Sample Category Title

RBNZ Remains On The Sidelines

Market movers today

Market focus will be on the escalating tension between the US and North Korea over North Korea's missile programme.

In the UK, industrial production and construction data for June are out today. This is of interest given the negative growth contributions from manufacturing and construction. The NIESR GDP estimate for July (usually a good predictor of actual GDP growth) and trade balance figures will be announced too.

In the US, FOMC member Dudley's speech is likely to be the main event. PPI data and the Monthly Budget Statement are also due for release.

In Scandi markets, Danish and Norwegian inflation data as well as Swedish industrialand services production data are released today. Please see the Scandi section on page 2 for further details.

Selected market news

North Korea sabre-rattling continues as US seeks to ease tensions. Overnight, state media reported that North Korea is examining plans to fire four intermediate-range ballistic missiles at Guam. The missiles would be fired by mid-August, pass over Japan and land near the island which holds strategically important US military bases. The statement came in response to US President Trump's 'fire and fury' warning on Tuesday. Earlier, US secretary of state Tillerson had sought to downplay tensions, saying that North Korea posed no 'imminent threat'.

UK real estate slump spreads. The RICS survey released overnight showed prices stagnating in July, as the price decline of prime properties in the centre of London spread to neighbouring areas. Meanwhile, prices in Northern Ireland, the West Midlands and the southwest increased.

RBNZ remains on the sidelines. In New Zealand, the central bank left the official cash rate unchanged at 1.75% overnight, in line with expectations. Reflecting recent subdued economic data, the RBNZ said that monetary policy would be kept accommodative for a considerable period.

Geopolitical concerns triggered by North Korea tensions set the course for a modest riskoff reaction on markets yesterday. In Europe, the Euro Stoxx 50 index closed down 1.3% and 10yr Bund yields declined 4bp. In the US, the S&P500 index pared earlier losses to close the day flat. US 10yr Treasury yields held steady around 2.25%. This morning, Asian stocks have reversed earlier gains, while emerging markets sold off more broadly.

Daily Technical Analysis: EUR/USD ABC Zigzag Challenges Support Zone And Aims At 1.16

Currency pair EUR/USD

The EUR/USD bearish retracement bounced at the support zone (blue lines), which might indicate that the wave A (purple) retracement has been completed. The wave A is part of a larger ABC correction within wave 4 (green) which could fall towards the 23.6% Fibonacci level of wave 4 vs 3.

The EUR/USD broke below the support trend line (dotted green) and completed a wave 5 (orange), which in turn could complete a larger wave A (purple). Now price is building a falling wedge chart pattern, which is a bullish reversal pattern. A break above the resistance trend line (orange) would confirm the break and potential ABC (brown) correction within wave B (purple). A break below the support trend line (blue) could indicate a bearish breakout towards the 23.6% Fib at 1.16.

Currency pair USD/JPY

The USD/JPY is testing a larger support trend line (blue) from the daily support at 109.50. A bearish break could see price continue lower within wave C (brown).

The USD/JPY seems to have completed a potential 5 wave which could be a wave 1 (orange). A break below support (green) could indicate the continuation of the bearish trend.

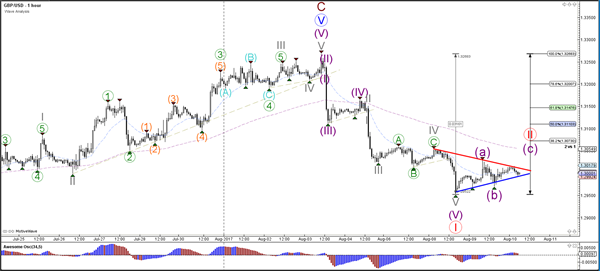

Currency pair GBP/USD

The GBP/USD seems to have completed 5 bearish waves within wave 1 (red). A bullish retracement could be part of a wave 2 (red).

The GBP/USD has support and resistance trend lines which could offer breaking spots for the Cable. A bullish breakout could a wave C (purple) develop whereas a bearish break could see the downtrend continue.

