Sample Category Title

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1705; (P) 1.1741 (R1) 1.1803; More...

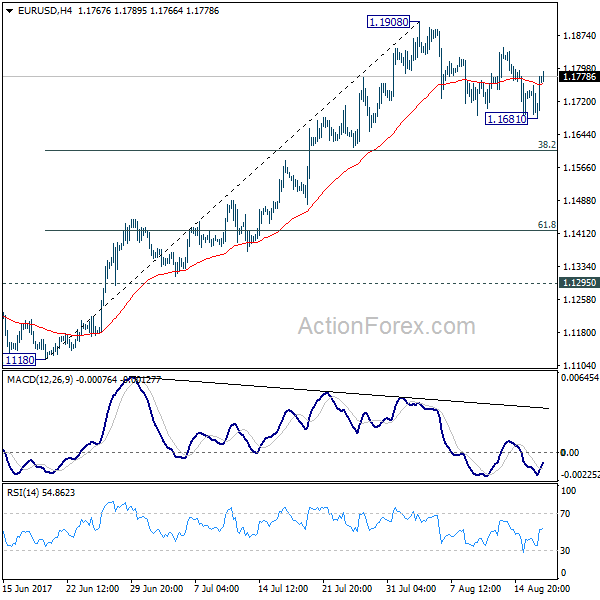

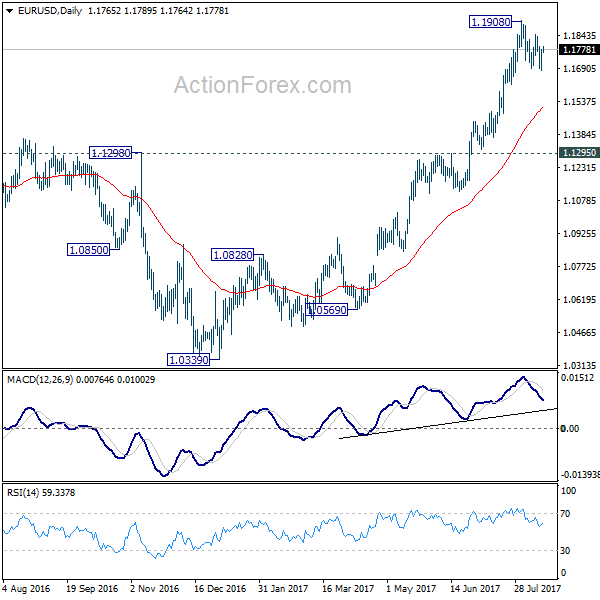

EUR/USD dipped to 1.1681 but quickly recovered. Intraday bias remains neutral as consolidation from 1.1908 is still in process. Another fall cannot be ruled out. But downside should be contained by 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring rebound. On the upside, break of 1.1908 will extend recent up trend to 1.2042 long term support turned resistance next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2565; (P) 1.2667; (R1) 1.2722; More....

