Sample Category Title

Canada’s Housing Starts Surprisingly Climbed In July, Building Permits Recorded An Unexpected Rise In June

For the 24 hours to 23:00 GMT, the USD rose 0.24% against the CAD and closed at 1.2698.

Macroeconomic data indicated that Canada's seasonally adjusted housing starts surprisingly advanced to a level of 222.3K in July, defying market expectations for a fall to a level of 205.0K and highlighting resilience in the nation's housing market. In the prior month, housing starts had recorded a revised level of 212.9K. Moreover, the nation's building permits unexpectedly climbed 2.5% on a monthly basis in June, amid increased plans for commercial buildings. Building permits registered a revised rise of 10.7% in the previous month, while markets had envisaged for a drop of 1.9%.

In the Asian session, at GMT0300, the pair is trading at 1.2713, with the USD trading 0.12% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2680, and a fall through could take it to the next support level of 1.2648. The pair is expected to find its first resistance at 1.2733, and a rise through could take it to the next resistance level of 1.2754.

Ahead in the day, the release of Canada's new house price index for June, will be on investors' radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages

Elliott Wave View: FTSE 100 Pullback In Progress

Short term FTSE 100 ( UKX-FTSE ) Elliott Wave view suggests that Minor wave B ended on 6/30 low 7302.7 and the rally from there is unfolding as a double three Elliott wave structure where wave ((w)) ended at 7515.12 and wave ((x)) pullback ended at 7338.2. Index has reached 100% from 6/30 low so cycle is mature and Minor wave 1 has ended at 7551.85. Index is currently pulling back in Minor wave 2 to correct cycle from 6/30 low before the rally resumes. As far as pivot at 7302.7 low remains intact, Index should find buyers in the sequence of 3, 7, or 11 swing at 7361.91 – 7427.76 area for further upside. If pivot at 7302.7 low fails during later pullback, the Index would be still remain in the same cycle from 6/2 peak. Index should then extend the correction to the downside. We don’t like selling the Index.

FTSE 1 Hour Elliott Wave Chart

7 swings structure is one of the most common patterns in the theory of New Elliott Wave & it is also mainly know as double three Elliott Wave pattern. Market find that very often nowadays in many instruments in almost all time frames. It is a very reliable structure by which we can make a good analysis and what is more important is giving us good business inputs with clearly defined levels invalidation and destination areas.

The image below shows what Elliott wave pattern Double Three looks like. It has (W), (X), (Y) and 3,3,3 internal structure, which means that all these 3 legs are corrective sequences. Each (W), (X) and (Y) are made of three waves, which are having the structure W, X, Y in lesser degree as well. Elliott Wave principle is a form of technical analysis that traders use to analyze the cycles of financial markets and market trends forecast by identifying extremes in investor psychology, high and low prices, and other collective factors. Important to Note that 3 waves could also be labeled ABC (5-3-5) structure as well. How are labeled 3 waves it depends on the internal price structure subdivisions waves i.e. whether the price action is corrective or motive.