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

We typically search for lower-timeframe confirmation between the M15 and H1 timeframes, since most of our higher-timeframe areas begin with the H4. Stops are usually placed 1-3 pips beyond confirming structures.

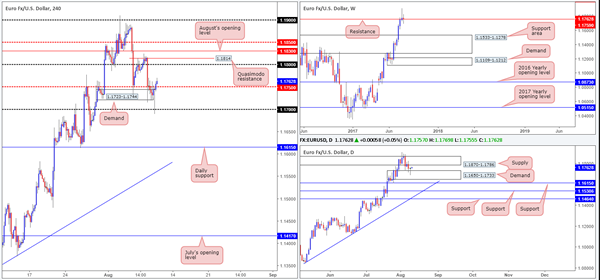

EUR/USD

EUR/USD bulls seem to have a slight edge this morning. After rather aggressively whipsawing through the lower edge of H4 demand at 1.1723-1.1744 and testing the 1.17 handle, the H4 candles ended the day marginally closing above the mid-level resistance pegged at 1.1750.

With room seen for price to extend north up to 1.18 (followed closely by a H4 Quasimodo resistance at 1.1814), and daily action recently printing a mouthwatering buying tail from within demand at 1.1650-1.1733, further buying is likely to be seen. However, one thing to keep in mind here is weekly price. Last week’s trade chalked up a strong-looking selling wick just above a resistance located at 1.1759. Although we have seen little bearish intent from here, it is still worth keeping an eyeball on.

Our suggestions: A retest of 1.1750 as support today could bring about a buying opportunity. Should the retest be accompanied by a lower-timeframe buying signal (see the top of this report), an intraday long targeting the 1.18 neighborhood has potential. Be that as it may, do remain aware of the nearby daily supply at 1.1870-1.1786, specifically the lower edge positioned at 1.1786. This could halt buying and prevent H4 price from reaching 1.18.

Data points to consider: US PPI figures and weekly unemployment claims at 1.30pm, followed by FOMC member Dudley taking the stage at 3pm GMT+1.

Levels to watch/live orders:

- Buys: 1.1750 region ([waiting for a lower-timeframe confirming signal to form is advised before pulling the trigger] stop loss: dependent on where one confirms the area).

- Sells: Flat (stop loss: N/A).

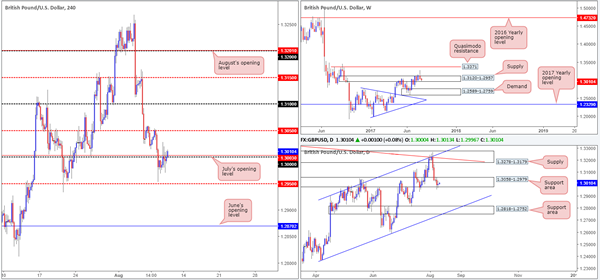

GBP/USD

Following Tuesday’s low of 1.2952, the GBP/USD staged a moderate recovery and, as far as we can see, looks poised to now close above the large psychological boundary 1.30 and July’s opening level at 1.3003. The next upside target beyond 1.30 can be seen at the mid-level resistance drawn from 1.3050, which did a superb job in holding the unit lower on Tuesday.

Over on the bigger picture, weekly price is currently trading within the walls of a supply zone coming in at 1.3120-1.2957. On the other side of the field, however, daily flow remains loitering within a support area fixed at 1.3058-1.2979. With that being said, it may be worth noting that daily candlestick action has printed very little in terms of bullish intent. In fact, the latest movement chalked in an indecision candle.

Our suggestions: With conflicting signals being seen between the weekly and daily charts at the moment, this leaves traders in a somewhat precarious position: either buy into potential weekly selling or sell into possible daily buying. On account of this, a trade above the 1.30 handle is challenging and not really something we want to get involved in.

