Sample Category Title

Swiss Franc Extends Its Gains In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.16% against the CHF and closed at 0.9622.

In the Asian session, at GMT0300, the pair is trading at 0.9613, with the USD trading 0.09% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9591, and a fall through could take it to the next support level of 0.9569. The pair is expected to find its first resistance at 0.9655, and a rise through could take it to the next resistance level of 0.9697.

Going ahead, investors will look forward to Switzerland’s producer and import prices data, the sole important release next week.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canada’s New House Price Index Rose Less-Than-Expected In June

For the 24 hours to 23:00 GMT, the USD rose 0.35% against the CAD and closed at 1.2742.

On the data front, Canada's new housing price index registered a rise of 0.2% MoM in June, falling short of market expectations for an advance of 0.5%. The index had risen 0.7% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.2745, with the USD trading a tad higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2694, and a fall through could take it to the next support level of 1.2644. The pair is expected to find its first resistance at 1.2774, and a rise through could take it to the next resistance level of 1.2804.

Investors will keep a close watch on Canada's consumer price index and existing home sales data, both set to be released next week.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

We typically search for lower-timeframe confirmation between the M15 and H1 timeframes, since most of our higher-timeframe areas begin with the H4. Stops are usually placed 1-3 pips beyond confirming structures.

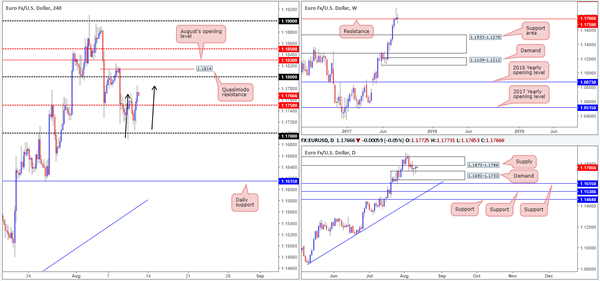

EUR/USD

Thanks to a healthy bout of buying from just ahead of the 1.17 neighborhood on Thursday, the EUR ended the day closing back above the H4 mid-level resistance pegged at 1.1750. Traders may have also noticed that the recent bid helped form a nice-looking H4 AB=CD bearish formation that completes around the 1.1785ish range (see black arrows).

Selling this Harmonic pattern may be appealing to some, given that daily price is also seen trading within striking distance of a supply noted at 1.1870-1.1786. Be that as it may, there are a few cautionary points you may want to consider:

The EUR has (and still is) entrenched within a strong uptrend.

The aforementioned daily supply suffered multiple breaks to the upside last week, thus potentially weakening the zone.

A sell on the H4 places you in direct conflict with the 1.1750 line.

Weekly price is currently trading above resistance at 1.1759.

Our suggestions: On account of the above points, selling this market is a risk that we're just not willing to take at the moment.

Although we're against selling, we're also not too fond of buying this market either. Buying into an AB=CD completion and a daily supply (despite its condition) is not something our team would label high probability.

Data points to consider: US Inflation figures scheduled for release at 1.30pm, followed closely by FOMC members Kaplan and Kashkari taking the stage at 2.40/4.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

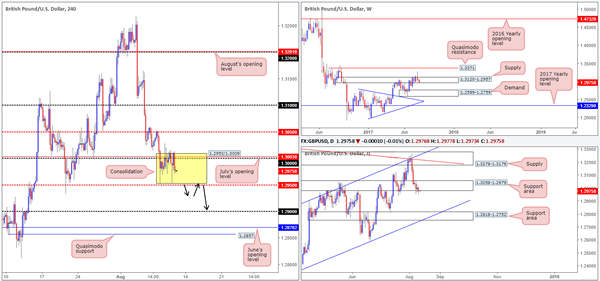

GBP/USD

As can be seen from the H4 chart this morning, the GBP/USD appears to be in the process of chiseling out a small consolidation between 1.2953/1.3009. Supporting the top edge of this area is a large psychological band at 1.30 as well as July's opening level seen at 1.3003. Bolstering the lower edge, however, we have a H4 mid-level support coming in at 1.2950.