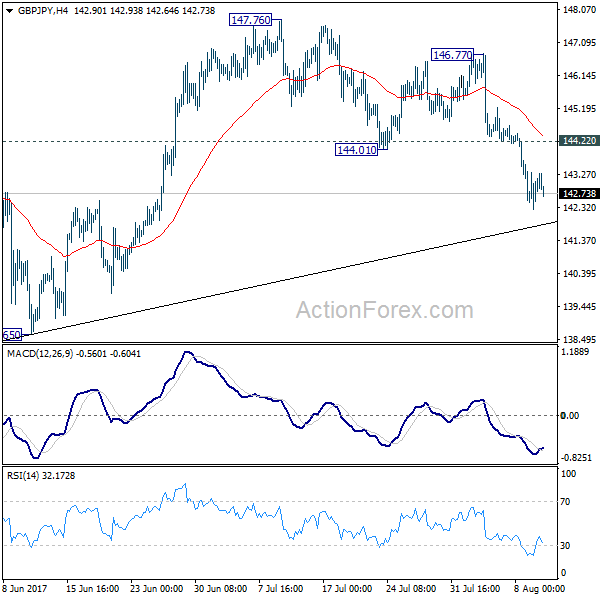

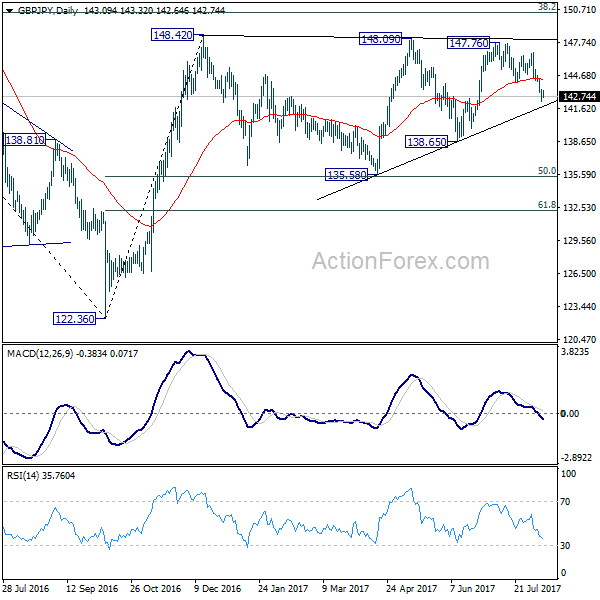

GBP/JPY Daily Outlook

Daily Pivots: (S1) 142.45; (P) 142.91; (R1) 143.55; More

GBP/JPY's fall from 147.76 is still in progress for trend line support (now at 141.87). Break there will target 135.58/138.65 support zone. As GBP/JPY is seen as staying in consolidation pattern from 148.42, we'd expect strong support from 135.58 to contain downside. On the upside, above 144.20 minor resistance will argue that the decline from 147.76 might be completed. In such case, intraday bias will be turned back to the upside for rebound.

In the bigger picture, rise from medium term bottom at 122.36 is expected to continue to 38.2% retracement of 196.85 to 122.36 at 150.43. Decisive break there will carry long term bullish implications and pave the way to 61.8% retracement at 167.78. In case the sideway pattern from 148.42 extends, we'd be looking for strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside.

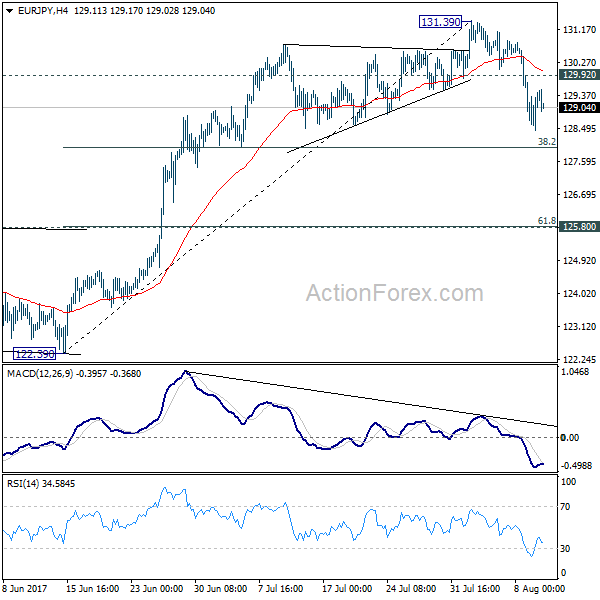

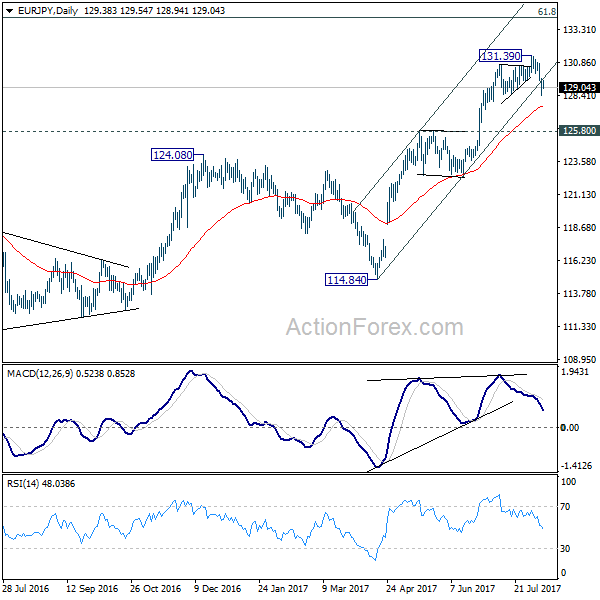

EUR/JPY Daily Outlook

Daily Pivots: (S1) 128.66; (P) 129.19; (R1) 129.95; More...