Data points to consider: UK Manufacturing production at 9.30am. US PPI figures and weekly unemployment claims at 1.30pm, followed by FOMC member Dudley taking the stage at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

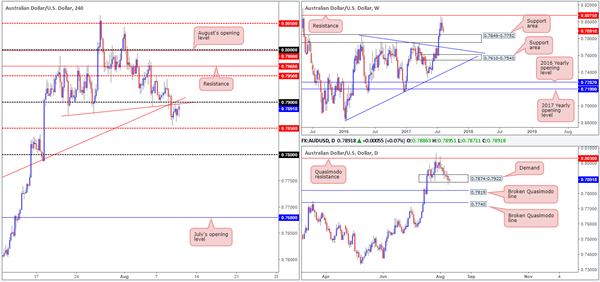

AUD/USD

In recent trading, we saw the H4 candles dive below the 0.79 boundary and bottom just ahead of the mid-level support at 0.7850. Shortly after this, price retested the underside of 0.79 which fuses beautifully with two H4 trendline resistances (0.7874/0.7635). Should the bears continue to defend this line, 0.7850 is likely going to see some action sometime today.

In support of further selling, the daily timeframe shows price recently pierced beneath the lower edge of demand at 0.7874-0.7922, likely triggering a truckload of sell stops and clearing the path south down to a broken Quasimodo line at 0.7819. In addition to this, on the weekly timeframe price shows space for the market to trade down to a support area coming in at 0.7849-0.7752.

Our suggestions: On account of the above notes, we are watching for H4 price to print a reasonably sized bearish candle from 0.79 in the shape of a full, or near-full-bodied candle. The first take-profit zone would, for us, be the H4 mid-level support at 0.7850 (largely because this denotes the top edge of the noted weekly support area), followed closely by a daily broken Quasimodo line mentioned above at 0.7819.

Data points to consider: US PPI figures and weekly unemployment claims at 1.30pm, followed by FOMC member Dudley taking the stage at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 0.79 region ([waiting for a H4 bearish candle, preferably a full, or near-full-bodied candle, to form is advised] stop loss: ideally beyond the candle’s wick).

USD/JPY

After dropping sharply over the past couple of days, the pair managed to find a floor of bids around a H4 support level at 109.62 on Wednesday. The response to this level helped break and eventually close above the 110 handle, leaving the path north free up to August’s opening line at 110.30, followed closely by the H4 mid-level resistance at 110.50 and then the H4 channel resistance extended from the high 111.71.

While near-term action shows the possibility of further buying, weekly price continues to head south in the direction of a small demand pegged at 108.13-108.95. The daily candles on the other hand, recently came within touching distance of a trendline support taken from the low 108.13 after selling off from resistance marked at 110.76.

Our suggestions: Seeing as H4 structure is rather cluttered above 110 at the moment, along with both weekly and daily price still showing room for further downside, we will not be considering any trades in this market today.

Data points to consider: US PPI figures and weekly unemployment claims at 1.30pm, followed by FOMC member Dudley taking the stage at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

USD/CAD

The US dollar, as you can see, pushed higher against its Canadian counterpart on Wednesday, bringing price up to within a few pips of the underside of a H4 supply seen at 1.2747-1.2722. According to weekly price, further upside should not really come as much of a surprise as the pair recently rebounded from a support area coming in at 1.2433-1.2569. Conversely, however, the daily timeframe shows that although further buying was seen, price remains within the confines of a resistance area carved from 1.2654-1.2734.

As we highlighted in previous reports, our desk would not consider becoming buyers in this market until a close above the current daily resistance area is seen. Despite what the weekly timeframe suggests, buying into the current daily structure is a risk we’re just not willing to take here. In Wednesday’s report, we also showed interest in selling should price tag the H4 supply and close back below 1.27, which recently came to fruition.

Our suggestions: The move below 1.27 from the H4 supply, for us, confirms lower prices down to at least the 1.26 neighborhood. As such, we have sold at 1.2696 and positioned our stop at 1.2723 (27 pips) and are looking to take partial profits around the 1.2650 region (46 pips). We understand that we have effectively sold into potential weekly buying here, but the evidence of a move lower is strong given the current trend and daily resistance area.

Data points to consider: US PPI figures and weekly unemployment claims at 1.30pm, followed by FOMC member Dudley taking the stage at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1.2696 ([live] stop loss: 1.2723).