Over on the bigger picture, weekly sellers remain defensive from within the walls of supply drawn in at 1.3120-1.2957. Down on the daily timeframe, the support area seen at 1.3058-1.2979 is, in our opinion, now vulnerable to the downside. Not only do we have weekly sellers coercing price lower here, there has also been little to no bullish intent registered here since the area came into play. The next downside target on this timeframe does not come into view until we reach a support area at 1.2818-1.2752, which happens to be glued to the top edge of weekly demand at 1.2589-1.2759 (the next area of interest on the weekly chart) and converges beautifully with a channel support etched from the low 1.2365.

Our suggestions: The H4 range is likely going to suffer a break to the downside either today or early next week, given the bearish tone being painted on the higher timeframes right now. To that end, we're watching for a H4 close to print below the current range. This – coupled with a successful retest would, in our humble view, be enough evidence to suggest a move down to the 1.29 handle, followed closely by June's opening line at 1.2870/H4 Quasimodo support at 1.2857.

Data points to consider: US Inflation figures scheduled for release at 1.30pm, followed closely by FOMC members Kaplan and Kashkari taking the stage at 2.40/4.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Watch for H4 price to close below the 1.2950 region and then look to trade any retest seen thereafter ([waiting for a reasonably sized bearish candle to form following the retest – in the shape of either a full, or near-full-bodied candle – is advised] stop loss: ideally beyond the candle's wick).

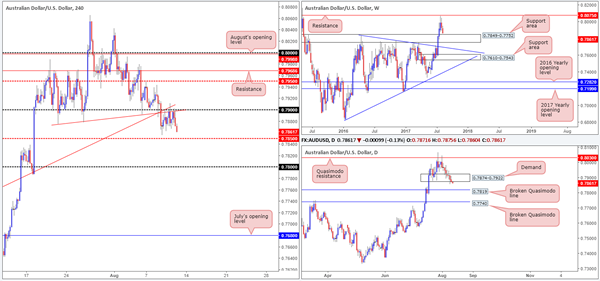

AUD/USD

Kicking this morning's analysis off with a quick look at the weekly timeframe, we can see that price is currently trading within striking distance of a major support area at 0.7849-0.7752. With this area having been a strong zone of resistance in the past, a bullish response will likely be seen from this region. In conjunction with weekly flow, daily demand at 0.7874-0.7922 appears incredibly vulnerable at the moment. Further selling from here will likely bring the unit down to a broken daily Quasimodo line drawn from 0.7819, which is planted around the top edge of the noted weekly support area.

Across on the H4 timeframe, Aussie bears remain defensive around the 0.79 handle. What gives this number extra credibility is the two H4 trendline resistances (0.7874/0.7635). A close below the nearby H4 mid-level support at 0.7850 today will likely open up the trapdoor down to the aforesaid broken daily Quasimodo line, and maybe even the 0.78 handle.

Our suggestions: Should the unit continue to decline in value, we'll then be eyeing the 0.7819/0.78 region for potential long opportunities. Given that psychological boundaries such as 0.78 attract stop hunts, we're going to wait and see if additional H4 candle confirmation is seen before committing to a position here. In the event that a trade comes to fruition, we'll look to reduce risk to breakeven around the 0.7850 range and take partial profits at 0.7874 (the underside of the current daily demand).

Data points to consider: US Inflation figures scheduled for release at 1.30pm, followed closely by FOMC members Kaplan and Kashkari taking the stage at 2.40/4.30pm GMT+1.

Levels to watch/live orders:

- Buys: 0.78/0.7819 region ([waiting for a H4 bullish candle, preferably a full, or near-full-bodied candle, to form is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

USD/JPY

Risk-off conditions, as you can see, continue to support the Japanese yen. The currency also gained momentum following the release of July's US PPI figures on Thursday, which came in lower than expected. This bearish run, however, could be tested today.