With 129.92 minor resistance intact, correction from 131.39 short term top could extend lower. At this point, we'd expect strong support from 38.2% retracement of 122.39 to 131.39 at 127.95 to contain downside and bring rebound. Above 129.92 will turn bias to the upside for retesting 131.39 first. Nonetheless, firm break of 127.95 will bring deeper decline to 125.80 resistance turned support before completing the correction.

In the bigger picture, the down trend from 149.76 (2014 high) is completed at 109.03 (2016 low). Current rally from 109.03 should be at the same degree as the fall from 149.76 to 109.03. Further rise is expected to 61.8% retracement of 149.76 to 109.03 at 134.20. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. Medium term outlook will remain bullish as long as 124.08 resistance turned support holds.

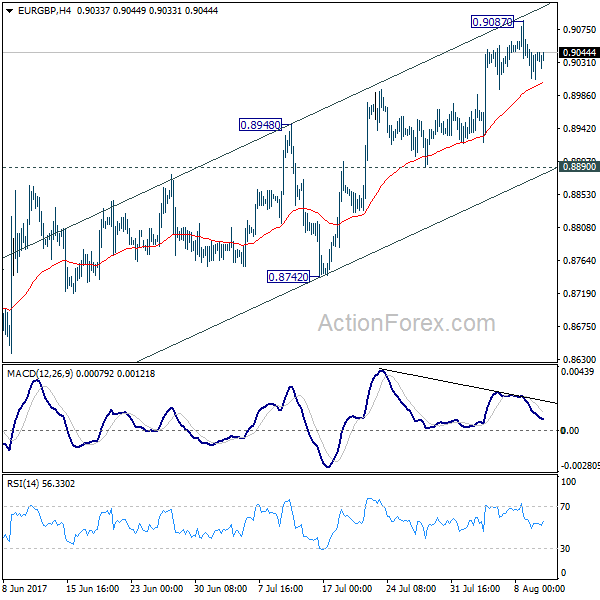

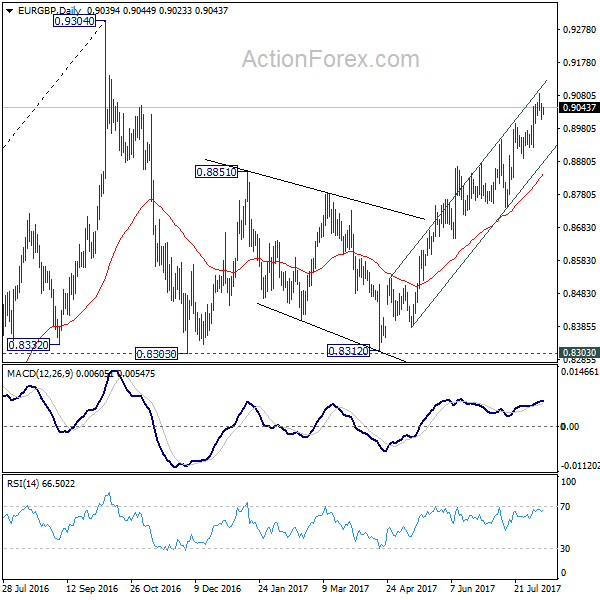

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.9015; (P) 0.9036; (R1) 0.9062; More

A temporary top is in place at 0.9087 in EUR/GBP and intraday bias is turned neutral first. Further rise is still expected as long as 0.8890 support holds. Above 0.9087 will extend the rebound from 0.8312 to 0.9304 key high. At this point, there is no clear sign of up trend resumption yet. Hence, we'll be cautious on strong resistance from 0.9304 to limit upside and bring another fall. On the downside, break of 0.8890 will be the first indication of near term reversal. In such case, intraday bias will be turned back to the downside for 0.8742 support for confirmation.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

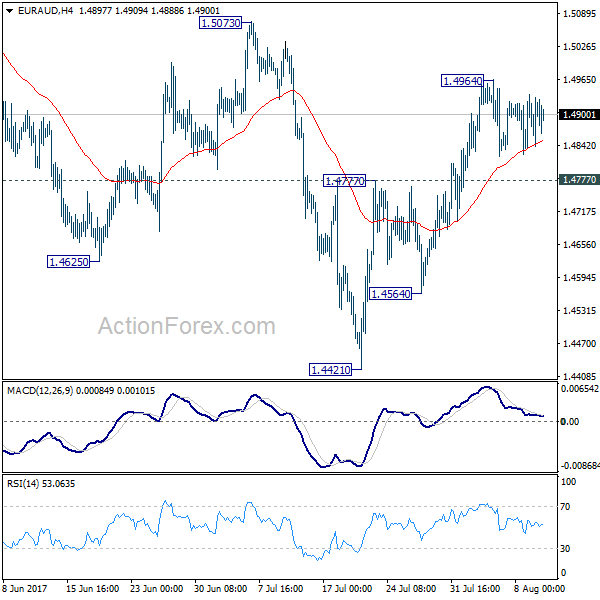

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4846; (P) 1.4891; (R1) 1.4948; More...

