Sample Category Title

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.62; (P) 109.98; (R1) 110.42; More...

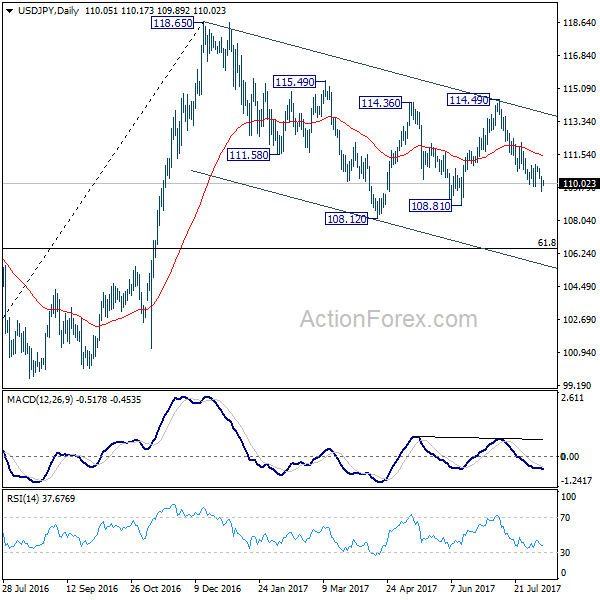

USD/JPY's fall from 114.49 is still in progress and intraday bias remains on the downside for 108.81 support. Break there will resume whole correction from 118.65 and target 61.8% retracement of 98.97 to 118.65 at 106.48. On the upside, break of 111.04 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2662; (P) 1.2692; (R1) 1.2724; More....