On the weekly timeframe, demand at 108.13-108.95 is now seen within shouting distance. In addition to this, a daily Quasimodo support was recently brought into the picture at 109.11, alongside the 109 handle printed on the H4 timeframe.

Our suggestions: Collectively, all three timeframes show structure suggesting a buy in this market today. The question is how does one go about finding an entry? Simply clicking the buy button, in our opinion, just won't do given the strength of the approach seen into the above said supports.

Personally, for us to commit to a long from 109, we would want to see H4 price break back into the nearby channel edge taken from the low 110.30, and then retest 109 again as support (as per the black arrows). Ultimately, we'd be looking to target 109.62 initially, followed by the 110 handle which converges with a H4 channel resistance taken from the high 111.71.

Data points to consider: US Inflation figures scheduled for release at 1.30pm, followed closely by FOMC members Kaplan and Kashkari taking the stage at 2.40/4.30pm GMT+1.

Levels to watch/live orders:

- Buys: 109 region ([waiting for a H4 bullish candle, preferably a full, or near-full-bodied candle, to form is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

USD/CAD

Trade update: small loss taken at 1.2723 – see Thursday's report for details.

The USD/CAD came under strong selling pressure from H4 supply at 1.2747-1.2722 in early US trading on Thursday. Although the move forced the pair below the 1.27 handle, there was little follow through generated. In fact, immediately after the bearish close registered, price was heavily bid back above 1.27 and driven into the upper extremes of the said H4 supply.

In view of the marginal close seen above the daily resistance area at 1.2654-1.2734, and the strong bullish sentiment seen on the weekly timeframe from the support area at 1.2433-1.2569, we feel further buying may be on the cards today, next week.

Our suggestions: Ultimately, what we're looking for is a decisive H4 close above the current H4 supply. This, alongside a retest would, in our view, be a valid buy signal especially considering that both weekly and daily action show room to extend much, much higher. The first area of concern, should a trade come to fruition, would be the 1.28 handle.

Data points to consider: US Inflation figures scheduled for release at 1.30pm, followed closely by FOMC members Kaplan and Kashkari taking the stage at 2.40/4.30pm GMT+1.

Levels to watch/live orders:

- Buys: Watch for H4 price to close above the current H4 supply and then look to trade any retest seen thereafter ([waiting for a reasonably sized bullish candle to form following the retest – in the shape of either a full, or near-full-bodied candle – is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

USD/CHF

For those who read Thursday's report on the USD/CHF, you may recall our desk placing emphasis on June and August's opening levels at 0.9680/0.9672 as a potential area to sell. As you can see, price reacted beautifully to this zone, and even chalked up a nice-looking H4 bearish pin bar. Well done to any of our readers who jumped aboard this move.

Technically speaking, the next hurdle on the hit list will likely be the 0.96 handle, followed closely by July's opening level at 0.9580. However, according to the weekly and daily timeframes, we could be looking at trading lower than these two structures, as the next area of support on the weekly chart comes in at 0.9443-0.9515, with a daily support seen pegged a little higher at 0.9546.

Our suggestions: Despite the higher timeframes suggesting lower prices, we would advise against selling into the 0.96 handle and nearby July opening level. The bounce from these structures could place you in unnecessary drawdown. Waiting for a break below these levels, therefore, could be an option, but by doing so you're left with little room to maneuver as the daily support mentioned above sits at 0.9546!

Data points to consider: US Inflation figures scheduled for release at 1.30pm, followed closely by FOMC members Kaplan and Kashkari taking the stage at 2.40/4.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

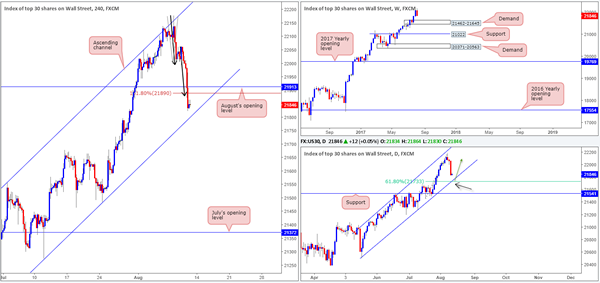

DOW 30:

The US equity market ended the day recording a rather substantial loss amid geopolitical issues between the US and North Korea. The index ran through August's opening level at 21913 and also took out the H4 AB=CD 161.8% Fib ext. point at 21890.

