Sample Category Title

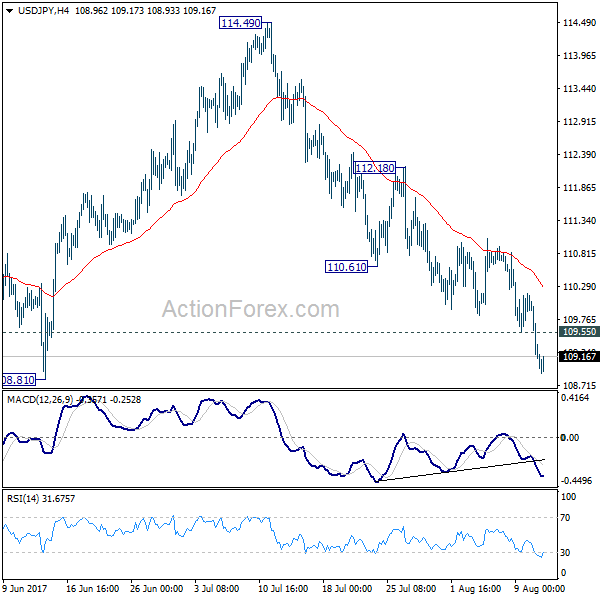

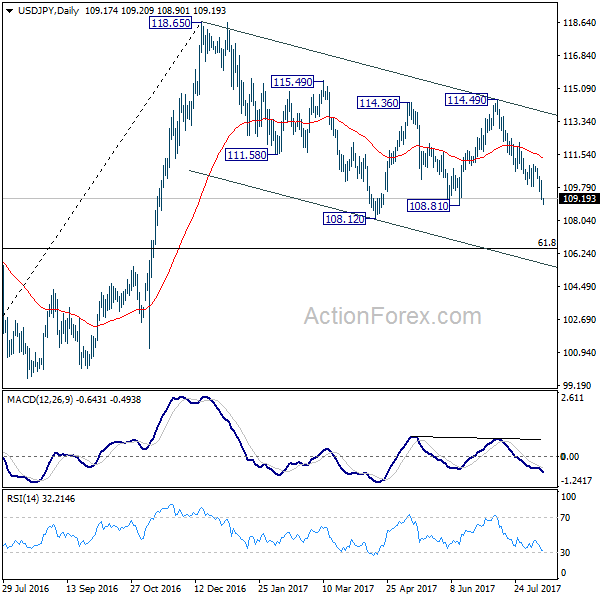

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.84; (P) 109.51; (R1) 109.87; More...

USD/JPY's fall accelerates again and reaches as low as 108.90 so far. Intraday bias remains on the downside for 108.81 support. Break there will resume whole correction from 118.65 and target 61.8% retracement of 98.97 to 118.65 at 106.48. On the upside, above 109.55 minor resistance will turn intraday bias neutral first. But near term outlook will remain bearish as long as 110.61 support turned resistance holds.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