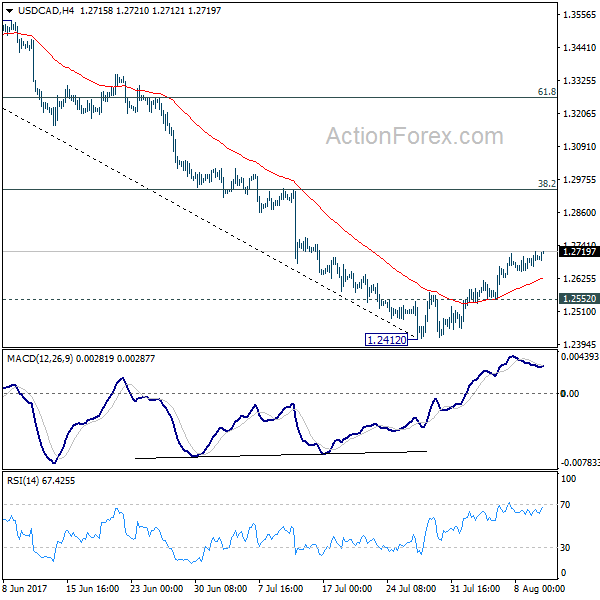

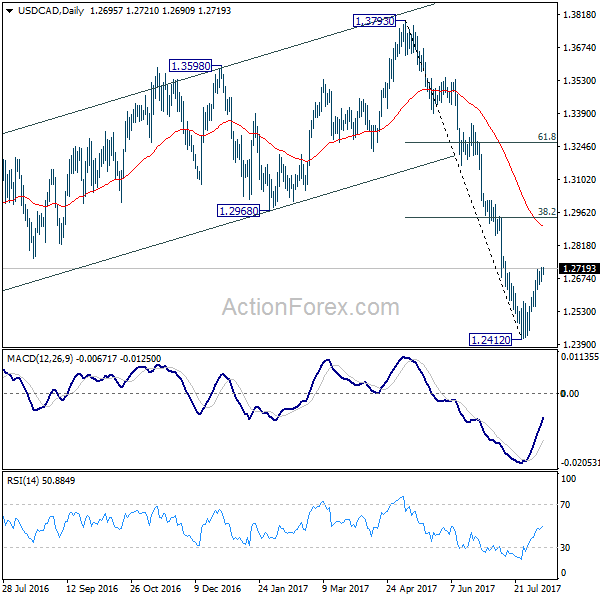

USD/CAD's rebound from 1.2412 short term bottom is still in progress. Intraday bias remains on the upside for 38.2% retracement of 1.3793 to 1.2412 at 1.2940. Considering the the pair is losing upside momentum, we'd expect upside to be limited by 1.2940 to complete the correction. On the downside, below 1.2552 minor support will turn bias back to the downside for retesting 1.2412 low first.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. A short term bottom is formed at 1.2412 after hitting 61.8% projection of 1.4689 to 1.2460 from 1.3793 at 1.2415. But there is no sign of completion of the correction yet. Break of 1.2412 will target 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. Meanwhile, sustained break of 1.2968, 38.2% retracement of 1.3793 to 1.2412 at 1.2940 will be the first sign of completion of the correction and will turn focus back to 1.3793 key resistance.

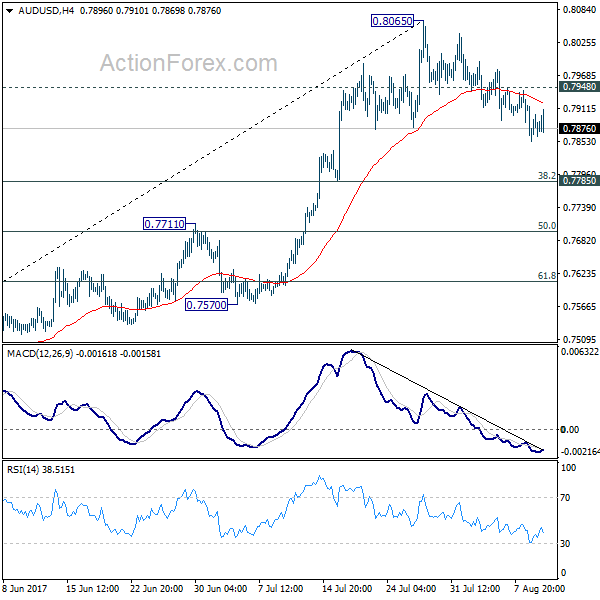

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7857; (P) 0.7885; (R1) 0.7916; More...

AUD/USD's pull back from 0.8065 is still in progress and intraday bias stays on the downside. Deeper fall would be seen to 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783). But we'd expect strong support there to bring rebound. Above 0.7948 minor resistance will turn bias back to the upside for retesting 0.8065. But decisive break there is needed to confirm rally resumption. Otherwise, we'd expect more consolidative trading in near term.

In the bigger picture, current development suggests that rebound from 0.6826 is developing into a medium term rise. There is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8100) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now expected.

Yen Firm as Risk Aversion Continues, RBNZ Stands Pat as Widely Expected

Risk aversion remains the main theme in the markets. Commodity currencies remain the weakest ones while Yen is staying firm. Dollar trades mildly higher but there is no follow through buying yet. RBNZ rate decision triggered a brief recovery in New Zealand Dollar but Kiwi is quickly back under pressure. Selloff in stocks seem to have stabilized though, with Nikkei hovering in tight range in red today, down around -0.15%. Gold is hovering between 1280/5 after yesterday's rally and is waiting for fresh inspiration. US-North Korea tension will remain the main focus today while data from UK and US will catch most attention.

RBNZ left OCR unchanged at 1.75% as widely expected

As expected, the RBNZ left the OCR unchanged at 1.75%. Governor Wheeler reiterated that the monetary policy would remain accommodative for some time. The staff projection continued to forecast the first rate hike to come in 2H19. They also revised lower the short term inflation outlook and intensified the warning that a lower currency is needed for growth. NZD/USD jumped to a 3-day high of 0.7371 after the announcement, but gains were erased afterwards. At the time of writing NZD/USD has already resumed recent fall from 0.7553 and reaches as low as 0.7298. More in RBNZ Left Policy Stance Unchanged, Heightened Warning Over NZD Strength.