On the H4 timeframe, we can also see that to the downside we have a nearby channel support extended from the low 21273. More importantly, however, there's a nearby DAILY channel support seen just below this which has been drawn from the low 20494. Given how close together both channel supports are, and the fusing of a daily 61.8% Fib support at 21733 (taken from the low 21462), a bounce higher from this area is likely.

Our suggestions: In view of the technical landscape at the moment, we believe that the H4 channel support will likely suffer a minor fakeout, as traders may press for the daily channel support and its converging 61.8% Fib support for long opportunities.

Therefore, our plan of attack is simple: wait for H4 price to connect with the said daily channel line, and enter long on the basis of a reasonably sized H4 bull candle, preferably in the shape of a full, or near-full-bodied candle.

Data points to consider: US Inflation figures scheduled for release at 1.30pm, followed closely by FOMC members Kaplan and Kashkari taking the stage at 2.40/4.30pm GMT+1.

Levels to watch/live orders:

- Buys: 21733 region ([waiting for a H4 bullish candle to form, preferably either a full, or near-full-bodied candle, is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

GOLD:

With the US dollar taking another hit to the mid-section, the yellow metal rose higher for a third consecutive day. This has brought the unit into an interesting area of weekly resistance (green zone) comprised of two Fibonacci extensions 161.8/127.2% at 1312.2/1284.3 taken from the low 1188.1. Weekly price has, as you can see, responded each time this area has been challenged, therefore there's a chance that we may see history repeat itself here.

Down on the daily timeframe, nevertheless, yesterday's move lifted price above a trendline resistance extended from the high 1337.3. This, at least on this scale, signals further upside could be on the horizon.

Bouncing over to the H4 candles, we can see that supply at 1281.1-1275.4 was recently taken out (now an acting support area) and saw the metal attack a nearby supply seen at 1288.8-1283.4.

Our suggestions: Judging the recent H4 candle action, sellers are active within the current supply. Whether they're strong enough to halt buying is difficult to judge. On the one hand, weekly sellers may come into the picture today/early next week, but on the other hand a great deal of daily buyers saw the recent close above the trendline resistance and will be looking to buy.

Although we're very tempted to begin hunting for sell opportunities in this market, we would prefer to see daily price close back below the said trendline resistance before taking that risk. Therefore, opting to wait on the sidelines may be the better path to take today.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

Daily Technical Analysis: EUR/USD Breaks Falling Wedge And Starts Wave B Correction

Currency pair EUR/USD

The EUR/USD bearish retracement indeed turned at the support zone (blue lines) as expected in yesterday's wave analysis. Considering the divergence on this 4 hour chart, the bearish price action could be just one part of larger ABC (purple) retracement within wave 4 (green).

The EUR/USD broke above the resistance (dotted orange) of yesterday's falling wedge chart pattern and could moving towards the Fibonacci levels of wave B vs A which could act as potential resistance spots.

Currency pair USD/JPY

The USD/JPY is breaking below the larger support trend line (blue) from the daily support at 109.50. This bearish break could indicate a downtrend continuation within wave C (brown).

The USD/JPY is breaking below the larger support trend line (blue) from the daily support at 109.50. This bearish break could indicate a downtrend continuation within wave C (brown).