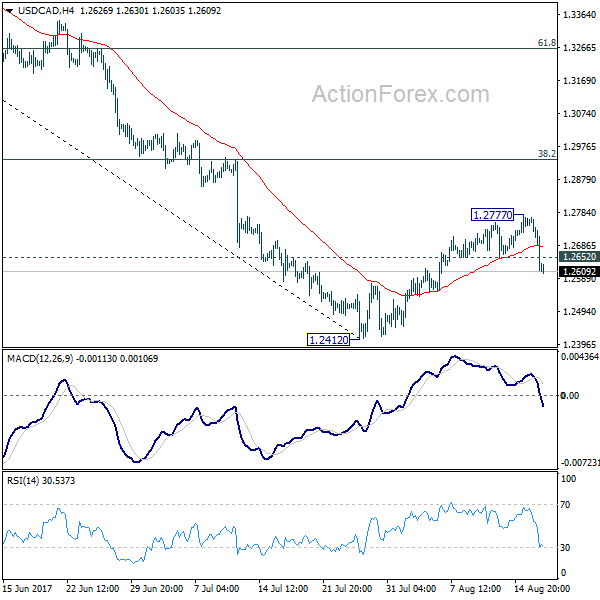

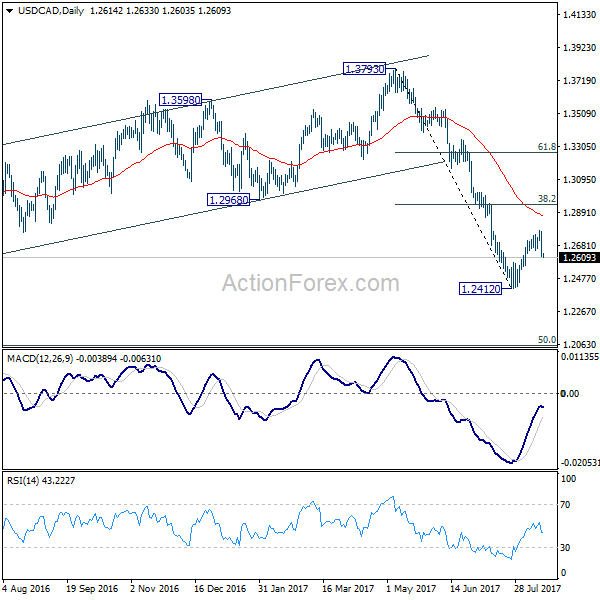

USD/CAD's fall and break of 1.2652 minor support suggests that recovery from 1.2412 has completed at 1.2777 already. Intraday bias is turned back to the downside for retesting 1.2412 low. Break there will resume the larger decline and target next long term fibonacci level at 1.2048. On the upside, above 1.2777 will extend the recovery. But we'd expect upside to be limited by 38.2% retracement of 1.3793 to 1.2412 at 1.2940 to bring fall resumption.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Such corrective fall is still expected to extend to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. Nonetheless, on the upside, sustained break of 1.2968, 38.2% retracement of 1.3793 to 1.2412 at 1.2940 will be the first sign of completion of the correction and will turn focus back to 1.3793 key resistance.

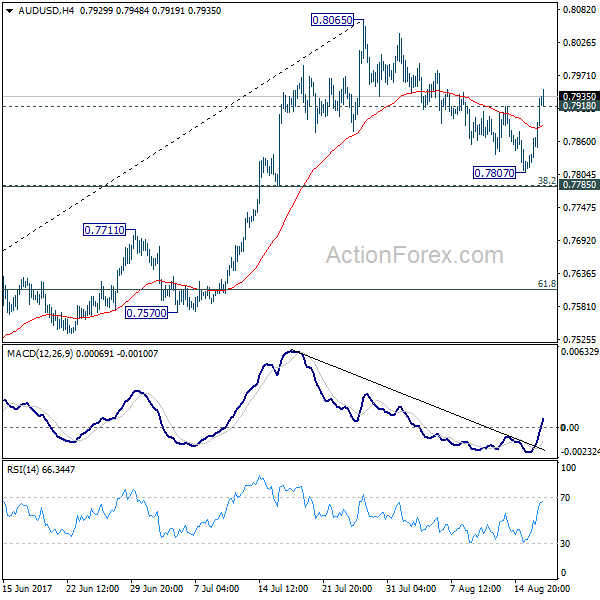

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7850; (P) 0.7891; (R1) 0.7967; More...

AUD/USD's strong rebound and break of 0.7918 resistance suggests that pull back fro 0.8065 has completed at 0.7807. The pair was supported by 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783) as expected. Intraday bias is turned back to the upside for retesting 0.8065 first. Firm break there will resume the medium term rise and target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8100) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now expected.

Dollar Reverses on FOMC Minutes, Political Drama

Dollar was sold off overnight as FOMC minutes showed worries of members over inflation. Political drama in the White House also added some weight to the greenback. Notable strength is seen in the Japanese Yen in Asian session. But commodity currencies are generally the strongest ones over the week. Weakness in the greenback was accompanied by strength in bonds, where 10 year yield dropped -0.04 to close at 2.226. Gold rode the wave and is back above 1290 after dipping to as low as 1272.7. And Gold looks set to have another attempt on 1300. WTI crude oil, on the other hand, continues to suffer and dipped to as low as 467.67, extending the decline from recent high at 50.43.

FOMC minutes show worries on inflation

The minutes of July 25-26 FOMC meeting showed that many policy makers "saw some likelihood that inflation might remain below 2 percent for longer than they currently expected". Also, "several indicated that the risks to the inflation outlook could be tilted to the downside." And, some officials suggested that Fed "could afford to be patient" regarding the next rate hike. Regarding the plan to unwind the USD 4.5T balance sheet, a few members wanted to announce in July meeting. Nonetheless, "most preferred to defer that decision until a coming meeting" for having a better assessment on the health of the economy.