Chicago Fed Evans: December hike is a subject for discussion

Chicago Fed President Charles Evans said that it's "quite reasonable" to start unwinding Fed's balance sheet in September even "with potentially temporary lower inflation data". Nonetheless, the matter of one more rate hike in December is a subject for discussion. He noted that if you thought that inflation was weaker and we needed more accommodation you could decide to put that off until later." He emphasized that the longer inflation stays below 2% target, "it creates a few more problems". And, "I'd like to see a little more evidence that we are actually getting to 2 percent sooner rather than later."

North Korea finalizing plan to strike Guam in mid-August

The tensions between US and North Korea continue to intensify. North Korea responded to US President Donald Trump's "fire and fury" warning and said that Trump "again let out a load of nonsense about 'fire and fury,' failing to grasp the on-going grave situation". And Pyongyang also said that "sound dialogue is not possible with such a guy bereft of reason and only absolute force can work on him." Meanwhile, North Korean also said that it's finalizing the plans for missile launches near Guam by mid-August.

On the other hand, it's reported that Trump didn't consult with Secretary of State Rex Tillerson before making his "fire and fury" warning. White House press secretary Sarah Huckabee Sanders said that the national security team was "well aware of the tone of the statement of the president prior to the delivery". But the words that Trump used "were his own".

Elsewhere

Japan machine orders dropped -1.9% mom in June while domestic CGPI rose 2.6% yoy in July. Australia inflation expectation slowed to 4.2% in August. UK RICS house price balance dropped to 1 in July.

UK data are the main focuses in European session. Industrial production, manufacturing production, construction output and trade balance will be released. From US jobless claims, PPI will be featured. Canada will release new housing price index.

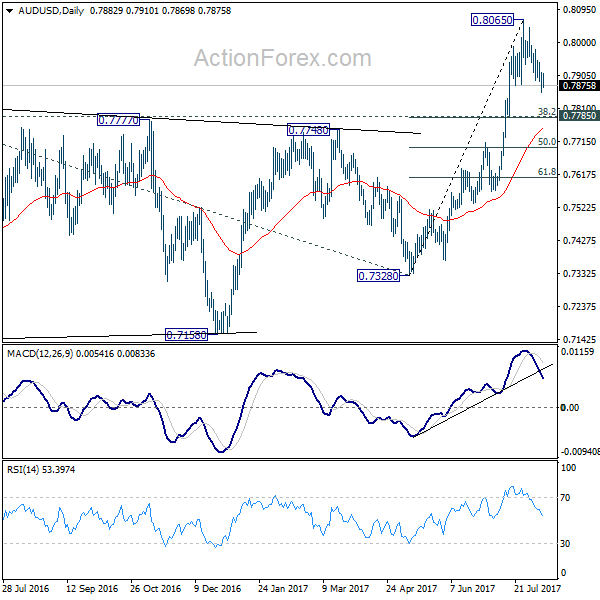

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7857; (P) 0.7885; (R1) 0.7916; More...

AUD/USD's pull back from 0.8065 is still in progress and intraday bias stays on the downside. Deeper fall would be seen to 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783). But we'd expect strong support there to bring rebound. Above 0.7948 minor resistance will turn bias back to the upside for retesting 0.8065. But decisive break there is needed to confirm rally resumption. Otherwise, we'd expect more consolidative trading in near term.