USD/CHF

In recent sessions the USD/CHF plunged lower, following Tuesday’s reaction to the H4 Quasimodo resistance at 0.9762 and the H4 mid-level resistance at 0.9750. Both June and August’s opening levels at 0.9680/0.9672 were easily cleared with price ultimately going on to bottom just ahead of the 0.96 handle. Shortly after this, price retested 0.9672 beautifully as resistance and held lower into the close.

Technically speaking, the move lower should have not really come as much of a surprise, as weekly price is seen trading from a major trendline resistance extended from the low 0.9257. Also noteworthy is daily price is now seen trading back into the walls of a daily descending channel (0.9808/0.9622).

Our suggestions: Basically, our team is watching 0.9680/0.9672 on the H4 chart for a potential shorting opportunity today, targeting the 0.96 line as an initial take-profit level. Not only has 0.9672 already proved its ability to hold price lower, the small area also houses a H4 38.2% Fib resistance at 0.9673 taken from the high 0.9772. However, due to the threat of a potential fakeout up to 0.97, we would strongly advise against placing pending orders here. Instead, wait for the candles to confirm bearish intent. What we personally look for is a candle response in the shape of a full, or near-full-bodied candle to confirm seller interest.

Data points to consider: US PPI figures and weekly unemployment claims at 1.30pm, followed by FOMC member Dudley taking the stage at 3pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 0.9680/0.9672 ([waiting for a H4 bearish candle to form, preferably either a full, or near-full-bodied candle, is advised] stop loss: ideally beyond the candle’s wick).

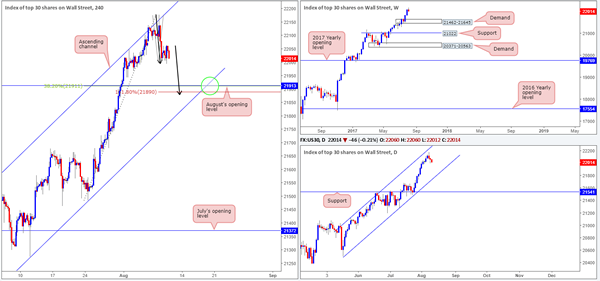

DOW 30

It was a quiet day in the US equity market yesterday, with price ranging no more than 85 points. Given the rather lackluster performance, much of the following report will echo thoughts put forward in Wednesday’s analysis.

On Tuesday, H4 action once again challenged the ascending channel resistance drawn from a high of 21556. Currently, we do not see much in the way of support until August’s opening level at 21913, so further selling could be on the cards today. As 21913 fuses almost perfectly with a H4 38.2% Fib support at 21911 (taken from the low 21484), we feel a bounce from this neighborhood could be on the cards.

Our suggestions: With this market currently entrenched within an incredibly strong uptrend which shows little sign of decelerating, a buy from the 21913 vicinity is of interest to our desk.

Just to be clear though, we would only consider a buy if one of the following takes shape:

H4 price tests 21913 once the market is in line with the neighboring channel support extended from the low 21273 (green circle).

The unit chalks up a H4 AB=CD approach as per the black arrows (161.8 Fib ext. point at 21890).

To avoid any fakeout through 21913, nonetheless, we would also strongly recommend waiting for H4 price to chalk up a bullish candle in the shape of a full, or near-full-bodied candle. This, of course, will not guarantee a winning trade, but what it will do is show buyer intent from a high-probability reversal zone.

Data points to consider: US PPI figures and weekly unemployment claims at 1.30pm, followed by FOMC member Dudley taking the stage at 3pm GMT+1.

Levels to watch/live orders:

- Buys: 21913 region ([waiting for a H4 bullish candle to form, preferably either a full, or near-full-bodied candle, is advised] stop loss: ideally beyond the candle’s tail).

- Sells: Flat (stop loss: N/A).

GOLD

The yellow metal sported another wave of buying during Wednesday’s segment, running through August’s opening level at 1269.3 and testing H4 supply at 1281.1-1275.4. Although the market has stalled within this boundary, we feel further buying may be upon us!