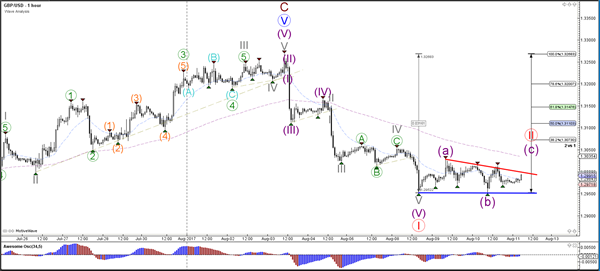

Currency pair GBP/USD

The GBP/USD seems to have completed 5 bearish waves within wave 1 (red). The Cable could be building a potential bullish retracement as part of a wave 2 (red).

The GBP/USD has support and resistance trend lines which could offer breaking spots for the Cable. A bullish breakout could lead to a wave C (purple) whereas a bearish break could see the downtrend continue.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 141.12; (P) 142.22; (R1) 142.82; More

GBP/JPY reaches as low as 141.37 so far as decline from 147.76 continues. Intraday bias stays on the downside for deeper fall. Sustained trading below trend line support will pave the way to 135.58/138.65 support zone. As GBP/JPY is seen as staying in consolidation pattern from 148.42, we'd expect strong support from 135.58 to contain downside. On the upside, above 142.25 minor resistance will turn intraday bias neutral first. But near term outlook will remain bearish as long as 144.01 support turned resistance holds.

In the bigger picture, the sideway pattern from 148.42 is extending with another leg. But we'd expect strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Medium term rise is still expected to resume later. And break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. However, firm break of 135.58/39 will dampen the bullish view and turn focus back to 122.36 low.

Yen Surges Further as Trump Stepped Up His Verbal Combat With North Korea

Risk aversion continues to dominate the global financial markets. DOW dropped -204.69 pts, or -0.93% overnight to close at 21844.01, comparing to intra-week high at 22179.11. S&P 500 also lost -35.81 pts, or -1.45% to close at 2438.21. Selloff in equities extends in Asian session. While Japan is on holiday, but Hong Kong HSI is trading down -1.8%, Korean KOSPI down -1.7% and Australia ASX 200 down -1.3%. In the currency markets, Japanese yen remains the strongest currency, followed by Swiss Franc and commodity currencies are all under pressure. Gold is staying firm above 1290 and is still on course for 1300 handle. WTI crude oil, however, is heading back to 48 after breaching 50 briefly.

Trump: They should be very nervous

Selloff in stocks and rally in Yen picked up steam again after US President Donald Trump stepped up his verbal combat with North Korea. Trump warned that "they should be very nervous, because things will happen to them like they never thought possible, OK?" And he said North Korea Kim Jong UN "has been pushing the world around for a long time". And, Trump stood by his "fire and fury" threat on North Korean and went further to say that the statement maybe "wasn't tough enough".

New York Fed Dudley: Take time to recent weak inflation readings to drop out

New York Fed President William Dudley said that inflation will "start to move higher in the medium term". However, he also noted inflation "probably not get all the way back to sort of 2% on a year-on-year basis". He noted that there have been "very weak inflation readings for a number of months in a row". And it will "take some time" for them to "drop out of" the annual readings. The economy will have a "continued moderate growth trend". However, the "comparatively modest" wage growth argues that "productivity growth has been sluggish compared to historical experience."

RBA Lowe: Next move will be up rather than down

RBA Governor Philip Lowe told the parliament today that the next move in interest rate will be "up rather than down", but that is "quite some time away". He referred to market pricing that "implies greater probability of a rate rise than a rate reduction". Also, another implication is that "the next move in interest rates is a long way out". Lowe said they're "both reasonable assumptions". Meanwhile, he also pointed to the high exchange rate as having negative impact on the outlook. He noted that "further appreciation, all else constant, would cause a slower pick-up in inflation and slower progress in reducing unemployment."

On the data front

New Zealand business NZ manufacturing index dropped to 55.4 in July. Germany will release CPI final in European session. US will release July CPI later in the day.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 141.12; (P) 142.22; (R1) 142.82; More

GBP/JPY reaches as low as 141.37 so far as decline from 147.76 continues. Intraday bias stays on the downside for deeper fall. Sustained trading below trend line support will pave the way to 135.58/138.65 support zone. As GBP/JPY is seen as staying in consolidation pattern from 148.42, we'd expect strong support from 135.58 to contain downside. On the upside, above 142.25 minor resistance will turn intraday bias neutral first. But near term outlook will remain bearish as long as 144.01 support turned resistance holds.