The minutes confirmed markets' view that the a December Fed hike is doubtful. And, unless inflation picks up in the coming months, Fed could hold off on rates till next year. Currently, Fed fund futures are pricing in 45.6% chance of a hike in December, slightly lower then yesterday's 50%. The key to watch ahead is whether Fed will continue to describe the slowdown in inflation as "transitory" ahead.

Trump disbands two advisory councils

Political drama in US seems never-ending as President Donald Trump announced to disband two of his business advisory councils. That came after a number of business executives quitted with strong disagreement to Trump's remarks about the violence at a white-supremacist rally in Charlottesville at the weekend. Those business leaders were deeply dissatisfied with Trump's equating of neo-Nazis to counter protestors. Some analysts pointed out that business leader will still support Trump's tax reform on policy basis. But the developments certainly won't give any help to Trump's administration and the Republicans on pushing through the economic agenda.

Dollar index stays bearish

We're pointed out before that Dollar's rebound this week doesn't worry a trend reversal yet. This is so far consistent with the development in the dollar index. Recovery from 92.54 was limited below near term resistance level at 94.28. Such recovery is also corrective looking and thus, maintaining bearish outlook. Fall from 103.82 is still expected to extend to have a test on 91.91 key support level ahead.

ECB accounts to watch today

On the data front, Japan trade surplus widened to JPY 0.34T in July. Australia employment grew 27.9k in July, above expectation of 20.0k. Australia unemployment rate was unchanged at 5.6%. New Zealand PPI inputs rose 1.4% qoq in Q2 while PPI outputs rose 1.3% qoq.

ECB monetary meeting accounts will be a key to watch for clues on how ready police makers are on tapering the asset purchase. Eurozone will also release trade balance and CPI final. UK retail sales will be featured. Later in the data, Canada will release manufacturing sales. US will release Philly Fed survey, industrial production , leading indicators and jobless claims.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7850; (P) 0.7891; (R1) 0.7967; More...

AUD/USD's strong rebound and break of 0.7918 resistance suggests that pull back fro 0.8065 has completed at 0.7807. The pair was supported by 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783) as expected. Intraday bias is turned back to the upside for retesting 0.8065 first. Firm break there will resume the medium term rise and target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8100) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now expected.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Inputs Q/Q Q2 | 1.40% | 0.90% | 0.80% | |

| 22:45 | NZD | PPI Outputs Q/Q Q2 | 1.30% | 0.70% | 1.40% | |

| 23:50 | JPY | Trade Balance (JPY) Jul | 0.34T | 0.20T | 0.08T | 0.09T |

| 23:50 | JPY | Merchandise Trade Exports Y/Y Jul | 13.40% | 13.40% | 9.70% | |

| 1:30 | AUD | Employment Change Jul | 27.9K | 20.0K | 14.0K | |

| 1:30 | AUD | Unemployment Rate Jul | 5.60% | 5.60% | 5.60% | 5.70% |

| 8:30 | GBP | Retail Sales M/M Jul | 0.60% | 0.60% | ||

| 9:00 | EUR | Eurozone Trade Balance (EUR) Jun | 20.3B | 19.7B | ||

| 9:00 | EUR | Eurozone CPI M/M Jul | -0.50% | 0.00% | ||

| 9:00 | EUR | Eurozone CPI Y/Y Jul F | 1.30% | 1.30% | ||

| 9:00 | EUR | Eurozone CPI - Core Y/Y Jul F | 1.20% | 1.20% | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | CAD | Manufacturing Shipments M/M Jun | -1.00% | 1.10% | ||

| 12:30 | USD | Initial Jobless Claims (AUG 12) | 240k | 244k | ||

| 12:30 | USD | Philadelphia Fed Business Outlook Aug | 18.8 | 19.5 | ||

| 13:15 | USD | Industrial Production Jul | 0.30% | 0.40% | ||

| 13:15 | USD | Capacity Utilization Jul | 76.70% | 76.60% | ||

| 14:00 | USD | Leading Indicators Jul | 0.30% | 0.60% | ||

| 14:30 | USD | Natural Gas Storage | 28B |

FOMC Minutes Not As Dovish As Seen By The Market

The price actions in US dollar and Treasuries suggested that the market views the July FOMC minutes as a dovish one. The minutes revealed that policymakers were concerned that US inflation might stay below +2% longer than previously anticipated. On the other hand, it appears that an announcement on balance sheet policy is imminent. The market pricing of a rate hike in December ranges from 35-45%. It only expects less than two times of rate hike through end-2018, compared with four projected in the Fed’s dot plot. US dollar initially climbed higher upon release of the statement. Gains were, however, erased shortly with the DXY index ending the day -0.33% lower. Treasury prices strengthened, sending 2-year yields -3 points lower to 1.33% and 10-year yields -5 points to 2.23%.