Intraday bias in EUR/AUD remains on neutral at this point. Near term outlook stays bullish with 1.4777 support intact and further rally is expected. As noted before, correction from 1.5226 should have completed with three waves down to 1.4421 already. Above 1.4964 will target 1.5073 resistance first. Break of 1.5073 will likely resume the rise from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4421 at 1.5411 next. However, firm break of 1.4777 will dampen this bullish view and turn bias to the downside for 1.4564 support. Break will extend the correction from 1.5226 through 1.4421.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to resume to retest 1.6587. The corrective structure of the fall from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, another decline will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

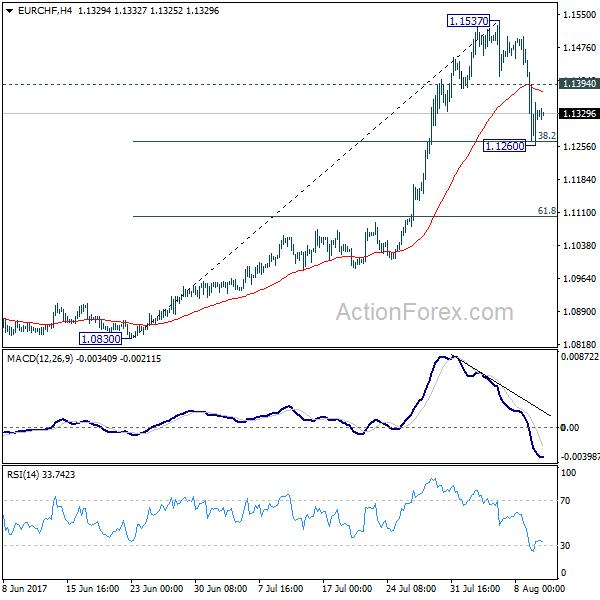

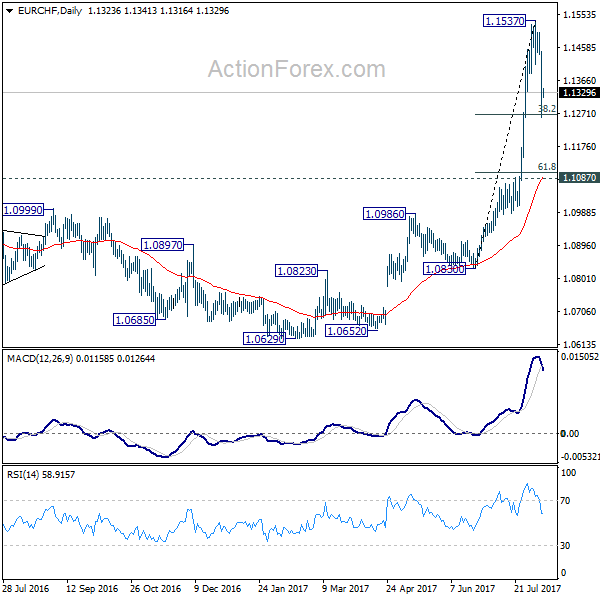

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1243; (P) 1.1345; (R1) 1.1429; More...

EUR/CHF's correction extended to as low as 1.1260 and draws support from 38.2% retracement of 1.0830 to 1.1537 at 1.1267 to recover. Intraday bias is turned neutral first. Break of 1.1394 will suggests that such pull back is completed and turn bias back to the upside for retesting 1.1537 first. However, firm break of 1.1267 will extend the fall and target 61.8% retracement at 1.1100.