In the bigger picture, the sideway pattern from 148.42 is extending with another leg. But we'd expect strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Medium term rise is still expected to resume later. And break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. However, firm break of 135.58/39 will dampen the bullish view and turn focus back to 122.36 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ Manufacturing Index Jul | 55.4 | 56.2 | 56 | |

| 6:00 | EUR | German CPI M/M Jul F | 0.40% | 0.40% | ||

| 6:00 | EUR | German CPI Y/Y Jul F | 1.70% | 1.70% | ||

| 12:30 | USD | CPI M/M Jul | 0.20% | 0.00% | ||

| 12:30 | USD | CPI Y/Y Jul | 1.80% | 1.60% | ||

| 12:30 | USD | CPI Core M/M Jul | 0.20% | 0.10% | ||

| 12:30 | USD | CPI Core Y/Y Jul | 1.70% | 1.70% |

Market Morning Briefing: Pound Has Come Off A Bit

STOCKS

Overall the stock indices are all in a corrective mode and could possibly take some time to recover. We need to see if the supports near current levels hold for Dax, Nikkei and Nifty.

Dow (21844.01, -0.93%) fell sharply from levels near 20000. The index could possibly test 21750/00 over the next couple of sessions before again rising back towards 22000.

Dax (12014.30, -1.15%) seems to be trading near interim support and could bounce back in the next few sessions.

Shanghai (3230.61, -0.95%) is expected to maintain the sideways movement for a few more sessions before trying to rise higher. For now, trade within the 3220-3300 region looks likely.

Nikkei (19729.74, -0.05%) is also testing immediate support on the 3-day candle charts. While that holds, there is some scope of bouncing back towards 20200; else a fall towards 19400 and lower could be seen within the next 1-2 weeks.

Nifty (9820.25, -0.89%) has tested an important medium term support near 9775 yesterday and if it fails to remain above 9775 it could be indicative of a sharp fall in the coming sessions towards levels near 9600-9400. Only if it sustains above 9775, we may expect a retest of levels near 10000 in the near term.

COMMODITIES

Gold (1291) has risen in line with our expectations and broke above the immediate resistance of 1285 thus it might continue the rally towards 1300-1315. Failure to rise above 1300 may push it back to1280 and 1267 respectively. We will remain bullish on Gold while it is trading above 1260-65 regions.

Silver (17.06) is trading above the higher end of the previous range of 16.00-17.00. Immediately resistance is at 17.22 levels, where we might see some weekly profit taking.

Copper (2.88) has been taking pause for the last 2 sessions but the trend remains firmly up and the target of 3.00 and the support of 3.12 remain unchanged. Only a close below 2.78 levels could negate the short term bullish view.

Brent (51.70) and WTI (48.22) had moved lower in line with our expectations. Brent needs a break above the immediate resistance of 53.00 and WTI, above 50.50 to extend their respective rally to 56 and 54. Othwise we might see consolidation at 50/brent and 46.50/WTI levels to gather fresh buying momentum.

FOREX

Dollar Index (93.33) is trading within a narrow range between 93-94.10 and a weekly close above 94.10 could open up 95 and 96.30 levels as well. Although the larger trend is still down but we have to a little cautious beyond 94.10 region to identify the possibility of a change in trend in short term time frame.

Euro (1.1762) is still continuing its corrective behavior and a upside possibilities can be considered only on a break above 1.1800-25 regions. Till then, the downside risk for 1.1650-00 remains greater.

Dollar Yen (108.92) has broken below our important support levels near 109.50. There are chances of seeing fresh fall towards 108.10 in the next few sessions. Near term looks bearish.