Over on the weekly chart, we can see that the market shows room for the metal to extend up to the green resistance zone comprised of two Fibonacci extensions 161.8/127.2% at 1312.2/1284.3 taken from the low 1188.1. What’s also interesting is that daily action also shows space for the unit to extend up to a trendline resistance taken from the high 1337.3. Not only do we have the higher timeframes suggesting a punch higher is likely on the cards, but H4 price also shows that a drive above the H4 supply could happen, as price attempts to complete the current AB=CD move (black arrows –127.2% ext. at 1282.2).

Our suggestions: In view of the above, we have absolutely zero interest in selling the piece right now. A buy on the other hand, would become interesting if the unit retested August’s opening level mentioned above at 1269.3. Apart from this, we see little else to hang our hat on until we reach the aforementioned daily trendline resistance and weekly resistance zone.

Levels to watch/live orders:

- Buys: 1269.3 region is interesting for a buy ([waiting for a H4 bullish candle to form, preferably either a full, or near-full-bodied candle, is advised] stop loss: ideally beyond the candle’s tail).

- Sells: Flat (stop loss: N/A).

European Open Briefing: Asian Stocks Turned Lower

Global Markets:

- Asian stock markets: Nikkei fell 0.04 %, Shanghai Composite down 0.92 %, Hang Seng dropped 1.28 %, ASX 200 fell 0.21 %

- Commodities: Gold at $1282.71 (+0.27 %), Silver at $16.86 (+0.06 %), WTI Oil at $49.55 (-0.02 %), Brent Oil at $52.70 (+0.02 %)

- Rates: US 10-year yield at 2.24, UK 10-year yield at 1.10, German 10-year yield at 0.43

News & Data:

- Crude Oil Inventories -6.5 M vs -2.6 M expected

- RBNZ Interest Rate Decision 1.75 % vs 1.75 % expected

- GBP Rics House Price Balance 1 % vs 8 % expected

- CAD Building Permits m/m 2.5 % vs -1.8 %

- AUD MI Inflation Expectations 4.2 % vs 4.4 % previous

- North Korea calls Trump's warning a 'load of nonsense'- RTRS

- Japan PM should focus on regulatory reforms, say economists- RTRS

Markets Update:

Asian stocks turned lower reversing earlier gains on Thursday as investors continued to take risks off the table owing to the continued tensions between the United States and North Korea

EUR/USD was little changed and slipped down only about 0.1 percent in value to the lows of 1.1732 while the dollar index against a basket of major currencies added 0.1 percent to 93.620.

NZD/USD slipped to a near one-month low of $0.7300 losing 0.5 % after Reserve Bank of New Zealand Governor Graeme Wheeler’s comments on the NZ Dollar.

AUD/USD opened Asia 0.7991 after a steady session in the Wall Street, before reversing lower to revisit the session low at 0.7870 loosely tracked by the movements in the NZD.

USD/JPY after going as low as 109.560, its weakest in eight weeks. ticked a few points higher into the Tokyo fix time today, popping above 110.10 briefly before giving back some of its gains.

Upcoming Events:

- 08:30 GMT – (GBP) Manufacturing Production m/m

- 12:30 GMT – (USD) Unemployment Claims

- 12:30 GMT – (USD) PPI m/m

- 23:30 GMT – (AUD) RBA Gov Lowe Speaks

Market Update – Asian Session: RBNZ Assures Rate To Be Left On Hold For Now

Asia Summary

Asian equity markets opened slightly higher before falling nearly 1% across the board on continued tensions with North Korea. The US has affirmed that all options remain on the table when it comes to North Korea. USD took safety flows on the continued tension, though outside of the NZ$ there were no large moves. Moves likely to remain a bit volatile on thinner volume, as we exit the peak of earnings season and get knee deep in the largest summer holiday month. China’s yuan has been steadily appreciating recently, with today’s setting the highest since mid-September, and is up ~4% so far in 2017.

The Kiwi fell 0.7% to 0.7300 after RBNZ kept cash target rate unchanged at 1.75%. Gov Wheeler said that RBNZ is still very much Neutral on rates and for foreseeable future does NOT see OCR increasing. He did confirm monitors "traffic light system" for currency intervention 'closely', won't comment on whether currency strength is affecting the system. Later speaking to Parliament said intervention in FX market is always open to us, have intervened in the past, Then reiterated that he does not feel rate cut is needed at this time.