In the bigger picture, current development suggests that rebound from 0.6826 is developing into a medium term rise. There is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8100) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now expected.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% | 1.75% | |

| 23:01 | GBP | RICS House Price Balance Jul | 1% | 9% | 7% | |

| 23:50 | JPY | Machine Orders M/M Jun | -1.90% | 3.70% | -3.60% | |

| 23:50 | JPY | Domestic CGPI Y/Y Jul | 2.60% | 2.30% | 2.10% | 2.20% |

| 1:00 | AUD | Consumer Inflation Expectation Aug | 4.20% | 4.40% | ||

| 4:30 | JPY | Tertiary Industry Index M/M Jun | 0.20% | -0.10% | ||

| 8:30 | GBP | Industrial Production M/M Jun | 0.10% | -0.10% | ||

| 8:30 | GBP | Industrial Production Y/Y Jun | -0.10% | -0.20% | ||

| 8:30 | GBP | Manufacturing Production M/M Jun | 0.00% | -0.20% | ||

| 8:30 | GBP | Manufacturing Production Y/Y Jun | 0.70% | 0.40% | ||

| 8:30 | GBP | Construction Output M/M Jun | 1.20% | -1.20% | ||

| 8:30 | GBP | Visible Trade Balance (GBP) Jun | -11.0B | -11.9B | ||

| 12:00 | GBP | NIESR GDP Estimate Jul | 0.30% | 0.30% | ||

| 12:30 | CAD | New Housing Price Index M/M Jun | 0.50% | 0.70% | ||

| 12:30 | USD | Initial Jobless Claims (AUG 05) | 240K | 240K | ||

| 12:30 | USD | PPI M/M Jul | 0.10% | 0.10% | ||

| 12:30 | USD | PPI Y/Y Jul | 2.20% | 2.00% | ||

| 12:30 | USD | PPI Core M/M Jul | 0.20% | 0.10% | ||

| 12:30 | USD | PPI Core Y/Y Jul | 2.10% | 1.90% | ||

| 14:30 | USD | Natural Gas Storage | 20B | |||

| 18:00 | USD | Monthly Budget Statement Jul | -55.5B | -90.2B |

Market Morning Briefing: Pound Has Barely Moved In The Last Session

STOCKS

Dow (22048.70, -0.17%) tested immediate resistance near 22200 and while that holds, we could possibly expect a dip towards 22000-21800 levels in the near term.

Dax (12154.00, -1.12%) could be headed towards 12100-12000 levels soon. For now the index seems to be in a sideways consolidation mode and could trade within 12000-12400 region in the medium term.

Shanghai (3265.98, -0.29%) has some chances of coming off towards 3240 in the near term. Trade within 3240-3300 region is likely to be seen in the next few sessions.

Nikkei (19736.72, -0.01%) could test support zone of 19600-19400/50 in the coming sessions. Near term looks bearish.

Nifty (9908.05, -0.71%) has some scope of testing levels near 9800 in the coming sessions from where a bounce looks likely. A break below 9800, if seen could take it higher towards 9700 in the medium term. For now the index is in a corrective mode.

COMMODITIES

Gold (1276.42) has risen in line with our expectations but needs a break above the immediate resistance of 1285 to continue the rally towards 1300. Failure to rise above 1285 may push it back to 1250 but at this point but at this point, the uptrend remains strong.

Silver (16.89) has reached the higher end of the range of 16.00-17.00 and in case, it breaks above the resistance of 17.00, it may extend the rally to 17.75 negating the preferred view of sideways trade in the range of 16.00-17.00.

Copper (2.93) has been taking pause for the last 2 sessions but the trend remains firmly up and the target of 3.00 and the support of 3.12 remain unchanged.

The bullish stance for Brent (52.70) and WTI (49.55) has paid off so far but now Brent needs a break above the immediate resistance of 53.00 and WTI, above 50.50 to extend their respective rally to 56 and 54.

FOREX

Decreasing chances of any imminent military confrontation between US and North Korea have cooled off the geopolitical tensions and checked the strength in safe havens like Yen (110.07). Dollar Yen has seen a sharp bounce from our support of 109.50 and a break above 110.20 may push it to 111.00 or even higher in the next few sessions.

Dollar Index (93.60) hit a high of 93.89, close to the major resistance of 94.10-40 before retreating a bit. The resistance of 94.10-40 may be tested but it is expected to hold and limit any further advance of Dollar as the larger trend remains down yet.

Euro (1.1743) shows no change from its corrective behavior yet and upside possibilities can be considered only on a break above 1.1800-25. Till then, the downside risk for 1.1600 remains greater.