In the bigger picture, firm break of 1.1198 key resistance confirms resumption of the long term rise from SNB spike low back in 2015. In this case, EUR/CHF would eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

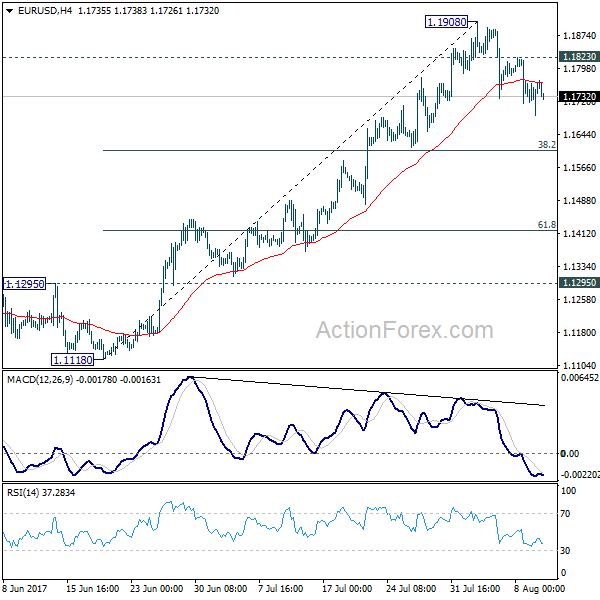

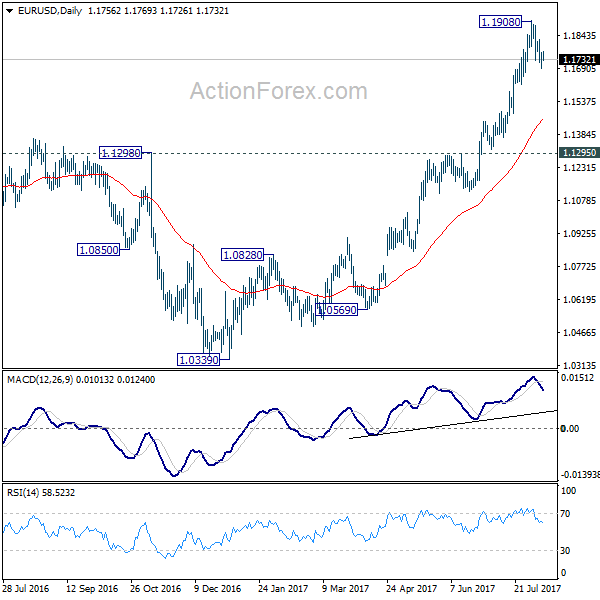

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1710; (P) 1.1736 (R1) 1.1784; More...

EUR/USD's pull back from 1.1908 is still in progress and intraday bias remains on the downside At this point, we'd expect strong support from 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring rebound. But break of 1.1908 is needed to confirm up trend resumption. Otherwise, more consolidation would be seen in near term. Meanwhile, sustained break of 1.1606 would bring deeper pull back to 61.8% retracement at 1.1420.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained break of 55 month EMA (now at 1.1760) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