Key economic data

(NZ) New Zealand July Retail Card Spending M/M: -0.5% v 0.2% prior; Total Card Spending M/M: -0.7% v 8.3% prior

(JP) JAPAN JUN MACHINE ORDERS M/M: -1.9% V +3.6%E; Y/Y: -5.2% V -1.1%E

(JP) JAPAN JULY PPI M/M: 0.3% V 0.2%E; Y/Y: 2.6% V 2.3%E

(UK) JULY RICS HOUSE PRICE BALANCE: 1% V 9%E

Speakers and Press

China

(CN) Said that China Govt has summoned steel execs, regulators, bourse to discuss price surge - financial press

(CN) China propaganda chief visited govt workers holidaying at the resort of Beidaihe, signaling that an annual conclave of senior leaders was happening before an autumn party congress - Chinese press

Australia/New Zealand

(NZ) RBNZ Gov Wheeler: Still very much in Neutral on rates, for foreseeable future does NOT see OCR increasing; Structural factors weigh on inflation globally - post rate decision press conference

(NZ) RBNZ Gov Wheeler: Intervention in FX market is always open to us, have intervened in the past, always assessing criteria; Do not feel rate cut is needed - speaking to parliamentary committee

Korea

(KR) North Korea govt: our military will have a strike plan against Guam prepared by mid-August, then await orders from our leader

Japan

(JP) Japan publicly traded foreign stock investment trust total assets likely reached record high at end of July - Nikkei

Asian Equity Indices/Futures (00:00ET)

Nikkei -0.2%, Hang Seng -1.6%, Shanghai Composite -1.1%, ASX200 -0.1%, Kospi -1.1%

Equity Futures: S&P500 -0.3%; Nasdaq100 -0.4%, Dax -0.3%, FTSE100 -0.4%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1770-1.1733; JPY 110.18-109.89; AUD 0.7911-0.7870; NZD 0.7368-0.7299

Dec Gold +0.3% at 1,282/oz; Sept Crude Oil 0.0% at $49.55/brl; Sept Copper -0.1% at $2.93/lb

(CN) China PBOC OMO injects CNY90B in 7 and 14-day reverse repos v CNY140B prior; Injects net CNY30B v CNY0B prior

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT: 6.6770 V 6.7075 PRIOR (strongest setting since Sept 29th)

Equities notable movers

Hong Kong/China

Wanda Hotel Development,169.HK To acquire Wanda Culture Travel Innovation from a company indirectly owned by Wang Jianlin for CNY6.3B – filing; +20.8%

Japan

Toshiba,6502.JP Reports Q1 Net ¥50.3B v ¥79.8B y/y, Op ¥96.7B v ¥16.3B Rev ¥1.14T v ¥1.06T y/y; +1.4%

Toshiba, 6502.JP Reports delayed FY16 results, Net loss ¥966B v loss ¥460B y/y, Rev ¥4.87T v ¥5.15T y/y

Shiseido, 4911.JP Reports H1 Net ¥18.8B v ¥24.5B y/y; Op ¥34.7B v ¥19.9B y/y; Rev ¥472.1B v ¥412.3B y/y; +14.%

Australia

Virgin Australia,VAH.AU Reports FY17 Net loss A$220.3M v loss A$260.9M y/y; Rev A$5.05B v A$5.02B y/y; +5.7%

Origin, ORG.AU To recognize ~A$1.2B non-cash impairment charge in H2 from ALPNG, sees A$357M impairment related to Lattice; -1.0%

AGL.AU Reports FY17 Underlying Profit A$802M v A$788Me; underlying EBIT A$1.37B v A$1.36Be; Rev A$12.6B v A$11.9Be; +1.2%

Boart Longyear, BLY.AU Reaches settlement with First Pacific Advisors; +9.4%

India

Tata Motors,TTMT.IN Reports Q1 (INR) Net 31.8B v 22.4B y/y, Rev 598.2B v 597.9Be; -4.6%

Australia’s Consumer Inflation Expectation Fell In August

For the 24 hours to 23:00 GMT, the AUD declined 0.34% against the USD and closed at 0.7888.