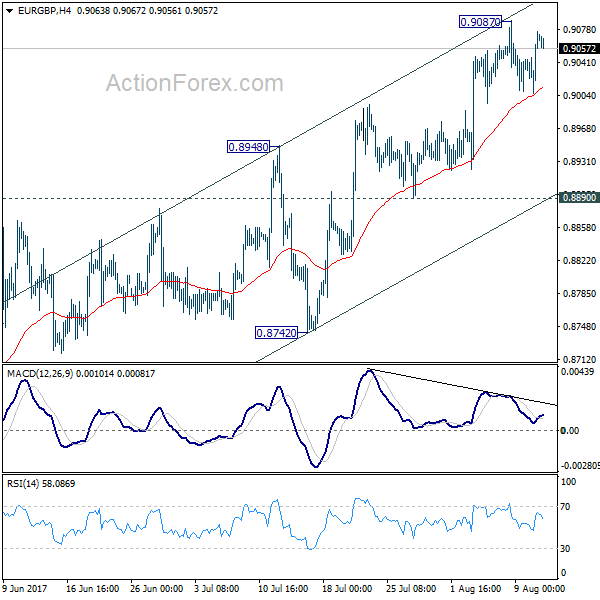

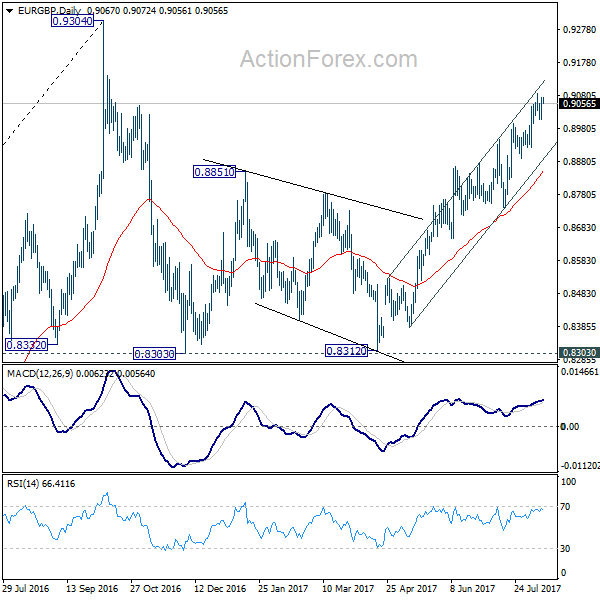

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.9027; (P) 0.9051; (R1) 0.9095; More

Intraday bias in EUR/GBP remains neutral for consolidation below 0.9087 temporary top. While another retreat cannot be ruled out, further is still expected as long as 0.8890 support holds. Above 0.9087 will extend the rebound from 0.8312 to 0.9304 key high. At this point, there is no clear sign of up trend resumption yet. Hence, we'll be cautious on strong resistance from 0.9304 to limit upside and bring another fall. On the downside, break of 0.8890 will be the first indication of near term reversal. In such case, intraday bias will be turned back to the downside for 0.8742 support for confirmation.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4875; (P) 1.4918; (R1) 1.4989; More...

EUR/AUD's rise from 1.4421 resumed by breaking 1.4964 and reaches as high as 1.5010 so far. Intraday bias is back on the upside for 1.5073 resistance next. As noted before, correction from 1.5226 should have completed with three waves down to 1.4421 already. Decisive break of 1.5073 will likely resume the rise from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4421 at 1.5411 next. Near term outlook will remain bullish as long as 1.4824 support holds, even in case of retreat.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to resume to retest 1.6587. The corrective structure of the fall from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, another decline will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

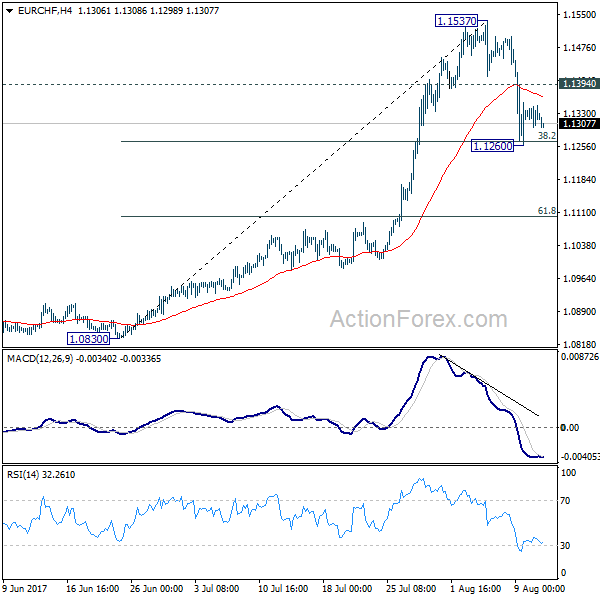

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1304; (P) 1.1326; (R1) 1.1351; More...

Intraday bias in EUR/CHF remains neutral with a temporary low formed at 1.1260. The cross is trying to draw support from 38.2% retracement of 1.0830 to 1.1537 at 1.1267. On the upside, break of 1.1394 minor resistance will indicate that the pull back from 1.1537 has completed. In such case, intraday bias will be turned back to the upside for retesting 1.1537 first. However, firm break of 1.1267 will extend the fall and target 61.8% retracement at 1.1100.