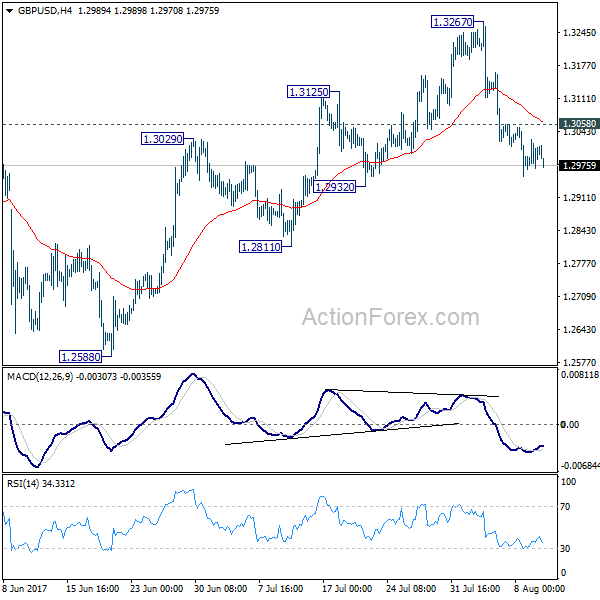

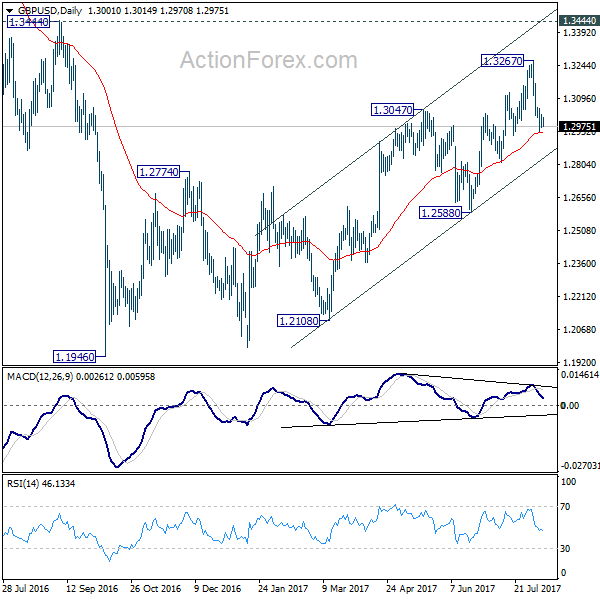

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2970; (P) 1.2998; (R1) 1.3030; More...

GBP/USD lost some downside momentum but there is no sign of bottoming yet. Intraday bias remains on the downside for 1.2932 support first. Price actions from 1.1946 are seen as a corrective pattern, no change is this view. Such correction could have completed at 1.3267 already. Break of 1.2932 will affirm this bearish case and target 1.2588 key near term support for confirmation. On the upside, however, above 1.3058 minor resistance will turn bias back to the upside for recovery first. But deeper fall is expected as long as 1.3267 resistance holds.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is expected, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

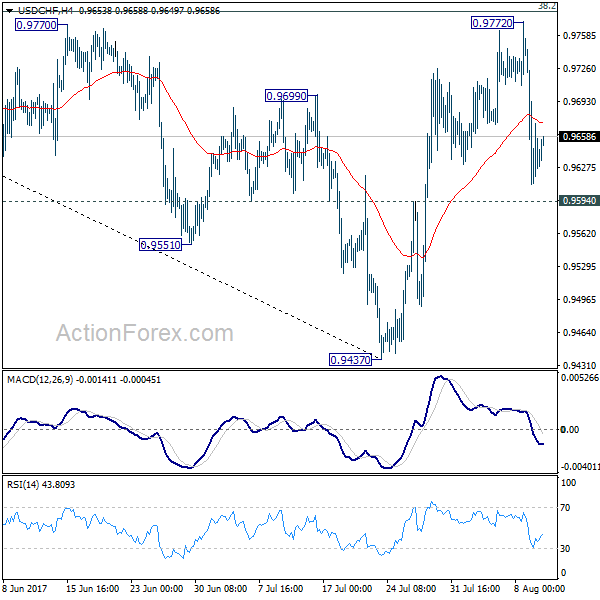

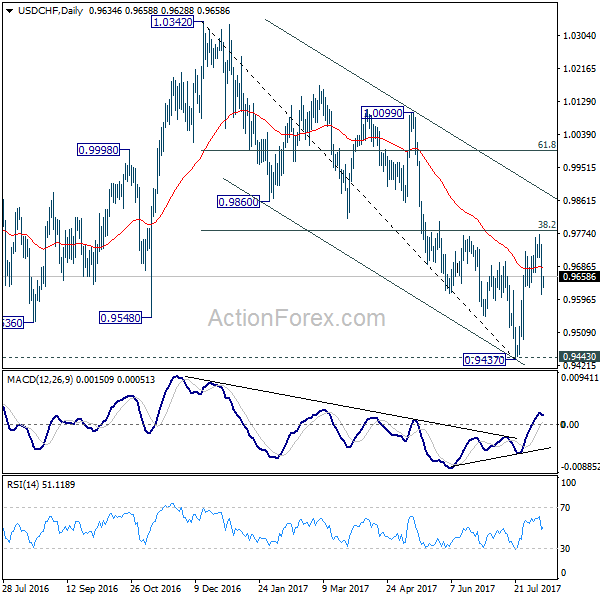

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9583; (P) 0.9663; (R1) 0.9716; More...

At this point, intraday bias in USD/CHF remains neutral. Outlook is a bit mixed as the pair is bounded inside medium term falling channel. The pair was also limited below 38.2% retracement of 1.0342 to 0.9437 at 0.9783. Firm break of 0.9594 will dampen our bullish view and turn bias back to the downside for 0.9437. This could also extend the fall through 1.0342 through 0.9437/43 key support level. On the upside, above 0.9772 will revive the bullish case of reversal and turn bias back to the upside.

In the bigger picture, current development argues that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rise. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996.