LME Copper prices rose 1.6% or $101.0/MT to $6465.0/MT. Aluminium prices rose 1.9% or $37.0/MT to $2018.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7883, with the AUD trading 0.06% lower against the USD from yesterday's close.

Early morning data showed that Australia's consumer inflation expectation dropped to 4.2% in August, following a reading of 4.4% in the previous month.

The pair is expected to find support at 0.7860, and a fall through could take it to the next support level of 0.7838. The pair is expected to find its first resistance at 0.7908, and a rise through could take it to the next resistance level of 0.7934.

Looking forward, a speech by the RBA Governor, Philip Lowe, scheduled overnight, will be keenly watched by market participants.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Euro Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the EUR slightly declined against the USD and closed at 1.1759.

On the data front, Italy’s seasonally adjusted industrial production rose more-than-expected by 1.1% on a monthly basis in June, compared to market expectations for an advance of 0.2%. In the previous month, industrial production had recorded a rise of 0.7%.

In the US, data revealed that mortgage applications rebounded 3.0% in the week ended 04 August 2017, after recording a drop of 2.8% in the prior week.

In the Asian session, at GMT0300, the pair is trading at 1.1744, with the EUR trading 0.13% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.1699, and a fall through could take it to the next support level of 1.1653. The pair is expected to find its first resistance at 1.1780, and a rise through could take it to the next resistance level of 1.1815.

In absence of any major macroeconomic releases in the Euro-zone today, investors will keep a close watch on the US initial jobless claims and the monthly budget statement for July, slated to release later in the day.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

UK’s RICS House Prices Rose At Its Slowest Rate In Over 4 Years In July

.

For the 24 hours to 23:00 GMT, the GBP rose 0.12% against the USD and closed at 1.3010.

In the Asian session, at GMT0300, the pair is trading at 1.3, with the GBP trading 0.08% lower against the USD from yesterday's close.

Overnight data indicated that Britain's RICS house price balance unexpectedly fell to a level of 1.0% in July, hitting its lowest since March 2013. In the prior month, house price balance recorded a level of 7.0%, while market participants were expecting for a rise to a level of 9.0%.

The pair is expected to find support at 1.2971, and a fall through could take it to the next support level of 1.2943. The pair is expected to find its first resistance at 1.3028, and a rise through could take it to the next resistance level of 1.3057.

Ahead in the day, traders will look forward to Britain's total trade balance, manufacturing as well as industrial production and NIESR GDP estimate data, to gauge strength in the nation's economic activity.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Japan’s Machinery Orders Surprisingly Fell In June, Tertiary Industry Index Remained Flat In The Same Month

For the 24 hours to 23:00 GMT, the USD declined 0.15% against the JPY and closed at 109.96.

On the data front, Japan's preliminary machine tool orders recorded a rise of 26.3% on an annual basis in July. In the prior month, machine tool orders had risen 31.1%.

In the Asian session, at GMT0300, the pair is trading at 110.07, with the USD trading 0.1% higher from yesterday's close.

Overnight data indicated that the nation's machinery orders unexpectedly dropped 1.9% on a monthly basis in June, compared to a drop of 3.6% in the prior month, while markets were anticipating for a gain of 3.6%. Meanwhile, the nation's tertiary industry index remained flat in July, compared to a fall of 0.1% in the prior month. Market participants had expected the index to rise 0.2%.

The pair is expected to find support at 109.69, and a fall through could take it to the next support level of 109.32. The pair is expected to find its first resistance at 110.31, and a rise through could take it to the next resistance level of 110.56.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Swiss Franc Reverses Its Gains In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.93% against the CHF and closed at 0.9637.

The Swiss Franc jumped against the USD, as excessive geopolitical fears surrounding North Korea lured investors to the safe-haven appeal of the currency.

In the Asian session, at GMT0300, the pair is trading at 0.9655, with the USD trading 0.19% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9607, and a fall through could take it to the next support level of 0.9559. The pair is expected to find its first resistance at 0.9708, and a rise through could take it to the next resistance level of 0.9761.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.