Pound (1.2998) has barely moved in the last session. View remains unchanged. Repeat - a corrective bounce from 1.2950-30 can’t be ruled out but the larger downtrend may drive it down to 1.2850 levels in the coming days.

Aussie (0.7879) remains in a near term corrective phase and needs a rise above 0.7950 to resume the larger uptrend. Failure to rise above 0.7950 by the end of the week may push it down to the support of 0.7835-20 or even 0.7760-50.

Dollar Rupee (63.84) is trading at 63.95 in the NDF. If the onshore market reflects the same rate, then the pair may enter the major resistance band of 63.90-64.10 where the Dollar sellers may return.

INTEREST RATES

The German-Japan 10YR yield spread (0.37%) has fallen below 0.40% and if it continues to remain lower, we could see a sharp fall in EUR/JPY (129.16) in the near term. Overall the yield spread looks bearish for the coming sessions.

The German-US 10YR (-1.81%) has bounced back from just above support levels and while that holds, it could rise again towards -1.75% pulling back Euro to higher levels.

(RBNZ) Official Cash Rate Unchanged at 1.75 percent

The Reserve Bank today left the Official Cash Rate (OCR) unchanged at 1.75 percent.

Global economic growth has become more broad-based in recent quarters. However, inflation and wage outcomes remain subdued across the advanced economies, and challenges remain with on-going surplus capacity. Bond yields are low, credit spreads have narrowed and equity prices are at record levels. Monetary policy is expected to remain stimulatory in the advanced economies, but less so going forward.

The trade-weighted exchange rate has increased since the May Statement, partly in response to a weaker US dollar. A lower New Zealand dollar is needed to increase tradables inflation and help deliver more balanced growth.

GDP in the March quarter was lower than expected, adding to the softening in growth observed at the end of 2016. Growth is expected to improve going forward, supported by accommodative monetary policy, strong population growth, an elevated terms of trade, and the fiscal stimulus outlined in Budget 2017.

House price inflation continues to moderate due to loan-to-value ratio restrictions, affordability constraints, and a tightening in credit conditions. This moderation is expected to persist, although there remains a risk of resurgence in prices given continued strong population growth and resource constraints in the construction sector.

Annual CPI inflation eased in the June quarter, but remains within the target range. Headline inflation is likely to decline in coming quarters as the effects of higher fuel and food prices dissipate. The outlook for tradables inflation remains weak. Non-tradables inflation remains moderate but is expected to increase gradually as capacity pressure increases, bringing headline inflation to the midpoint of the target range over the medium term. Longer-term inflation expectations remain well anchored at around 2 percent.

Monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly.

RBNZ Left Policy Stance Unchanged, Heightened Warning Over NZD Strength

As expected, the RBNZ left the OCR unchanged at 1.75%. Governor Wheeler reiterated that the monetary policy would remain accommodative for some time. The staff projection continued to forecast the first rate hike to come in 2H19. They also revised lower the short term inflation outlook and intensified the warning that a lower currency is needed for growth. NZDUSD jumped to a 3-day high of 0.7371 after the announcement, but gains were erased afterwards.

The central bank's monetary policy stance remained neutral. As noted in the accompanying statement, 'monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly'. It continued to project the first rate hike to come in the second half of 2019, unchanged from the assessment in May.

On the macroeconomic developments, RBNZ acknowledged that recent GDP growth came in weaker than expected, while housing prices moderated and inflation softened. Yet, it affirmed growth would pick up, thanks to growing population, elevated terms of trade and fiscal stimulus. It forecast growth to stay above 3% in coming years. Policymakers noted that the 'outlook for tradable inflation remains weak', while 'non-tradables inflation remains moderate but is expected to increase gradually as capacity pressure increases, bringing headline inflation to the midpoint of the target range over the medium term. The central bank's longer-term inflation expectations stayed at around 2%.