On inflation, the minutes unveiled that 'many participants' still believed that 'much of the recent decline in inflation had probably reflected idiosyncratic factors…and the monthly readings might be depressed by possible residual seasonality in measured PCE inflation'. Moreover, 'most participants indicated that they expected inflation to pick up over the next couple of years from its current low level and to stabilize around the Committee's 2% objective over the medium-term'. However, the minutes also indicated that 'many participants' pointed out the possibility that 'inflation might remain below 2% for longer than they currently expected' while 'several indicated that the risks to the inflation outlook could be tilted to the downside'

The implications of soft inflation on the monetary policy were relatively balanced. 'Some participants' believed that the Fed should 'be patient under current circumstances in deciding when to increase the federal funds rate further and argued against additional adjustments until incoming information confirmed that the recent low readings on inflation were not likely to persist and that inflation was more clearly on a path toward the Committee's symmetric +2% objective over the medium term'. These comments were then balanced by 'some other participants' who 'were more worried about risks arising from a labor market that had already reached full employment and was projected to tighten further or from the easing in financial conditions that had developed since the Committee's policy normalization process was initiated in December 2015'. These members warned that 'a delay in gradually removing policy accommodation could result in an overshooting of the Committee's inflation objective that would likely be costly to reverse, or that a delay could lead to an intensification of financial stability risks or to other imbalances that might prove difficult to unwind'.

A formal announcement of balance sheet reduction appears imminent. The minutes noted that 'participants generally agreed that, in light of their current assessment of economic conditions and the outlook, it was appropriate to signal that implementation of the program likely would begin relatively soon, absent significant adverse developments in the economy or in financial markets'. For details of how the Fed plans to gradually shrink its US$4.5 trillion balance sheet, please see: https://www.federalreserve.gov/monetarypolicy/files/FOMC_PolicyNormalization.20170613.pdf.

The minutes were not as dovish as we had anticipated. Despite the disappointment in June inflation, most members continued to maintain the view that the current weak price levels were transitory, although some were worried that inflation might take longer than previously expected to reach the +2% target. Indeed, headline inflation improved modestly, while core inflation steadied, in July. These should be a relief for the members. Barring any dramatic deterioration the economic outlook, we continue to expect one more rate hike in December and a formal announcement of balance sheet reduction to come in September.

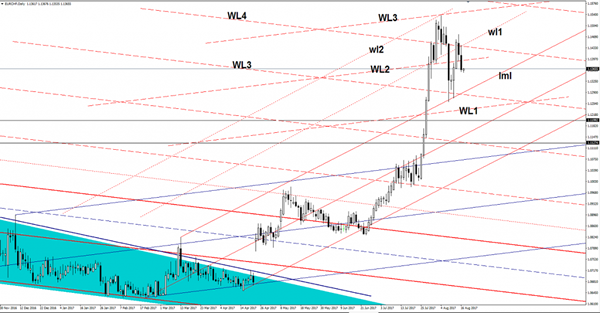

EUR/CHF On The Way Down

Price is into a corrective phase, after the false breakout above the WL4 and above the first warning line (wl1) of the minor ascending pitchfork. A retest of the upper median line (ml) is favored at this moment, we’ll see what will react then. A breakdown below the upper median line (uml) will signal a major drop in the upcoming weeks.

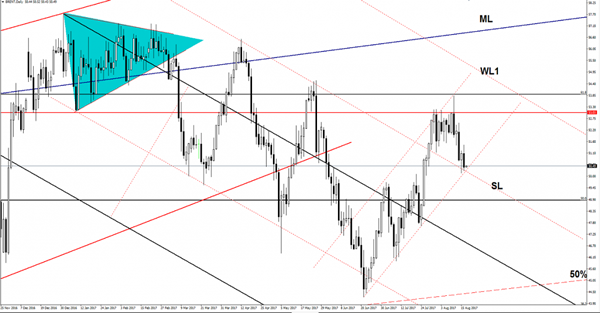

Brent Oil Throwback Favored

Price is trading within a minor ascending channel, the perspective is bullish as long as is trapped within this channel. Has come down to retest the downside line of the chart pattern and the sliding line (SL) and now is expected to bounce back. Is trading near the $50.50 per barrel, and above the confluence area formed by SL with the downside line of the ascending channel. Only a valid breakdown will confirm a further drop.