In the bigger picture, firm break of 1.1198 key resistance confirms resumption of the long term rise from SNB spike low back in 2015. In this case, EUR/CHF would eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

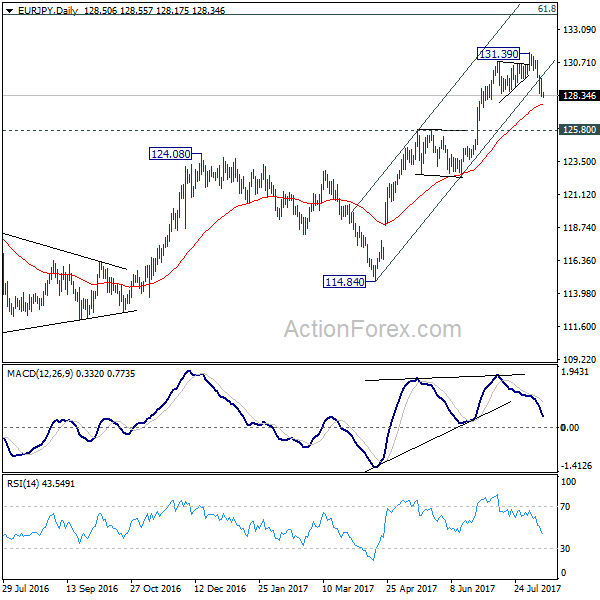

EUR/JPY Daily Outlook

Daily Pivots: (S1) 128.01; (P) 128.78; (R1) 129.33; More...

EUR/JPY's correction from 131.39 extends lower today and intraday bias remains on the downside for 38.2% retracement of 122.39 to 131.39 at 127.95. At this point, we'd expect strong support from 127.95 to contain downside and bring rebound. Above 129.54 minor resistance will turn bias back to the upside for retesting 131.39. However, firm break of 127.95 will bring deeper decline to 125.80 cluster support (61.8% retracement at 125.82) before completing the correction.

In the bigger picture, the down trend from 149.76 (2014 high) is completed at 109.03 (2016 low). Current rally from 109.03 should be at the same degree as the fall from 149.76 to 109.03. Further rise is expected to 61.8% retracement of 149.76 to 109.03 at 134.20. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. Medium term outlook will remain bullish as long as 124.08 resistance turned support holds.

European Open Briefing: Asian Equity Markets Continued Their Tumble Yet Again On Friday

Global Markets:

- Asian stock markets: Nikkei fell 0.05 %, Shanghai Composite down 1.52 %, Hang Seng dropped 1.70 %, ASX 200 fell 1.32 %

- Commodities: Gold at $1291.82 (+0.13 %), Silver at $17.06 (-0.01 % %), WTI Oil at $48.16 (-0.88 %), Brent Oil at $51.43 (-0.91 % %)

- Rates: US 10-year yield at 2.20, UK 10-year yield at 1.08, German 10-year yield at 0.40

News & Data:

- GBP Manufacturing Production m/m 0.0 % vs 0.0 % expected

- GBP Goods Trade Balance -12.7 B vs -11.0 B expected

- USD PPI m/m -0.1 % vs 0.1 % expected

- USD unemployment claims 244 K vs 240 K expected

- USD Core PPI m/m -0.1 % vs 0.2 % expected

- Fed buys $5.2 billion of mortgage bonds, sells none- RTRS

- Wall Street stock rally could be derailed by U.S.-North Korea war of words – RTRS

Markets Update:

Asian equity markets continued their tumble yet again on Friday as risk concerns were reignited in the markets following the Comments from US President Trump on North Korea in the US afternoon

USD/JPY has dropped more than 125 pips advancing to the strongest in eight weeks and closing below 108.90 in the Asian session in spite of a weak session overnight, being a Japanese holiday today, this move has been attributed to North Korea jitters

EUR/USD was little changed seen trading at $1.1776 after climbing 0.1 percent in the previous session. The US Dollar index was steady against a basket of six major currencies at 93.385 after falling 0.2 percent on Thursday.

Aussie was seen trading relatively steadily, but finally gave away 30-odd points losing 0.4 % in value and falling to lows below 0.7840 against the US Dollar. NZD/USD slipped a little with the AUD but recovered immediately and seen currently trading above 0.7270.

Upcoming Events:

- JPY Bank Holiday

- 12:30 GMT – (USD) CPI m/m

- 12:30 GMT – (USD) Core CPI m/m

- 13:40 GMT – FOMC Member Kaplan Speaks

- 15:30 GMT – FOMC Member Kashkari Speaks

Wage Growth Too Low, Interest Rates Are More Likely To Rise But Not Yet: RBA Governor

For the 24 hours to 23:00 GMT, the AUD declined 0.29% against the USD and closed at 0.7865.

LME Copper prices declined 0.8% or $48.5/MT to $6416.5/MT. Aluminium prices rose 0.3% or $6.0/MT to $2024.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7850, with the AUD trading 0.19% lower against the USD from yesterday's close.