Pound (1.2983) has come off a bit. 1.3050 is an important levels to watch for and while the price remains below 1.3050, we will have to allow for a fall towards 1.2930 or even 1.2850 in the coming sessions.

Aussie (0.7849) is headed towards 0.7835 which is an immediate interim support. On a break below 0.7835, we my have to consider a fall towards 0.7760 in the coming sessions.

Dollar Rupee (64.08) closed just below our initial target of 64.10/12 yesterday but on the offshore market the currency pair is trading near 64.25 that we had been looking for on a break above 64.12. Dollar rupee could open higher on the Official market but we will have to keep an eye on whether it breaks above 64.25/27 or not. A break above 64.27 could open up fresh rise on the upside.

INTEREST RATES

The US yields have fallen. The 10YR (2.21%) is down from 2.24% seen yesterday and we could see the current fall to continue towards 2.20-2.18% in the near term.

The US-Japan 10Yr (2.15%) is testing important near term support at current levels and could possibly bounce back in the next couple of sessions taking up Dollar Yen with itself. In that case some recovery is possibly in Nikkei too. Else, a break below 2.15% on the yield spread could indicate a fresh fall coming up.

The German-US 10Yr (-1.80%) has bounced back sharply and if it continues to rise towards -1.75% as expected, Euro strength could be expected in the coming sessions.

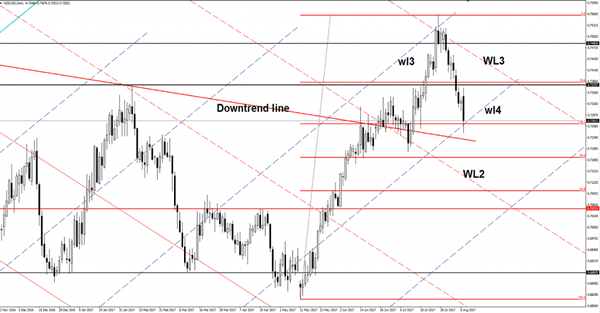

NZD/USD Is This A False Breakdown?

NZD/USD plunged and reached the 0.7251 level, but failed to stay there as the USDX has slipped lower after the poor US data. Price dropped below the confluence area formed at the intersection between the 38.2% with the fourth warning line (wl3), a valid breakdown will accelerate the sell-off, while a fake out will send the rate towards the 23.6% retracement level.

Brent False Breakout, Sell-off Favored

Price made another false breakout above the 53.03 static resistance and now is trading in the red again. Is trading near the $52.30 per barrel and could drop towards the $50.30 per barrel because the price could be attracted by the confluence area formed at the intersection between the sliding line (SL) with the uptrend line (ascending dotted line). The perspective remains bullish as long as is trading within the minor ascending channel.

USD/JPY Poised For Valid Breakdown

Price dropped significantly on Thursday and looks determined to drop towards fresh new lows in the upcoming period. Is very heavy as the USDX slips lower after the poor US data and because the Yen is boosted by the Nikkei stock index.

I've said in the previous days that the Yen should dominate the currency market if the JP225 will take out the 19700 static support. Nikkei plunged much below the mentioned static support and looks unstoppable on the daily chart. The index could find support at 19278 or lower at the 18936 static support.

USD/JPY is going down as the greenback has taken a hit from the US high impact data, the PPI dropped by 0.1%, even if the traders have expected to see a 0.1% growth, while the Unemployment Claims increased from 241K to 244K, failing to reach the 240K jobs in the previous week.

Price is trading in the red and has managed to drop below the downside line (red line) of the symmetrical triangle and below the 50% retracement level. A valid breakdown from the chart pattern and a retest of the 50% level will confirm a further drop. Price should drop around 700 pips if will breakout from the symmetrical triangle. I don't know if it will drop so much, but a broader drop will come for sure.

Support can be found at the warning line (wl1), but a further Nikkei's drop will help the price to ignore this downside obstacle.

We have important downside targets at 61.8% retracement level, at the 38.2% retracement level and at the second warning line (WL2).