Gold Rebounded On FOMC Minutes

Gold rallied aggressively after the FOMC Meeting Minutes release and now tries to take out a strong horizontal resistance. Price increased as the USD was punished by the dovish FOMC Minutes and by the poor US data. The yellow metal move in range on the daily chart, could resume this extended sideways if will fail to close above the 1292 previous high.

Gold may increase further as the Kiwi and Aussie appreciated significantly versus the greenback, the currencies could receive a helping hand from the Australia and New Zealand in the early morning. The New Zealand PPI input could increase by 0.9%, more versus the 0.8% in the previous reporting period. On the other hand, the Aussie is waiting for a helping hand from the Australian Employment Change, which should increase from 14.0K to 19.8K, while the Unemployment Rate could remain steady at 5.6%.

Price is pressuring the 38.2% retracement level, should close and stabilize above this level if the USDX will drop much towards the 93.00 psychological level. Is trading in range and a failure to climb and close above 1292 will signal a major drop. Is premature to say what will happen, but the failure to reach the $1295 per ounce and to reach the 23.6% retracement level signaled an exhaustion on the short term.

Price is located in the green zone as long as is trading above the warning line (WL1), but a drop below this level will open the door for a broader drop.

Gold Hugging Daily Trend Line

Back at the beginning of the month, we were watching price action in gold when it printed a long legged doji at trend line resistance.

Normally, the trading textbook would have you believe that this is bearish price action. But I ended that particular blog post with this:

'It doesn't have to represent a pending reversal.

With price now continuing to show bullish strength, it could just as easily continue to hug the trend line as price continues moving up, or even reactivate it as support and carry on with the original trend line like nothing had happened and it was never broken in the first place!”

Now take a look at what price has done:

XAU/USD Daily:

There was a small re-test but with no lower low, price pretty quickly rallied to a new high back above the original trend line and has now continued to hug the level as expected.

When you come across a daily trend line like this, the subjective nature means that a break is never clean. You'll find that more often than not, what looks to be highly bearish on the surface, actually isn't. Never get carried away with these sorts of setups.

FOMC Members Express Concern Over Inflation, But Agreement on Normalizing the Fed’s Balance Sheet

Federal Open Market Committee (FOMC) members noted little change to the economic or labor market outlook, but spent a considerable time pondering the "the softness in inflation" and how to react to it.

While most members saw inflation returning to two percent over the medium term, "many...saw some likelihood that inflation might remain below two percent for longer than they currently expected, and several indicated that the risks to the inflation outlook could be tilted to the downside."

Balancing some of the concern around soft inflation was an opposing perspective that financial conditions had eased despite gradual policy tightening.

FOMC members largely agreed to the timing of balance sheet normalization. The minutes noted that: "participants generally agreed that, in light of their current assessment of economic conditions and the outlook, it was appropriate to signal that implementation of the program likely would begin relatively soon, absent significant adverse developments in the economy or in financial markets."

Key Implications

No major surprises here. Just like everyone else, FOMC members are trying to understand why inflation is decelerating even as the economy continues to tighten. There is not one simple answer, but the Fed meeting minutes showed members discussing some of the potential factors, namely a weakened relationship between resource slack and inflation, a lower natural rate of unemployment, greater lags in the relationship between tightening and inflation, and restraints on pricing power from technology and globalization.

Despite the debate, the orthodoxy appears to be holding and most members continue to believe that a hot economy will eventually push price growth higher. Nonetheless, there appears to be enough doubt in the minds of members to take a wait and see approach. This would appear to bar the door on any immediate increase in policy rates (in September) and suggests that a December hike will require at least some evidence that inflation is moving higher.

At the same time, there appears little disagreement on the need to begin normalizing the size of the balance sheet or the general belief that this should have little effect on the broad conduct of monetary policy, which the FOMC hopes to achieve mainly through adjusting the federal funds rate target.