD/CAD Attracted By Confluence Area

Price plunged in the yesterday's session and now is expected to hit the confluence area formed at the intersection between the median line (ml) of the minor descending pitchfork with the fourth warning line (wl4). The retreat could be temporary if the US data will come in better today, only some good numbers will save the greenback from the downside. A rebound is favored from the mentioned levels if the economic figures will impress.

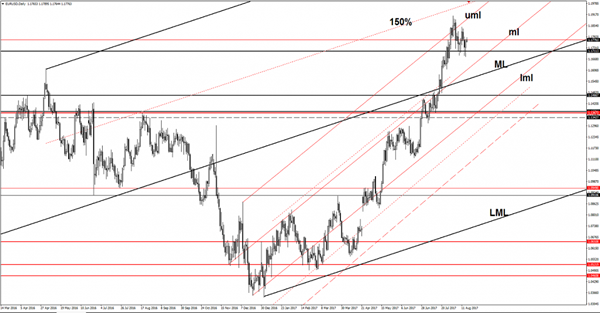

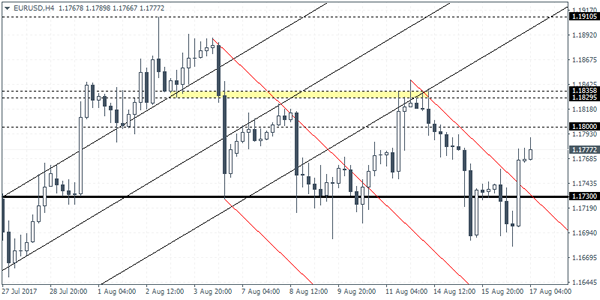

EUR/USD Still Bullish

Price remains bullish until more sellers appear. The 1.1712 major static support remains intact, so it could climb higher on the short term. Technically was expected to drop towards the median line (ml) of the minor ascending pitchfork. Could still reach this downside target if will move in range above the 1.1712 level. I've said in the previous weeks that we may have a minor consolidation above it, which will signal a further increase on the Daily chart.

Only a valid breakdown below the horizontal support will signal a larger corrective phase, this scenario could take shape only if the US data will impress in the afternoon.

The Euro needs a bullish spark to be able to drive the pair towards new highs in the upcoming hours, the Euro-zone Trade Balance could increase from 19.7B to 20.4B, the Final CPI by 1.3%, same like in the former reading period, while Final Core CPI may increase by 1.2%.

Price posted little gains after the yesterday's rebound, but remains under some selling pressure after the failure to retest the upper median line (uml) of the ascending pitchfork. Technically was somehow expected to drop towards the median line (ML) of the major ascending pitchfork after the failure to react at least the 150% Fibonacci line (ascending dotted line).

A larger increase will be confirmed after will close above the 1.1909 previous high, but is hard to believe that will jump so high until will retest the median line (ml).

USDJPY Intraday Analysis

USDJPY (109.90): The USDJPY declined after failing to break past the resistance level of 110.80. Declines are likely to push USDJPY to test the lower support at 109.70 where support is currently being tested. A rebound off this level, which coincides with the trend line support would suggest some upside in prices. The USDJPY is also likely to form an inverse head and shoulders pattern on a successful rebound off 109.70. If the currency pair manages to break past the resistance level of 110.80, then the next target is towards 111.77 resistance level.

GBPUSD Intraday Analysis

GBPUSD (1.2904): The British pound managed to post a modest rebound yesterday. Slightly better than expected labor market data helped to improve the sentiment in the cable which weakened earlier in the week on account of inflation data. The rebound off 1.2835 is likely to see some upside in prices. Near-term resistance is seen at 1.2980 - 1.3000 which could be tested. If resistance is formed here, then GBPUSD could be forming the final right shoulder in the head and shoulders pattern that is evolving on the daily charts. This would suggest further downside in prices on a break below 1.2835.

EURUSD Intraday Analysis

EURUSD (1.1777): The EURUSD managed to recover the losses from Wednesday following the FOMC meeting minutes which turned out to be dovish than expected. Still, the current retracement is likely to be a minor pullback with the overall bias shifting to the downside. The key risk is the fact that EURUSD once again managed to rally back above the support of 1.1730. Near-term bullish momentum could send EURUSD back to the resistance level of 1.1800. After that, the sideways range is likely to be formed. A break down below 1.1730 would suggest a move to 1.1635. To the upside, above the resistance of 1.1800, expect EURUSD to continue pushing towards the next main resistance level of 1.1835.

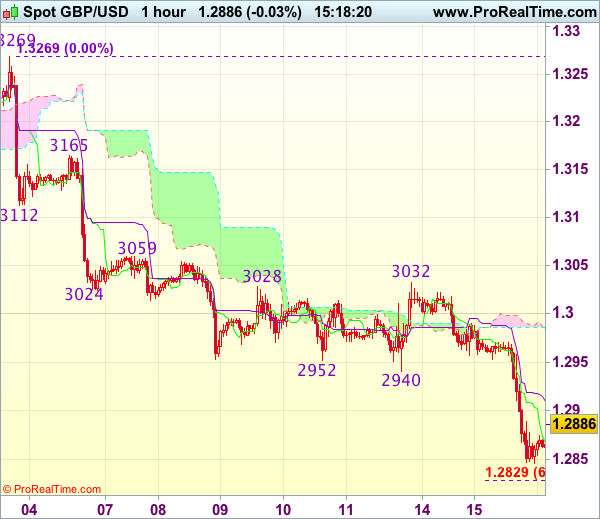

Trade Idea : GBP/USD – Sell at 1.2920

GBP/USD - 1.2886

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2868

Kijun-Sen level : 1.2910

Ichimoku cloud top : 1.2986

Ichimoku cloud bottom : 1.2984

Original strategy :

Sell at 1.2920, Target: 1.2820, Stop: 1.2955

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.2920, Target: 1.2820, Stop: 1.2955

Position : -

Target : -

Stop : -

As cable has remained under pressure after yesterday’s selloff, adding credence to our bearish view that the decline from 1.3269 top is still in progress for retracement of early upmove, hence downside bias remains for further weakness to 1.2825-30 (61.8% projection of 1.3269-1.2940 measuring from 1.3032), having said that, near term oversold condition should limit downside to 1.2800 and reckon 1.2770 would hold from here, bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell sterling on recovery as said previous support at 1.2933 should turn into resistance and cap cable’s upside, bring another decline. Above 1.2950 would defer and risk a stronger rebound to 1.2990-00 before another decline.

Greenback Weakens On The Back Of FOMC Meeting Minutes

The US dollar gave up some of the gains on Wednesday following the release of the FOMC meeting minutes. The minutes showed that Fed officials were divided on the course of interest rates. They also raised concerns about the underlying inflation with some members expecting inflation to remain below the Fed's 2% target rate. On the other side, some hawkish members argued that there would be risks from the tightening conditions in the US labor markets.

On the economic front, data yesterday saw the UK's unemployment rate falling to historic lows. Beating estimates, the unemployment rate in the UK slipped to 4.4%. However, wages continued to lag behind inflation. The British pound managed to post a modest recovery as a result. In New Zealand, the producer prices data showed a 1.4% increase in input prices, while output prices rose 1.3%, both beating the median estimates.

Looking ahead, the economic calendar today will include the UK retail sales which are expected to rise just 0.2%. In the eurozone, final inflation figures for July will be released. Consumer prices are expected to rise 1.3% on the headline and 1.2% on the core.