There is a tweak in the currency reference, where the RBNZ suggested that 'a lower New Zealand dollar is needed to increase tradables inflation and help deliver more balanced growth'. Previously, the central bank noted that a drop in New Zealand dollar would 'help to rebalance the growth outlook towards the tradables sector'.

Euro Dollar Remains Weak Despite Small Gain

Key Points:

- Price action manages to stage a small rise despite plenty of selling pressure.

- RSI Oscillator continues to trend lower away from over bought territory.

- A further correction lower likely in the coming session.

The Euro managed to find a modicum of support during today's session as the pair despite the very evident ongoing selling pressure. The pair was initially pushed to a low of 1.1687 but managed to claw its way back to trade around the 1.1757 mark following the release of a relatively poor U.S. Labour Cost Index of 0.6%, as well as ongoing risk in North Korea. However, given that price penetrated support at 1.1700 the downside is likely beckoning in the coming session.

In fact, a cursory review of the pair's charts tells us that the coming days could be a little rough for the Euro. Price action has now dipped below the 12EMA and remains fixated on the 1.1700 support zone. Additionally, the RSI Oscillator continues to trend lower, away from overbought territory, signalling that there is still some distance to go before the downside momentum ebbs.

Subsequently, the intra-day bias still remains on the downside, despite the small gain, and the present technical structure supports a target at 1.1606 (38.2% retracement level from 1.1119 to .1908). Once price action reaches that level, expect a rebound to be likely given the renewed focus on the 1.20 level for the pair.

However, the bigger picture still calls for more gains when taking the longer term view with bullish convergence still evident on the weekly charts. In fact, a concerted break of the 55 monthly EMA at 1.1760 could suggest valuations for the pair well above the 1.20 handle which would see the Euro trading in a zone last observed in 2014.

Regardless, our initial bias remains on the downside in the coming session given that the 1.1813 resistance level remains intact. Subsequently, the technical factors argue for further corrective declines with a downside target at 1.1606 likely to be achieved. However, do not expect a sustained break of that level as fundamentals currently argue against it.

Finally, from a fundamental perspective, monitor the U.S. Initial Jobless Claims numbers because they could be a relatively important window into the current health of the economy. A current broad consensus view puts the result at 240k, a slight fall from the prior result of 245k, but watch for any variations. The PPI data is also due for release and could also impact the pair, albeit to a lesser extent.

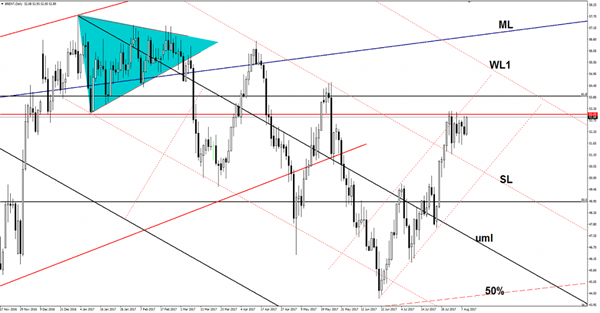

GBP/JPY Downside Paused

GBP/USD downside momentum was stopped right above a crucial support level. Has turned to the upside and is very close to reach and retest the median line (ml) of the minor descending pitchfork. Will drop further if the resistance will hold and will reject the price.

A major drop will come if will take out the dynamic support from the red uptrend line, while another leg higher will appear after the breakout above the median line and after a retest of the uptrend line.

Bent Oil: Breakout Attempt

Price rallied on Wednesday again and looks determined to resume the upside movement, but needs to take out a major static resistance to do that. Is consolidation on the short term and tries to recapture more directional energy before will try to climb towards fresh new highs.

Brent jumped higher as the United States Crude Oil Inventories have dropped unexpectedly lower in the previous week, were reported at -6.5 million barrels, much lower versus the -2.6M estimated and compared to the -1.5M in the former reading period.

Only a valid breakout above the 53.03 will confirm a further increase, another rejection will bring attract the sellers again.