Overnight, the Reserve Bank of Australia's (RBA) Governor, Philip Lowe, stated that the central bank had been prepared to be “patient” on monetary policy and acknowledged low wage growth as one of the key risks to the Australian economy. Further, Lowe indicated that any move in interest rate will likely be gradual and probably to the upside.

The pair is expected to find support at 0.7825, and a fall through could take it to the next support level of 0.7801. The pair is expected to find its first resistance at 0.7888, and a rise through could take it to the next resistance level of 0.7927.

Going forward, the Reserve Bank of Australia's August meeting minutes, followed by Australia's unemployment rate data, set to release next week, will be on investors' radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro Trading Marginally Higher, Ahead Of Germany’s Final Inflation Data

For the 24 hours to 23:00 GMT, the EUR slightly rose against the USD and closed at 1.1765.

In economic news, French industrial production dropped more-than-expected by 1.1% on a monthly basis in June, dropping by the most in four months and compared to market expectations for a fall of 0.6%. Industrial production had climbed 1.9% in the previous month.

Macroeconomic data indicated that the number of Americans filing for jobless claims for the first time unexpectedly rose to a level of 244.0K in the week ended 05 August 2017, confounding market consensus for a fall to a level of 240.0K. In the previous week, initial jobless claims had recorded a revised level of 241.0K. Additionally, the nation's producer price index (PPI) surprisingly fell 0.1% on a monthly basis in July, hitting its lowest in nearly a year. The PPI had advanced 0.1% in the previous month, while markets were anticipating for a rise of 0.1%.

In the Asian session, at GMT0300, the pair is trading at 1.1768, with the EUR trading a tad higher against the USD from yesterday's close.

The pair is expected to find support at 1.1720, and a fall through could take it to the next support level of 1.1671. The pair is expected to find its first resistance at 1.1801, and a rise through could take it to the next resistance level of 1.1833.

Going ahead, traders will closely monitor Germany's final consumer price inflation for July, slated to release in a few hours. Also, the US inflation report for July, slated to release later in the day, will pique significant amount of investor attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Britain’s Total Trade Deficit Unexpectedly Widened To A 9-Month High In June

For the 24 hours to 23:00 GMT, the GBP declined 0.26% against the USD and closed at 1.2976, following disappointing economic data in the UK.

Data indicated that Britain's total trade deficit surprisingly widened to a nine-month high level of £4.56 billion in June, as exports dipped and imports surged. The nation had posted a revised deficit of £2.52 billion in the previous month, whereas market participants had envisaged for a deficit of £2.50 billion. Further, the nation's construction output recorded an unexpected drop of 0.1% on a monthly basis in June, compared to a revised fall of 0.4% in the prior month, while market participants had anticipated for a gain of 1.4%. Further, NIESR estimated UK's gross domestic product (GDP) climbed less-than-anticipated by 0.2% in the three months to July, compared to market expectations for a rise of 0.3%. In the April-June 2017 period, NIESR estimated GDP had climbed 0.3%.

In other economic news, manufacturing production in the UK remained flat on a monthly basis in June, at par with market expectations. In the prior month, manufacturing production had recorded a revised drop of 0.1%. On the other hand, the nation's industrial production climbed 0.5% on a monthly basis in June, more than market consensus for an advance of 0.1%. Industrial production had registered a revised flat reading in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.2982, with the GBP trading 0.05% higher from yesterday's close.

The pair is expected to find support at 1.2951, and a fall through could take it to the next support level of 1.2921. The pair is expected to find its first resistance at 1.3013, and a rise through could take it to the next resistance level of 1.3045.

Amid no macroeconomic releases in the UK today, investors will keep a close watch on UK's inflation figures, retail sales and ILO unemployment rate data, all scheduled to release next week.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Japanese Yen Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.73% against the JPY and closed at 109.16.

The Japanese Yen gained ground, amid increased risk aversion as investors continue to grapple with geopolitical tensions between the US and North Korea.

In the Asian session, at GMT0300, the pair is trading at 108.97, with the USD trading 0.17% lower against the JPY from yesterday’s close.

The pair is expected to find support at 108.59, and a fall through could take it to the next support level of 108.22. The pair is expected to find its first resistance at 109.71, and a rise through could take it to the next resistance level of 110.46.

Next week, investors will focus on Japan’s 2Q GDP data, to gauge strength in the Japanese economy.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.